Section 80EEA Deduction in respect of Interest paid on Loan Taken for Acquisition of Residential House Property (Affordable Housing)

{Sec. 80EEA as introduced by Finance Act, 2019.}

Q 1. Who is eligible to get benefit under this Section 80EEA?

Ans: An Individual who has taken a Loan for acquisition of residential house property from any Financial Institution.

Q 2. What is the benefit accruing to the Eligible Assessee under Section 80EEA?

Ans:Interest payable on such loan would qualify for deduction under this section.

Q 3. For what Period the benefit can be enjoyed?

Ans: The benefit of deduction under this section would be available from A.Y.2020-21 and subsequent assessment years till the repayment of loan continues.

Q 4. What is the Amount of deduction an Eligible Assesse can get under Section 80EEA?

Ans: The maximum deduction allowable is ₹150000/-. The deduction of up to ₹150000/- under section 80EEA is over and above the deduction available under section 24(b) in respect of interest payable on loan borrowed for acquisition of a residential house property.

Note: – In respect of self-occupied House Property, interest deduction under section 24(b) is restricted to ₹ 200000/-. In case of let out or deemed to be let out property, even though there is no limit under section 24(b), section 71(3A) restricts the amount of loss from house property to be set-off against any other head of income to ₹ 200000/-Accordingly, if interest payable in respect of acquisition of eligible house property is more than ₹ 200000/- the excess can be claimed as deduction under section 80EEA, subject to fulfillment of conditions.

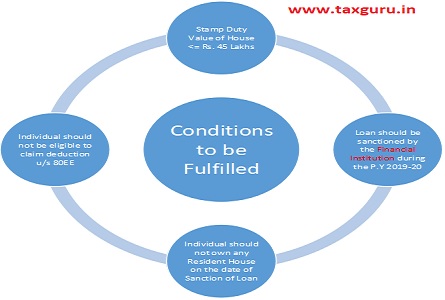

Conditions to be fulfilled: –

Note:

- For claiming Interest deduction U/s.24, it is to note that the amount may be borrowed from either of the Financial Institution/from friends/from relatives.

- But to get deduction under this section, one need to borrow from Financial Institutions only.

Example:

Mr. B incurred an Interest Expense of Rs. 250000/- on the amount borrowed for acquisition of Residential House Property. What are the deductions available to him for the A.Y 20-21 w.r.t Interest Expense?

Mr. B can claim deduction with respect to Interest Expense as follows:

- 200000/- can be claimed in Sec.24(b)

- Balance Rs.50000/- can be claimed in Sec.80EEA

Author Bio

Can 80EEA be availed on Home loan transfers?? Like, I have taken loan in FY 2018-19 and in FY 2021-22 i have transferred loan to a new lender. Having satisfied all the other conditions can we avail the above 80EEA limit over and above u/s 24

Can 80EEA be availed on Home loan transfers?? Like, I have taken loan in FY 2018-19 and in FY 2021-22 i have transferred loan to a new lender. Having satisfied all the other conditions can we avail the above 80EEA limit over and above u/s 24

Hi Rupesh,

Did you received response for the query from Taxguru? I have similar query, can you help me if you got any response?

Regards,

Vishnu

But for claiming under 80EEA , does the Construction of House should complete? or we can start claiming on the interest portion while is house is under construction itself?

if any self occupied employee availed HBA in the F/Y-2019-2020 He can eligible for 80EEA or not

Question for Tax Expert:

I had booked a flat at “ABC Project” at Greater Noida in June 2019 during FY 2019-20. I have got the possession along with Registry completed on 2nd Dec 2020 (during current FY 2020-21).

Property is in my name with my Mother as Co-Applicant (added for Honorary purpose). I have availed the home loan from bank, and I am paying all the PEMI and EMI’s from my income. Mother is housewife aged 66 years and she is not contributing to EMI’s of course.

I need help with the following questions:

1. The property is currently vacant, I think it would be considered as Self Occupied? Neither I have any property in my name, nor my Mother has any property in her name. We live in New Delhi and this property is in Greater Noida, Gautam Budh Nagar District, UP.

2. What all tax benefits I can claim for current FY 2020-21 in terms of interest, principal and pre-EMI. My Pre EMI’s started from July 2019 till Nov 2020. December 2020 onwards I paid full EMI’s.

a. During the year 2019-20, my PEMI was INR 1,55,775 thus 1/5th of that = 31,155 can be claimed during 2020-21. Please confirm?

b. During the year 2020-21; I have paid PEMI= 134707 plus Interest of 62135 , thus total is 196842

c. Grand Total of a and b is 31155 + 196842 that is 227,997

Therefore, can I claim INR 2 lac in Section 24 and rest INR 27,997 under section 80 EEA.

Other facts my property value is INR 28 lac and loan was sanctioned on June 2019. Project was started in 2014 while I started the deal in June 2019 it was ready to move.

My another question is basis this link cleartax.in/s/section-80eea-deduction-affordable-housing#1 around carpet area clause as well. Do I have to face any restriction due to carpet area? As per the clause this restriction is only for projects approved on or after Sep 1st, 2019 but my project is completed even before that. Carpet area for my flat is 780 Sq. ft

3. I hope I can claim deduction under Section 80EEA?

I have also paid INR 196200 as Stamp Duty and INR 26000 as Registration fees? Can I claim this? If yes does Stamp paper (it has amount and our names) along with Registry and the receipt of INR 26000 from Registrar Gautam Budh Nagar Satisfy?

Sir,

The residential property was purchased in 2017. FMV was 58L on which stamp duty was paid in 2017.

Housing loan taken in 2017 for purchase of residential property was transferred from one bank to another in Nov 2019. Total interest amount paid to both the banks amounted Rs. 4.62 L during the y.e. 31/03/2020. Whether eligible to claim deduction under 80EEA?

My home loan is on 14-06-2019, all conditions satisfied but flat is old, the building is completed on 2017, can i take the benifit of 80EEA

Sir, my loan was sanctioned in year 2018 for a particular loan account type and in year 2019 the same loan account was closed and new loan account of another type was opened with loan amount transferred from previous account to new loan account. In this case, am I eligible to claim rebate under section 80EEA ?

Can 80EEA be availed on Home loan transfers?? Like, I have taken loan in FY 2018-19 and in FY 2019-20 i have transferred loan to a new lender. Having satisfied all the other conditions can we avail the above 80EEA limit over and above u/s 24

Can 80EEA be availed on Home loan transfers?? Like, I have taken loan in FY 2018-19 and in FY 2019-20 i have transferred loan to a new lender. Having satisfied all the other conditions can we avail the above 80EEA limit over and above u/s 24!!!!!!

Sir, My loan of Rs. 30 Lakh for a property of 36 Lakh was sanctioned by bank in June, 2018 and now I am paying almost Rs. 2,48,000 as home loan interest this year. I had availed Rs. 2 Lakh deduction u/s 24 previous year and same will be claimed this year, too. But can I avail any more deduction u/s 80EE or 80EEA?