1. Meaning of different terms under Income Tax Act, 1961:-

i. Trust : A trust is an obligation in relation to ownership of property & which is arising out of confidence reposed in and accepted by owner or declared and accepted by him, for the benefit of another, or of another and the owner.

ii. Author of the trust/Settlor: The person who declares the confidence is called the Author of the Trust. In other words, settlor is a person who settles property on trust law for the benefit of beneficiaries.

iii. Trustee: The person who accepts the confidence is called the Trustee.

iv. Beneficiary: the person for whose benefit the confidence is accepted is called the Beneficiary.

v. Trust-property: The subject-matter of the trust is called Trust Property.

vi. Beneficial Interest: The beneficial interest or interest of the beneficiary is his right against the trustee as owner of the trust-property.

The above terms can be easily understood with an example:-

Mr A wants to pass his property to Mr C for the benefit of his minor granddaughter. Mr A passes his property to C, because he reposes (has) confidence on C.

In this case, Mr. A is author of trust, Mr. C is trustee, Minor Granddaughter is beneficiary and property is Trust Property.

2. Difference between Will and Trust:-

In our day to day lives we would have come across the terms such as “Will” or “Trust”. Do they mean the same or whether they can be used interchangeably? The answer is NO.

One main difference between a will and a trust is that a will goes into effect only after you die, while a trust takes effect as soon as you create it. Basically will is a document that directs who will be receiving property post death and it appoints legal representative to carry out the wishes stated in will.

Another difference between a will and a trust is that in case of a will court oversees the administration of the will and ensures the will is valid and the property gets distributed the way the deceased wanted, whereas in case of trust court does not oversees the process.

Will eventually becomes a part of Public Records and Trust remains to be Private.

3. Benefit of Private Trust:-

- Effective and efficient mode of managing and passing of family assets.

- In creation of Trust, court does not oversee the process unlike at the time of execution of Will.

- Safeguards interest of family members including maintenance of members with special needs.

- Avoids family disputes.

- Under trust, conditions can be attached such as attainment of particular age/fulfillment of authors’ wishes.

4. Trust Creation:-

The common question when it comes to creation of Private Trust is who can create trust, who can be a trustee and who can be a beneficiary.

- A trust may be created:-

(a) By every person competent to contract, and

(b) With the permission of a principal Civil Court of original jurisdiction, by or on behalf of a minor,

but subject in each case to the law for the time being in force as to the circumstances and extent in and to which the author of the trust may dispose of the trust property.

- Every person capable of holding property may be a trustee; but, where the trust involves the exercise of discretion, he cannot execute it unless he is competent to contract.

- Every person capable of holding property may be a beneficiary.

5. How to register a trust:-

A registered document called as trust deed is necessary to set up trust and should be registered with the Registrar. The deed should be executed on a stamp paper.

The trust deed should have following:-

- Details in relation to trust property.

- Purpose of trust.

- Beneficiaries of trust.

6. Difference between Public Trust and Private Trust:-

A Public Trust is created for the benefit of society at large and for charitable purpose like education, poverty eradication, promotion of sports, medical welfare or for religious or scientific purpose. Beneficiary in Public Trust is society at large and is governed and regulated by respective State Government.

A Private Trust is mainly created for the benefit of one or more than one person and is governed and regulated by Indian Trusts Act, 1882.

7.Types of Private trust:-

- Revocable Trust – It’s an alternative to Will. It does not protect any assets, as they can be withdrawn from this trust. In this, assets are neither considered given away; hence they are taxed in the hands of Settlor at the slab rate.

- Irrevocable Non-Discretionary Trust – Assets cannot be withdrawn here. Settlor has complete control over trust norms as he can decide which beneficiary receives which asset, and in what proportion. If the Settlor is the primary beneficiary, he/she is taxed at slab rate. For e.g. the settlor may grant 40% of the trust’s benefits to 1st child and 60% of the trust’s benefits to 2nd child. Or the trust may be established for a handicapped child to ensure that he or she is properly cared for if the child’s parents or guardians die.

- Irrevocable Discretionary Trust – In this case, Settlor lets the trustee decide which beneficiary gets which asset and in what proportion. The Settlor only decides beneficiaries. In other words, while the beneficiaries are identified, their beneficial interest in the Trust is not ascertained upfront. A well-drafted discretionary trust allows the trustee to add or exclude beneficiaries from the class, giving the trustee greater flexibility to address changes in circumstances. The beneficiaries cannot compel the trustee to use any of the trust property for their advantage.

Discretionary trusts are more common than Non Discretionary trusts. Today, most family trusts are discretionary.

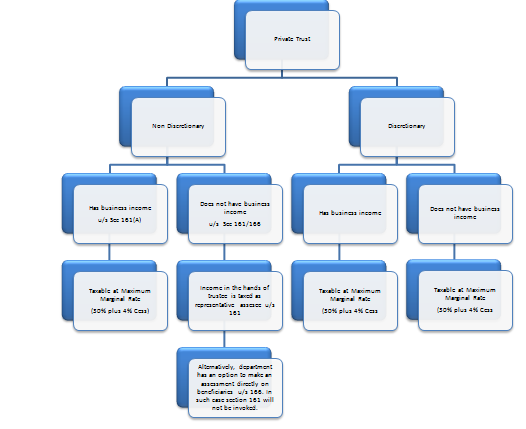

Taxation of Private Trust

Note 1:- Where in case of non discretionary private trust has business income, Maximum Marginal Rate will not apply if a trust has been declared by way of a will from which business income is derived by any person and is exclusively for the benefit of any relative dependent on him and also such trust is the only trust so declared by him.

Note 2:- Where in case of discretionary private trust, slab rates applicable to individual will apply

- Where none of the beneficiaries

1. Has taxable income exceeding the maximum amount not chargeable to tax

2. Is a beneficiary under any other private trust; or

- Where the relevant income or part of the relevant income is receivable under a trust declared by any person by will and such trust is the only trust so declared by him; or

- Where the trust yielding the relevant income or part thereof was created by a non-testamentary instrument before 1-3-1970 and the A.O. is satisfied that it was created bona fide for the benefit of the dependant relatives of the settlor, or where the settlor is HUF, exclusively for the benefit of the dependant members.

- Where the relevant income is receivable by the trustees on behalf of a provident fund, superannuation fund, gratuity fund or pension fund or any other fund created bonafide by a person carrying on a business or professional exclusively for the benefits of his employees.

Note 3:- Capital Gain Tax – Under section 47(iii) of Income Tax Act, 1961 Transfer of capital asset under a an irrevocable trust shall not be charged to capital gain tax.

The information which is summarised herein does not constitute financial or other professional advice and is general in nature. It does not take into account your specific circumstances and should not be acted on without full understanding of your current situation and future goals and objectives by a fully qualified advisor.

Authored By:- Hosakote Akshay Shrinivas | Address– Gurudatta Layout, Bangalore -560 085 | Email id:- hosakoteakshay@gmail.com

Author Bio

very use full information.

Pl also provide more details like these Discretionary trusts are eligible for opening savings account with banks and Trust are exempted from income tax.

Very good information being a trustee in one trust. Need minor details on opening a university under the trust