CA Aasmee Mangla

It’s been a while now since the amendment has come on Reverse Charge Liability on Rent a Cab Service. But, the Finance Departments of the Big Corporates are still facing hardship in calculating the correct amount of Reverse Charge Liability they need to deposit with the Service Tax Department, especially when they receive diversified invoices from Rent a Cab Service Providers.

It is seen that due to little acquaintance with law, Rent a Cab Service Receivers are bluntly charging service tax on 50% of the invoice value, thereby causing working capital loss as well as wrong compliance of law.

Before taking deeper dive into the area of turmoil which may crop up pursuant to stated amendment, it is apposite here to have an overview of the amendment brought on Rent a Cab Service w.e.f. from 1st October’2014.

RCM on Rent a Cab Service is governed by 2 Notifications-26/2012 and 30/2012. In regard to N.No. 26/2012 (Abatement Notification), there has been no change, i.e. even after 1st Oct’2014, abatement available on Rent a Cab service is 60% only and therefore taxable portion is 40% as depicted below;

| 9 | RENTING OF MOTOR CAB | 40 |

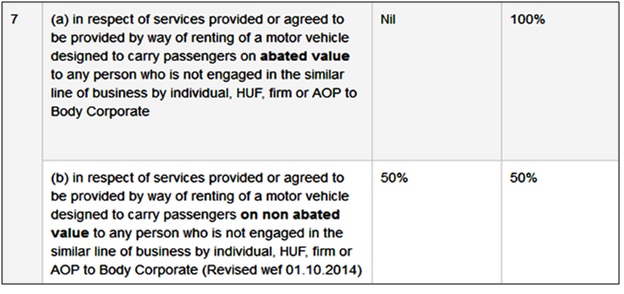

However, RCM Notification has been amended w.e.f. 1st Oct’2014 and post amendment scenario is depicted hereunder;

It is pivotal to highlight here that in case of Reverse Charge Liability, there can be following two situations;

Abatement of 60% claimed by Service Provider- In such cases, 100% liability of Service Tax is on Service Recipient and therefore no Service Tax will be charged on the Invoice by the Service Provider. Henceforth, Service Tax has to be deposited with the department by Service Recipient @ 14.5% on 40% of the Invoice value.

Abatement of 60% not claimed by Service Provider- This case arises when Service Provider wishes to claim CENVAT Credit on Input Services taken by him and thereby foregoes the benefit of Abatement. In these cases, there arises 50-50 liability of Service Tax on both Service Provider and Receiver. Therefore, 7.25% of ST will be charged by Rent a Cab Provider on the invoice and other 7.25% has to be deposited with the department by Service Recipient from his pocket.

To sum up, if the compliance of law at the end of Service Provider is correct, then only two following situations can arise at the end of Service Recipient;

However, problem arises when the invoice received in respect of rent a cab service taken contains Service tax amounts at different rates from what stated above. Following two situations arises when Service Provider charges Service Tax at wrong rate on the invoice;

It is hoped that after reading this article, there remains no confusion in the minds of Business Entities receiving Rent a Cab Services in respect of Reverse Charge Liability they need to discharge.

Sir, if i go on official tour by hiring Taxi from Market and RCM or any ??????

Hii

Our cab vendor is not mentioning service tax registration number on the invoice and we don’t know whether he registered to service tax dept. or not.

now should we discharge 50% liability of Service tax under RCM

Under rent a cab operator service RCM rule

Bill Value of service provider (Rs.113700/-) inclusive of 15% ST. Basic Value of bill Rs.98870/- ST = 6921 SBC 247 KKC 247 Is it ok or not –

Any body can suggest me

Bill Value of service provider (Rs.113700/-) inclusive of 15% ST.

Basic Value of bill Rs.98870/-

ST = 6921

SBC 247

KKC 247

Is it ok or not

Hi

I m receiving an Invoice for renting a cab from diff vendor with ST of 6% i.e 40%

do i need to pay RCM of Rs. 60% it is mandatory to pay?

hi, we provide ‘renting of motor cab’ service. we availed cenvat credit on capital goods i.e. on purchase of cabs. at that time we paid service tax at full rate, i.e. without availing abatement. now we want to avail the benefit of abatement. do we have to reverse the canvat credit taken on capital goods as we are still using same cabs on which credit has been taken in previous years.

Hi Aasmee

I would like to seek to ask that the abatement has been a bit modified through notification 08/2014 bringing thereby the word ‘motor cab’ in place of ‘motor vehicle’ earlier. Won’t this restrict the scope of abatement. Further, in reverse charge the expression is ‘motor vehicle’ only (Though notification 10/2014 is in relation to this only but it amends the rate of tax payable by provider & receiver, keeping the descripttion intact). If you may please elaborate upon this inconsistency between the provisions of abatement & RCM, the scope of both when we are to assess about hiring of bus. – See more at: https://taxguru.in/service-tax/service-tax-reverse-charge-mechanism-renting-motor-vehicle-designed-carry-passengers.html#comment-1947288I would seek to ask that the abatement has been a bit modified through notification 08/2014 bringing thereby the word ‘motor cab’ in place of ‘motor vehicle’ earlier. Won’t this restrict the scope of abatement. Further, in reverse charge the expression is ‘motor vehicle’ only (Though notification 10/2014 is in relation to this only but it amends the rate of tax payable by provider & receiver, keeping the descripttion intact). If you may please elaborate upon this inconsistency between the provisions of abatement & RCM, the scope of both when we are to assess about hiring of bus.

Q1) If cab operator applying a service tax tax @6%, is it right?

Q2) what shall be the liability of service recipient in this case?

Hi Aasmee. That was of really a great help!! i had a couple of questions and wanted you to help me on it.

1) Car provided on rent on SELF DRIVE basis, does this service fall under the meaning of RENT A CAB SERVICE?

2) If yes, for example a company is taking car on rent and then lets it out to the customer. Now the company has two liabilities, one for the Car taken on rent under RCM and the other one as service provider. Now, assuming that the service provider is a SSP, he does not charge any service tax on the bill. Now the company wants to follow method 2 as explained by you above, i.e. charge service tax on non-abated value @ 7.50% (i.e.) 50% of the Service Amount? Is this method acceptable considering the fact that Service Tax on the other 50% will not be paid by the service provider on the ground that he is a SSP

3) Also, when the cars are allowed on rent without fuel, can the abatement of 60% be availed?

Dear Sir,

if Provider exempt form Service tax (10 Lakh turnover), than we Can deposit service tax 40% on invoice value,

Whether the receiver of rent of cab services can avail cenvat credit… under both the situation i.e. with and without abated values.

which exemption notification is applicable for rent a cab operator. While filling the service tax return form its asking. Thanks in advance

Hi Aasmee,

Thanks for the nicely explained article. I needed couple of clarifications on this:

1) When service provider doesn’t charge Service Tax on invoice (probably due to reason being he is small service provider), then also we should deposit service tax @ 5.8% under RCM?

2) Judging that Service Provider has availed abatement or not on the basis of his invoice: will this practice stand good during Service Tax Audit? Won’t they will ask for more concrete evidence like some declaration from service provider?

Thanks in anticipation.

Dear Mentor – Please suggest what should be the effective rate of service tax for service receiver in case service provider is individual and not charges any service tax because he has not taken any registration in service tax.

good article. Thank you.