Month: April 2018

709 articlesGoods and Services Tax

Goods and Services Tax

An Insight into Taxability of Free Samples under GST

Corporate Law

Corporate Law

IBBI Debars an IP from practicing as Insolvency Professional for 90 days

Goods and Services Tax

Goods and Services Tax

A Comprehensive understanding of Job Work provisions Under GST

Income Tax

Income Tax

TDS U/s. 194C not deductible on Reimbursement of haulage charges paid by C & F agents

Goods and Services Tax

Goods and Services Tax

10 Major changes for GST composition dealer

Goods and Services Tax

Goods and Services Tax

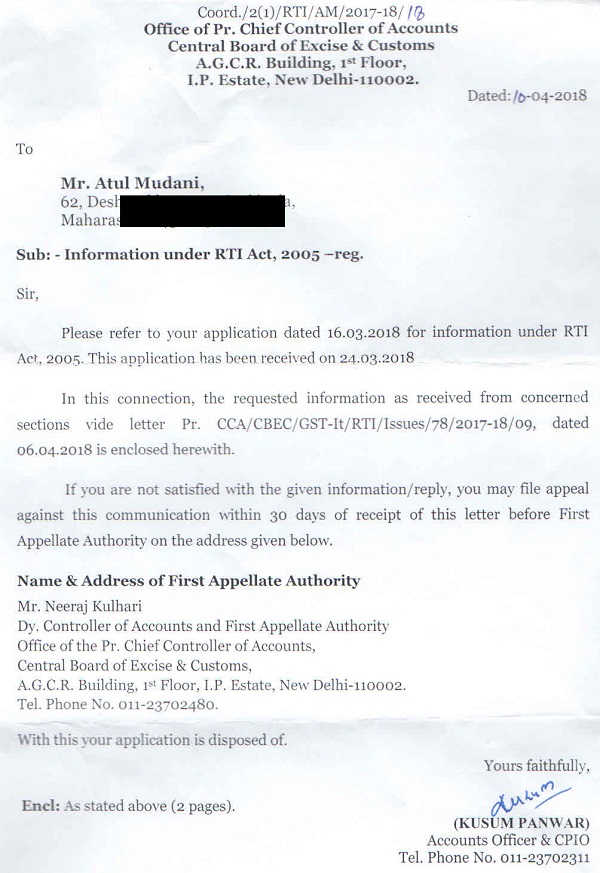

RTI reveals collection of Rs 900 Crores as GST Late Fees

Goods and Services Tax

Goods and Services Tax

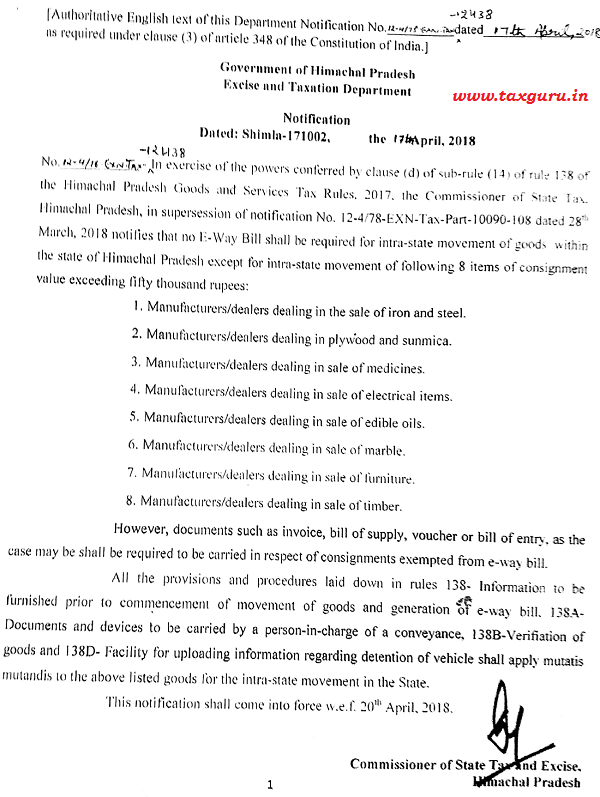

Tripura and Himachal to roll out intra-state e-way bill on Apr 20

Goods and Services Tax

Goods and Services Tax

What are pre-requisites to generate e-way bill?

Income Tax

Income Tax

Major changes in Income Tax For FY 2017-18 & 2018-19 for SME

Goods and Services Tax

Goods and Services Tax