Introduction

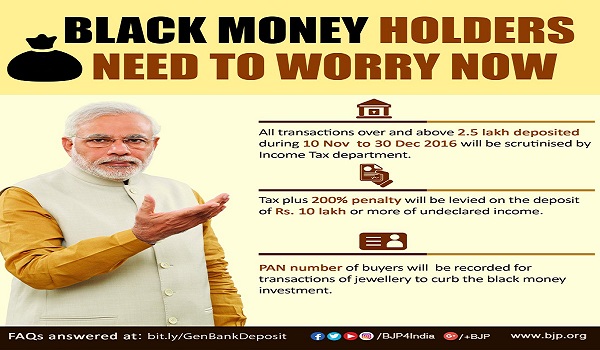

The ban of Rs.500/1000 note in India is creating havoc in the Indian markets. Everybody is either rushing towards banks or towards jeweler market to safeguard the black money.

In this article, we will discuss how government will levy penalty or tax on the cash deposit in bank account of the public. We will also discuss the possibilities of action that government may take depending upon the size of the money deposited.

Everybody is living with the fear that government will slap 200% penalty for sure. However, this is not the case. Government works under a system and make laws for everything. Everybody works under the ambit of law even the government. So if they have to slap any sort of penalty, they levy it under income tax act, 1961 by following a proper procedure. Hence, let us understand the type of depositors and the chances of penalty imposition upon them.

#Point 1 – Cash Deposited Up to 2.5 lakh: The first category of person is those who have deposited cash up to 2.5 lakh. This category doesn’t have to worry about. As, finance minister in his speech has also said that we will not going to disturb or ask any question on deposit up to 2.5 lakh.

Hence, if have money up to 2.5 lakh, then go ahead and deposit the same without any fear.

#Point 2 – Cash Deposited Up to 10 Lakh: Most of the middle class are covered under this point. They save their hard earned money and secure it in their lockers. They have saved this money over the years. It is all legitimate money which they have earned and saved by working hard over the years like someone has saved it for daughter marriage or someone may have saved it purchase a small house.

Though the government will be keeping an eye on this category as well, however there are little chances that government will interfere in this category. Nowadays the value of 10 lakh is no more considered as superior.

The current practice

Also, people may deposit this sum breaking into smaller sum of 2.5 lakh and may deposit it in the name of family members which is also a lot of people may already be doing.

Further, government also understands this fact and they will not interfere with this needy money of the middle class.

#Point 3 – Cash Deposited Up to 50 Lakh: Anything over and above 10 Lakh will catch the eye of the taxman. If your returned income does not match with the amount you deposit, then you might be in trouble.

E.g. suppose, you regularly file the ITR with 5 lakh income. Now suddenly you deposit the sum of 40 Lakh in your account which cannot be justified with a small income. Hence, department may treat this income as unexplained credits and may tax the income at 30% with 200% penalty under section 270A.

This point is very important; hence we must understand this point well.

– Cash credit: Once you deposit the sum into the bank account and under scrutiny proceedings, you were unable to justify the sum, then IT department will deemed that deposit as unexplained credit or cash credit under section 68 of Income tax act, 1961.

– Section 115BBE: This section is one of the harsh sections of the income tax act. Once it is proved that the cash deposit is cash credit under section 68, and then it shall levy the tax rate of flat 30% without even providing the basic exemption limit.

E.g. if you have cash credit of Rs.40 lakh, then 12 Lakh will be the tax amount.

– Penalty under section 270A: Once it is proved that you are a mischief, then penalty provision under income tax act would automatically comes into picture. The AO shall use the section 270A, to levy the penalty of 200%.

However, the penalty of 200% under section 270A can only be levied if any of the conditions is fulfilled:

a) Misrepresentation or suppression of facts.

b) Failure to record investments in the books of account.

c) Claim of expenditure not substantiated by any evidence.

d) Recording of any false entry in the books of account.

e) Failure to record any receipt in books of account having a bearing on total income;

f) Failure to report any international transaction or any transaction deemed to be an international transaction or any specified domestic transaction, to which the provisions of Chapter X apply. (ignore, applicable in case of international transaction).

Hence, the above three sections will play a big role under IT department scrutiny.

Important Point

“The most important point of this whole process starts from non justification. Hence, if you can justify the deposits and has already paid the full taxes, then no penalty can be imposed upon you.”

#Point 4 – Cash Deposited more than 50 Lakh: Anything over and above 50 Lakh will require a strong justification otherwise there will be very less chances that penalty can be saved. However, if you plan well, justify your income and the deposits thereof, and then you don’t need to worry.

Conclusion

This is not going to be easy for anyone of you. This is an historic event. Let us not panic under these circumstances rather help each and other and let’s make this government’s step a success. Hope we win this fight against illicit practice of black money, terror funding etc.

(For any feedback, Comment or suggestion author may be reached at paras.mehra18@gmail.com or at +919654622792, Authotr is Co-founder of www.hubco.in )

My sister is currently working in SBI, she hold savings of rs 7lakh in their saving bank account ,

Now she want to transfer the whole amount to my mother bank account, so what are the provision of gift, and my mother file IT return this year with income less than 2.3 lakh, so plz give suggestions what to do, any evidence ? Or any gift deed required??? Plz ans

My Aunti is an income tax payee,but she had saved some unaccounted money saved as NSC N KISAN VIKAS PATRA amounting to less than 10 lacs maturity amount,a part of which she had encashed in this financial year and the other part not encashed yet though they got matured in this current financial year and some in earlier financial year so what shall she do to handle it.

The unholy alliance between the CAs and the AOs (both not as a class but as individuals) is one of the ailments in tax compliance in India.

The advice in this article is outright invitation of clients to evade the tax due on black money through feasible loop hole in the law; as rightly said the law is for every one including the Govt machinery to follow.

The conclusion about achieving the avowed purpose of the Govt in undoing black money is something said by the way.

Dear sir,

I am working in Saudi Arabia as an accountant and I have my 12 months salary remaining amounting to 38000 Saudi riyals with me. I have to remit the amount to my mother’s saving account in India. If I send the amount to my mother’s account will it be taxable or not. Kindly please throw some light and advise us what to do.

Sir my last year income 264700 rs soI can deposited cash how many

I am a senior citizen of 74 years age. In 2014, we entered into a deal to sell our house and on the day of registration, the buyer gave the last payment in cash (rs. 10 Lakhs). We were told that it is white money. After getting a copy of the sale deed, I also realized that the executed sale deed mentioned 10 L rs. less than government assessed value (both amounts are mentioned on the document). In the tax return, I paid capital gains tax on the bigger amount, including the cash amount. We are from a small town and I am not good at using electronic devices nor comfortable with online and cards so I kept this cash for medical requirements and expenses etc we have been facing for the last two years but I am uncertain about the cash with me now. Will I face problems if I deposit the cash in the bank now? Thanks.

I am PSU employee, I am filing ITR from last 19 years. From last 3 years ,I am showing my salary income 12 lakhs, TDS is being done.Can I deposit cash savings of Rs 10 Lakhs in old currency into bank without any penalty from IT dept?

If an NRI is having 15000-2000 Rs , which is made up birthday gifts , Diwali etc , accumulated overs years . How they can deposit in banks ? Abroad or in their NRO account in India ? This money are lying in india in their cupboards

IS THEIR PRESENCE MANDATORY IN INDIA ?

If one is having , Rs 100000 as cash on hand from professional income , if deposited in bank in piecemeal , is it ok ? Or has to be deposited at one go

If one is having say sbout Rs 25000-30000 , as their savings over the years , over and above cash on hand from professional income , can it be deposited in bank ? How to show in their account ?

Thanks

I am PSU employee, I am filing ITR from last 19 years. From last 3 years ,I am showing my salary income 12 lakhs, TDS is being done. Now can I deposit cash savings of Rs 10 Lakhs in old currency into bank without any penalty from IT dept?

Hi I have a income of 3lakh per year and I have a hard cash if 2lakh can I deposit to bank without any problems.. will I be penalised?

Shopkeepers can’t charge 1-2% extra on Debit Card Payment – RBI.

Hello Sir.I am a salaried professional paying IT as per my tax bracket.I deposited 2.4 lakhs which was my emergency fund in a bank.I was informed through the news floating around that deposits upto 2.5 lakh will not come under the taxmen’s net.Now today I read an article in Business Standard stating that as per a press release of Economics Secretary,those deposits of above 50,000 done after November 9th will come under taxman’s radar.Will I be penalized?The framework and rules weren’t mentioned in clear terms to the public.I am sure there are quite a few who are facing the same predicament as mine.

Dear Sir,

My dad is 67 years old ,we have sold 2 lands have an cash of 40L will it be taxed and penalty will be imposed.??Can he deposit this amount in bank don’t have any other form of income.plz reply.

Dear Sir, I am 62 years female. I am getting family pension 1,50,000. I have 5,00,000 hard cash . Which I have kept with me. Can I deposit this amount in my account. Will it create any problem with me. Please reply.

i want to know how many time cash deposit in current bank a/c up to 30th decemeber

Sir, i want to know that the amount of Rs. 2,50,000-00 declared and deposited in the account, whether this amount shall be included in the next taxable return or it shall be considered exempted seperately.

Suppose my taxable income is 10 lakh and i deposit 2,50000 extra in my account then whether my income shall be considered as Rs. 10 lakh or it shall be considered Rs. 12,50000. Please guide.

Regards. S.P.Jain

My mother is an 86-year-old lady. She has Rs. 7,30,000 being cash collected as Gift from children, grandchildren, and other relatives for last 7 years. Can she deposit this amount in bank

The penalty u/s 270 A sub section 8 200% penalty can be imposed only in case the under reported income is in consequence of of any misreporting thereof . Firstly there should be under reporting of Income . Under reporting of income is difference between the returned income and assessed income . If there is no difference in the returned income and assessed income there can not be under reported income and misreporting thereof . Hence no penalty of 200% can be imposed

Sir, I am a farmer. But in last year (2015-2016) I also bought and sold 2-3 plots. I have agriculture crop loan of 15 lacs which usually I repaid every-year in last 3 years in Nov itself and withdrew cash later. Now, if I deposit the whole cash this Nov also, will it be taxed and penalty will be imposed.?? I have cash of 15 lacs but no papers to show, I kept last year’s produce stocked (Matar) and sold it just 10-15 days back in cash. plz reply.

I m a jeweller , can my client deposit the old currency in my current account for a credit bill with a valid Id proof? The amount is below two lakhs

I m tuition teacher.I have 3 itr with 3.5lakh each.so total money 10.5 lakhs.I have 8 lakh hard cash.to mujhe 8 lakh deposit karne chahiye mujh pr bi penalty lagegi kya

My Father is 63 Years Old. He is not Working and Depends On us or Taking Pension. Can I deposit My amount in his account. How Much Amount can i deposit in his account.

Hello sir,

I am a business man , more than 90 lac rupees are in Market, Can i receive these money and deposit in my Current Business Account ,

From April – 16 to Oct- 16 I deposited Rs. 40-50 lac per month. How Much Rs. Can i Deposit in old 500/1000 Denomination Note in Bank.

Dear Sir, I am an unemployed unmarried person (male) and I have inherited my father’s inheritance (All in form of FDs) after his death back in 2007. In 2016-2017 my income is around 1.44 lacs from those FDs. I have always given 15 g form and never had to give any TDS on my interests. I have also never submitted any tax return as such. I don’t have any other form of income. On 10th November 2016 I have deposited 1.2 lakh on my own account lying with me in the form of 500 and 1000 Rupee notes. Some of this money is my own savings, some for household expenses, and some I have kept as emergency as my mother is suffering from cancer. Will I be facing any trouble from the Income tax department regarding my 1.2 lakh deposited on 10th November 2016?

I have already deposited some cash from 01.04.16 to 08.11.16, say around Rs.45000/-. Will it be considered as a part of cap of Rs.2.5 Lakhs OR any cash deposited after 10.11.16 to 31.03.17?

Hello,

I show my income as Rs 4 lakh in form of tution fees , servicing etc and pay taxes accordingly.I keep my income in cash so balance in my account is not more than Rs 10000. If my relative which have black money ask me to deposit money in my account and after some time to withdraw it by cash then will IT department will take care of this as balance in my account have increased suddenly.

I am 82 years old senior citizen. with total yearly interest income around 200,000 i have household savings of 150000 over the years kept for any kind of medical & social needs. will i attract any tax / penalty liabilities for depositing this cash? or basic limit of 500000 will cover this? please reply at earliest. Thanks

I am a senior citizen still working to support my family’s financial needs. Over a period of 4 years my bank balance reached 7 lakhs by means of salary. However, in Oct I withdrew 7 lakh money to buy a property but the deal cancelled. Now I have that cash with me (700*1000), can I deposit the full amount in bank? will I face any penalty? pls suggest….

Thx for lucid presentation. Is 270 A now prevelent or will be effective from 1st Apr,2017