Background: The National Pension System (NPS) is a pension cum investment scheme launched by the Government to provide old age security to Citizens of India. It brings an attractive long-term saving avenue to effectively plan your retirement through safe and regulated market-based return. Contribution in the NPS can be made by employee himself or his Employer and by any person not in the Employment, i.e. self-Employed.

From the Income Tax point of view, it is an attractive scheme as the subscriber in the NPS is entitled to get additional tax benefit up to Rs. 50,000 in a financial year u/s 80CCD (IB) of Income Tax Act which is over and above the deduction of Rs. 1,50,000 available u/s 80C /80CCE of Income Tax Act. Earlier the tax-free withdrawal on retirement were allowed up to 40% of corpus, which has been increased to 60%.

Features of the Scheme

1. Types of Account under NPS

Tier I Account

Tier II Account

Tier I A/C is a mandatory retirement account and offers various tax benefit, whereas Tier II A/C is a voluntary saving Account associated with your PRAN and does not give any tax benefit. From Tier II A/C, money can be withdrawn at any point of time.

2. Who can Join NPS: NPS is open to all citizens of India between the age of 18 and 65 on a voluntary basis. An NRI can also join subject to regulatory requirement.

3. How to join the Scheme: Visit to the site https://enps.nsdl.com/eNPS for opening of NPS account. NPS account may be opened in the specified bank also.

4. Tax Benefit on Contribution to NPS

| Topic | Section | Description |

| Employee Contribution | 80CCD (1) | Deduction up to 10% of Salary (Basic + DA)

10 % of GTI (for self-employed taxpayer). This is within the overall ceiling of Rs.1,50,000 u/s 80C/80CCE |

| Additional Contribution from Employee | 80CCD (IB) | Addition deduction up to Rs. Rs.50, 000

This is over and above the limit of Rs 1,50,000 u/s 80C/80CCE |

| Employer Contribution | 80 CCD (2) | 10%* of salary (Basic + DA)

Employer can claim as business expenses u/s 36 of IT Act. *14% from 01.04.2019 if employer is Central Government |

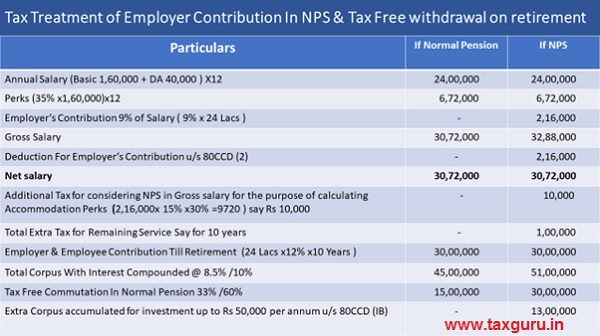

5. Tax Treatment of Employer Contribution In NPS

Any payment made by the Employer to employees NPS account is a part of Gross Salary and thereafter the same is deducted as deduction u/s 80 CCD (2) of Income Tax Act up to 10%/14% of salary (Basic + DA). The calculation is explained with an example is as under with respect to Non-Government employee:

Since the contribution in NPS is normally made within, 10%/14% limit so it does not impact in net salary of employee as the addition and deductions are made with the same amount. Since the Employer contribution becomes the part of Gross salary, the same is considered while calculating the accommodation perks. By this way accommodation perks gets little bit fatty. But if we compare the Tax-free cash withdrawal (60 %) at the time of retirement in NPS with other pension scheme in which it is normally 33%, the extra tax paid on perks is offset with the higher tax free cash withdrawal in NPS .The employees who are on HRA does not get affected at all with the above treatment.

6. Tax Benefit On Withdrawal of Corpus under various situations

I. Withdrawal of Corpus on Retirement: Currently, on retirement or on reaching the age of 60, NPS subscribers are allowed to withdraw 60% (Tax free) of the corpus while 40% has to be invested in annuity plans for getting regular pension.

II. Partial Withdrawal From NPS: Pre mature withdrawal is not allowed from the scheme, however for some specific purposes (say Higher education of children, marriage of children, Treatment of Critical illnesses, Housing etc.) partial withdrawal can be allowed up to the extent of 25% of employee contribution. Let us suppose there is a corpus of Rs. 15 Lacs of an employee Mr X. the Corpus has a mix of Employee contribution of Rs. 7 Lacs and Rs 8 Lacs of Employer. This corpus of employee consists of Rs 6 lacs of contribution and Rs 1 lac of Interest. Here 25% out of contribution i.e. Rs 1.50 Lacs (25% of Rs 6 Lacs) only can be allowed to be withdrawn without any tax implication.

III. Closure of NPS before Retirement: 20% of the corpus can be withdrawn (Tax Free) and remaining 80% will have to be utilized for purchase of annuity.

IV. Death Benefit: Full withdrawal (Tax Free) by the nominee is allowed. However, if annuitized by nominee, the pension income would be taxed as per nominee’s income tax slab.

V. Purchase Of Annuity : Amount invested in purchase of Annuity, is fully exempt from tax. However, annuity income (Pension) will be subject to income tax.

VI. 100% Tax Free Withdrawal if Corpus is up to Rs 2 Lacs: Subscriber can claim 100% Withdrawal if the total accumulated corpus is less than or equal to Rs. 2 Lakh at the time of Superannuation/attaining age of 60 years without any Tax.

VII. Subscriber can withdraw lump sum amount in 10 instalment: Subscriber can opt for withdrawal of lump-sum amount in a phased manner (up to 10 instalments) over a period up to 70 years without any tax implication. However, Subscriber has to buy Annuity prior to Phased Withdrawal.

7. Investment Choice: Subscribers can select any of the two investment Choice:

Auto Choice: Under this option, funds of the subscriber are automatically allocated amongst three funds E (Equity Fund), C (Corporate Bonds) and G (Government Bonds) in a pre-defined portfolio pattern prescribed by PFRDA. When a subscriber chooses this option, it adopts a lifecycle-based approach, in which the allocation to Equity decreases gradually as the subscriber’s age increases. Subscribers are given three types of funds to choose from as follows:

| Fund Nature | Fund Type | Equity allocation |

| Aggressive Fund | Type E | Maximum equity allocation 75% |

| Moderate Fund (default option) | Type C | Maximum equity allocation 50% |

| Conservative Fund | Type G | Maximum equity allocation 25% |

Active choice – Under this option, subscriber selects the allocation pattern amongst the three types of funds namely E, C and G. The Maximum allocation to Equity can be 75%. In the Corporate bonds or Government bonds, it can be 100%. NPS subscribers can change their investment Choice and asset allocation ratio ‘twice’ in a year.

8. The Pension Fund Managers (PFM): At present, there are 8 PFMs. These are UTI, SBI, LIC, Kotak, Reliance, ICICI Prudential. HDFC, Birla Sun Life. However, Subscriber can change the pension fund manager once a year.

9. Regulator of NPS : The pension scheme is administered on behalf of the Government by the Pension Fund Regulatory and Development Authority India (PFRDA). (http://www.pfrda.org.in/)

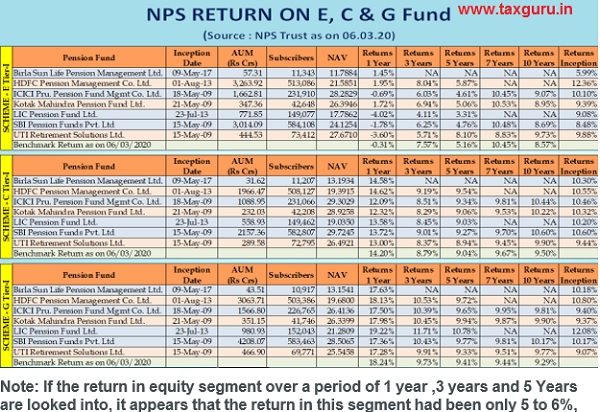

10. Past Performance of Various Scheme In The Last 10 Years By Different PMC (As on 06.03.2020 From Website of NPS trust )

Note: If the return in equity segment over a period of 1 year ,3 years and 5 Years are looked into, it appears that the return in this segment had been only 5 to 6%, whereas in the Non-Equity segment namely (Corporate Bond and Government Bond)) it is fairly high which is around 10%.

11. Whether Multiple NPS A/C is allowed in one PAN : No

12. Exit Options and Tax Benefit From NPS on Superannuation/at the age of 60:

i. Continuation of NPS A/C: Subscriber can continue to contribute to NPS beyond the age of 60 years/superannuation (Up to 70 years). This contribution beyond 60 is also eligible for tax benefits which is normally available under NPS.

ii. Deferment (Annuity as well as Lump sum amount): Subscriber can defer withdrawal as well annuity and stay invested in NPS up to 70 years of age. Subscriber has choice also to defer only one i.e. either lump sum Withdrawal or Annuity only.

13. From where shall I get the tentative pension amount offered by ASPs.

The pension amount can be calculated based on indicative annuity rates (subject to change from time to time) provided by Annuity service provider (ASPs) . The Pension Fund Regulatory and Development Authority (PFRDA) has empanelled the seven IRDA approved life insurance companies for providing annuity services to the subscribers of National Pension Scheme. However, the actual annuity amount will depend on the prevailing rates at the time of purchase of annuity.

14. Accumulation Of Corpus:A person start contributing Rs. 50, 000 u/s 80CCD (IB) at his young age say at 30 years gets accumulated corpus of Rs 95 Lacs assuming a return @ 10 %.

15. Conclusion: While it is true that NPS returns are, market-linked and therefore bound to be volatile even for Corporate Bond and Government Securities. However, if remain invested for longer period, return may be higher than the return on traditional investment. It gives transparency in the sense that you can view your investment status at any time besides facility of various switching options.

Disclaimer: The views expressed herein are the personal view and opinion of the author and in no way invoke any one to join or subscribe to the scheme. If anyone desire to invest in the scheme, he will be doing at his own risk and therefore advisable to consult your investment advisor before taking any decision and entering into NPS.

How to reach author: Author is working in the Tax Department of a reputed PSU and can be reached at deepakjauhari@powergridindia.com

Author Bio

My age is 44 & I have lost my Job; to live my livehood I want to withdraw my corpus from my NPS account (Tier 1); pls let me know how much Taz will get deducted in this scenario.

Interest acrual aspect of nps is not given in the diascussion.

For example in PPF interst is acrued on 31st march of every year. In case of fixed depoit interest is acrued on the date of opening every year.

Please clarify that an employer gives contribution to NPS for a period of date of joining to October 2017 period of employee along with interest for the delayed period and same also invested to NPS account. In this circumstance what will be the tax treatment in per view of employer regarding TDS on salary and in Per view of employee for his deductions under section 80ccd ( 2). Can relief be claimed under section 89 subsection 1 regarding principal and deduction regarding deposit and compensating interest thereon.

Pl.clarify that if corpus is less than 2 lacs and 100%amount is withdrawn at 60 years of age, whether this amount is added to taxable income? If Yes, how much % is added to taxable income.

on retirement 60 percent of NPS withdrawal Will be shown in ITR or not?

IV. Death Benefit: Full withdrawal (Tax Free) by the nominee is allowed. However, if annuitized by nominee, the pension income would be taxed as per nominee’s income tax slab.

Full withdrawal means total market value as on date

VI. 100% Tax Free Withdrawal if Corpus is up to Rs 2 Lacs:

Somewhere I have read that this withdrawal amount gets added to taxable income.

Please clarify

Sir,

What are taxation rules on withdrawl of NPS tier 2 account.

Can you please help me to withdraw the money as I have crossed 60 years of age

CCD 1b benefit of 50000 and increased tax free withdrawal of 60percent is old story!