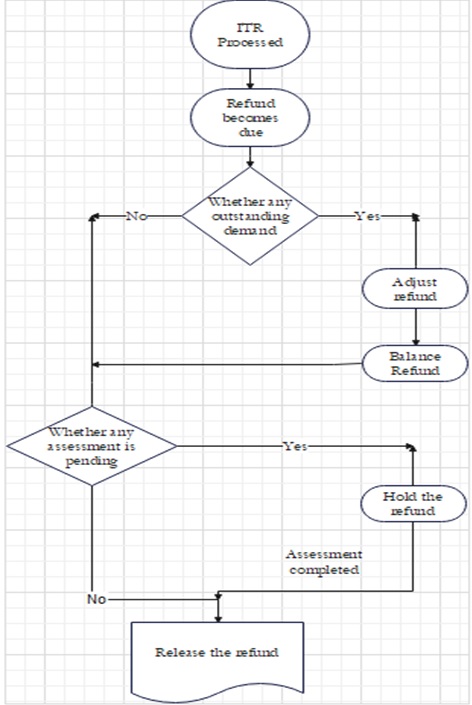

One of the common issues faced by taxpayers is the mismatch between the income tax refunds claimed and the income tax refunds received. Sometimes, the Income Tax Department may adjust the refund due to a taxpayer against any tax demand outstanding from the same or any other assessment year. This adjustment is done under section 245 of the Income Tax Act, which gives the department the power to set off any refund against any tax liability.

However, the department cannot make such an adjustment without giving an opportunity to the taxpayer to explain his or her position. Section 245 requires the department to send an intimation to the taxpayer before making any adjustment, stating the amount of refund due, the amount of tax demand outstanding, and the proposed adjustment. The taxpayer is given a chance to respond to the intimation within 30 days, either agreeing or disagreeing with the adjustment.

If the taxpayer agrees with the adjustment, the department will proceed to adjust the refund against the demand and issue the balance refund, if any, to the taxpayer. If the taxpayer disagrees with the adjustment, and the claim of the Assessee is found not to be true based on the information available with the Assessing Officer and explanation provided by the Assessee, the department may still adjust such refund.

In such cases, the taxpayer should submit a response to the intimation under section 245, along with the relevant documents and evidence to support his or her claim. The response can be submitted online through the e-filing portal of the department. The taxpayer should also check the status of the tax demand and the refund on the portal and rectify any errors or discrepancies.

Before the beginning of Financial Year 2023-24, Section 241A of the Act empowers the Assessing Officer, in case where a refund becomes due to an Assessee after processing the ITR but the Assessment/reassessment proceeding(s) are pending against him, to hold the refund till the date of completion of such assessment/reassessment, if he is of the opinion that the grant of refund is likely to adversely affect the tax revenue of the Government. Such withholding can be done only with the prior approval of the Principal Commissioner or Commissioner, and applicable to assessment years on or after 2017-18.

The Finance Act, 2023, substituted Section 245 of the Act and merged Section 241A with this Section. Actually, earlier, these Sections were overlapping each other and creating a lot of hustles among the taxpayers. Where department would proceed to hold the refund owing to pendency of assessment, the Assessee would take the plea of Section 245 and the litigation on this issue kept creeping up.

Therefore, now it has been provided in Section 245 itself that where a part of the refund has been set off or where no amount is set off, and refund becomes due to a person but the assessment/reassessment proceeding is pending, then, the Assessing Officer may withhold the refund till the date on which such assessment or reassessment is completed with the approval of the Principal Commissioner or Commissioner.

Further, it has also been provided by amending Section 244A of the Act that interest on income tax refund shall not be given for the period starting from the date of holding the refund till the date of completion of assessment/reassessment.

It is also noted that the Assessing Officer can hold the refund (where assessment/reassessment proceeding is pending) only when the refund amount is more than Rs. 10 lakhs. That means if after adjusting refund, the balance refund amount is less than Rs. 10 lakhs, the Assessing officer cannot hold the refund even if the assessment/reassessment proceeding is pending.

To summarize the above, we would like to depict the whole scenario in a flow-chart for the better understanding of the readers:

Conclusion

Understanding the set-off and adjustment of income tax refunds is crucial for taxpayers navigating the complexities of the tax system. The recent amendments introduced by the Finance Act, 2023, aim to simplify the process and reduce disputes. Taxpayers should stay informed, respond promptly to intimations, and utilize online portals to ensure a smooth resolution of refund-related issues.

About the Author

The author is Ruchika Bhagat, FCA helping foreign companies in setting up and closing businesses in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants is a well-established Chartered Accountancy firm founded in the year 1997 with its head office in New Delhi.