Summary: An Annual Information Statement (AIS) may include details of off-market transactions, which are share transfers made outside of a stock exchange. These transactions can appear in two sections of the AIS: the Taxpayer Information Summary (TIS) or the Sale of Securities section. Transactions listed in the TIS, such as those from gifts or inheritance, are generally for informational purposes and are not taxable. However, transactions in the ‘Sale of Securities’ section, like the sale of bonus shares with a zero acquisition cost, can have tax implications and must be carefully reviewed. Taxpayers should also be aware of potential mismatches between the AIS data and their own records. For example, a transaction might be incorrectly classified as a short-term capital gain in the AIS when it should be a long-term gain based on the holding period. In such cases, taxpayers should rely on their personal records, such as demat statements and broker reports, to correctly calculate and report capital gains in their Income Tax Return (ITR). Maintaining documentation is essential to support the figures reported in case of an inquiry from the tax authorities.

Off-Market Transactions In AIS – A Simple Guide For Taxpayers

1. The Annual Information Statement (AIS) now covers many financial activities, including off-market transactions—share transfers made outside the stock exchange. Taxpayers are often surprised to see these transactions in their AIS without fully understanding what they mean, why they are reported, or how they impact their tax filing.

2. This article explains the concept of off-market transactions, why they appear in AIS, and the precautions taxpayers should take when filing their returns.

3. Off-market transactions appear in the AIS in two ways—first, in the TIS summary, and second, under Sale of Securities.

4. In the TIS summary, off-market transactions usually involve transferring securities through gifting, inheritance, or similar methods. Since these transfers are not taxable when they happen, these entries are only for informational purposes and can be safely ignored when filing the ITR.

5. On the other hand, under the ‘Sale of Securities’ section, off-market transactions are cases where securities are sold or transferred. These might have tax implications, so taxpayers should carefully review the details to ensure proper reporting in their ITR. Let us understand this better with an Illustration.

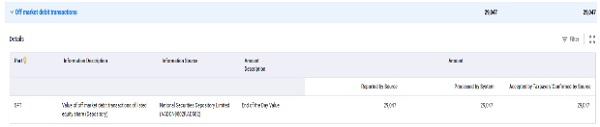

6. Illustration: Anupam extracted his Capital Gain details from AIS and downloaded them in Excel format. (For a complete step-by-step guide, read the article: How to Extract Capital Gain Details from AIS. https://taxguru.in/income-tax/extract-capital-gain-details-ais-step-by-step-guide. The transaction details are shown in the table below:

| Sl. | Name of Security | Asset Type | Credit Type | Sale consideration Rs. | Cost of Acquisition Rs. | Capital Gain Rs. |

| (a) | XYZ | Long Term | Off-Market | 1,00,000 | 0 | 1,00,000 |

| (b) | ABC | Short Term | Off-Market | 85,000 | 0 | 85,000 |

7. After careful verification, it was found that the cost of securities XYZ was zero, as these shares were received as bonus shares at no cost. In such cases, tax is payable on Rs. 1,00,000, and no further action is required.

8. Bonus Shares – Meaning and Tax Implications: Bonus shares, also called scrip dividends or capitalization issues, are additional fully paid-up shares a company issues to its existing shareholders at no cost, based on their current holdings. While receiving bonus shares doesn’t provide immediate financial gain, it’s important to understand how they are taxed.

Under Section 55(2)(aa)(i) of the Income Tax Act, the cost of acquiring bonus shares is considered zero. This means that when such shares are sold, the entire sale amount (after deducting expenses like brokerage) is used to determine capital gains. The tax treatment of these gains depends on whether the bonus shares are classified as short-term or long-term capital assets under Sections 45 and 48 of the Act.

9. The second case of ABC shares is not related to bonus shares. Mr. Anupam was surprised to see that AIS shows a short-term capital gain on the sale of ABC shares. In reality, he had been holding these shares for more than five years, having purchased them in FY 2019-20 for Rs 28,000. Since the holding period exceeds 12 months, the gain should correctly be classified as long-term capital gain (LTCG) and not short-term.

10. For Mr. Anupam, it was quite a challenge to dig up old records and retrieve the data needed to determine the acquisition cost of these shares. After much effort, he confirmed that the shares had indeed been purchased in FY 2019 for Rs . 28,000. He decided to recalculate his taxable capital gains after including the cost of ABC shares and is now prepared to file his return with accurate information and full confidence.

11. Checklist for Handling AIS Mismatches: A simple checklist can help taxpayers identify, verify, and correct AIS mismatches before filing their ITR:

(a) Verify with your records – Always cross-check AIS entries with demat statements, contract notes, and broker reports.

(b) Correct classification – Confirm whether the gain is short-term or long-term based on the actual holding period, not just what AIS shows.

(c ) Report accurately in the ITR – File the return with correct figures even if AIS reflects differently; consistency with records is key.

(d) Keep documents ready – Maintain proof of purchase and sale to support reporting if the tax department raises a query.

12. Sometimes, AIS may incorrectly classify a transaction—for example, showing short-term capital gains even when the shares qualify as long-term holdings. Such mismatches often occur due to incomplete or incorrect reporting by intermediaries. In these cases, taxpayers should rely on their own purchase and sale records to calculate the correct capital gains and report them accurately in the ITR. Supporting documents like contract notes and demat statements should be kept handy in case of any queries from the tax department.

Disclaimer: The article is for educational purposes only.

The author may be approached at caanitabhadra@gmail.com

Author Bio

A clear and succinct explanation. Thanks!