Securities and Exchange Board of India

Consultation Paper on Holding of Sponsor in Real Estate Investment Trust (REITs) and Infrastructure Investment Trust (InvITs)

Feb 23, 2023 | Reports : Reports for Public Comments

I. Objective

1. The consultation paper seeks to solicit public comments on the proposal to review norms with respect to Sponsor(s) of Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InvITs) in order to ensure alignment of interest between the Sponsors and unit holders.

II. Background

2. SEBI (Real Estate Investment Trusts) Regulations, 2014 (‘REIT Regulations’) and SEBI (Infrastructure Investment Trusts) Regulations, 2014 (‘InvIT Regulations’) defines “Sponsor” as a person who set(s) up the REIT/InvIT and is designated as such at the time of application for registration. Further REIT Regulations and InvIT Regulations defines “Manager” and “Investment Manager” (‘IM’) as a person who manages the assets and investments of the REIT and InvIT respectively and undertakes activities of the REIT and InvIT as per SEBI Regulations.

3. The Sponsor is responsible for setting up of the REIT/InvIT and the formation transaction. The Sponsor plays a key role in the context of the registration of the REIT or InvIT as registration is inter alia granted based on the eligibility conditions fulfilled by the Sponsor. The Sponsor monetizes its assets by transferring its real estate assets or infrastructure projects in the REIT/InvIT and funds are raised from public or by private placement for such acquisition and the listed units are offered to the unit holders. The underlying assets of REITs/InvITs are long term assets and require active management. The key decisions regarding management of the assets keep impacting the unit holders and their return on their investment.

4. REIT Regulations and InvIT Regulations mandate the Sponsor to mandatorily hold certain percentage of units of REIT/InvIT for a period of three years in order to ensure alignment of interest between the Sponsor and the unit holders. As per the data, most of the Sponsor(s) have significant shareholding in Manager/Investment Manager of REIT/InvIT which gives them right to appoint directors on the Board of Manager/Investment Manager. By virtue of the shareholding in the Manager/Investment Manager, the Sponsor controls the Manager/Investment Manager and has a say in the financing related decisions of the REIT/InvIT especially debt financing. Further, REITs/InvITs are permitted to raise debt amounting up to 49% and 70% of the value of the assets of REIT/InvIT respectively, where the maturities whether of initial debt or debt raised post initial offer usually exceeds 10 years, in most of the cases. It is also observed that acquisition of assets is from Sponsor(s) or its associates.

5. As the REIT/InvIT industry is in a nascent stage and continuously evolving, there is a need to have at least one Sponsor throughout the life of the REIT/InvIT. It is considered that the Sponsor needs to hold certain percentage of units on a perpetual basis in order to ensure that there is alignment of interest between the Sponsor and the unitholder and taking into account the fact that the assets of the REIT/InvIT are leveraged and are of long term nature.

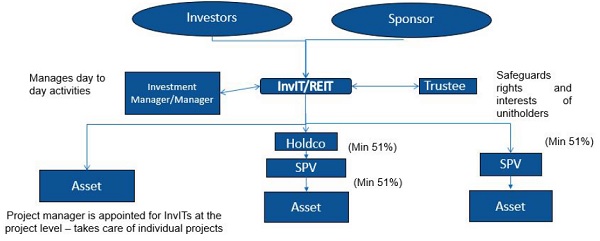

6. The structure of REIT/InvIT is as follows:

7. As on date, there are 5 REITs and 19 InvITs registered with SEBI, of which 3 REITs and 15 InvITs have raised funds through initial offer and/or further offer.

8. The details of fund raising through Initial Offer and Further Offer of units as on December 31, 2022 is as follows:

|

Table 1 |

|||||

| S.No. | Name of Entity | Structure | (In INR crores) | ||

| Initial offer |

Further offer |

Total | |||

|

InvITs |

|||||

| 1. | IRB INVIT Fund | Public listed | 5,033 | – | 5,033 |

| 2. | India Grid Trust | Public listed | 2,250 | 3798 | 6,048 |

| 3. | Powergrid Infrastructure Investment Trust |

Public listed | 7,735 | – | 7,735 |

| 4. | Indinfravit Trust | Privately placed listed | 3,145 | 2924 | 6,069 |

| 5. | India Infrastructure Trust | Privately placed listed | 952 | – | 952 |

| 6. | Oriental Infra Trust | Privately placed listed | 2,306 | – | 2,306 |

| 7. | Data Infrastructure Trust | Privately placed listed | 25,215 | 900 | 26,115 |

| 8. | Digital Fibre Infrastructure Trust | Privately placed unlisted | 14,706 | 4,788 | 19,495 |

| 9. | IRB Infrastructure Trust | Privately placed unlisted | 3,753 | 1,134 | 4,887 |

| 0. | Indian Highway Concessions Trust | Privately placed unlisted | 910 | 2,612 | 3,521 |

| 1. | National Highways Infra Trust | Privately placed listed | 5,910 | 1,430 | 7,340 |

| 2. | SHREM InvIT | Privately placed listed | 600 | – | 600 |

| 3. | Virescent Renewable Energy Trust | Privately placed listed | 460 | – | 460 |

| 4. | Highways Infrastructure Trust | Privately placed listed | 416 | – | 416 |

| 5. | Anzen India Energy Yield Plus Trust | Privately placed listed | 750 | – | 750 |

| InvIT Total | 74,141 | 17,586 | 91,727 | ||

|

REITs |

|||||

| 1. | Embassy Office Parks REIT | Public listed | 4,750 | 6,000 | 10,750 |

| 2. | Mindspace Business Park REIT000 |

Public listed | 4,500 | 0 | 4,500 |

| 3. | Brookfield India Real Estate Trust | Public listed | 3,800 | 950 | 4,750 |

| REIT Total | 13,050 | 6,950 | 20,000 | ||

9. REIT and InvIT Regulations mandate Sponsor to hold certain percentage of units of REIT/InvIT for a period of three years in order to ensure alignment of interest between the Sponsor and the unit holders. However, there is no requirement for Sponsor to hold units post the time period of three years post listing of units of REIT/InvIT.

10. As per InvIT Regulations, w. e. f. September 26, 2014,

10.1. The Sponsor(s) of the InvIT, together, to hold not less than 25% of the total units of the InvIT for a period of not less than 3 years from the date of listing of units issued on initial offer. After three years, there was no mandatory unit holding requirement for Sponsor of an InvIT.

11. Post amendment of InvIT Regulations dated November 30, 2016,

11.1. The Sponsor(s) of the InvIT, together, to hold not less than 15% (subject to certain conditions) of the total units of the InvIT for a period of not less than 3 years from the date of listing of units issued on initial offer. After three years, there is no mandatory unit holding requirement for Sponsor of an InvIT.

12. As per REIT Regulations, w. e. f. September 26, 2014,

12.1. REIT Regulations required Sponsor(s) and Sponsor group(s) to collectively hold minimum 25% of the total units of the REIT for a period of at least three years from the date of listing of units issued on initial offer. After three years, Sponsor(s) and Sponsor group(s) were required to hold at least 15% of the outstanding units (with each Sponsor holding not less than 5%) at all times.

13. Post amendment of REIT Regulations dated June 16, 2020

13.1. REIT Regulations required Sponsor(s) and Sponsor group(s) to collectively hold minimum 25% of the total units of the REIT for a period of at least three years from the date of listing of units issued on initial offer. After three years, there is no mandatory unit holding requirement for Sponsor(s) and Sponsor group(s) of a REIT.

14. Post amendment of REIT Regulations dated November 09, 2022 in order to align with InvIT Regulations,

14.1. REIT Regulations required Sponsor(s) and Sponsor group(s) to collectively hold minimum 15% of the total units of the REIT for a period of at least three years from the date of listing of units issued on initial offer. After three years, there is no mandatory unit holding requirement for Sponsor(s) and Sponsor group(s) of a REIT.

15. Considering the importance of the Sponsor(s) and Manager/Investment Manager in REIT/InvIT, a Working Group was formed under the aegis of Hybrid Securities Advisory Committee (HySAC) to evaluate the roles and responsibilities of the Sponsor(s) and Manager/Investment Manager. The Working Group submitted its reports on November 9, 2022 and November 23, 2022. The Working Group in its report recommended that REITs and InvITs are relatively a new form of business organization in India and hence currently it is not advisable to have Sponsor-less REIT/InvIT and that there should be at least one Sponsor for the REIT/InvIT on an ongoing basis.

16. It is felt that the requirement of at least one Sponsor fulfilling the necessity of alignment of interest could be addressed by specifying a mandatory minimum unitholding by the Sponsor during the lifetime of the REIT/InvIT (or till such other time, as considered appropriate). Considering the same, there is a need to review the mandatory minimum unit holding requirement by the Sponsor of the REIT/InvIT. Further the consultation paper also discusses about the present regulatory guidelines on creation of encumbrance on locked -in units of the Sponsor and need for consequential review of same in view of the review being undertaken of the regulatory provisions on unitholding requirements of the Sponsor.

III. Extant Regulatory Framework with respect to Sponsor(s) in REIT and InvIT Regulations:

17. With respect to the Sponsor, REIT/InvIT Regulations inter-alia mandate the following:

17.1. Current Provisions on Setting up of REIT and InvIT:

17.1.1. In case of REITs, “Sponsor” means any person(s) who set(s) up the REIT and is designated as such at the time of application made to the Board and shall include an inducted Sponsor.

In case of InvITs, “Sponsor” means any company or LLP or body corporate which sets up the InvIT and is designated as such at the time of application made to the Board and shall include an inducted Sponsor.

17.1.2. The application for grant of certificate of registration as REIT/InvIT has to be made by the Sponsor on behalf of the trust. The applicant is the Sponsor on behalf of the trust and the instrument of trust is in the form

of a deed duly registered in India under the provisions of the Registration Act, 1908.

17.1.3. The persons designated as Sponsor(s), Manager/ Investment Manager and trustee are separate entities.

17.2. Current Provisions on Eligibility Criteria for Sponsor in REIT and InvITs:

17.2.1. Each Sponsor shall be clearly identified in the application of registration to the Board and in the offer document/ placement memorandum.

17.2.2. In case of REITs, the Sponsor(s) on collective basis shall have net worth of not less than INR 100 Crore and each Sponsor has net worth of not less than INR 20 Crores.

Further, in case of InvITs, each Sponsor has a net worth of not less than INR 100 crore if it is a body corporate or a company or net tangible assets of value of not less than INR 100 crore in case it is a limited liability partnership:

17.2.3. In case of REITs, the Sponsor or its associate(s) has at least 5-year experience in development of real estate or fund management in real estate industry and where the Sponsor is a developer, at least two projects of the Sponsor have been completed.

In case of InvITs, the Sponsor or its associate has at least 5 year experience in development of infrastructure or fund management in the infrastructure sector and where the Sponsor is a developer, at least two projects of the Sponsor have been completed.

17.3. The Sponsor(s) set up the REIT/InvIT and appoint the trustees of the REIT/ InvIT who is required to be a debenture trustee registered with SEBI.

17.4. Current Provisions on Transfer of shareholding or interest and rights of assets by Sponsor(s):

17.4.1. The Sponsor(s) shall transfer or undertake to transfer, subject to a binding agreement and adequate disclosures in the initial offer document or placement memorandum, their entire shareholding or interest and rights in the holdco and/or SPV or entire ownership of the real estate assets/ infrastructure projects to the REIT/InvIT respectively prior to allotment of units of the REIT/InvIT.

17.5. Current Provisions on Borrowings – REIT

Regulation 20 of REIT Regulations reads as follows:

“ (1) A REIT, whose units are listed on a recognized stock exchange, may issue debt securities in the manner specified by the Board: Provided that such debt securities shall be listed on recognized stock exchange(s)”

(2) The aggregate consolidated borrowings and deferred payments of the REIT, holdco and/or the SPV(s), net of cash and cash equivalents shall never exceed forty nine per cent. of the value of the REIT assets: Provided that such borrowings and deferred payments shall not include any refundable security deposits to tenants.

Explanation 1. –Investment by REITs in overnight mutual funds, characterized by their investments in overnight securities, having maturity of one day, shall be considered as cash and cash equivalent.

Explanation 2. –The amount of cash and cash equivalent shall be excluded from the value of the assets of the REIT

(3) If the aggregate consolidated borrowings and deferred payments of the REIT, holdco and/or the SPV(s), net of cash and cash equivalents exceed twenty five per cent. of the value of the REIT assets, for any further borrowing,

(a)credit rating shall be obtained from a credit rating agency registered with the Board; and

(b)approval of unit holders shall be obtained in the manner as specified in regulation 22.

17.6. Current Provisions on Borrowings – InvIT

Regulation 20 of InvIT Regulations reads as follows:

“(1) An InvIT, whose units are listed on a recognized stock exchange, may issue debt securities in the manner specified by the Board:

Provided that such debt securities shall be listed on recognized stock exchange(s).

(2) The aggregate consolidated borrowings and deferred payments of the InvIT, holdco and the SPV(s), net of cash and cash equivalents shall not exceed seventy per cent. of the value of the InvIT assets.

(3) If the aggregate consolidated borrowings and deferred payments of the InvIT, holdco and the SPV(s), net of cash and cash equivalents exceed twenty five per cent. of the value of the InvIT assets, for any further borrowing,–

Explanation 1. –Investment by InvITs in overnight mutual funds, characterized by their investments in overnight securities, having maturity of one day, shall be considered as cash and cash equivalent. Explanation 2. –The amount of cash and cash equivalent shall be excluded from the value of the assets of the InvIT

a) upto forty nine percent, an InvIT shall –

(i)obtain credit rating from a credit rating agency registered with the Board; and

(ii) seek approval of unitholders in the manner as specified in Regulation 22.

b) above forty nine percent, an InvIT shall –

(i) obtain a credit rating of “AAA” or equivalent for its consolidated borrowing and the proposed borrowing, from a credit rating agency registered with the Board;

(ii) utilize the funds only for acquisition or development of infrastructure projects;

(iii) have a track record of atleast six distributions, in terms of sub-regulation (6) of regulation 18, on a continuous basis, post listing, in the years preceding the financial year in which the enhanced borrowings are proposed to be made;

(iv) obtain the approval of unitholders in the manner specified in sub-regulation (5A) of regulation 22.

17.7. Current Provisions on mandatory unitholding requirement for Sponsor in REITs:

17.7.1. The Sponsor(s) and Sponsor group(s) shall collectively hold a minimum of 15% of the total units of the REIT for a period of at least three years from the date of listing of such units pursuant to initial offer on a post-issue basis, subject to the following:

the Sponsor(s) and the Sponsor group(s) shall continue to be liable to the REIT, trustees and unit holders for all acts of commission or omission, representation or covenants related to the formation of the REIT and the sale or transfer of assets or holdco or SPV to the REIT.

Further, any holding of the Sponsor(s) and Sponsor group(s) exceeding the minimum holding, shall be held for a period of atleast one year from the date of listing of such units.

17.8. Current Provisions on mandatory unitholding requirement for Sponsor in InvITs:

The Sponsor(s) together shall hold not less than 15% of the total units of the InvIT after initial offer of units, on a post-issue basis for a period of not less than 3 years from the date of the listing of such units, subject to the following:

17.8.1. Sponsor(s) would be responsible for all acts, omissions and representations/covenants of the InvIT related to formation of InvIT, sale/ transfer of assets/holdco/SPV to the InvIT.

17.8.2. the InvIT/the trustee of the InvIT shall also have recourse against the Sponsor for any breach in this regard.

17.8.3. project Manager of the InvIT shall be the Sponsor or an associate of the Sponsor and shall continue to act in such capacity for a period of minimum three years from the date of listing of InvIT units unless suitable replacement is appointed by the unit-holders through the Trustee.

Further, holding by Sponsor in InvIT, exceeding 15% on a post issue basis, shall be held for a period of not less than one year from the date of listing of such units.

However the condition specified at para 17.8.3 above shall not be applicable where the Sponsor(s) together hold not less than twenty five percent of the total units of the InvIT after initial offer of units, on a post-issue basis for a period of not less than 3 years from the date of the listing of such units.

17.9. Current Provisions on de-classification of the status of a Sponsor(s):

17.9.1. De-classification of the status of a Sponsor(s) of a REIT/InvIT whose units have been listed on the stock exchanges for a period of three years is permitted upon receipt of an application from the REIT/InvIT and subject to compliance with the following conditions:

17.9.1.1. The unit holding of such Sponsor and its associates taken together does not exceed 10% of the outstanding units of the REIT/InvIT;

17.9.1.2. The manager/investment manager of the REIT/InvIT is not an entity controlled by such Sponsor or its associates;

17.9.1.3. In case of REIT, the Sponsor or its associates are not fugitive economic offender;

17.9.1.4. Approval of unit holders has been obtained in accordance with Regulation 22(5) and Regulation 22(4) of REIT Regulations and InvIT Regulations respectively.

IV. Need for Review of unit holding requirement of the Sponsor in the REIT and InvIT

18. REITs/InvITs as an investment vehicle provides Sponsor(s) of REIT/ InvIT a medium to monetize the real estate assets and infrastructure assets owned and operated by them respectively.

19. The Sponsor plays an important role by setting up the REIT/InvIT and transferring the assets into the REIT/InvIT on allotment of the units of the REIT/InvIT which are then listed. As per the extant Regulations, the Sponsor of REIT/InvIT is required to hold at least 15% of units on post initial offer basis for a period of 3 years. Post completion of mandatory lock-in, the Sponsor is permitted to sell its unit holding in the REIT/InvIT. However, REIT and InvIT Regulations consider Sponsor as a party to the REIT/InvIT and cast the following responsibility on the Sponsor(s) including:

19.1. setting up the REIT/InvIT,

19.2. appointing the Trustees of the REIT/InvIT,

19.3. transferring or undertaking to transfer to the REIT/InvIT its entire shareholding or interest and rights in the holdco and/ or SPV or ownership of the real estate assets/ infrastructure projects.

19.4. the Sponsor(s) shall continue to be liable to the REIT/InvIT, trustees and unit holders for all acts of commission or omission, representation or covenants related to the formation of the REIT/InvIT and the sale or transfer of assets or holdco or SPV to the REIT/InvIT.

20. REIT/InvIT has the option to acquire assets from entities other than the Sponsor or its associates. However, from the table below, it is observed that majority of further acquisition of assets by REIT/InvIT have been from the Sponsor or its associates. Thus, the role of Sponsor seems to be of paramount importance in the growth of REIT/ InvIT industry. The details of further acquisition of assets by the REITs/InvITs post listing of units are as under:

|

TABLE 2 (INR Cr) as on Jan 2023 |

|||

| Name of Entity | Purchase of Assets from Unrelated Parties | Purchase of Assets from Related Parties |

Total Purchase of Assets |

|

InvIT |

|||

| InvIT Total | 5,758 | 29,152 | 34,910 |

| InvIT % | 16.5% | 83.5% | 100% |

|

REITs |

|||

| REIT Total | 0 | 12,762 | 12,762 |

| REIT % | 0% | 100% | 100% |

21. REITs and InvITs are permitted to take leverage upto 49% and 70% of the total value of assets (subject to certain conditions) respectively. It is observed that at the time of initial offer, all the existing debts of HoldCo/SPV (i.e. bank loans, debt securities, etc) are not paid through the proceeds of initial offer but are carried forward in the books of REIT/ InvIT and continues to subsist after the transfer to the REIT/InvIT. Such debt/bank loan facilities are generally long term considering the nature of investment i.e. real estate or infrastructure financing. As per the extant Regulations, if the REIT/InvIT desires to increase the borrowing over and above 25%, approval of the unitholders, mandatory credit ratings and/or certain other conditions are to be fulfilled. Such stipulations are in place to ensure that the unitholders have a say on incremental leverage of REIT/InvIT. The details of total consolidated borrowing of the InvIT as a percentage of value of InvIT assets are as follows

|

TABLE 3 |

||

| S.No. | Name of Entity | Consolidated borrowing on March 31, 2022 as a % of value of InvIT assets |

|

InvIT |

||

| 1. | A1 | 4.75% |

| 2. | A2 | 19.41% |

| 3. | A3 | 19.77% |

| 4. | A4 | 38.99% |

| 5. | A5 | 40.17% |

| 6. | A6 | 41.18% |

| 7. | A7 | 41.90% |

| 8. | A8 | 42.15% |

| 9. | A9 | 43.09% |

| 10. | A10 | 48.72% |

| 11. | A11 | 52.63% |

| 12. | A12 | 63.30% |

|

REIT |

||

| 1. | R1 | 16.85% |

| 2. | R2 | 24.51% |

| 3. | R3 | 30.42% |

22. From Table 3 above, it is observed that 12 InvITs that have raised funds by way of issuance of units as on March 31, 2022 have also raised funds through borrowings or issuance of debt securities. Of these, the consolidated borrowings of nine InvITs exceed the threshold of 25% and two InvITs exceed the threshold of 49%. Similarly in case of REITs, all REITs that have raised funds through issuance of units as on March 31, 2022, have also raised funds through borrowings or issuance of debt securities and one REIT has consolidated borrowing exceeding the threshold of 25%.

23. As noted earlier, at the time of initial offer, it is possible that the assets proposed to be included in the REIT/InvIT are already leveraged. Upon transfer of assets to the REIT/InvIT by the Sponsor, post initial offer, the debt also stands transferred to the REIT/InvIT. An overview of the consolidated debt of the each InvIT / REIT as on the date of listing along with the maturity profile of the debt is provided as under:

| TABLE 4 | |||||||

| S. No. |

Name of Entity | Amount (debt) outstandin g (In INR Crores) |

Maturity profile from the end of FY of initial offer/funds raised | ||||

| 0-1 years |

1-3 years | 3-5 years | 5-10 years |

10-20 years | |||

| InvIT | |||||||

| 1. | X1 | 0 | 0 | 0 | 0 | 0 | 0 |

| 0% | 0% | 0% | 0% | 0% | 0% | ||

| 2. | X2 | 0 | 0 | 0 | 0 | 0 | 0 |

| 0% | 0% | 0% | 0% | 0% | 0% | ||

| 3. | X3 | 0 | 0 | 0 | 0 | 0 | 0 |

| 0% | 0% | 0% | 0% | 0% | 0% | ||

| 4. | X4 | 0 | 0 | 0 | 0 | 0 | 0 |

–

| TABLE 4 | |||||||

| S. No. |

Name of Entity | Amount (debt) out standing (In INR Crores) |

Maturity profile from the end of FY of initial offer/funds raised | ||||

| 0-1 years |

1-3 years | 3-5 years | 5-10 years |

10-20 years | |||

| 0% | 0% | 0% | 0% | 0% | 0% | ||

| 5. | X5 | 593 | 0 | 0 | 0 | 593 | 0 |

| 100% | 0% | 0% | 0% | 100% | 0% | ||

| 6. | X6 | 750 | 0 | 450 | 300 | 0 | 0 |

| 100% | 0% | 60% | 40% | 0% | 0% | ||

| 7. | X7 | 1,379 | 192 | 307 | 183 | 452 | 245 |

| 100% | 14% | 22% | 13% | 33% | 18% | ||

| 8. | X8 | 995 | 14 | 82 | 719 | 180 | 0 |

| 100% | 1% | 8% | 72% | 18% | 0% | ||

| 9. | X9 | 3,364 | 157 | 480 | 686 | 1,067 | 974 |

| 100% | 5% | 14% | 20% | 32% | 29% | ||

| 10. | X10 | 3,974 | 213 | 676 | 442 | 1,188 | 1,455 |

| 100% | 6% | 17% | 11% | 30% | 36% | ||

| 11. | X11 | 4,861 | 46 | 204 | 332 | 1,737 | 2,542 |

| 100% | 1% | 4% | 7% | 36% | 52% | ||

| 12. | X12 | 6,277 | 458 | 1,342 | 1,829 | 2,402 | 246 |

| 100% | 7% | 21% | 29% | 38% | 4% | ||

| 13. | X13 | 7,752 | 1 | 64 | 174 | 2899 | 4614 |

| 100% | 0% | 1% | 2% | 37% | 60% | ||

| 14. | X14 | 16,836 | 0 | 1,684 | 3,367 | 8,418 | 3,367 |

| 100% | 0% | 10% | 20% | 50% | 20% | ||

| 15. | X15 | 71,605 | 27,763 | 16,900 | 400 | 26,342 | 200 |

| 100% | 39% | 24% | 1% | 37% | 0% | ||

| InvIT Total | 1,18,386 | 28,844 | 22,189 | 8,432 | 45,278 | 13,643 | |

| REITs | |||||||

| 16. | Y1 | 3,796 | 603 | 960 | 538 | 1,389 | 306 |

| 100% | 16% | 25% | 14% | 37% | 8% | ||

| 17. | Y2 | 2100 | 0 | 0 | 1265 | 835 | 0 |

| 100% | 0% | 0% | 60% | 40% | 0% | ||

| 18. | Y3 | 3,654 | 458 | 705 | 850 | 1,117 | 524 |

| 100% | 13% | 19% | 23% | 31% | 14% | ||

| REIT Total | 9,550 | 1,061 | 1,665 | 2,653 | 3,341 | 830 | |

24. From the Table 4 above, it is observed that out of 15 InvITs, consolidated debt of 8 InvITs have the maturity profile of such debt beyond 10 years as on date of listing. Similarly, out of 3 REITs, consolidated debt of two REITs have the maturity profile of such debt beyond 10 years as on date of listing.

25. An overview of the consolidated outstanding debt of each REIT/InvIT at the end of each financial year post initial offer till FY 2022 is provided below:

|

Table 5 |

||||||

| S.No . | Name of Entity | Consolidated Outstanding Debt (in INR Crores) | ||||

| FY 2018 | FY 2019 | FY 2020 | FY 2021 | FY 2022 | ||

| InvITs | ||||||

| 1. | M1 | 2405 | 2,637 | 6,394 | 13,168 | 13,384 |

| 2. | M2 | 1547 | 1,513 | 1,479 | 1,476 | 1,422 |

| 3. | M3 | Not listed | 6,370 | 6,452 | 6,452 | 6,452 |

| 4. | M4 | Not listed | 931 | 4,281 | 4,170 | 4,041 |

| 5. | M5 | No initial

offer |

No initial

offer |

7881 | 9,498 | 9,820 |

| 6. | M6 | Not listed | Not listed | 5,291 | 4,895 | 4,454 |

| 7. | M7 | No initial

offer |

No initial

offer |

No initial

offer |

86842 | 1,06,793 |

| 8. | M8 | Not listed | Not listed | Not listed | 18185 | 21,885 |

| 9. | M9 | Not listed | Not listed | Not listed | Not listed | 575 |

| 10 | M10 | Not listed | Not listed | Not listed | Not listed | 3,206 |

| 11 | M11 | Not listed | Not listed | Not listed | 0 | 1470 |

| 12 | M12 | Not listed | Not listed | Not listed | Not listed | 1,624 |

| InvIT TOTAL | 3,952 | 11,451 | 31,778 | 1,44,686 | 1,75,126 | |

| REITs | ||||||

| 1. | N1 | Not listed | Not listed | Not listed | 3,765 | 4,462 |

| 2. | N2 | Not listed | Not listed | Not listed | 2,120 | 5,199 |

| 3. | N3 | Not listed | Not listed | 5,420 | 10,056 | 12,173 |

| REIT TOTAL | 0 | 0 | 5,420 | 15,941 | 21,834 | |

26. From table 5 above, it is observed that most of the REITs and InvITs have continuously raised funds through either issuance of debt securities or through bank borrowings post initial offer and the level of debt has mostly increased on year on year basis in majority of the REITs/InvITs. However, it is noted that an increase in leverage exceeding 25% is required to be done with the approval of unit holders. As noted in Table 2 above, the majority of the assets post initial offer has been acquired by REIT/ InvIT from the related parties i.e. Sponsor and its associate and as can be seen from Table 4, the assets/SPVs which are acquired from the Sponsor and its associates generally are leveraged.

27. Further, the role of the Sponsor can be highlighted from the fact that Sponsor owns a significant amount of units in the REITs/InvITs and the majority of the Manager/Investment Managers are Sponsor controlled. The data pertaining to unitholding in REIT/InvIT and shareholding in Manager/ Investment Manager is provided below in table 6 and 7 respectively:

| Table 6: Unit Holding Pattern of Sponsor and its associate in REIT and InvITs | |||

| Sr No. |

Name of entity | Sponsor and its associates holding as on listing date (in %) |

Sponsor and its associate holding as on September 30, 2022 (in %) |

| InvITs | |||

| 1. | Highway Infrastructure Trust | 90 | 90 |

–

| Table 6: Unit Holding Pattern of Sponsor and its associate in REIT and InvITs | |||

| Sr No. |

Name of entity | Sponsor and its associates holding as on listing date (in %) | Sponsor and its associate holding as on September 30, 2022 (in %) |

| 2. | Data Infrastructure Trust | 90 | 88 |

| 3. | India Infrastructure Trust | 86 | 75 |

| 4. | SHREM InVIT | 78 | 78 |

| 5. | Virescent Renewable Energy Trust | 77 | 77 |

| 6. | Indian Highway Concessions Trust | 75 | 75 |

| 7. | Oriental Infra Trust | 60 | 59 |

| 8. | IRB Infrastructure Trust | NA | 51 |

| 9. | Digital Fibre Infrastructure Trust | NA | 49 |

| 10 | India Grid Trust | 17 | 24 |

| 11 | National Highways Infra Trust | 16 | 16 |

| 12 | IRB InvIT Fund | 15 | 16 |

| 13 | Powergrid Infrastructure Investment Trust | 15 | 15 |

| 14 | IndInfravit Trust | 65 | 50 |

| REITs | |||

| 1. | Embassy Office Parks REIT | 70 | 36 |

| 2. | Mindspace Business Parks REIT | 63 | 63 |

| 3. | Brookfield India Real Estate Trust | 18 | 16 |

–

| Table 7: Sponsors and its associates Shareholding Of Manager/Investment Manager of

REIT/InvIT |

|||

| Sr No. | Name of entity | % holding (as on date of listing) | % holding(as on September 30, 2022) |

| InvITs | |||

| 1. | IRB Infrastructure Trust | NA | 51 |

| 2. | Indian Highway Concessions Trust | NA | 99.99 |

| 3. | India Grid Trust | 100 | 100 |

| 4. | Powergrid Infrastructure Investment Trust | 100 | 100 |

| 5. | National Highways Infra Trust | 100 | 100 |

| 6. | IRB InvIT Fund | 100 | 100 |

| 7. | SHREM InVIT | 100 | 100 |

| 8. | IndInfravit Trust | 100 | 100 |

| 9. | Oriental Infra Trust | 100 | 100 |

| 6. | Virescent Renewable Energy Trust | 100 | 86 |

| 7. | Highway Infrastructure Trust | 0 | 0 |

| 8. | India Infrastructure Trust | 0 | 0 |

| 9. | Data Infrastructure Trust | 0 | 0 |

| 10. | Digital Fibre Infrastructure Trust | NA | 0 |

| REITs | |||

| 1. | Embassy Office Parks REIT | 100 | 100 |

| 2. | Mindspace Business Parks REIT | 100 | 100 |

| 3. | Brookfield India Real Estate Trust | 100 | 100 |

28. As on date, the Sponsor is required to mandatorily hold at least 15% of total units of REIT/ InvIT, on post-issue basis for a period of at least 3 years. Post completion of 3 years, the Sponsor has the option to divest its stake below 15% and/or declassify itself as a Sponsor. As per the extant regulations,

28.1. In case of divestment, post 3 years of listing, the Sponsor is permitted to sell its entire holding in the REIT/InvIT and still can continue as the Sponsor.

28.2. In case of declassification, the extant Regulations inter alia mandate that the Sponsor and its associates holds less than 10% of the units of the REIT/InvIT and approval of unitholders are required in terms of Regulation 22. There is no mandate to induct a new Sponsor on declassification of the current Sponsor.

29. In view of the facts illustrated above, it is highlighted that the Sponsor is responsible for setting up of the REIT/InvIT and for the formation transaction. The registration of REIT/InvIT is granted based on the eligibility conditions fulfilled by the Sponsor. By virtue of the shareholding in the Manager/Investment Manager, the Sponsor controls the Manager/Investment Manager and has a say in the financing related decisions of the REIT/InvIT especially debt financing. The key decisions regarding management of the assets are made over the long term which keep impacting the investor and their return on their investment. Further, REITs/InvITs are permitted to raise debt up to 49% and 70% of the value of assets of REIT/ InvIT respectively, and that the maturities whether of initial debt or debt raised post initial offer exceeds 10 years, in most of the cases. It is also observed that acquisition of future assets is from Sponsor(s) or its associates. Hence, allowing sponsor to dilute its unit holding completely immediately after the mandatory 3 year lock in period would be inappropriate in view of the impending debt obligations much of which would have been contracted by the sponsor before transferring the assets into the REIT/InvIT. Thus, the need for ensuring alignment of interest between the sponsor and unitholders becomes necessary in case of REIT/InvIT.

30. In view of the same, keeping in mind the interest of unit holders and the structural vulnerabilities associated with absence of Sponsor, it is felt that there is a need to have at least one Sponsor throughout the life of the REIT / InvIT and the Sponsor needs to hold certain percentage of units on a perpetual basis in order to ensure that there is some alignment of interest with the unitholder.

31. In view of the same, there is a need to review the existing norms for unit holding requirement of the Sponsor and declassification of the Sponsor.

Proposals

32. For alignment of interest between the Sponsor and unitholder, the following is proposed:

32.1. The Sponsor shall be required to mandatorily hold certain percentage of total unit capital, in the manner as proposed below, at all points in time:

| TABLE 8 | ||

| S No | Time period | In percentage |

| 1. | Upto 3 years | 15% of total unit capital |

| 2. | 3-5 years | 5% of total unit capital |

| 3. | 5-10 years | 3% of total unit capital |

| 4. | 10-20 years | 2% of total unit capital |

| 5. | Post 20 years | 1 % of total unit capital |

32.2. The units required to be mandatorily held by the Sponsor(s) or Sponsor group(s) cannot be encumbered.

32.3. Further, it is proposed to review the norms for declassification as follows:

32.3.1. The Sponsor(s) of a REIT/InvIT whose units have been listed on the stock exchange(s) for a period of three years is permitted to declassify as the Sponsor subject to compliance with the following conditions:

32.3.1.1. There shall be a new inducted Sponsor in place of existing Sponsor declassifying.

32.3.1.2. The inducted Sponsor shall comply with the eligibility conditions prescribed in REIT Regulations/InvIT Regulations.

32.3.1.3. The mandatory unit holding of the inducted Sponsor shall be as prescribed in Table 8 above.

32.3.1.4. The outgoing Sponsor(s) and its associates shall not have any equity shares or interest or control in the Manager/Investment Manager of the REIT/InvIT.

32.3.1.5. Approval of unit holders has been obtained in accordance with Regulation 22(5) and Regulation 22(4) of REIT Regulations and InvIT Regulations respectively.

32.4. The above mentioned norms will be applicable to all SEBI registered REITs and InvITs raising fresh funds through issuance of units on and from coming into force of the amendments in Regulations. For REITs and InvITs not raising fresh or further funds, this proposal will not be applicable.

33. Consultation:

33.1. Keeping in mind the interest of unit holders and the structural vulnerabilities associated with absence of a Sponsor, comments are sought on the following:

33.1.1. Whether the above approach is suitable for aligning the interest of the Sponsor and the unitholder or alternatively if there is any other proposal that can align the interest of Sponsor and unitholders?

33.1.2. Whether the above mentioned norms for declassification of Sponsor are adequate or any other additional norms needs to be prescribed?

Public comments:

34. Considering the implications of the said matter on the market participants, public comments are invited on the proposal. The comments/ suggestions may be provided as per the format given below:

| Name of the person/entity proposing comments: | ||||

| Name of the organization (if applicable): | ||||

| Contact details: | ||||

| Category: whether market intermediary/ participant (mention type/ category) or public (investor, academician etc.) | ||||

| Sr. No. | Extract from Consultation Paper | Issues (with page/para nos., if applicable) | Proposals/ Suggestions | Rationale |

35. Kindly mention the subject of the communication as, “Comments on Consultation Paper on Holding of Sponsor in REITs and InvITs”.

36. Comments as per aforesaid format may be sent to the following, latest by March 8, 2023, by email to: deenar@sebi.gov.in and; or mneeraj@sebi.gov.in

Issued on: February 23, 2023