Month: November 2018

588 articlesCA, CS, CMA

CA, CS, CMA

Framework Governing Internal Audits

CA, CS, CMA

CA, CS, CMA

Preface to the Framework and Standards on Internal Audit

Goods and Services Tax

Goods and Services Tax

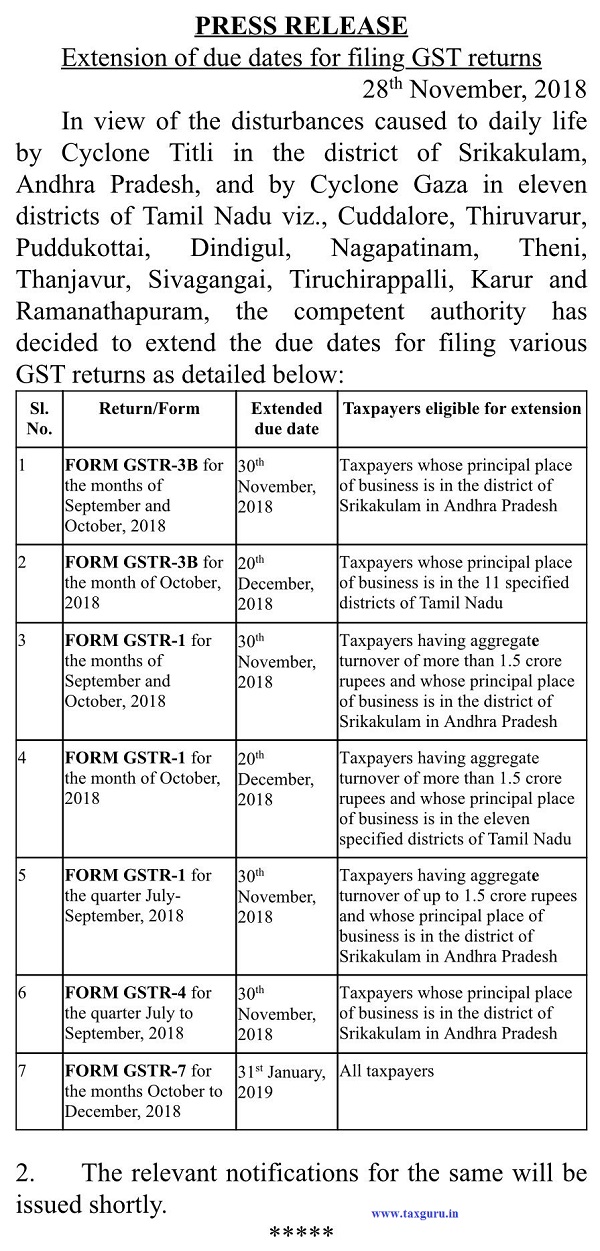

Extension of due dates for filing GST returns for districts affected by Cyclone Titli & Gaza

Income Tax

Income Tax

CBDT directives on scope of inquiry in cases selected for Limited Scrutiny

Income Tax

Income Tax

Taxation of leave Encashment

Goods and Services Tax

Goods and Services Tax

Deputation of Employee’s – Whether A Supply or Cost Sharing ?

Income Tax

Income Tax

Deduction U/s. 80P to cooperative society on Interest earned on FDs and saving bank deposit

Income Tax

Income Tax

Notice u/s 143(2) issued by AO before return filing has no meaning

Income Tax

Income Tax

ITAT order cannot be termed erroneous for negligence of Dept

Income Tax

Income Tax