1. WHAT IS ESOP?

ESOP means Employees Stock Option Plan. It enables employees to buy company share at discounted price. Start-ups have great business idea but a limited financial resource to operate in the initial years. It is popular these days as starts-ups generally use ESOP to attract and retain highly talented employees for long term in low salary which gives them sense of ownership in company.

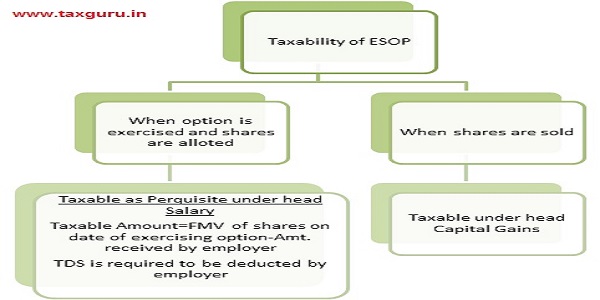

2. TAXABILITY OF ESOP UNDER INCOME-TAX ACT

The taxation of ESOPs is split into two components:

a) Tax on perquisite as income from salary at the time of exercise of option.

b) Tax on income from capital gain at the time of sale.

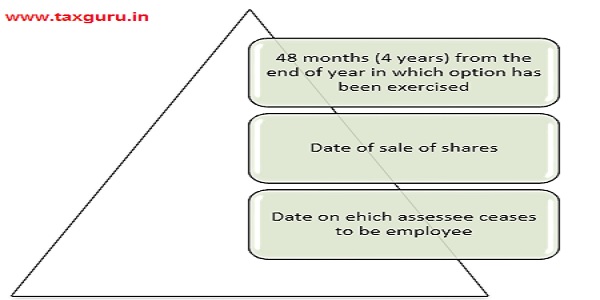

2. AMENDMENT MADE IN BUDGET 2020 APPLICABLE FROM 1ST APRIL 2020

- Tax on perquisite is required to be paid at the time of exercising option which may lead to cash flows problem as this benefit of ESOP is in kind. In order to give boost to start-ups ecosystem, payment of tax at the time of exercising option has been deferred to earliest of following dates-

Payment shall be made within 14 days of above dates.

Perquisite shall be chargeable in year of exercising option but payment shall be made at deferred dates.

For Example-

XYZ Pvt. Ltd. is start-up and it granted 100 stock options to Mr. A on 01/07/2016 i.e. A.Y.2017-18 at discounted price of Rs.400/- per share. Vesting period is 4 years. Mr. A exercised option on 01/07/2020 when Fair Market Value of shares is Rs.900/-. Taxability in this case shall be determined as follows-

| Particulars | Pre-Amendment | Post-Amendment |

| Taxable amount on date of exercise of option i.e. 01/10/2020 as perquisite under the head salary=

FMV of shares=90000 (100 shares@Rs.900 per share) Less: Amount paid by employee=40000 (100 shares@Rs.400/share) |

50000 | 50000 |

| TDS to be deducted | Yes, in F.Y.2020-21. Suppose rate in force is 30%, then TDS deducted shall be of Rs.50000 *30% = 15,000 and will be paid to credit of Central Govt. | No, not in F.Y.2020-21 but after deferred period. |

| Cash Outflows | In year 2020-21 of Rs.15000/- out of Salary | Not in year 2020-21 but in later year out of salary or sale proceeds as the case may be |

3. TDS OBLIGATION UNDER DIFFERENT SCENARIO

| Particulars | Scenario-1:He does not sell the shares and continues working for 5 years | Scenario-2:He continues working with the employer but sells the shares on 31.01.2025 | Scenario-3:He does not sell he shares but leaves the job on 31.12.2023 |

| Income chargeable to tax in F.Y.2020-21 | Yes | Yes | Yes |

| Date of TDS obligation | 01.04.2026(i.e. 48 months after end of A.Y.) | 01.02.2025 | 01.01.2024 |

| Due date for deduction or payment of TDS(14 days) | 14.04.2026 | 14.02.2025 | 14.01.2024 |

| Cash Outflows | Out of salary income | Out of sale proceeds | Out of salary income |

4. CONSEQUENCES OF DEFERMENT OF TDS OBLIGATION

- Employer can claim expenditure without any disallowance u/s 40(a)(ia)/(iii) since there is no obligation to deduct TDS.

- Further increase or fall in price of shares is not relevant since tax liability has been crystallized in year of exercising option. Law only provides for deferment of tax payment.

- This amendment only cover sale of shares and not transfer. Therefore transfer of share in other manner like gifting of shares, transfer by way of amalgamation, exchange would not be covered under this section.

- This amendment is applicable only to start-ups being company or LLPs incorporated during 01/04/2016 to 31/03/2021 whose total turnover does not exceeds 100 cr and holds certificate of business from Inter-Ministerial Board of Certification.

- Employee is not under obligation to make direct payment of taxes u/s 191 of Income-tax Act, 1961 if employer does not deducts TDS.

- Rate of TDS shall be rate in force. It means rate specified in Finance Act for relevant A.Y.

5. OTHER LAWS-

ESOP is also regulated by Companies Act 2013, SEBI Regulations and Exchange Control Regulations (FEMA). Due considerations is required to all the laws attracted.

6. OUR COMMENTS-

ESOPs are great way to retain employees for long term as it gives a sense of ownership in company. Start-up in initial years requires support and care to flourish their business. ESOPs help them in meeting targets with cash crush. Start ups are engine in growth of economy and Govt. has taken several measures to support them. One such measure is deferring payment of taxes when option is exercised. Formation and regulation of ESOP requires lots of consideration. There are many angles to be seen like ESOP in case of resident, non-resident employee, parent and subsidiary company, employee send outside India, implications of different laws attracted, etc. It obviously needs help of an Expert.

*****

The above comments do not constitute professional advice. The Author can be reached at companyfinancialtree@gmail.com or visit website www.financialtreecompany.com . My name is CA Divya Agrawal and I am Practising Chartered Accountant, CEO and Founder of FINANCIAL TREE COMPANY (An online return filing and Tax Consultancy Company) where we have taken an initiative that allows person to Pay from Heart. We also upload educational videos in You tube and name of our channel is FINANCIAL TREE COMPANY. Our aim is to help people in improving their financial health by spreading knowledge and love. Stay Financially Fit and Healthy.

This provision apply only for ‘Eligible start-ups’ which is defined separately. All newly started company can not be called as Startup

Kindly rectify the figures of taxable amount on date of exercise of options from Rs. 50,000/- to Rs. 86,000/-

very helpful