Introduction:-

Gifts are usually capital receipts by nature. The Income Tax Act, 1961 (‘Act’) which is levies tax on incomes, that is revenue receipts, carves out certain exceptions and levies tax on capital receipts as well. Gifts are one such receipt. The Act defines gifts as any asset received without consideration like money or money’s worth (in kind). It can include Cash, movable property, immovable property, jewellery, etc. If such gifts are received from a close relative, it is not taxable. If received from others, the value if equal to less than Rs. 50,000, no tax is levied on the recipient. But if the value exceeds Rs. 50,000, the whole amount is taxable under the head “Income from Other Sources (IFOS)” as per the prevalent slab rates or rates of income tax.

Till 1st October, 1998 all gifts including gifts to relatives (barring few exceptions) were chargeable to tax under the hands of the giver under Gift Tax Act, 1957 at flat rate of 30%. Later from assessment year 2005-2006 the concept of recipient based taxation on gifts was introduced to curb the practice of tax planning/tax evasion.

Which gifts are taxed under the Act?

- Gifts received by Resident Individuals and HUF’s

- From whichever source, wherever situated

- Received wherever in the world

- Gifts received by Non-Residents / Not Ordinary Residents

- Received or deemed to be received in India

- Accrues or Arises (or is deemed to) in India

The Act provides source based taxation as well under certain cases and therefore if the source (the giver) is in India, Gift may become taxable

Relatives Under Income Tax Act, 1961:

“Relatives” is defined as follows in case of Individuals under the Act:

| Following are the exceptional cases, wherein the taxability does not arise in case any sum of money, specified movable/immovable property is received:

(there is no ceiling limit and therefore, entire sum of money or property received shall be exempt from tax)

|

From any Relative |

| On the occasion of marriage of the Individual | |

| Under a will or by way of inheritance | |

| In contemplation of death of the payer or donor, as the case may be | |

| From a local authority | |

| From any fund, university, hospital, medical institution | |

| From any Trust or institution registered under the Act | |

| Given by Individual to trust for benefit of relative | |

| From holding company to 100% subsidiary company or vice versa |

Taxation Of Gifts:

The Gifts received are usually without consideration. In certain scenarios the gifts consist of some consideration whether in money or in kind the value of which is neglible. The Act has also brought such bogus transactions in the name of gifts under taxation by introducing the term “Inadequate Consideration”. Thus any asset received from a person other than relatives for Inadequate Cosideration attracts tax under the head “Income from Other Sources” Let us understand all the scenorios of taxation under one chart:

(Note: FMV stands for Fair market value and SDV stands for Stamp Duty Value)

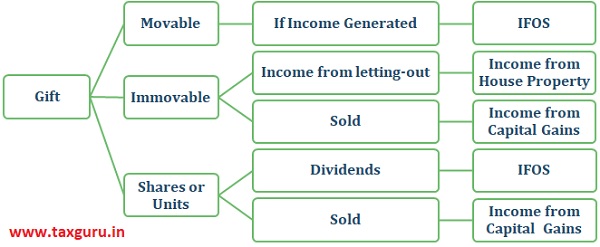

Taxability Of Income Generated From Gifts Received:

Gifts received are tax free as per the specified limits but if any income is generated from it, the same is taxable as per the respective heads of the Act. Let us understand the Income and its taxability based on the nature of assets:

Conclusion:

- All other personssuch as Firm, Company, AOP’s, BOI’s are excluded from exemptions, but they can be the giver.

- Gifting won’t result in Evasion of Tax.

- Any Income arising from the Gift received is Taxable.

- A Gift Deed is highly recommended when a person wishes to gift his property or any amount of money to a relative or any other person.

- Any person beyond the definition of relative is not a relative under the Act.

- Gifts received by NRI’s arealso taxable. This means that regardless of destination of the receiver, the Origin of the Gift is relevant for the purpose of Taxation in India.

(This article represents the views of the authors only and does not intent to give any kind of legal opinion on any matter)

Authors:

Ashish Raithatha | Consultant | +91-9819911153 | ashish.raithatha@masd.co.in

Kushal Mehta | Associate Consultant | +919930612247 | kushal.mehta@masd.co.in

Author Bio

If I receive GIFT in cash from my daughter, is it taxable?

gift received from cousin brother will be covered as gift from relative u/s 56(2)(v) or not please guide.

If gift recd from father in law of Rs. 650000 through Bank transfer is taxable?

if i deposit 251000 cash received from grandmother on birthday as a gift i taxable

as per your tree diagram for relatives, gifts received from nephew or niece will also be exempt from the tax, however it seems it is not mentioned in the definition proveded in the Act. could anyone confirm?

What is the tax liability of a wife who has inherited all movable and immovable property from her deceased husband, assuming this inheritance is by way WILL registered by the deceased husband?

Dear Sir,

Can NRI having OCI Cardholder, make a private family trust in India for his son, who is also NRI, Funds being transferred from his NRO A/c. on non-repatriation basis.

Can the Trust lend this money to other Trust on interest? Will the limitation of 3 years will be applicable on the funds so given as loan?

How about the grand children in the definition of relatives ,for the purpose of gift tax ?

Yes. As per Income Tax Act any lineal ascendants and descendants of an Individual are convered under the definition of relatives. Accordingly Grandchildren’s being the lineal descendants of an Individual are considered as relatives