WHAT IS TDS/TCS?

In case of certain prescribed payments (e. g. Interest, commission, brokerage, rent, etc.) the person making payment is required to deduct tax at source (TDS) at prescribe rate. Payer is known as deductor and the payee, who receives the net payment is called the deductee.

TCS is Tax Collected at Source by seller from buyers at the time of selling some prescribed goods. Seller is called ‘collector’ and the buyer is called ‘collectee’.

WHICH NUMBER IS TO BE OBTAINED BY DIE DEDUCTOR/COLLECTOR?

Every person deducting/collecting tax at source is required to obtain TAN & Quote it in every correspondence related to TDS/TCS

Note: Not mandatory in case of tax deduction on purchase of immovable property and also in case of TDS on rent (paid by non-auditable Individual & HUF.

INTERNET BASED FUNCTIONALITIES FOR TDS/TCS COMPLIANCE BY DEDUCTORS/ COLLECTORS

- Mandatory to register on TRACES (www.tdscpc.gov.in) before use.

- View “Deductor Dashboard” to know about TDS performance (Staternent status, challan status, Default payable, Deductor Compliance Profile).

- View “TDS CPC Communications” on TRACES Homepage to access communications sent by CPC (TDS).

- Online/Offline One TDS Statement Corrections directly on TRACES.

- Downloads-TDS/TCS Certificates, Transaction Based Report (TBR) for non-PAN & deductees reported in Form 27Q Consolidated file, Justification Report, TAN-PAN Consolidated File.

- Intermidiary Communication-Alerts (SMS/email) in case of challan and PAN errors identified in regular TDS Statements during preliminary screening, to avoid Default Intimation from CPCO(TDS)

- Aggregated TDS Compliance Report – Consolidated default summary of all TANs corresponding to a PAN in case of corporates/banks (available in taxpayer login on TRACES).

- e-Tutorials, FAQs, Circular & Notifications and CPC (TDS) Communication . Deductor Grievanace Module – Request for Resolution online on TRACES

WHEN TO DEDUCT/COLLECT TAX?

- At the time of making the prescribed payment or credit of the income / payment to the deductee, whichever is earlier.

- In case of TCS, tax has to be collected by the seller at the time of debiting account of buyer or at the time of receipt of such amount from buyer in cash or issue of cheque/draft, or by any other mode, whichever is earlier.

- In case of TDS on salary, tax Is to be deducted at the time of actual payment.

- In case of TDS on rent, at the time of credit of rent for the last month of the year.

WHEN TO DEPOSIT THE TAX DEDUCTED/COLLECTED AT SOURCE TO THE CREDIT OF THE GOVERNMENT?

Table No. 1

| Mode of TDS/TCS payment | Due date of payment |

|

On same day (applicable in case of book adjustment) |

|

On or before 30th April. |

|

On or before 7 days from the end of the month. |

|

On or before 30 days from the end of the month of deduction. |

|

On or before 30 days from the end of the month of deduction. |

| (* Challan cum statement in Form 26QB/ 26QC needs to be filed) | |

Note: In certain cases, quarterly payment of TDS can be permitted with the prior approval of the Assessing Officer.

WHICH CHALLAN IS USED FOR PAYMENT OF TDS/TCS?

TDS/TCS is to be deposited to the credit of the Government by using Challan No. ITNS-281

WHAT IS CHALLAN IDENTIFICATION NO. (CIN)?

Every Income Tax Challan is identified by CIN which contains Bank BSR Code, Date of Payment & Challan serial no.

HOW TO DEPOSIT TAX?

TDS / TCS is required to be deposited in cash/cheque in Bank through Challan manually or electronically. Electronic payment of TDS/TCS is mandatory for:

(a) All corporate assessees;

(b) Non-corporate assessees who are subject to audit under section 44AB.

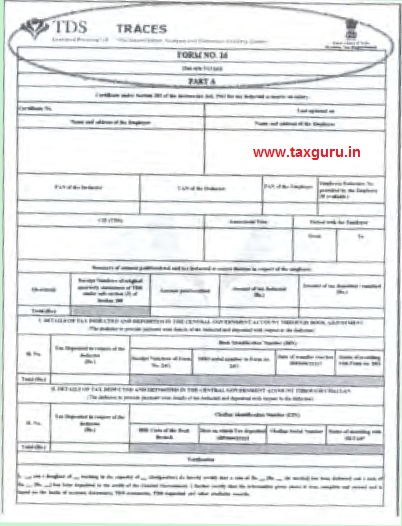

WHAT IS THE FORM OF TDS/TCS CERTIFICATE AND WHAT SHOULD BE THE FREQUENCY FOR ISSUANCE OF TDS/TCS CERTIFICATE?

Every deductor/collector has to issue a certificate to the deductee/collectee in respect of tax deducted / collected by him in following form:

- Download TDS/TCS certificate (Form 16/16A/27D)(www.tdscpc.gov.in) bearing unique TDS certificate number and issue to the taxpayers within due date.

- Part A of Form 16 shows PANs that are reported in Annexure II of 24Q statement for 4th Quarter. Salary details for whole or part of the year in Annexure II of Quarterly TDS Statement for 4th Quarter is mandatory.

Table No. 2

| Particulars | Form No. | Frequency of certificate issuance |

| TDS certificate on salary | Form 16 | Annually |

| TDS certificate on payments other than salary | Form 16A | Quarterly |

| TCS certificate | Form 27D | Quarterly |

| TDS certificate on purchase of immovable property | Form 16B | 15 days of filing 26QB |

| TDS certificate on rent | Form 16C | 15 days of filing 26QC |

Multiple payments can be clubbed in quarterly TDS/TCS certificate

WHAT IS THE DUE DATE FOR ISSUANCE OF TDS/TCS CERTIFICATE?

Table No. 3

| Form No | Due date |

| Annual Form No.16 | 15th June following the financial year. |

| Quarterly F 16A/F 27D | See column 3 & 5 of table no. 5 |

W.e.f. 01/04/2012 it mandatory to issue TDS certificate only 16A downloaded from www.tdscpc.gov.in. The deductor shall verify the correctness of contents & authenticate it by digital or manual signature. It is only then a valid certificate.

WHAT ARE THE CONTENTS OF A TDS/TCS CERTIFICATE?

a. The TDS/TCS certificate contains the following details:

(a) Valid PAN of the deductee;

(b) Valid TAN of the deductor/collector ;

(c) Challan Identification Number (CIN), which is a number generated by a combination of BSR code of the bank where tax is deposited, date of deposit and the challan serial number allotted by the bank;

(d) Receipt number of the relevant quarterly statement of TDS/TCS (i.e., TDS/TCS return).

WHAT IS STATEMENT OF TDS/TCS AND IN WHICH FORM IT IS TO BE FURNISHED?

- Every person responsible for deducting/collecting tax at source must furnish TDS/TCS statement.

- Correct Reporting: Cancellation of TDS/TCS statement and deductee row is no longer permissible. Accordingly, it is very important to report correct and valid particulars (PAN/TAN/catogry etc) in the quarterly TDS/TCS statement.

- Quote correct and valid lower rate TDS/TCS Certificate Number in TDS/TCS statement in case of lower deduction. The deductor/collector can verify the Lower TDS/TCS Certificate number online on the TRACES website www.tdscpc.gov.in.

- Last provisional receipt number to be quoted in regular TDS/TCS statements: While filing new regular (original) TDS/TCS statement, it is mandatory to quote the last accepted provisional receipt number of the regular quarterly TDS/TCS statement of any form type.

- TDS/TCS statement cannot be filed without quoting any valid challan and deductee row.

- Download TAN-PAN Master from TRACES and use the same to file new statement to avoid quoting of incorrect and invalid PAN.

- Validate PAN and name of fresh deductees from TRACES before quoting it in TDS statement.

- File correction statements promptly in case of incomplete and incorrect reporting. The TRACES website tdscpc.gov.in provides the facility for Online Correction of Statements.

- Government deductors should obtain BIN (Book Identification Number) from their Accounts Officer (AIN holder) in time and quote the same correctly in TDS/TCS statement.

Table No. 4

| Statement in respect of TDS/TCS | TDS/TCS statement Form |

| TDS on salary | Form No. 24Q |

| TDS on payment other than salary to a non- resident or a foreign company or a resident but not ordinarily resident. | Form No. 27Q |

| TDS on payment other than salary to any person other than above. | Form No. 26Q |

| TCS | Form No. 27EQ |

| TDS on sale of immovable property | Form No. 26QB |

| TDS on payment of rent by certain individual or HUF | Form No. 26QC |

WHAT IS THE FREQUENCY & DUE DATE OF SUBMISSION OF TDS/TCS STATEMENT?

Due dates for filing of TDS/TCS statement

Table No. 5

| Quarter ending on | Due date of TDS statement | Due date | Due dates of TCS Statement | Due date for 27D |

| 30th June | 31st july | 15th Aug | 15th july | 30th july |

| 30th Sept | 31st October | 15th Nov | 15th October | 30th October |

| 31st Dec. | 31st January | 15th Feb | 15th January | 30th jan |

| 31st March | 31st May | 15th June | 15th May | 30th May |

WHAT ARE THE CONSEQUENCES OF TDS/TCS DEFAULTS AND NON-PAYMENT TO GOVERNMENT?

- Failure to deduct tax or short deduction of tax or failure/delay in payment of the tax deducted to the credit of Government by the due date, would make the deductor an assessee in default in respect of such tax and also liable to penalty which is equal to the amount for which the assessee is a deemed defaulter.

- In case of non-deduction/short deduction or delay in deduction of tax, interest @ 1 % per month or part of the month is levied on the tax deductible and in case of delay in payment of tax after deducting, interest @ 11/2% per month or part of the month, till such time the tax deducted is not credited to the Government shall also be payable.

- In case of delay in payment of tax after collecting, interest @1% per month or part of the month till such time the tax is not paid.

- Failure on part of the deductor to pay the tax deducted at source, to the credit of Central Government makes him liable to rigorous imprisonment of a minimum period of three months but which may extend to seven years.

- Delay in filing TDS/TCS quarterly statements attracts:

- late fee of Rs. 200/- per day for each day of default, subject to certain limits (u/s 234E).

- Minimum Penalty of Rs. 10,00* (may be extended to Rs. 1 Lakh).(u/s 271 H)

- Download the justification report to know the details of TDS/TCS defaults, if any, on processing of TDS/TCS statement from the TRACES website tdscpc.gov.in

WHAT ARE THE CONSEQUENCES OF DEFAULT IN FURNISHING STATEMENT/ FILING INCORRECT INFORMATION THEREIN?

- With effect from 1st July 2012, failure to file TDS/TCS statement within the prescribed time shall make the deductor/collector liable to pay by way of fee u/s 234E, a sum of two hundred rupees for each day during which the default continues.

- With effect from 1st July 2012, furnishing of incorrect information in the statement by the deductor/collector would make him liable to penalty, which shall not be less than ten thousand rupees but which may extend to one lakh rupees.

- In case the delay in filing TDS/TCS statement is more than one year from the prescribed date, then the deductor shall be additionally liable to pay a minimum penalty of ten thousand rupees which may extend to one lakh rupees.

- Failure to apply for TAN or quote correct TAN by the deductor may result in levy of penalty of ten thousand rupees.

- Late filling fee u/s 234E, being statutory in nature, cannot be waived off.

AGGREGATED TDS COMPLIANCE

- The PAN of an entity (Central Office, Headquarter etc.), having more than one TAN of its branches, associated with the referenced PAN, can review the “Aggregated TDS Compliance” report on a regular basis for a summary TDS compliance at Organization level.

- This feature provides for a summary of TDS defaults of all respective TANs across all Financial Years, which assists in effective TDS administration, monitoring, control and compliance at Organization level.

- The feature will be extremely useful for the purpose of complying with the provisions of Section 40(a)(ia) of the Income Tax Act, 1961 by the concerned entity, to ensure that correct information is disclosed in paragraph 21(b) & 34(b) of the Tax Audit Report (Form 3CD u/s 44AB the Act).

- To use this feature, the deductor needs to register on TRACES with its PAN.

WHAT IS THE FORM OF FILING STATEMENT OF TDS/TCS?

The statement of TDS/TCS can be filed either in:

(1) Paper form (for less than 20 deductees).

(2) Electronic form : Form No. 27A is also to be furnished along with return on electronic form.

Following deductors/collectors have to file the statement of TDS/TCS in the form specified in electronic form only.

(a) Deductor who is an office of the Government; or

(b) Deductor who is a company; or

(c) Deductor who is a person who is required to get his accounts audited under section 44AB in the immediately preceding financial year; or

(d) Deductor in whose case the number of deductee’s records in the quarterly statement for any quarter of the financial year is equal to or more than twenty.

Note: In case of any other deductor/collector, furnishing the quarterly statement in electronic form is optional.

WHAT IS THE DUTY OF DEDUCTOR/COLLECTOR IF THE DEDUCTEE DOES NOT FURNISH HIS PAN?

If the deductee does not furnish PAN or furnishes incorrect PAN to the deductor/collector, the deductor/collector shall deduct tax at source at higher of the following rates:

(a) the rate prescribed in the Act; or

(b) at the rate in force, i.e., the rate mentioned in the Finance Act; or

(c) at the rate of 20%.

TDS is to be deducted on the bill amount and not on the GST. Can you give the notification as some clients deduct the tax on the total bill amount which is including the GST.