Case Law Details

Sh. Anil Jain Vs DCIT (ITAT Delhi)

On perusal of the provisions of Section 50C(1) of the Act is evident that prior to 1/10/2009, Section 50C was applicable only in a case where the value was adopted or assessed by the Stamp Valuation Authority. The word “assessable” has been inserted by the Finance (No.2) Act, 2009 w.e.f. 01/10/2009. This means, if any property has been transferred through agreement to sale or otherwise, without registration with the Stamp Valuation Authority prior to 01.10.2009, the deeming fiction provided under section 50C(1) of the Act would not apply. However, if the property has been transferred w.e.f. 01/10/2009, and it is not registered with the Stamp Valuation Authority, the value ‘assessable’ by the Stamp Valuation Authority shall be deemed to be the full value consideration, if the sale consideration is less than the assessable value.

In the instant case, the Ld. counsel has filed a paper book before us, in which, page No. 70 has been claimed as agreement to sale for transfer of the property. On perusal of the said document, we find that it is a letter dated 06/11/2008 addressed by the assessee to M/s Ansal Properties and Infrastructure Ltd. In the letter, the assessee has submitted that he had booked a Shop No. BG-5 Rs.4,02,35,76,000/- and requested for transfer of right to purchase of the property in favour of M/s Jagirdar Exports P Ltd. This letter has also been signed by the purchaser party. The change of right to purchase has been confirmed by M/s Ansal Properties and Infrastructure Ltd. on 11/11/2008 subject to approval from the competent authority under the provisions of Urban Land (Ceiling and Regulation) Act, 1976.

From the above facts, we are of the opinion that provisions of section 50C of the Act are not applicable in the case of the assessee as the capital asset involved here was not land or building but it is a right to purchase a building (shop).

FULL TEXT OF THE ITAT ORDER IS AS FOLLOWS:-

This appeal preferred by the assessee is directed against order dated 28/03/2013 passed by the Ld. Commissioner of Income-tax (Appeals)-VIII, New Delhi [ in short ‘the Ld. CIT-(A)’] for assessment year 2009-10 raising following grounds:

1. Because the action for denying the admission of ‘Additional Evidence’………….. to issue in dispute is being challenged on facts & law since defeating the case of substantial justice.

2. Because the action for upholding the addition of Rs.1,15,44,888/- attributable to the difference in the valuation qua the declared amount is being challenged on facts and law.

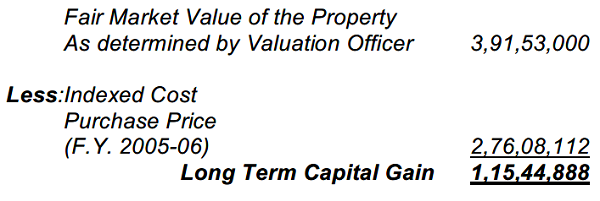

2. Briefly stated facts of the case as culled out by the lower authorities are that in the return of income filed for the year under consideration, the assessee claimed capital loss of Rs.26,28,113/- on sale of property, namely, No. BG-5, Ansal Plaza, HUDCO, New Delhi. In the scrutiny proceedings under section 143(3) of the Income-tax Act, 1961 (in short ‘the Act’), the assessee stated that the said property was purchased on 09/07/2005 for a consideration of Rs.2,44,00,000/- and it was sold for a consideration of Rs.2,50,00,000/- in the year under consideration. The Ld. Assessing Officer referred the matter to the valuation officer under section 55A of the Act for determination of fair market value of the property as on 01/07/2009 (i.e. the date of sale). The Ld. Valuation Officer vide his order dated 27/12/2011 assessed the market value of the property as on 01/07/2009 at Rs.3,91,53,000/- as against Rs.2,50,00,000/- declared by the assessee. The report of the Ld. Valuation Officer was confronted to the assessee. Before the Assessing Officer, the assessee made detailed submission objecting the fair market value adopted for computing the capital gain. In the submission, the assessee also relied on the decision of the Hon’ble Delhi High Court in the case of CIT Vs. Smt. Nilofer I Singh, (2009) 309 ITR 233 ( Delhi). The Assessing Officer did not accept the contention of the assessee on the ground that the assessee did not file any objection before the Ld. Valuation Officer for determination of the fair market value of the property. Accordingly, he computed the capital gain on sale of the property as under:

2.1 Aggrieved, the assessee filed appeal before the Ld. CIT-(A) but could not succeed. The learned CIT-(A) relied on the decision of the CIT Vs. Meerut Cement Co. Private Limited, (2006) 150 Taxmann 7 (ALL) wherein the matter for determination of the cost of construction was referred to the valuation cell and he justified the action of the Assessing Officer in making a reference to the valuation officer.

2.2 Aggrieved, the assessee is in appeal before the Tribunal raising the grounds as reproduced above.

3. The Ld. counsel of the assessee argued ground No. 2 of the appeal challenging the action of the Assessing Officer in replacing the “full value of sale consideration” by “fair market value of the property” for the purpose of computation of capital gain. The Ld. counsel filed a paper book containing pages 1 to 71 including documents supporting purchase and sale of shop.

3.1 The Ld. counsel referred to section 48 of the Act, wherein mode of computation of the capital gain has been specified. He submitted that for the purpose of computing the capital gain cost of acquisition of the asset and any expenditure incurred in connection with transfer of the said is required to be deducted from the full value consideration received or occurring as a result of the transfer of the capital asset.

3.2 He further submitted that in case of capital asset being land or building or both the full value consideration could have been substituted by the value adopted or assessed by the stamp valuation authority in accordance with the provision of section 50C of the Act. He submitted that as per the provisions of Section 50C existed during relevant period, in case the value of the land or building or both was less than the value adopted or assessed by the stamp valuation authority then, value so adopted or assessed shall for the purpose of Section 48 of the Act was deemed to be full value consideration received or accruing as a result of the transfer. He submitted that in the case of the assessee, the property was transferred on agreement to sale and it was not registered with the stamp valuation authority so no value was assessed or adopted by the stamp valuation authority in the case of the assessee. He further submitted that the amendment to include the “assessable value” for the purpose of section 50C of the Act, was only inserted w.e.f. 01/10/2009 and, therefore, provisions of section 50C of the Act were not applicable in the instant case for year under consideration.

3.3 According to him, for the purpose of computation of capital gain, it was not legally allowed to substitute the fair market value in place of the full value of consideration received/accrued. He submitted that in the case of the assessee, the full value consideration received was of Rs.2,50,00,000/- only and accordingly, the Assessing Officer was not justified in computing the capital gain adopting fair market value of the property at Rs.3,91,53,000/-. In support of his contention, he relied on the following case laws:

1. Dev Kumar Jain Vs. Income Tax Officer and Another, (2009) 309 ITR 240 (Del)

2. Commissioner of Income Tax Vs. Smt. Nilofer I Singh, (2009) 309 ITR 233 (Del)

3. Commissioner of Income Tax Vs. Gauranginiben S. Shodhan INDL. (2014) 367 ITR 238 (Guj)

3.4 On the contrary, the Ld. Sr. DR submitted that in the case immovable property has been transferred and, thus, full value of consideration was to be adopted as specified in section 50C of the Act, but the assessee has not filed required documents to establish non-applicability of section 50C of the Act and, thus, the necessary direction need to be issued by the Tribunal in the matter to the Assessing Officer. 3.5 We have heard the rival submissions and perused the relevant material on record. The Ld. counsel of the assessee has contested that in terms of section 48 of the Act, only full value consideration received or accrued by the assessee was only to be taken for computing the capital gain and there was no scope for substituting the full value consideration by the fair market value of the property determined by the Valuation Officer. In the case of CIT versus Smt. Nilofer I Singh (supra), the assessment year involved is 1998-99. The Hon’ble High Court in the said case held that “in case of sale simplicitor, where the full value consideration is the sale price of asset transferred, there is no necessity of computing fair market value and hence AO could not have referred the matter to the Valuation Officer”. The Hon’ble High Court further observed that the reference under section 55A of the Act could be made in the circumstances occurring in section 45(4) and 45(1A) of the Act. In the case of Dev Kumar Jain (supra), the Hon’ble High Court of Delhi following the decision in the case of Smt. Nilofer I Singh (supra) held that “the actual sale consideration recorded in the agreement to sale could not be substituted by the value of the property arrived at by the DVO under section 55A for the purpose of computing the capital gains. In the case of CIT Vs. Gauranginiben S. Shodhan INDL (supra)”, the Hon’ble Gujarat High Court has given similar finding that “reference to DVO for ascertaining the fair market value of the capital asset as on the date of the sale in the case would be wholly redundant.”

3.5.1 We are bound to follow the ratio laid down in above decisions and accordingly the full value of consideration received by the assessee of Rs.2,50,000/- cannot be replaced by the fair market value of Rs.3,91,53,000/- determined by the Ld. DVO. But we also note that as far as transfer of capital assets being land or building or both are concerned, a special provision i.e. section 50C of the Act has been introduced w.e.f. 01/04/2003, which provides for replacement of full value of consideration in certain cases. The said section reads as under:

“Special provision for full value of consideration in certain cases.

50C. (1) Where the consideration received or accruing as a result of the transfer by an assessee of a capital asset, being land or building or both, is less than the value adopted or assessed or assessable by any authority of a State Government (hereafter in this section referred to as the “stamp valuation authority”) for the purpose of payment of stamp duty in respect of such transfer, the value so adopted or assessed or assessable shall, for the purposes of section 48, be deemed to be the full value of the consideration received or accruing as a result of such transfer :

69[Provided that where the date of the agreement fixing the amount of consideration and the date of registration for the transfer of the capital asset are not the same, the value adopted or assessed or assessable by the stamp valuation authority on the date of agreement may be taken for the purposes of computing full value of consideration for such transfer:

Provided further that the first proviso shall apply only in a case where the amount of consideration, or a part thereof, has been received by way of an account payee cheque or account payee bank draft or by use of electronic clearing system through a bank account, on or before the date of the agreement for transfer.]

(2) Without prejudice to the provisions of sub-section (1), where—

(a) the assessee claims before any Assessing Officer that the value adopted or assessed or assessable by the stamp valuation authority under sub-section (1) exceeds the fair market value of the property as on the date of transfer;

(b) the value so adopted or assessed or assessable by the stamp valuation authority under sub-section (1) has not been disputed in any appeal or revision or no reference has been made before any other authority, court or the High Court,

the Assessing Officer may refer the valuation of the capital asset to a Valuation Officer and where any such reference is made, the provisions of sub-sections (2), (3), (4), (5) and (6) of section 16A, clause (i) of sub-section (1) and subsections (6) and (7) of section 23A, sub-section (5) of section 24, section 34AA, section 35 and section 37 of the Wealth-tax Act, 1957 (27 of 1957), shall, with necessary modifications, apply in relation to such reference as they apply in relation to a reference made by the Assessing Officer under sub-section (1) of section 16A of that Act.

Explanation 1.—For the purposes of this section, “Valuation Officer” shall have the same meaning as in clause (r) of section 2 of the Wealth-tax Act, 1957 (27 of 1957).

Explanation 2.—For the purposes of this section, the expression “assessable” means the price which the stamp valuation authority would have, notwithstanding anything to the contrary contained in any other law for the time being in force, adopted or assessed, if it were referred to such authority for the purposes of the payment of stamp duty.

3.5.2 Thus, sub-section (1) creates a deeming fiction under which sale consideration received or occurring as a result of the transfer of land or building or both, can be replaced by the value ‘adopted’ or ‘assessed’ or ‘assessable’ by the stamp valuation authority for the purpose of payment of stamp duty in relation to such transfer. Further, subsection (2), permits the assessee to dispute such valuation adopted by the state stamp valuation authority and in such a case, it is open for the Assessing Officer to refer the valuation of the capital asset to the Valuation Officer. 3.5.3 In the instant case, the Ld. counsel of assessee has claimed that property in question was transferred through agreement to sale and it was not registered with the stamp valuation authority and, therefore, provisions of section 50C of the Act, were not applicable.

3.5.4 On perusal of the provisions of Section 50C(1) of the Act is evident that prior to 1/10/2009, Section 50C was applicable only in a case where the value was adopted or assessed by the Stamp Valuation Authority. The word “assessable” has been inserted by the Finance (No.2) Act, 2009 w.e.f. 01/10/2009. This means, if any property has been transferred through agreement to sale or otherwise, without registration with the Stamp Valuation Authority prior to 01.10.2009, the deeming fiction provided under section 50C(1) of the Act would not apply. However, if the property has been transferred w.e.f. 01/10/2009, and it is not registered with the Stamp Valuation Authority, the value ‘assessable’ by the Stamp Valuation Authority shall be deemed to be the full value consideration, if the sale consideration is less than the assessable value.

3.5.5 In the instant case, the Ld. counsel has filed a paper book before us, in which, page No. 70 has been claimed as agreement to sale for transfer of the property. On perusal of the said document, we find that it is a letter dated 06/11/2008 addressed by the assessee to M/s Ansal Properties and Infrastructure Ltd. In the letter, the assessee has submitted that he had booked a Shop No. BG-5 Rs.4,02,35,76,000/- and requested for transfer of right to purchase of the property in favour of M/s Jagirdar Exports P Ltd. This letter has also been signed by the purchaser party. The change of right to purchase has been confirmed by M/s Ansal Properties and Infrastructure Ltd. on 11/11/2008 subject to approval from the competent authority under the provisions of Urban Land (Ceiling and Regulation) Act, 1976.

3.5.6 From the above facts, we are of the opinion that provisions of section 50C of the Act are not applicable in the case of the assessee as the capital asset involved here was not land or building but it is a right to purchase a building (shop). Further, the Revenue Authorities has also not brought on record whether the transfer of the property was registered with the Stamp Valuation Authority.

3.5.7 Since in the case provisions of section 50C of the Act are not applicable, the provisions of section 48 of the Act would be applicable and as observed by us in earlier paras that full value consideration received cannot be substituted by the fair market value determined by the DVO as held in the various decisions cited above, we set aside the finding of the lower authorities on the issue in dispute and delete the addition made by the Assessing Officer. The ground No. 2 of the appeal is accordingly allowed.

4. The ground No. 1 of the appeal was not pressed before us and accordingly dismissed as infructuous.

5. In the result, the appeal of the assessee is allowed partly.

The decision is pronounced in the open court on 16th Jan., 2018.