Section 92 of the Income Tax Act deals with any income or expense arising from an ‘International Transaction’. In order to understand the definition of ‘International Transaction’, it is essential to understand the definition of ‘Transaction’.

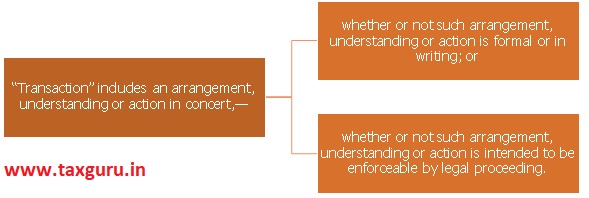

Clause (v) of Sections 92F of the Act defines a transaction as:

Section 92F of the Act provides an inclusive definition of the term “transaction”. Based on the reading of the section, it is evident that it is not necessary that for a transaction undertaken between two enterprises there needs to be a formal written agreement between them. It is only relevant whether a transaction has been entered into in substance. The section also negates the requirement as to the legal enforceability of agreement or understanding.

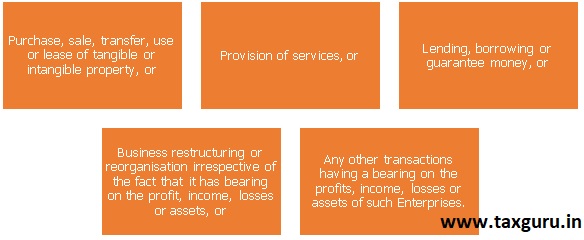

As per section 92B of the Act, the term international transaction refers to a transaction between two or more AEs, either or both of whom are non-residents, which is in nature of:

It also includes a mutual agreement or arrangement between two or more AEs for:

Further, a transaction entered into by an enterprise with a person other than an associated enterprise shall be deemed to be a transaction entered into between two AEs, if:

The definition of the term ‘international transaction’ also includes several other items including tangible / intangible property.

Author Bio