1. An individual having Capital Gain on sale of Equity is required to file ITR 2. The article discusses the procedure to report Equity Capital Gain in Income Tax Return New Portal.

2. STEP BY STEP PROCEDURE

(a) Login to www.incometax.gov.in

(b) The path is: – e-file>Income Tax Return > File Income Tax Return. Select: AY 2021-22 (Current AY) > online. Start New filing > Individual> Select ITR Form > ITR 2> Let’s Get Started. Tick on the reason for filing Tax. Taxable income is more than basic exemption limit.

(c) Select Schedules – General

(d): Click on Income Schedule and select the following schedules: –

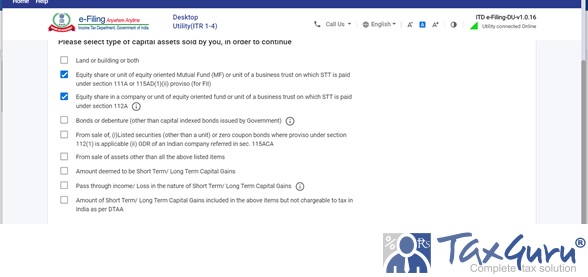

(e) Click on Schedule Capital Gain. Select Type of Capital Assets: –

3 DOWNLOAD DEMAT ACCOUNT STATEMENT: Demat Account statement is a summary of all the transactions in the Demat account. The statement provides the relevant details like sale consideration, date of acquisition, cost of acquisition, Period of holding, ISIN Code, etc. These details are required to be reported in Capital Gain Schedules of Income Tax Return.

Demat Statement can be download either directly from the website of the relevant national depository or through a broker with whom the taxpayer maintains a Demat account.

4. Capital gains tax on Equity can be long-term or short-term, depending on the duration for which the individual holds the Equity.

5. SHORT TERM CAPITAL GAIN (STCG): Equity shares, units of equity-oriented mutual funds, or units of business trust having a holding period of less than 12 months are considered Short Term Capital Assets.

Capital Gain arising on transfer of such Capital Assets, transferred through a recognized stock exchange and liable to Securities Transaction Tax (STT), is Short Term Capital Gain covered under section 111A of Income Tax Act.

Short-term capital gain under section 111A is taxed at a flat tax rate of 15% provided that such transaction is chargeable to Security Transaction Tax.

If total taxable income excluding short-term gains is below taxable income i.e. Rs 2.5 lakh the shortfall of basic exemption can be adjusted against short-term gains. The remaining short-term gains shall be then taxed at 15% + 4% cess on it.

Security Transaction Tax (STT) is a tax levied at the time of purchase and sale of securities listed on Stock Exchanges in India.

Equity Oriented Mutual Fund is the funds that invest 65% of the investible funds in the Equity Shares of the domestic companies.

Business trusts are like mutual funds that raise resources from many investors to be directly invested in realty or infrastructure projects.

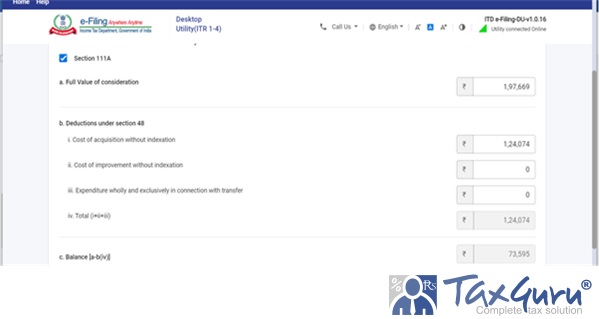

5.1 REPORTING OF STCG UNDER SECTION 111A

Click on Add details.

The example of Demat Account Statement indicating the details of Capital Gain is as follows: –

Enter Consolidated amount of consideration received from sale of short term Assets & cost of acquisition thereof in the financial year. CBDT vide press release dated 26 September 2020 clarified that script-wise reporting is not required for the sale of the short term listed shares

Note: Indexation is not considered for calculating the Cost of Acquisition / Improvement in the case of Short Term Capital Gain.

6. LONG TERM CAPITAL GAIN The Equity Share and Equity related instruments like Mutual Fund Units having more than one year of holding is Long Term Capital Assets.

Long Term Capital Gain on sale of Equity Share and Equity related instruments like Mutual Fund Units, liable for Security Transaction tax covered under Section 112A of Income Tax Act.

The rate of long-term capital gains tax on these listed securities is 10% for gains exceeding the threshold of Rs 1 Lakhs

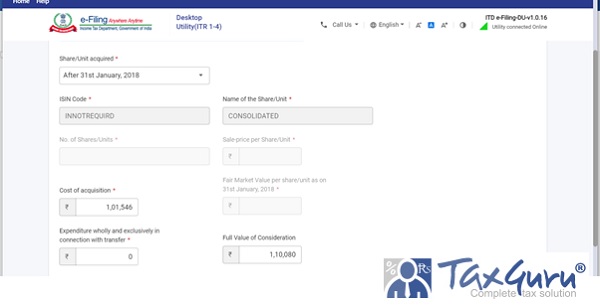

7. REPORTING OF LTCG – SHARES ACQUIRED AFTER 31ST JAN 2018

Capital Gains on sale of shares, acquired after 31.01.2018 is the difference between the selling price and the actual cost of acquisition, as no indexation benefit is provided under section 112A

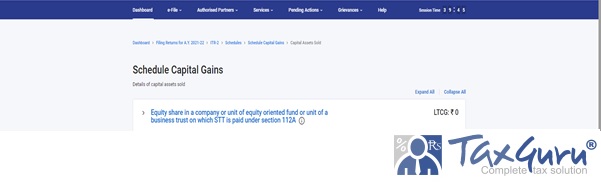

The following screen indicating Long Term Capital Gain will be displayed

8. GRAND FATHERING PROVISION -SHARES ACQUIRED BEFORE 31ST JAN 2018

Capital gains from the sale of listed equity shares, units of the mutual fund, and business trust were exempted until FY 2017-18 (AY 2018-19)

The Finance Act, 2018 introduced the grandfathering provisions to exempt long-term capital gains earned until 31 January 2018.

A method of determining the Cost of Acquisition (COA) has been specifically laid down in the case of specified securities bought before 1 February 2018.

Cost of Acquisition will be calculated as follows:

| (a) | Fair Market value as of 31st Jan 2018 | F | |

| (b) | Actual Selling Price | S | |

| (c ) | Lower of (a) and (b) | L | |

| (d) | Original Cost of Acquisition( purchased before 31st Jan 2018 | P | |

| (e) | Cost of Acquisition ( Higher of the L & P ) | C |

ILLUSTRATION

| Sl. | Fair Market Value(F) | Actual Selling Price (S) | Lower of (F) & (S) = L | Original Cost of Acquisition (P) | Cost of Acquisition (Higher of L & P = C ) |

| (a) | 2,00,000 | 4,00,000 | 2,00,000 | 1,00,000 | 2,00,000 |

| (b) | 1,80,000 | 1,00,000 | 1,00,000 | 1,50,000 | 1,50,000 |

ILLUSTRATION

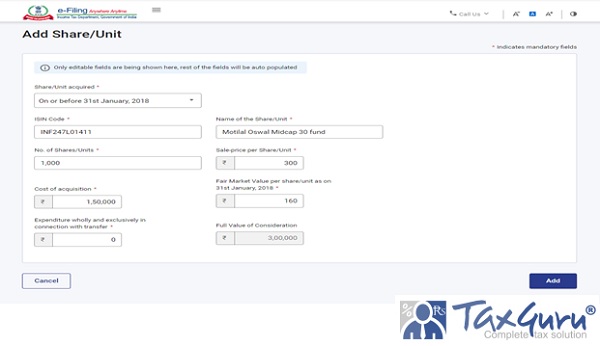

Mr. Anupam purchased 1000 shares @ Rs 150 in the year 2005. On 17.09.2021, he has sold the shares @ 300/- per share. Fair Market price of these shares as on 31st Jan 2018 is Rs 160/- per Share. The Cost of Acquisition and Long Term Capital Gain will be computed as follows

Cost of Acquisition

| Sl | Fair Market Value(F) | Actual Selling Price (S) | Lower of (F) & (S) = L | Original Cost of

(P) |

Cost of Acquisition (Higher of L & P = C ) |

| 1000*160 =1,60,000 | 1000*300 =3,00,000 |

1,60,000 |

1000*50 = 1,50,000 |

1,60,000 |

Capital Gain = Selling Price – Cost of Acquisition

3,00,000- 1,60,000

= Rs. 1,40,000

Tax on Long-term Capital gain on equity shares listed on a stock exchange are not taxable up to the limit of Rs 1 lakh.

The long term capital gain of more than Rs 1 lakh on the sale of equity shares or equity-oriented units of the mutual fund will attract a capital gains tax of 10% and the benefit of indexation will not be available to the seller

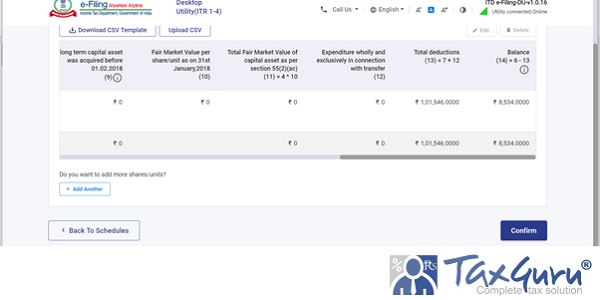

8.1 REPORTING OF CAPITAL GAIN UNDER GRANDFATHERING PROVISION

Scrip-wise details are required to be reported in ITR 2 for LTCG eligible for Grandfathering clause. Script-wise details include the name of the scrip, ISIN, purchase price, sales price, and the dates of these transactions.

The purpose is to ensure that tax officials can verify and validate the computation of capital gain after factoring in the grandfathering clause.

Once you enter script-wise detail in 112A Schedule and click on Add, the cost of Acquisition and Capital gain will be auto calculated by the portal and will be displayed as indicated below: –

8.2 CHALLENGES: – The biggest challenge is to obtain script-wise details in an appropriate format from broking and mutual fund aggregator firms. “Many do not provide ISIN codes in their transaction statements. The taxpayer needs to search manually and feed this data into the return filing software. Further, most demat and mutual fund statements are provided in PDF format, which means that each transaction detail has to be manually copied and pasted in return filing software. This is particularly cumbersome when it comes to disclosing systematic investment plans (SIP). It is better to ask brokerage, fund house, or mutual fund aggregator to provide the details in excel to facilitate easy copying and pasting on to online ITR form as also ISIN of each scrip.

9. SCHEDULE SI The taxpayer having Short term – long-term Capital gain is required to select Schedule SI: – Income chargeable to tax at special rates. This schedule is nothing but a summary of taxable Capital gain, special tax rate, and tax thereon.

10. ADJUSTMENT AGAINST BASIC EXEMPTION LIMIT: A resident individual and resident HUF can apply for adjustment of the exemption limit against Long Term Capital Gain.

In the above illustration, Mr. Anupam does not have any other income. The total income including the LTCG is below the basic exemption limit, hence there is no tax liability.

No tax deduction under sections 80C to 80U is allowed from long-term capital gains.

*****

Disclaimer: The article is for educational purposes only.

The author can be approached at caanitabhadra@gmail.com

Author Bio

i dont have the record of acquisition price. what price should I take as acquisition price for reporting LTCG under ITR2

Click on ” Sale of Securities” in AIS Report , there you will find Cost of Acquisition also .

I sold shares during Fy 2021-22

It’s reflected in AIS

And my income is not taxable

and profit/loss from shares is not huge

Therefore I didn’t show in my ITR

And i field ITR 1

So is there any compulsion to show CG because it’s reflected in AIS or simple I can ignore? If I don’t want to show?

It is not mandatory to file return if your income is less than basic exemption limit , still it as advisable to report the transaction and file ITR .

In ITR -2 Schedule Capital Gains (CG-F)

“F. Information about accrual/receipt of capital gain”

We have Q1 & Q2 gains and Q3 in loss. We are able to enter the Q1 and Q2 gain values. Q3 loss value we are not able to enter with a minus (-) or value within brackets like (100). What is the right way to report loss?

Adjust Q3 losses with gain in Q1 and Q2 and report net amount in any of the Quarter

if acquisition cost with indexation is 40 lacs and sell price is 30 Lacs then capital gain is showing -10 Lacs. I am salaried person and doesn’t have other income sources other than bank interest /dividend income.

a. Should I carry forward and how or leave it.

b. How this amount could be utilized / knock-off in future.

Capital Gain on Property:

me and my spouse sold Apts for 30 Lacs (50% each share) in Mar/2022. Bought it for 10 Lacs: contract date is July 2010, Allotment dt Aug 2010 and possession dt July 2018.

a. Can I consider Acquisition date as Aug 2010 which is allotment date.

b. Salary is less than 10 Lacs for showing capital gain I am filling ITR2… is this okay? or i should fill any other form.

c. In ITR2, when I enter apartment property selling details, should I enter 30 Lacs or 15 Lacs as sell price bcoz, my share is 50% of total 30 Lac sale value. Pls. note that TDS deducted amount showing is ITR and 26as is 15K with 15 Lacs sale of my share. And 15k with 15 Lacs in my spouse itr / 26as.

how to show periodical short term capital loss in part f of information about accrual/receipt of capital gain as the negative figures are not accepted by the portal.

I was going through your article on filing returns using ITR2, especially CG and SI sections. Just need further info on the following:

How to report LTCG on sale of gold ETFs purchased before 31st Jan, 2018 where STT is not paid both at the time of buy and sale? Can indexation be applied and if yes, will the gain upto Rs.1 lakh is exempted from tax liability?

Where are these details to be reported as I am not seeing any sub section for STT not paid case.

Request you to please clarify the above.

Thanks.

Gold ETF is considered as non- equity investment for the purpose of tax .

Indexation will be applied but Rs 1 Lakh exemption is not available.

This is to be reported as ” Assets other than indicated above ” in CG Schedule .

Thanks a lot, this clarifies my doubt to proceed with filing my returns.

Murthy

How to fill up in ITR 2 the long term capital gain exemption u/c 64EC after investing in PFC bonds

I am salaried and have an investment of RS.2000 in paytm stocks, please tell about the itr form no. to file itr. ie itr1 ,itr2 etc.

In case , you have not sold any stock and there is no gain/ loss from such sale of stock.

You can file ITR 1.

Hi

is that mandatory to show STCG and LTGC quarter wise in ITR 2

How to report in itr gain or loss on equity shares which are not listed.

Details of unlisted shares are required to be reported under the heading – Part A- General’ information tab in ITR.

When the STCG is calculated, does the brokerage and other charges need to be deducted?

Yes , Brokerage and other charges need to be deducted in case of STCG also.

Pl let me know can we deduct following expenses as expenditure for STCG

1. Exchange Transaction

2. STT

3. IGST

4. Sebi turn over fees

5. Stamp Duty

6. Dp charges

7. Brokerage charges

If i eam salaried person and earn only 4000rs profit of short term CG then which need to file itr1 or itr2 please suggest.

ITR 2 .

It doesn’t matter whether there is less or even loss.

Capital gain transactions need to be reported in ITR 2 only.

I have Ltcg on mf with ultra short , acquired before 31.1m2018, with cost indexation. In which schedule it is to be filled in itr2?. 112a does not any provision for that

In Schedul Capital Gain , click on “Assrts other than indicated above”.

There you will find option to select Long Term / Short Term .

Select Long Term and go ahead entering the details

OK

How to show the STCG on foreign stocks in ITR2?

As per AIS statements, my capital gain amt is less than transaction amt which is shown in acct statement provide by broker. What ahould i do while. Filling itr 2

Please clarify where and how to report long-term shares off market transaction transferred to wife at a token money say 1 Rs

The Short term capital gain (from selling of shares) is getting combined to my overall income and being taxed at highest tax slab. Which step I am missing that it is not getting taxed at 15%

Short Term Capital gain is added in total income but taxed at special rate @15%.

Make sure you have clicked and confirm the SI ( special Income )schedule while filing Return

Thank you Anita for prompt response.

Very good article. I wan to know how to enter

Negative amount in the long term capital gain where is loss is reported. The problem is when we give breakup for each quarter where one quarter is is in loss and negative number has to ve entered . Thank you.

Sale proceeds less than cost of acquisition will result in CG Loss.

Further , in my view , if net profit is there in the FY from Capital gain , you can enter the same in any of the quarter against the schedule -” details of capital gain accrued/ receipt) .

For net loss , you won’t find validation error for not providing specific details.

Unlike dividend , quarterly bifurcation is not relevant for IT purposes.

I’m entering quarter-wise details in CG-F in ITR-2 but then during validation I’m getting errors that the quarter-wise CG figures are not matching with BFLA data. I am not able to submit online because of this error.

Click on schedule BFLA and confirm . The amount in BFLA schedule shall be entered in Quarter wise accrued details in ” F” of Capital Gain Schedule.

Still if you are facing issue , e mail the details to caanitabhadra@gmail.com

This is helpful. I have one query-

My total LTCL carry forward is Rs.6000 from previous years. In current AY, my LTCG is Rs.30000.

In the new IT portal, this LTCG amount is getting adjusted with previous year losses and amount carried forward to next year is Rs.30000 (60000-30000).

My query is – LTCG from Equity is non-taxable upto Rs.1 lakh. And my current year profit is Rs.30000, hence it is non-taxable profit, then why the previous year losses (LTCL) is getting adjusted with non-taxable LTCG? Is this how Income Tax calculation happens? Ideally the full previous year losses should be carry forwarded to next year w/o any adjustment.

Please suggest and guide.

Is it necessary to report quarterwise figures of capital gain in schedule CG column F. It is not allowing to report loss figures as – sign in one quarter. Then how to report. Please help

It is necessary to report Quarter wise details of capital Gain ,otherwise there will be a validation error while submitting ITR.

You can report in the subsequent quarter in which there is a profit and show the net figure in that quarter.

To report quarter wise figures of capital gain in schedule CG column F. It is not allowing to report loss figures as – sign in one quarter. Then how to report as it is taking it as positive value due to which total does not tally. Please help.

Nice article.

Only one question. If i have made a longterm capital gain of rs.27000,it will not attract tax. should it be

shown seperately in the ITR form all the scrips wher no profit was made and where the gain was below Rs.100000.

can u advise.

Script wise details are required for LTCG , even if there is a loss

Scrip wise reporting is required for LTCG .

There is a section “off market credit/debit transactions” in AIS. Do we have to report these in ITR2?

No

Nice article. One question: If I have multiple transactions in several scrips, is it valid to consolidate them scripwise for LTCG reporting?

Scrip wise reporting is required for LTCG .

Consolidated details can be entered for STCG

If one has negative gain as in loss in short term any reason to add that in the return ?

The reason is to carry forward and set off the losses in future profit

1. if I have say reliance scrip which were bought before jan 31 2018 and sold after in discrete manner how to report them ? I know it has grandfathering but how can we club them together. below is example if you can answer.

10 Jan 2017 – bought – 100share – for 100rs per share

10 Feb 2017 – bought – 100share – for 200rs per share

10 Mar 2017 – bought – 50share – for 300rs per share

10 Apr 2017 – bought – 75share – for 150rs per share

10 Jan 2019 – sold – 200share (jan/feb above) – for 500 per share

10 Feb 2019 – sold – 10share (mar above) – for 700 per share

10 Mar 2019 – sold – 115share (mar/apr above) – for 800 per share

now how to report these for income tax ? if in above example say in 10 Jan 2017 along with reliance I also bought HCL 100 share for Rs. 200 per share and that was sold in 10 Mar 2019 how to split the brokerage charges ?

if there is article that explains similar scenarios please share.

2. If after Jan 31 2018 I have bought and sold shares then do I have to enter isin can i just enter amounts. ex. 100 shares of ril as Rs. 100 in Feb 10 2018 purchased and sold say in Feb 10 2021 for Rs. 400. also say i bought hcl 100 shares for 500 in March 2018 and sold in 2019 for 1000 and never reported. then do I enter just buy and sell price in full value consideration without giving details of of shares. so 100 x 100 + 100 x 500 total purchase and 100×400 + 100×1000 total sale.

Script wise detail is required to be entered. You can add as many transactions.

ISIN details not to be provided for shares purchased after 31 Jan 2018

Short Term Gains in Stocks – How to add speculative / intra-day gains?

File ITR 3

UNABLE TO FILE SHORT TERM CAPITAL GAIN. STCG IS NOT ACTIVE

I am salaried employee with capital gain tax. Do I need to file both ITR 1 and ITR 2?

No, Only ITR 2

But ITR2 says, income > 50 lakhs which does not hold for me. Salary + Capital gain < 50 Lakh. Still we need to file ITR2 ?

I have capital gain on Debt Mutual Fund(short and long term )

1) In the ITR 2 form, schedule captial gains section, which option I must select?

I have some bank interest , should I add in schedule income from other sources ?

2) As its avilable in pre filled json,but Those values are not auto populating in the form, should I add manually?

I have large number of sell transactions in debt fund having short term gain and long term loss. How can i fill aggreated value of capital gain in ITR without giving individual transaction details?

I have STCG on sale of debt oriented mutual fund.Where to show this in ITR 2?Thanks in advance

Schedule CG

Where is schedule CG…i do not see any option for non STT paid MF

I got some units of Franklin Templeton Debt Fund redeemed during the last year and the holding period was less than 36 months. Am I to pay 15% Tax on the STCG or 30% which is my tax slab otherwise? Also, where in the Capital Gains schedule I have to report it?

While filing ITR3 Sch112a sale of Shares & MF investment of CG done in tax savings bonds however the ITR provided investment in sec 54F-HP instested of Sec 54 EC how to resolve

In 112a in ITR2, while adding details of shares (with grandfathering clause), the option to write share name is now a drop down menu in which it shows ‘no results found’ on typing name of any equity share. How do we add the share name now? Please help. Thank you.

Seems to be portal issue .

Just mention ISIN Number and leave the name of the script

Dear Ma’am, Thank you for a nice article on the subject of CG. I have a few clarifications though. I have shares purchased long before 31 Jan 2018, converted into demat form and hence actual CoA is forgotten. Also, there are some shares with splits and bonuses before sale. How do I go about sharing this info’ on my return? CG report from demat account does not show details of scrips converted into demat form. What’s the solution. Kindly reply. Many thanks in advance! Regards

Dear Ma’am, Thank you for a nice article on the subject of CG. I have a few clarifications though. I have shares purchased long before 31 Jan 2018, converted into demat form and hence actual CoA is not forgotten. Also, there are some shares with splits and bonuses before sale. How do I go about sharing this info’ on my return? CG report from demat agent does not show details of scrips converted into demat form. What’s the solution. Kindly reply. Many thanks in advance! Regards

I found the article very informative, lucid & helpful.

However, I am experiencing a problem on which I would appreciate help. My LTCG on sale of shares is Rs 14, 458/- My understanding is that this income is Tax-Free (as it is below the threshold of Rs 1 lakh). However, for some mysterious reason, this figure is getting added into my total income & thereby inflating my tax liability. Kindly advise as to how to handle this. Is it that the IT dept feels that income above the threshold of Rs 1 lakh needs to be reported & those below the threshold need not be reported?

Tax on Capital Gain up to Rs 1,00,000 is not being calculated

You can confirm this by clicking on Schedule SI and also reconfirm by calculating tax separately.

The portal presentation is such as tax is added whereas actual tax liability is on total income after basic exemption of Rs 100000 on LTCG

I have a gain of Rs 98000 on sale of equity oriented mutual funds In my case also due to some mysterious reason the the tax is getting calculated after adding for this amount to my income.by the system.

I am filing my itr2.I am pensioner with agriculture income over Rs.5000 and some capital gain on mutual fund units. My problem is the schedule EI is not appearing in the it Portal and have tried several times but unable to enter the agriculture income due to missing of schedule EI. Please help. Thanks.

with regards.

It is appearing .

First time when you select , it won’t display .

Click on > Add more schedules ( Left side down ) You will find Schedule EI

Kindly request you to explain the same in the specific context of its applicability to NRI Individuals. Given the fact that all Purchase/sale transactions are executed through the NRE PIS Accounts held with a bank in India whereby the Capital gains tax is computed by the bank and is deducted in full as TDS and credited to Revenue.

After filling Schedule 112A, LTCG is 1040/-.

But it’s getting added to Total Income and being taxed. But upto 1.0 lakh is exempted.

Kindly advise how to avail of rebate.

For this Filing of ITR2 by me is getting delayed.

Plz help.

Check the schedule SI . You will find the net figure after adjustment of basic exemption.

You can also check preview before filing the return .

Lucid article on capital gains on equity shares and MF units.

Likewise I would appreciate information on capital losses on shares and MF units.

Thanks for your humble comment . You will find my article on Capital losses soon.

What about capital losses?Can those be adjusted against capital gains?For only that year or next year too?

My next article on Capital Losses will have all the details

Thanks for this extremely educative piece of information. Kindly also let me know about which form I am required to submit for IT Return informing capital gains and dividends given I have already a monthly income from pension also.

File ITR 2

If I redeem MF, and have long term Capital Gain and I reinvest this to by another MF, can I get any tax deduction?

You won’t get any specific deduction for re-investing of Mutual Fund redeem.

Good article, Please explain about speculative trading by way of future and options. And also on MCX commodity trading

Thank you for humble comment .

Certainly , I will write article about speculative trading by way of future and options

Useful article

Thanks a lot .

How did you arrived Rs.160 rate where as rate mentioned is Rs.37.5 is it typo error ?

Yes , it is typing error in description. The Fair market per share is Rs. 160/-.

Inconvenience is highly regretted

How do you account a investment capital loss and STCG net loss / but LTCG profit and hundreds of share security transactions done in a iifl portfolio managed fund when those people don’t supply info as required by itr2 and uploadable and even info in report cannot be copied.

Because in the form those are separatly demanded

And if you have dabbled in securities on your own too then to combine the two is another hassle as even depository banks like icici dont generate report in itr2 requurd format.

Your suggestions please.

Sir

Please share your e-mail ID .

I will try to elaborate.

If there is capital gain due to sale of only equity mutual funds, form ITR2 is to be used or a different form

ITR2 is to be used

very informative.I am yet to begin preparation. Can u pl mail me your mail id to enable me to get in touch with you for clarification of doubts? thanks in advance.

Thanks for humble comment . E-Mail ID is mention at the end of the article – caanitabhadra@gmail.com

The Illustrations of the 111A are completely erroneous. The figures given in the situation like ‘FV as on 31st Jan, 2018’ is 37.537.5 per share, but the calculation takes it as 160 per share while solving it. Also the Original COA given is 50 per share, but taken as solved under 150 per share.

Good artical, but most individuals hide this info. CBDT should work on including it in 26AS.

Thanks for your humble comment

It is very good information. That means both 111A & SI to be filled.

Thanks for your humble comment . Schedule 111A and SI both to be selected . Amount in SI will automatically flow from 111A . However, it need to be confirmed