CA Paras Mehra

Currency Ban: How penalty CANNOT be imposed on cash deposits in bank account under Income Tax Act, 1961

Introduction

We are going through a very unusual phase of Indian economy where people are rushing nowhere carrying cash in hand. I have experience it first time when people are ready to pay the full amount of tax or they are ready to even forego 50% of the amount still they are not able to buy peace of mind thanks to the Modi government. I really appreciate this brave and very bold step of Indian government.

However, things are now turning little ugly on ground with regard to tax terrorism. I support tax friendly measure, honest tax scrutiny but as a responsible citizen of this country, I nowhere in favor of tax terrorism.

Further, in this article I would also discuss about the penal provisions and related aspects where government is claiming to levy 200% penalty on cash deposit with regard to currency ban in India.

How it all started?

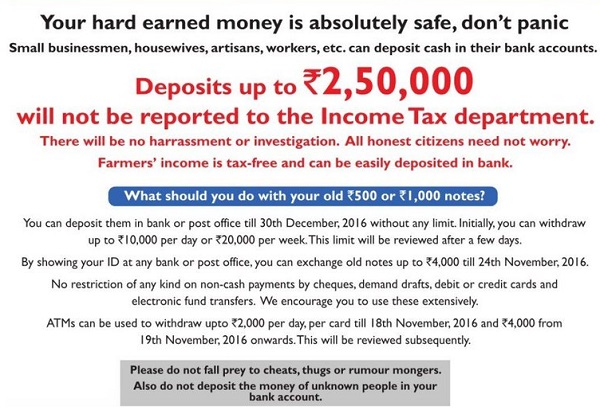

On 8th November, 2016 Prime Minister Modi announced that Rs.500/1000 note shall not be a legal tender and asked people to submit/exchange all the Rs.500/1000 currency notes till 30th December, 2016. Since then, things have become ugly;

- There are raids conducted by Income tax and sales tax department which is also bothering the honest person.

- Environment of fear and anxiety all around.

- Everyone is scared of income tax levying penalty of 200%

- Ministers adding to tax terrorism by giving unnecessary speeches.

I suppose this must not be the intention of PM Modi as well. Further, people from legislature (e.g. Ministers) are guiding or I should say influencing the work of the executives which are powered independently under constitution of India. Furthermore, the electronic media, social media is only making things worse by making information viral which is most of the time is fake.

All the people of India are under panic and they are actually scared in depositing cash into bank because of Income tax notices and harassment.

The reality of 200% penalty

The penalty of 200% is a reality and levied under section 270A of the income tax act, 1961 in cases of under-reporting of income or misreporting of income. Some of the points are outlined:

1. Cash Deposited more than returned income: Here I am not talking about the deposits up to Rs.10 lakh. If you want to read about deposits of less than 10 Lakh, kindly read my previous article.

I am talking about the deposits in lakh, crores. Now in case you have deposited huge cash into your account and you are not able to justify then you are under trouble. You will have to pay tax, penalty @ 200% or interest if any.

2. Changing money through illicit practice: Since people understand the point no.1, so they are looking for different options in order to safeguard themselves. However, they should understand that these measures are temporary and will only making the things worst afterwards.

3. Buying gold: People are rushing towards buying gold and jewelry. However, here are the following reasons which may prove detrimental:

- Jewelers are now covered under excise law, which means that they have to maintain records for inputs and output made during the year.

- Since everybody will be rushing to jewellers to covert cash into gold, this would surge up the price for gold and ultimately, people will buy it at a higher price. Since it will be a temporary surge, the prices of gold will come down soon. This would lead to fall in value of wealth.

- Jewelers are raided by the authorities and vigilance is also after them. Hence, government will get all the information about the buy/sell of gold.

Under which situation penalty can’t be levied

Suppose, a professional have some 10 crore with him and he deposited the entire amount in bank and paid the income tax and service tax on the amount. So he conducts the following calculation:

| PENALTY | SUB TOTAL | AMOUNT |

| Total Amount Deposited (A) | 10 Crore | |

| Service tax included in above (Reverse Calculation) (B) | 1.30 Crore | |

| Revenue Amount (A-B) | 8.70 Crore | |

| Tax on above amount (assume 30%) (C) | 2.60 Crore | |

| In Total he paid (B+C) | 3.90 Crore | 39% of total amount |

He paid the entire amount of Rs.3.90 Crore and filed the Income tax Return for FY 2016-17.

Assessment Proceedings

As expected, AO shall issue the notice under section 143(2) to open the scrutiny against the assessee. Further, AO shall ask for justification of the amount credited.

Suppose Assessee not able to justify the AO. AO shall impose section 68 and mark it as cash credits. Further, he shall revoke section 115BBE which will tax the cash credit at the maximum rate possible.

In our case, assessee has already paid the required tax to the government of India. Hence, there will not be any balance tax to be collected.

Now, AO shall also try to impose the section 270A to levy the penalty at 200%. So, let us now discuss the section 270A.

- Section 270A has been introduced in finance act, 2016.

- This section is applicable in case of under-reporting of income.

- The minimum penalty of 50% and maximum of 200% (only in case of misreporting) is prescribed in this section.

Analysis:

On the plain reading of this section, it is very clear that it is applicable in case of under reporting of income. Under-reporting of income means where assessed income is more than returned income.

In our case, assessed income shall be equal to returned income. As assessee has voluntary disclosed all the facts and information about the income. Since, the basic condition of this section is not triggered and hence, section 270A cannot be imposed.

Other possible options

- The other possible option for AO is the recourse of section 148. One may think that he may open the scrutiny proceeding of previous years. However, in that case, AO will have to record reasons to believe to open scrutiny under section 148. In our case, Assessee already declaring and disclosing all the income and paying the required taxes. Hence, this option may remain feasible for AO until he record reasons to believe.

- Income tax Raid: Income tax department may initiate IT raid as soon as they get to know about the deposits. However, this may only harass assessee because he has already disclosed all the income and paid all the tax on the cash deposited hence IT raid may become useless in this regard.

Conclusion

In the end, we observe that there is lack of income tax machinery under which penalty can be levied in the aforesaid case. However, these are my personal views. One can always differ. If you have any contrary view against my views, I would love to have them from you. You can send your views or queries at paras.mehra18@gmail.com.

Appeal from all professionals

I would also like to appeal to all the professionals in the industry about not too carried away by the media and the trends. This is the opportunity where we can prove our brain and ability. We are here to resolve the queries of our clients and general public not by unfair practices but through our own capability.

Let us unite together once again and lead the path of honesty, contribute to the society and to the great nation.

About the author

CA Paras Mehra is a practicing Chartered Accountant having a vast experience in this field of Taxation.