Our current Finance Minister (FM) is well known for breaking traditions while presenting the budget, this year, the tradition of using only English as the medium of presenting the budget was altered into bilingual speech with the use of English and Hindi combined. Even though English was prominent, many important announcements were made in Hindi, which of course is a great thing.

The speech started with stating Government’s visions and key practices that the Narendra Modi government has achieved or at least tried to achieve in the past 4 years of the NDA tenure. This was an important budget in light of the 2019 general elections and is the last complete budget of the current elected government. As speculated, it was mainly focused on the agricultural and rural economy along with the less privileged sector and senior citizen getting certain benefits. Healthcare, Infrastructure has been given a lot of importance, many major announcements are made in the same. (Major announcements are discussed later)

Major Direct Taxation aspects of the Finance Bill, 2018

The Finance Bill has not altered the Slab rate per se but there is some benefit in the form of Standard deduction to the salaried class of people.

The Important amendment of granting a Standard deduction of Rs. 40,000 to salaried persons is in lieu of (it is in place of / instead of) exemption of Transport allowance and exemption of medical reimbursement earlier allowed to salaried employees.

Transportation allowance is presently exempted @ Rs. 1,600 per month and medical reimbursement is exempted up to Rs. 15,000 per year so total 1,600*12 = Rs. 19,200 + Rs. 15,000 = Rs. 34,200 is already exempted as on date and instead of these two deductions /exemption standard deduction of Rs. 40,000 has been allowed. So net benefit of just Rs. 40,000 – Rs. 34,200 = Rs. 5,800 /- is what will additionally be available to the taxpayer. However, the private employees who were not eligible for any transport allowance and medical reimbursement will surely be able to avail the benefit Rs. 40,000 /- standard deduction completely. However, the transport allowance at enhanced rate shall continue to be available to differently-abled persons. Also, other medical reimbursement benefits in case of hospitalisation etc., for all employees shall continue.

The Education cess @ 2% and Higher Secondary Education Cess @ 1% is subsumed into a single cess called the Health and Education cess @ 4%. Thus, leading to an additional outflow of 1% cess on the amount of Tax and Surcharge.

The tax on Cooperative Societies, Firms/LLP, foreign companies has remained unchanged. Only domestic companies which have a turnover or gross receipts of 250 crores or less in the previous year FY 2016-17 will pay tax @ 25% instead of 30%. (Previously the limit of 250 crores was only 50 crore). However, the rate at which surcharge is applicable for all persons has remained unchanged.

Rate of Income Tax for Individual & HUF for FY 2018 – 19 (AY 2019 – 20)

| Individuals (Below 60 years) and HUF | Resident Senior Citizen* (60 to 80 years) | Resident very Senior Citizen* (Above 80 years) | |||||||||||

| Income Slabs | Tax Rate | Income Slabs | Tax Rate | Income Slabs | Tax Rate | ||||||||

| Rs. 0 – Rs. 2,50,000 | NIL | Rs. 0 – Rs. 3,00,000 | NIL | Rs. 0 – Rs. 5,00,000 | NIL | ||||||||

| Rs. 2,50,001 – Rs. 5,00,000 | 5% of the amount by which the total income exceeds Rs. 2,50,000/- | Rs. 3,00,001 – Rs. 5,00,000 | 5% of the amount by which the total income exceeds Rs. 3,00,000/- | ||||||||||

| Rs. 5,00,001 – Rs. 10,00,000 | Rs. 12,500/- + 20 % of the amount by which the total income exceeds Rs. 5,00,000/- | Rs. 5,00,001 – Rs. 10,00,000 | Rs. 10,000/- + 20 % of the amount by which the total income exceeds Rs. 5,00,000/- | Rs. 5,00,001 – Rs. 10,00,000 | 20 % of the amount by which the total income exceeds Rs. 5,00,000/- | ||||||||

| Above Rs. 10,00,000 | Rs. 1,12,500/- + 30 % of the amount by which the total income exceeds Rs. 10,00,000/- | Above Rs. 10,00,000 | Rs. 1,10,000/- + 30 % of the amount by which the total income exceeds Rs. 10,00,000/- | Above Rs. 10,00,001 | Rs. 1,00,000/- + 30 % of the amount by which the total income exceeds Rs. 10,00,000/- | ||||||||

Surcharge#:

|

|||||||||||||

| Health & Education Cess @ 4% (Previously was 3%, now Increased) It will be computed on the aggregate of Income-Tax and Surcharge. | |||||||||||||

| Rebate** of Rs. 2,500/- (Maximum) – If Total Income is up to Rs. 3,50,000/- (Section 87A) | |||||||||||||

* The benefit of the Senior citizen is applicable only for Resident Individuals as per section 6 of Income Tax Act, 1961. Therefore, the Non-resident senior citizen is not covered and shall be liable to pay tax as per provisions applicable for Individual (Below 60 years) and HUF.

# Surcharge will be applicable over and above Normal Slab Rate Taxes (Only if Total Income exceeds the mentioned limits) otherwise, it won’t be applicable.

** Rebate will be applicable only in the cases where the Total income is up to Rs. 3,50,000/-, in such cases there will be a rebate of maximum Rs. 2,500/- allowed or the tax payable, whichever is lower.

TOTAL INCOME: The sum of all money received, under each head of income, by an individual or organization, which is reduced by the deductions applicable (under Chapter VI-A) is called total income.

Special Benefits for Senior Citizens

To care of those who cared for us is one of the highest honours.

– Arun Jaitley

1. Under Section 80D – Health Insurance Premium and Medical Treatment, the deduction of Rs. 30,000/- were applicable to the Senior citizen which has been enhanced to Rs. 50,000/- for the AY 2019-20.

2. Under Section 80DDB – Enhanced deduction to senior citizens for medical treatment of specified diseases which was Rs. 60,000/- in case of senior citizen and Rs. 80,000/- in case of very senior citizen has been uniformly been enhanced to Rs. 1,00,000/-

3. Under Section 80TTA – Interest Income from Saving Accounts of Rs. 10,000/- is deductible from tax. For Senior Citizen a new Section 80TTB has been inserted to provide a deduction of Rs. 50,000/- in place of Rs. 10,000/- from AY 2019-20.

4. Under Section 194A – TDS from Interest Income has been amended for Senior citizens only. The threshold of Rs. 10,000/- has been increased to Rs. 50,000/-. Therefore, any Interest getting accrued or paid from 1st April 2018, for senior citizen shall not attract TDS up to Rs. 50,000/-.

5. Standard Deduction of Rs. 40,000 shall also be applicable to Senior citizens also in lieu of Transport allowance and Medical reimbursement. However, the transport allowance at enhanced rate shall continue to be available to differently-abled persons. Also, other medical reimbursement benefits in case of hospitalisation etc., for all employees shall continue.

Corporate Taxes Rates Tax FY 2018 – 19 (AY 2019 – 20)

| Turnover Particulars | Type of Tax | Nil to 1 crore | 1 crore to 10 crores | 10 crores to 250 crores | Exceeding 250 crores |

| Domestic Company | Basic Rate | 25% | 25% | 25% | 30% |

| Surcharge | 0% | 7% | 12% | 12% | |

| H&E Cess | 4% | 4% | 4% | 4% | |

| Effective Tax | 26% | 27.82% | 29.12% | 34.944% | |

| Foreign Company | Basic Rate | 40% | 40% | 40% | 40% |

| Surcharge | 0% | 2% | 5% | 5% | |

| H&E Cess | 4% | 4% | 4% | 4% | |

| Effective Tax | 41.6% | 42.432% | 43.68% | 43.68% | |

| Firm / Local Authority / Cooperative Society | Basic Rate | 30% | 30% | 30% | 30% |

| Surcharge | 0% | 12% | 12% | 12% | |

| H&E Cess | 4% | 4% | 4% | 4% | |

| Effective Tax | 31.2% | 34.944% | 34.944% | 34.944% |

FM has reduced the Domestic Companies tax rate to 25% from 30% for the companies which have turnover up to 250 crores. (MSME Tax) This shall include 99% of companies. Only XL companies will have to bear the tax at the old rate. Since there is no change in the surcharge applicable, therefore it remains as per previous finance acts. Instead of 3% cess of EC & HSEC, there will be a single Health and Education Cess of 4% applicable.

NOTE: Provisions like MAT, AMT and Marginal relief are applicable without any change.

Section 112A – Taxation of Long-Term Capital Gains

Currently, long-term capital gains arising from a transfer of listed equity shares or units of equity-oriented fund or units of business trusts, (assets held for a period of more than one year) are exempt from income-tax under Section 10(38) of the Act. As per newly proposed Section 112A, long-term capital gains arising from a transfer of an equity share, or a unit of an equity-oriented fund or a unit of a business trust shall be taxed at 10% of such capital gains. Such capital gains tax shall be levied in excess of Rs. 1 lakh. This concessional rate of 10% will be applicable if STT has been paid on both acquisition and transfer of such capital asset, in case of equity shares, and paid at the time of transfer in case of a unit of an equity-oriented fund or a unit of a business trust.

The concept of Grandfathering was introduced while levying the tax on LTCG on above-mentioned shares and securities, which means to exempt something from the new law or regulation. Therefore, any gains made up to 31st January 2018 would be totally exempt. Therefore, this tax comes into force for all sales happening from 1st February 2018 and the shares and securities being Long-term capital assets. The long-term capital gains shall be computed without giving effect to the first and second provisos to section 48, i.e. inflation indexation in respect of the cost of acquisitions and improvement if any, and the benefit of computation of capital gains in foreign currency in the case of a non-resident, will not be allowed.

| Particulars | Rs. | Rs. |

| Full value of Sale Consideration | XXX | |

| Less: Transfer Expenses | (XX) | |

|

Net Consideration |

XXX | |

| Cost of Acquisition | ||

|

a. Actual Cost of Acquisition |

XXX | |

|

b. FMV as on 31.01.2018* |

XX | |

|

c. Amount of sale consideration |

XX | |

|

d. Lower of (b) or (c) |

XX | |

| Cost of Acquisition – Higher of (a) or (d) | (XXX) | |

| Capital gains taxable u/s 112A | XXX |

* The Fair Market Value (FMV) of a listed equity share shall mean its highest price quoted on the stock exchange on January 31, 2018. However, if there is no trading in such shares on such exchange on January 31, 2018, the highest price of such asset on such exchange on a date immediately preceding January 31, 2018. While in case of units which are not listed on the recognized stock exchange, the net asset value of such units as on January 31, 2018, shall be deemed to be its FMV.

If the Capital gains taxable u/s 112A is up to Rs. 1,00,000/- then there will be no tax payable. However, if the amount of gain exceeds Rs. 1,00,000/- then the tax will be payable on the gain above Rs. 1,00,000/-.

The deduction under Chapter VIA shall not be allowed for the purpose of payment of capital gains tax u/s 112A. However, the benefit of Rebate u/s 87A shall be allowed before calculating tax u/s 112A.

NOTE: In case of Capital loss, whether the set off will be allowed to be carried forward or not is not is not explained. Going by the principles of Set off provisions, if a gain is taxable then any loss arising out of the same nature of income would be allowed to be set off. But if the gain is tax-free then any loss of such nature cannot be set off. However, this scheme of calculation, where the base of acquisition of the asset is getting shifted, should the loss be allowed or not. This can lead to fresh litigation and therefore to avoid this, the government is expected to clarify its stand soon.

Further, the complication can increase in the case of Bonus issues or rights issues of shares.

Therefore, presently the Capital gains on Long-Term Shares can be summed up as:

| Nature of Shares | Rate of Tax (%) | |

| Resident Investor | Non-Resident Investor | |

| Unlisted Shares | 20% | 10% |

| Listed Shares (Sold off the Market) | 10% / 20%** | 10% |

| Listed Shares (STT paid* on Sale and Purchase) | 10% | 10% |

| * Rate of Tax applicable only for gains exceeding Rs. 1,00,000/- and government is to notify acquisitions in respect of which STT shall not apply.

** After applying Indexation. |

||

These amendments will take effect from 1st April 2019 and will, accordingly, apply in relation to the assessment year 2019-20 and subsequent assessment years.

Section 115AD – Long-Term Capital Gains in case of Foreign Institutional Investors (FIIs)

Consequent to the proposal of withdrawing the exemption u/s 10(38) of Long-term capital gains, such Long term Capital gains in excess of Rs. 1,00,000/- shall be taxable in the hands of FIIs at the rate of 10% u/s 115AD.

Section 115R – Dividend distribution tax on dividend payouts to unitholders in an equity-oriented fund

Under existing provision Section 115R – any income distributed to a unitholder of equity-oriented funds is not chargeable to tax. To provide a level playing field between growth-oriented funds and dividend paying funds, it is proposed to amend the said section to provide that where any income is distributed by a Mutual Fund being, an equity-oriented fund, the mutual fund shall be liable to pay additional income tax at the rate of 10% percent on income so distributed.

This amendment will take effect from 1st April 2018.

Rationalization of section 43CA, section 50C and section 56

At present, while taxing income from capital gains (section 50C), business profits (section 43CA) and other sources (section56) arising out of transactions in immovable property, the sale consideration or stamp duty value, whichever is higher is adopted.

The difference is taxed as income both in the hands of the purchaser and the seller.

It is proposed that No adjustment needs to be made to the full value of consideration in based on stamp duty valuation if the variation is within the range of 5% of sales consideration.

The corresponding amendment in section 43CA, 50C and 56 are made.

These amendments will take effect from 1st April 2019 and will, accordingly, apply in relation to the assessment year 2019-20 and subsequent assessment years.

Rationalisation of provision relating to conversion of stock-in-trade into Capital Asset

Currently, section 45(2) covers conversion of Capital Assets into Stock in Trade. (Post the landmark judgement of “CIT vs. Bai Shirinbai K. Kooka”

But surprisingly, the reverse scenario was not covered in the tax net and in this budget it has been proposed to be brought under tax net i.e. conversion of Stock in Trade into Capital Assets.

Section 28 is also amended so as to provide that any profit or gains arising from the conversion of inventory into a capital asset or its treatment as capital asset shall be charged to tax as business income.

The fair market value of the inventory on the date of conversion shall be deemed to be the full value of the consideration received.

Consequently, corresponding amendments proposed in Section 2(24), 2(42A) & 49.

Rationalisation of provision of Section 54EC

Section 54EC of the Act provides that capital gain, arising from the transfer of a long-term capital asset, invested in the long-term specified asset at any time within a period of six months after the date of such transfer, shall not be charged to tax subject to certain conditions specified in the said section.

The scope of this section now proposed to restrict only to “long-term specified asset” being land or building or both.

It is also proposed to provide that long-term specified asset, for making any investment under the section on or after the 1st day of April, 2018, shall mean any bond, redeemable after five years (The period of holding (lock-in) enhanced from present level of 3 years to proposed 5 years.) and issued on or after 1st day of April, 2018 by the National Highways Authority of India or by the Rural Electrification Corporation Limited or any other bond notified by the Central Government in this behalf.

This amendment will take effect, from 1st April 2019 and will, accordingly, apply in relation to the assessment year 2019-20 and subsequent assessment years.

Other Important Direct Tax Proposal in the Union Budget

Deductions in respect of certain incomes not to be allowed unless return is filed by the due date

Existing provisions contained in the section 80AC of the Act provide that no deduction would be admissible under section 80IA, 80IAB, 80IB, 80C, 80ID and 80IE unless the return of income by the assessee is furnished on or before the due date specified under subsection 139(1).

It is proposed to extend the scope of section 80AC to provide that the benefit of deduction under the entire class of deductions under the heading C – “Deduction in respect of certain incomes” in chapter VIA.

Other deductions in Chapter VI-A continue to be allowed.

Farm Produce Companies

Farm Producer Companies (FPC), having a total turnover up to Rs. 100 Crore shall eligible to deductions u/s 80P.

The benefit shall be available for a period of five years from the financial year 2018-19.

This amendment will take effect from 1st April 2019 and will, accordingly, apply in relation to the assessment year 2019-20 and subsequent assessment years.

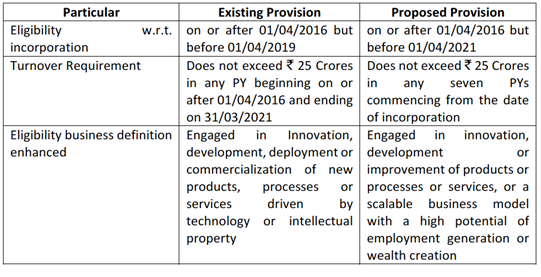

Measures for Promoting Start-ups u/s 80-IAC

Section 80-IAC of the Act provides that deduction under this section shall be available to an eligible start-up for 3 consecutive AY out of 7 years at the option of the assessee.

In order to improve the effectiveness of the scheme for promoting start-ups in India, it is proposed to make following changes.

The amendment will take effect, from 1st April 2018 and will, accordingly, apply in relation to the assessment year 2018-19 and subsequent assessment years.

Application of Dividend Distribution Tax to Deemed Dividend u/s 2 (22) (e) – Now Taxable to Companies Only

At present dividend distributed by a domestic company is subject to dividend distribution tax payable by such company. However, deemed dividend u/s 2 (22) (e) is taxed in the hands of the recipient at the applicable marginal rate. The taxability of deemed dividend in the hands of the recipient has posed a serious problem of the collection of the tax liability and has also been the subject matter of extensive litigation.

Proposed to delete the Explanation to Chapter XII-D occurring after section 115Q of the Act

Now DDT chargeable u/s 115-O also include dividend u/s 2 (22) (e) in the hands of company @ 30% (without gross-up).

Proposed DDT structure –

| Dividend covered u/s 2 (22) (a) to (d) | DDT @ 15% (with grossing up) |

| Dividend covered u/s 2 (22) (e) | DDT @ 30% (without grossing up) |

Tax neutral transfers

Section 47 provides for certain tax neutral transfers, which includes the transfer of capital assets between the wholly owned subsidiary company and its holding company.

However, no corresponding provision was available in statute book in section 56 under the head “Income from Other Source”

Accordingly, in order to further facilitate the transaction of money or property between a wholly owned subsidiary company and its holding company, it is proposed to amend the section 56 so as to exclude such transfer from its scope.

This amendment will take effect, from 1st April 2018 and shall accordingly, apply in relation to the transaction made on or after 1st April 2018.

Quoting of PAN

It is proposed to use a PAN as Unique Entity Number (UEN) for non-individual entities which enter into a financial transaction of an amount aggregating ₹ 2,50,000 Lakh or more in FY.

In order to link the financial transactions with the natural persons, it is also proposed that the managing director, director, partner, trustee, author, founder, Karta, chief executive officer, principal officer or office of such entities shall also apply for PAN u/s 139A.

Penalty for failure to furnish statement of financial transaction or reportable account u/s 285BA

| Penalty | Existing Penalty | Proposed Penalty |

| Failure to furnish statement of financial transaction or reportable account within the prescribed time | Rs. 100 / day | Rs. 500 / day |

| Failure to furnish the statement of financial transaction or reportable account within the period specified in the notice | Rs. 500 / day | Rs. 1,000 / day |

These amendments will take effect from 1st April 2018.

ICDS

Recent judicial pronouncements had raised doubts about the legitimacy of the notified ICDS.

In order to regularise the compliance with the notified ICDS by a large number taxpayer so as to prevent any further inconvenience to them, this Union Budget has proposed many amendments in the existing law and inserted new sections for smooth compliance with the ICDS.

- Marked to market loss computed as per ICDS to be allowed under section 36.

- Gain or loss on Foreign Exchange as per ICDS to be allowed under new section 43AA.

- Construction Contract income to be computed on percentage completion method as per ICDS.

- Valuation of Inventory including Securities to be as per ICDS.

- Interest on compensation, enhanced compensation. Claim or enhancement claim and subsidy, incentives to be taxed in the year of receipt only as per new Section 145B.

- Conversion of stock in trade to a capital asset to be charged as business income in the year of conversion on Fair Market value on the date of conversion.

It is proposed to bring the amendments retrospectively with effect from 1st April 2017 i.e. the date on which the ICDS was made effective and will, accordingly, apply in relation to the assessment year 2017-18 and subsequent assessment years.

Major Indirect Taxation aspects of the Finance Bill, 2018

Amendments to the Customs Act, 1962

- Scope of Customs Act amended to include any offence or contravention committed thereunder outside India by any person

- Definition of term “assessment” and “re-assessment” has been expanded significantly to include factors such as classification, valuation, exemption or concession, quantity, weight & measure, origin and any other specific factor which impact the computation of Customs duty.

- The limit of ‘Indian Customs Waters’ into the sea from the existing ‘Contiguous zone of India’ has been extended to the ‘Exclusive Economic Zone (EEZ)’ of India.

- Verification of self-assessed imported goods shall be based on a risk-based selection Criteria.

- Provisional assessment of duty would also cover export consignments.

- Provision to exempt goods imported for repair, further processing of manufacture from payment of Customs Duty introduced, similar provisions inserted for re-import of exported goods as well.

- Pre-notice consultation to be held with assessees in cases not involving collusion, willful mis-statement, suppression before issuing of demand notice.

- Provision for issuance of supplementary show-cause notice introduced subject to specified timelines and circumstances.

- Adjudication of notices to be completed within prescribed timelines

-

- 6 months for notices issued under normal limitation period

- 1 year for cases involving collusion, willful mis-statement, suppression. Time limit extendable up to 6 months / 1-year subject to approval from the higher authorities.

- Proceedings of a show-cause notice shall be deemed to be concluded if adjudication not completed within specified prescribed timelines

- Definition of “Advance Ruling” expanded to cover subjects beyond the mere determination of duty.

- Advance Ruling can now be obtained in respect of taxes apart from duties either under Customs Act or any other law for the time being in force.

- Time limit to pronounce Advance Ruling reduced from 6 months to 3 months

- Customs authorities or applicant authorized to file appeal against a ruling passed by the Advance Ruling authorities within 60 days from the date of communication of the ruling – extendible up to 30 days

- Presentation of Bill of entry/Shipping Bill/Bill of export can also be made through Customs

- Automated System for import and export of goods

- Provision for advance payment of duty under Electronic Cash Ledger introduced

- Audit provisions introduced under the Customs Act

- New Section inserted regarding a reciprocal arrangement for exchange of information between India and any other country in connection with specified Customs matters.

- Social Welfare Surcharge (SWS) introduced, as Customs duty, on all imported goods:

- 3% on import of Petrol, HSD, Silver and Gold

- 10% of all other imported goods (except goods which were hitherto exempt from EC and SHEC)

Ad-valorem rate of SWS will be on the aggregate of Customs Duty (excluding IGST, GST compensation cess, Anti-Dumping Duty, Safeguard Duty, etc.)- essentially on BCD.

- BCD rationalization at 7.5% for various Refractory items.

- Motor Spirit and Petroleum Products

- Basic Excise duty on manufacture of Motor Spirit and HSD reduced by Rs. 2/- per litre

- Road cess of Rs. 6 per litre on petroleum products abolished

- Road and Infrastructure Cess (R & I Cess) on petroleum products of Rs. 8 per litre Introduced.

- Additional Duty of Customs levied on import of Motor spirit and HSD abolished.

Major Rate Changes in Customs

| Description | Existing BCD Rate | Proposed BCD Rate | Future Price Indicator |

| Automobiles | |||

| Specified Radial tyres (Bus and Truck) | 10% | 15% | Costlier |

| Specified parts of motor vehicles | 7.5% -10% | 15% | Costlier |

| CKD parts of motorized four and two Wheelers | 10% | 15% | Costlier |

| CBU Import of Motor vehicle | 20% | 25% | Costlier |

| Diamond and Precious Stones | |||

| Specified Diamond | 2.5% | 5% | Costlier |

| Coloured gemstones | 2.5% | 5% | Costlier |

| Capital Goods and Electronics | |||

| PCBA for chargers of Mobile Phones | Nil | 10% | Costlier |

| Silica (used for Telecom / optical fibre cables) | Nil | 5% | Costlier |

| Specified Parts for Mfg. of Panels of LCD/LED TV | Nil | 10% | Costlier |

| Solar tempered glass for Mfg. of solar cells | 5% | Nil | Cheaper |

| Inputs for manufacture of PCBA or moulded plastics for chargers of Mobile Phones | Applicable Rate | Nil | |

| Specified Inputs for Manufacture of CNC Machine Tools | 7.5% | 2.5% | Cheaper |

| Electronic products | |||

| Cellular mobile phones | 15% | 20% | Costlier |

| Specified parts and accessories of cellular mobile phones | 7.5% – 10% | 15% | Costlier |

| Smart watches | 10% | 20% | Costlier |

| LCD/LED/OLED panels and their parts | 7.5% / 10% | 15% | Costlier |

| Video games | 10% | 20% | Costlier |

| Watches and Clocks | |||

| Watches and clocks including stopwatches and alarm clocks | 10% | 20% | Costlier |

| Footwear | |||

| Specified footwear | 10% | 20% | Costlier |

| Specified parts of footwear | 10% | 15% | Costlier |

| Miscellaneous Items | |||

| Specified Parts of Furniture | 10% | 20% | Costlier |

| Sunglasses | 10% | 20% | Costlier |

| Imitation jewellery | 15% | 20% | Costlier |

Major Non-Taxation Announcement in the Finance Bill, 2018

Health Care

The announcement of Universal Health Coverage programme by launching a flagship National Health Protection Scheme to cover over 10 crore poor and vulnerable families (approximately 50 crore beneficiaries) providing coverage up to 5 lakh rupees per family per year for secondary and tertiary care hospitalization. This is the most cheered thing of the budget, making it the aam aadmi budget, now the only concern is the smooth implementation of this programme and how the benefit will reach the required masses is still not very clear. Creating the awareness among the beneficiaries is the key to its success. Additionally, there shouldn’t be any procedural complexities while taking the benefit of this scheme of government by the people. Therefore, Implementation will hold the key here.

Agriculture

With the Prime Minister strong desire to double the farmer’s income by 2022, the government had already set the major rabi crops Minimum Selling Price (MSP) at 1.5 times their cost of production. Now, in the budget, the government has decided to implement this resolution as a principle for the rest of crops. The government has decided to keep MSP for the all unannounced crops of Kharif at least at one and half times of their production cost. This decision will prove to be an important step towards doubling the income of our farmers. However, the fool-proof mechanism of deciding what will be the adequate cost of production for every crop, whether will it differ state wise or not are some of the questions that the Niti Ayog, in consultation with Central and State Governments will have to decide upon. Additionally, this will not give any immediate relief to the farmer community since the Kharif crops are grown from July to October and sold thereafter. So, the government needs to come out with all possible answers of the agricultural community and offer them the fair deal as promised in the budget.

The Government is keen in improving conditions of farmers by providing better warehousing conditions, connecting APMC’s to e-NAM (National Agriculture Market), allocating ₹ 2,000 crores for agri-market infrastructure fund, developing Grameen Agricultural markets. The FM in his speech has stated the need for developing a cluster-based method for farming in more scientific manner, Organic farming, setting up long-term irrigation fund and many other allocations for specific purposes. How many of this sees the light of the day will be an interesting thing to witness. Successful implementation of these things at a scale which can make a difference will require coordination and cooperation from different stakeholders.

Other Important Announcements in Budget Speech

- GDP growth at 6.3% in the second quarter signalled turnaround of the economy.

- India is expected to grow at 7.2% to 7.5% in the second half (October – March)

- Exports grew by 15% in 2017-18.

- India is now firmly on course to achieve high growth of 8% plus.

- More than 800 medicines are being sold at a lower price through more than 3 thousand Jan Aushadhi Centres.

- The government will aim to double farmers’ income by 2022.

- In the year 2016-17 India achieved a record food grain production of around 275 million tonnes and around 300 million tonnes of fruits and vegetables.

- Food Processing sector is growing at an average rate of 8% per annum

- Prime Minister Krishi Sampada Yojana is our flagship programme for boosting investment in food processing. Allocation of Ministry of Food Processing is being doubled from Rs. 715 crores in the year 2017-18 to Rs. 1,400 crores in the year 2018-19.

- India’s agri-exports potential is as high as US $ 100 billion against current exports of US $ 30 billion.

- FM announce setting up a Fisheries and Aquaculture Infrastructure Development Fund (FAIDF) for fisheries sector and an Animal Husbandry Infrastructure Development Fund (AHIDF) for financing infrastructure requirement of animal husbandry Total Corpus of these two new Funds would be `10,000 crores.

- Prime Minister’s Ujjwala Scheme to make poor women free from the smoke of wood. With the successful implementation of Ujjwala scheme and its popularity among the women, FM proposes to increase the target of providing a free connection to 8 crore poor women.

- Prime Minister Saubhagya Yojana for providing electricity to all households of the country, four crores poor households are being provided with electricity connection free of charge. We are spending `16000 crores under this scheme.

- Loans to Self Help Groups of women increased to about Rs. 42,500 crores in 2016-17, growing 37% over previous The proposed growth estimate is that loans to SHGs will increase to Rs. 75,000 crores by March 2019.

- Technology will also be used to upgrade the skills of teachers through the recently launched digital portal ‘‘DIKSHA’’.

- To step up investments in research and related infrastructure in premier educational institutions, including health institutions, a major initiative named ‘‘Revitalising Infrastructure and Systems in Education (RISE) by 2022’’ with a total investment CAPEX of Rs. 1,00,000 crore in next four years was announced.

- National Health Policy, 2017 has envisioned Health and Wellness Centres as the foundation of India’s health system, FM announced Rs. 1,200 crores in this budget for this flagship These centres will provide comprehensive health care, including for non-communicable diseases and maternal and child health services. These centres will also provide free essential drugs and diagnostic services.

- FM has allocated additional Rs. 600 crores to provide nutritional support to all TB patients at the rate of Rs. 500 per month for the duration of their

- FM announced that government will contribute 12% of the wages of the new employees in the EPF for all the sectors for next three years Also, the facility of fixed-term employment will be extended to all sectors.

- To incentivise women employment, FM has proposed to reduce women employees’ contribution to 8% for first three years of their employment against existing rate of 12% or 10% with no change in employers’

- 306 Pradhan Mantri Kaushal Kendra has been established for imparting skill training through such centres.

- Smart Cities Mission aims at building 100 Smart Cities with state-of-the-art FM inform that 99 Cities have been selected with an outlay of Rs. 2.04 lakh crore.

- The AMRUT programme focuses on providing water supply to all households in 500 State level plans of Rs. 77,640 crores for 500 cities have been approved. Water supply contracts for 494 projects worth Rs. 19,428 crores and sewerage work contract for 272 projects costing Rs. 12,429 crores have been awarded.

- Bharatmala Pariyojana has been approved for providing seamless connectivity of interior and backward areas and borders of the country to develop about 35000 km in Phase-I at an estimated cost of Rs. 5,35,000

- Railways’ Capex for the year 2018-19 has been pegged at Rs. 1,48,528 A large part of the Capex is devoted to capacity creation. 18,000 kilometres of doubling, third and fourth line works and 5000 kilometres of gauge conversion would eliminate capacity constraints and transform almost entire network into Broad Gauge.

- Redevelopment of 600 major railway stations is being taken up by Indian Railway Station Development Ltd. All stations with more than 25,000 footfalls will have escalators. All railway stations and trains will be progressively provided with wi-fi. CCTVs will be provided at all stations and on trains to enhance the security of passengers.

- President’s Salary to be enhanced to Rs. 5,00,000/- per month, Vice-president’s Salary to be enhanced to Rs. 4,00,000/- per month and Governor’s Salary to be enhanced to Rs. 3,00,000/- per month.

- FM proposed changes in the salary, constituency allowance, office expenses and meeting allowance payable to Members of Parliament with effect from April 1, 2018. The law will also provide for automatic revision of emoluments every five years indexed to inflation.

- FM revised the Fiscal Deficit estimates for 2017-18 are Rs. 95 lakh crore at 3.5% of GDP. FM projected a Fiscal Deficit of 3.3% of GDP for the year 2018-19.

- All companies irrespective of income to file a return and in case it is not filed, such companies will be liable for prosecution irrespective of the fact whether it has the tax liability of Rs 3,000 or not.

- Assessments to be E-assessment under new section 143(3A)

- No adjustment under section 143(1) while processing on account of the mismatch with 26AS and 16A.

Allocation of Rs. in Lakhs

Disclaimer:

This document is intended for knowledge sharing purpose only. All efforts have been made to ensure the accuracy of information in this publication. The information contained in this document is published for the knowledge of the recipient but is not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient. The publication is a service to all recipients only to provide an overview of the Union Budget Proposals and shall not be construed as professional advice or an authoritative opinion. Whilst due care has been taken in the preparation of this publication and information, I am not responsible for any errors that may have crept in inadvertently and do not accept any liability whatsoever, for any direct or consequential loss howsoever arising from any use of this publication or its contents or otherwise arising in connection herewith.

(Compiled by CA. Siddharth P. Jani, for any queries/suggestion or rectifications kindly write at casiddharthjani@gmail.com)

Author Bio

CORRECTION: Currently, long-term capital gains arising from a transfer of listed equity shares or units of equity-oriented fund or units of business trusts, (assets held for a period of more than one year) are exempt from income-tax under Section 10(38) of the Act. The exemption u/s 10(38) will come to an end from 1st April 2018, therefore any capital gains till 31.03.2018 will continue to remain exempt u/s 10(38). As per newly proposed Section 112A, long-term capital gains arising from a transfer of an equity share, or a unit of an equity-oriented fund or a unit of a business trust shall be taxed at 10% of such capital gains. Such capital gains tax shall be levied in excess of ₹ 1 lakh. This concessional rate of 10% will be applicable if STT has been paid on both acquisition and transfer of such capital asset, in case of equity shares, and paid at the time of transfer in case of a unit of an equity-oriented fund or a unit of a business trust.

The concept of Grandfathering was introduced while levying the tax on LTCG on above-mentioned shares and securities, which means to exempt something from the new law or regulation. Therefore, any gains made up to 31st January 2018 would be totally exempt, when the share is sold post 31st March 2018. Therefore, this tax comes into force for all sales happening from 1st April 2018 and the shares and securities being Long-term capital assets. The long-term capital gains shall be computed without giving effect to the first and second provisos to section 48, i.e. inflation indexation in respect of the cost of acquisitions and improvement if any, and the benefit of computation of capital gains in foreign currency in the case of a non-resident, will not be allowed.

Well written article keep it up bro