Interesting Issues Under Section 44AD, 44ADA And 44AE of The Income Tax Act,1961

Presumptive Taxation allows taxpayers to offer their income for tax without any compliance burden. This taxation scheme provides ease of doing business and simplify the taxation process for small business enterprises, traders and professionals. As per the Income tax Act, 1961, a person engaged in business or profession is required to maintain regular books of account and further, in some cases he has to get his accounts audited. To provide relief to small taxpayers from this tedious work, lawmakers framed “Special provisions for computing profit and gains on presumptive basis” under sections 44AD, 44ADA and 44AE. The taxpayer can declare his income at prescribed rates or higher than that.

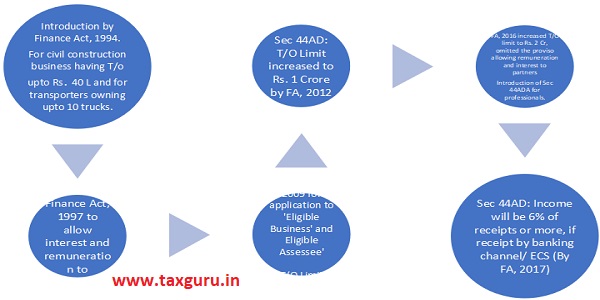

Historical Background

However, taxpayers are still facing numerous practical and technical issues while adopting these provisions. There have been fundamental issues such as maintenance of books of accounts for taxpayers adopting the specified schemes, other deductions and disallowances in PGBP, additions as per other provisions of the Act etc. In this write up, we will discuss the various technical and practical issues faced by taxpayers adopting the presumptive taxation scheme.

Page Contents

- A. Meaning of ‘Notwithstanding anything to the contrary contained in Sec. 28 to 43C’

- B. Is it mandatory for professionals opting for presumptive taxation to maintain books of account?

- C. No audit is required if turnover is up to Rs. 1 crore and taxable income is below exemption limit

- D. Applicability of TDS provisions after amendment by Finance Act, 2020

- E. Meaning of words ‘claimed to have been earned by the eligible assessee’

- F. Applicability of Section 44ADA to a partner of firm receiving remuneration and/or interest from the firm

- G. Presumptive Taxation in case of Partnership firms

- H. Changes in Tax Audit Turnover Limit under section 44AB by Finance Act 2020

A. Meaning of ‘Notwithstanding anything to the contrary contained in Sec. 28 to 43C’

The Section 44AD(1) begins with “Notwithstanding Anything to contrary contained in section 28 to 43C” it means section 28 to 43C of Income Tax Act, 1961 is not applicable on eligible assessee carrying on eligible business. Hence, no disallowance / no deemed income under Section 40(a), 40A, 40A(3), 40A(3A), 41 can be made.

Example : If any person opting for sec 44AD has made cash purchases worth Rs. 15,000 no disallowance can be made u/s 40A(3), even if the cash payment to a person exceeds Rs. 10,000 in a day. Cash payment to transporter in excess of Rs. 35,000 in a day shall not be disallowed.

Similarly, disallowance u/s 40A for excess payment to relatives cannot be made. No addition u/s 41 can be made.

Example : Mr. Y has claimed bad debts written off of Rs. 50,000 in year 2014-15. In P.Y. 2019-20 he has recovered Rs. 30,000. Separate addition of bad debts recovered may not be made if the profits are declared under presumptive taxation scheme.

Example : Mr. Saurav declaring income u/s 44AD has made payment of interest to non-resident. However, no TDS has been deducted. Whether the expense will be disallowed u/s 40(a)?

The interest expense will not be disallowed as sec 44AD overrides sec 40(a). The assessee was required to deduct TDS as per sec 195. Although, he has not deducted the TDS, expense will not be disallowed. However, he may be considered as assessee in default as per sec 201 and other penal provisions may be applicable as sec 44AD does not override TDS provisions. This issue is discussed in detail later in this article.

But a very interesting issue on the disallowance u/s 43B of the Income Tax Act,1961 has been considered by Panaji Tribunal in case of Good Luck Kinetic v. ITO (2015) 58. The Tribunal held that 44AD starts with “notwithstanding anything to the contrary contained in Sec. 28 to 43C” whereas section 43B starts with the words “notwithstanding anything contained in any other provisions of this Act”. The non-obstante clause in Sec. 43B has a far wider amplitude. Hence, disallowance could be made by invoking the provisions of Sec. 43B.

This is because the said provisions u/s 28 to 43C are provisions relating to the computation of business income of the Assessee. However, a perusal of the provisions of Sec. 43B shows that the said provision is a “restriction” on the allowance of a particular expenditure representing statutory liability and such other expenses, claimed in the profit and loss account unless the same has been paid before the due date of filing the return.

Further, the non-obstante clause in Sec. 43B has a far wider amplitude because it uses the words “notwithstanding anything contained in any other provisions of this Act”. Therefore, even assuming that the deduction is permissible or the deduction is deemed to have been allowed under any other provisions of this Act, still the control placed by the provisions of Sec. 43B in respect of the statutory liabilities still holds precedence over such allowance. This is because the dues to the crown has no limitation and has precedence over all other allowances and claims. The disallowance made by the AO by invoking the provisions of Sec. 43B of the Act in respect of the statutory liabilities are in order even though the Assessee’s income has been offered and assessed under the provisions of Sec. 44AF of the Act.

Therefore, considering the view held by the aforesaid Tribunal, addition/ disallowance can be made u/s 43B even though the income has been declared u/s 44AD, 44ADA or 44AE.

Example : Mr. Dawar, having turnover of Rs. 70,00,000 declared profit at 8% amounting to Rs. 5,60,000. He has not deposited employer’s share of EPF of Rs. 25,000 up to due date of return filing. Also, he has not paid bonus amounting to Rs.40,000 to his employees. Whether addition can be made u/s 43B if Mr. Dawar opts for sec 44AD?

Yes, addition can be made u/s 43B even if income is declared u/s 44AD. In this case the income will be assessed as:

| Profits declared u/s 44AD | Rs. 5,60,000 |

| Add-Disallowances u/s 43 B | |

| : EPF not deposited upto due date of return filing | Rs. 25,000 |

| : Bonus not paid upto due date of return filing | Rs. 40,000 |

| Assessed Income | Rs. 6,25,000 |

It is to be noted that if an assessee who has opted for presumptive taxation system, then as per Sec 44AD(3), any deduction allowable under sections 30 to 38 shall be deemed to have been already given effect to and no further deduction under those sections shall be allowed. It is to be noted that deduction for depreciation which is allowed u/s 32 shall be deemed to be allowed. Therefore, current year depreciation as well as unabsorbed depreciation i.e. brought forward depreciation shall not be allowed. However, WDV of the block of assets shall be calculated as if the depreciation has been allowed.

Sec 44AD overrides sec 28 to 43 C but does not override chapter VI. Therefore, current year losses & brought forward losses can be set off against deemed income. The same was held by ITAT, Pune in the case of DCIT v. Sunil M. Kankariya [2008].

Example:

Mr. Y has turnover of Rs. 50,00,000 for the P.Y. 2019-20. He has declared profits at the rate of 8% amounting to Rs. 4,00,000. He has bought machinery worth Rs. 12,00,000 on 15/04/2019. He has loss from house property of Rs. 75,000. Can he deduct depreciation of Rs.1,80,000 (15% of Rs.12,00,000) and set off loss from the above profit of Rs.4,00,000?

No, depreciation shall not be reduced from the above profits. It is deemed that depreciation has been already claimed and allowed. The closing WDV as on 31/03/2020 shall be Rs. 10,20,000 (12,00,000 – 1,80,000).

Mr. Y shall be allowed to set off the loss of Rs. 75,000. The total income will be Rs.3,25,000 (4,00,000 – 75,000)

B. Is it mandatory for professionals opting for presumptive taxation to maintain books of account?

A very interesting issue is that if a professional who has opted presumptive system of taxation has to maintain books of account also. To resolve this issue firstly we have to see the provisions of section 44AA(1) of the Act. Sec 44AA reads as:

“44AA- (1) Every person carrying on legal, medical, engineering or architectural profession or the profession of accountancy or technical consultancy or interior decoration or any other profession as is notified by the Board in the Official Gazette shall keep and maintain such books of account and other documents as may enable the Assessing Officer to compute his total income in accordance with the provisions of this Act.

(2) Every person carrying on business or profession [not being a profession referred to in sub-section (1)] shall,—

(i) if his income from business or profession exceeds one lakh twenty thousand rupees or his total sales, turnover or gross receipts, as the case may be, in business or profession exceed or exceeds ten lakh rupees in any one of the three years immediately preceding the previous year; or

(ii) where the business or profession is newly set up in any previous year, if his income from business or profession is likely to exceed one lakh twenty thousand rupees or his total sales, turnover or gross receipts, as the case may be, in business or profession are or is likely to exceed ten lakh rupees, during such previous year; or

(iii) where the profits and gains from the business are deemed to be the profits and gains of the assessee under section 44AE or section 44BB or section 44BBB, as the case may be, and the assessee has claimed his income to be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, during such previous year; or

(iv) where the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,

keep and maintain such books of account and other documents as may enable the Assessing Officer to compute his total income in accordance with the provisions of this Act:

Provided that in the case of a person being an individual or a Hindu undivided family, the provisions of clause (i) and clause (ii) shall have effect, as if for the words “one lakh twenty thousand rupees”, the words “two lakh fifty thousand rupees” had been substituted :

Provided further that in the case of a person being an individual or a Hindu undivided family, the provisions of clause (i) and clause (ii) shall have effect, as if for the words “ten lakh rupees”, the words “twenty-five lakh rupees” had been substituted.

(3) The Board may, having regard to the nature of the business or profession carried on by any class of persons, prescribe, by rules, the books of account and other documents (including inventories, wherever necessary) to be kept and maintained under sub-section (1) or sub-section (2), the particulars to be contained therein and the form and the manner in which and the place at which they shall be kept and maintained.

(4) Without prejudice to the provisions of sub-section (3), the Board may prescribe, by rules, the period for which the books of account and other documents to be kept and maintained under sub-section (1) or sub-section (2) shall be retained.”

From the perusal of above section, it is clear that it is mandatory for the professional who is covered under Section 44ADA to maintain books of accounts even though he has opted for the presumptive taxation scheme. Although, the Memorandum to the Finance Bill, 2016 provides that an assessee opting for Section 44ADA would not be required to maintain books of account under Section 44AA(1), the same has not been brought out clearly in the Section 44AA. Section 44AA is silent in relation to the assessee who is covered by Section 44ADA. Moreover the provisions of Sec 44ADA overrides sec 28 to 43C and not sec 44AA of the Act. Hence, on combined reading of 44AA(1), 44AA(3) read with Rule 6F, the specified professionals would need to maintain books of account even if they opt for section 44ADA.

However, as per the FAQs on presumptive taxation issued by Income Tax Department provides that if assessee declares income u/s 44ADA, there is no need to maintain books of account. The FAQ issued is provided here

“If a person adopts the presumptive taxation scheme of section 44ADA, then he is required to maintain books of account as per section 44AA?

In case of a person engaged in a specified profession as referred in sections 44AA(1) and opts for presumptive taxation scheme of sections 44ADA, the provision of sections 44AA relating to maintenance of books of account will not apply. In other words, if a person opt for the provisions of sections 44ADA and declares income @50% of the gross receipts, then he is not required to maintain the books of account in respect of specified profession.”

From the above FAQ it can be concluded that person opting for sec 44ADA would not be required to maintain books of account. However, the FAQs do not have any legal backing and it may change in future.

C. No audit is required if turnover is up to Rs. 1 crore and taxable income is below exemption limit

To resolve this issue, firstly we have read the relevant provisions of sec 44AD of the Act which are as under

“(4) Where an eligible assessee declares profit for any previous year in accordance with the provisions of this section and he declares profit for any of the five assessment years relevant to the previous year succeeding such previous year not in accordance with the provisions of sub-section (1), he shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the previous year in which the profit has not been declared in accordance with the provisions of sub-section (1).

(5) Notwithstanding anything contained in the foregoing provisions of this section, an eligible assessee to whom the provisions of sub-section (4) are applicable

and

whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB.”

| Income from Eligible Business | Total Income | Applicability of Section 44AD | Applicability of section 44AA | Applicability of section 44AB |

| More than 8% of turnover | Exceeds basic Exemption Limit | YES | NO | NO |

| Less than 8% of Turnover | Exceeds basic Exemption Limit | NO | YES | YES |

| Less than 8% of Turnover | Dose not Exceeds basic Exemption Limit | NO | NO | NO |

| Equal to 8% of Turnover | Exceeds basic Exemption Limit | YES | NO | NO |

From the reading of above provisions, it is concluded that there are two conditions of sec 44AD(5) of the Act. The first is regarding applicablility of provisions of sec 44AD(4) of the Act and the second is that the income of assessee is more than the basic exemption limit. These both conditions are connected with word “and”. These two conditions must be fulfilled simultaneously. If the assessee fails to fulfill any one condition or both, then the assessee is not required to maintain books of account and not to get the accounts audited.

In other words, we can say that the assessee is bound to get the books of accounts audited, if the following two conditions are satisfied:-

a. The profits and gains are lower than the prescribed rates i.e lower than 8% or 6% of turnover if income declared u/s 44AD of the Act.

b. The total income of the assessee exceeds the maximum amount which is not chargeable to income tax

To claim the benefit of above sec 44AD(5),firstly we have to see the meaning of total income. As per sec 2(45) of the Act. Total income means the total amount of income referred to in section 5 computed in the manner laid down in the Act. Thus total income for the purpose of Sec 44AD(5) would be determined as under :

i) Income from all heads of income be aggregated after adjusting for brought forward losses, unabsorbed depreciation, etc. and after excluding exempt incomes;

ii) From the resultant, amount eligible for deduction under Chapter VI-A will be deducted.

iii) Balance will be total income for the purposes of section 44AD(5)

iv) If the total income is below the maximum amount not chargeable to tax in the case of assessee then the assessee will not be required to maintain books and get them audited if he declares profit from eligible business lower than that deemed under section 44AD.

Further, if any individual/HUF has incurred loss, then also there is no need to maintain books and to get them audited.

It is to noted that above exemption can be claimed only by individual or HUF and not in case of partnership firm a Firm as partnership firm do not avail any basic exemption limit , hence ,Tax Audit u/s 44AB is applicable. These provisions can be presented in tabular form as under:

| More than 8% of turnover | Exceeds basic Exemption Limit | YES | NO | NO |

| Less than 8% of Turnover | Exceeds basic Exemption Limit | NO | YES | YES |

| Less than 8% of Turnover | Dose not Exceeds basic Exemption Limit | NO | NO | NO |

| Equal to 8% of Turnover | Exceeds basic Exemption Limit | YES | NO | NO |

Example : Mr. Fancy aged about 52 years runs a grocery shop. He sells goods on cash basis only. For the P.Y. 2019-20, he provides the following information. He has no income other than profits from his shop. Whether Mr. Fancy will be required to get books of account audited?

| Case | Sale/Receipts | Net Profit | 8% of Sale | Whether Audit Applicable? |

| 1 | Rs. 80,00,000 | RS.4,00,000 | Rs.6,40,000 | Yes, because profit lower than 8% of sale and his total income exceeds basic exemption limit. |

| 2 | Rs. 60,00,000 | Rs.2,25,000 | Rs.4,80,000 | No, because his total income is less than basic exemption limit of Rs.2,50,000 even though profits are less than 8% of sale. |

| 3 | Rs.1,40,00,000 | Rs.1,75,000 | Rs.11,20,000 | Yes, because sale has exceeded Rs. 1 crore. therefore, this case is covered u/s 44AB(a) and not 44AB(e). It is to be noted that limit u/s 44AB(a) is Rs. 1 crore and not Rs.2 crore. However, if the assessee having turnover up to Rs. 2 crore opts for sec 44AD, then he will not be required to get his books audited. |

| 4 | Rs. 70,00,000 | Rs.9,00,000 | Rs.5,60,000 | No, as he has declared profits more than the 8%. |

D. Applicability of TDS provisions after amendment by Finance Act, 2020

It is to be noted that the provisions for presumptive taxation override only sec 28 to 43C and not the provisions of TDS. Therefore, assessee declaring income u/s 44AD, 44ADA or 44AE is liable to deduct TDS. e.g. Every ‘person’ is required to deduct TDS u/s 192 if the estimated salary exceeds the maximum amount not chargeable to tax. Any individual paying salary of Rs. 8,50,000 p.a. would be required to deduct TDS even though he is declaring income u/s 44AD.

Further, sec 194A, 194C, 194H, 194I and 194J have been amended by Finance Act, 2020.

Now, individual or HUF having turnover/ gross receipts of more than Rs. 1 crore in case of business and more than Rs. 50 Lakh in case of profession during the preceding financial year shall be required to deduct TDS under the above sections. Earlier in sec 194A, 194H, 194I and 194J it was mentioned that if the turnover/ receipts exceed the monetary limits specified u/s 44AB in the preceding financial year. In sec 194C, it was if individual or HUF was liable for audit under clause (a) or (b) of section 44AB in the preceding financial year.

Effect of amendment: The persons having turnover of more than Rs. 1 crore but less than Rs. 2 crore and declaring income u/s 44AD would be required to deduct TDS under the above sections.

Example 8:

Mr. A has a turnover of Rs. 1,25,00,000 in the P.Y. 2018-19. In F.Y. 2019-20 he paid interest of Rs. 25,000. Whether Mr. A has to deduct TDS u/s 194A if he declares income u/s 44AD?

Yes, Mr. A will be required to deduct TDS u/s 194A as his turnover in the preceding F.Y. is above Rs. 1 crore. The interest amount is above Rs. 5,000. Hence, Mr. A will be required to deduct TDS even if income is declared u/s 44AD otherwise he will be deemed as assessee in default as per sec 201. However, he does not deduct TDS, no disallowance of expense will be made as per sec 40(a).

E. Meaning of words ‘claimed to have been earned by the eligible assessee’

To understand the meaning of the term claimed to have been earned by the eligible assessee, firstly we have to read the sec 44AD(1) of the Act. Sec 44AD. (1) reads as

“Notwithstanding anything to the contrary contained in sections 28 to 43C, in the case of an eligible assessee engaged in an eligible business, a sum equal to eight per cent of the total turnover or gross receipts of the assessee in the previous year on account of such business or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the eligible assessee, shall be deemed to be the profits and gains of such business chargeable to tax under the head “Profits and gains of business or profession”

The section has been amended for the benefit of the assessee and the words claimed to have been earned by the eligible assessee. By the introduction of these words in section 44AD(1), the legislature shows his intention to accept specified income as returned income even if higher sum is earned by eligible assessee unless it is claimed by assessee in his Income Tax Return. The word “Claim” signifies the right of assessee, and it is not an obligation of the assessee. The distinction between Right and obligation is very necessary here. The language of section of section 44AD(1) requires claims to have been made by an assessee for returning higher income. If there is no claim made by assessee in return for higher income, there is no higher income. The assessee , who has opted presumptive taxation system ,is under no obligation to explain individual entry of cash deposit in bank unless such entry has no nexus with gross receipts.

[CIT v. Surinder Pal Anand [2010] 192 TAXMAN 264 (PUNJ. & HAR.)

Example– Mr. Sham is carrying on business. The Turnover is Rs.90 Lacs. The profit as per his books or calculation is Rs.9 Lakhs. However, he opts to return the income under section 44AD @ 8% i.e. Rs.7.20 lacs. Now a question arises regarding the power of AO to assess the difference of 1.8 lacs as undisclosed income. In this case Mr. Sham has claimed the income of Rs.7.20 lac as in his return of income as his claim. The assessee is free to exercise this option at his will. Legally he is given the option by the statute and such an option cannot be equated with obligation cast upon the assessee. There is a definite difference between OPTION and OBLIGATION and an Option granted to the assessee cannot be construed to be his obligation when his actual income is more than 8% of Turnover. The AO cannot make any addition on this count as there is no provision under the Act permitting to make such addition. Further, the words used are “higher income claimed to have been earned by the assessee”. It is to clarified that if the assessee has not made a claim in the Return of Income regarding any higher income, it implies there is no claim for Higher Income made by assessee. AO cannot claim that the assessee has earned higher income, because under the statue, he is not entitled to do so.

F. Applicability of Section 44ADA to a partner of firm receiving remuneration and/or interest from the firm

A very interesting is that whether the provisions of Section 44ADA shall be applicable to the remuneration and other receipts by a partner from a professional services firm? In this connection, it is to be noted that the Income Tax Act, 1961 vide Section 40(b) states that the firm is eligible to claim remuneration as deduction to the extent specified therein and such remuneration is deductible in hands of the firm. The balance amounts are subjected to tax as profits in the hands of the firm. In other words, the eligible remuneration is deductible in the hands of firm and taxable in hands of partners, the remainder (profit) is taxable in hands of the firm and exempted in the hands of partners u/s 10(2A).

Hence, in the hands of the partner, the following will be the impact:

1. Remuneration which was allowed as deduction in firm will be taxable

2. Profit which was taxed in the hands of the firm will be exempt.

Now a question arises whether the remuneration and other income received from the firm can be called as ‘gross receipts’ for the purposes of Section 44ADA. Whether the share of profits of a partner can be

considered as gross receipts for the purpose of Section 44ADA? The Mumbai Bench of the Income Tax Appellate Tribunal in the case of: ACIT v. India Magnum Fund (81 ITD 295) held that in order to trigger the provisions of Section 44AB, there should be first computation of profits and gains of business or profession i.e. computation of total income as per Section 4. As the income exempt under Section 10 does not form part of the total income, such exempt income cannot be subjected to the provisions of Section 44AB. Consequently, one may argue that share of partners profit which is exempt under section 10(2A) would not be considered for the purposes of the gross receipts This view is also supported by the guidance note issued by the Institute of Chartered Accountants of India on tax audit. As per the guidance note,gross receipts exclude partner’s share of profit which is exempt u/s 10(2A).

We are of the opinion that the provisions of Section 44ADA is applicable either for an individual or partner in a profession firm. This is also supported by certain judicial pronouncements (though not directly on the said issue) in the case of Sagar Dutta vs DCIT (ITAT Kolkata) and Usha A Narayanan vs Deputy Commissioner of Income Tax (ITAT Kolkata). The following is evident from the above judgments:

1. In both the judgments, the tax payers were chartered accountants in partner capacity in a firm.

2. Both of them have received remuneration, salary, interest on capital and others more than the threshold limit specified under Section 44AB.

3. The department is of the view that since the gross receipts (remuneration, salary, interest on capital and others) were in excess of threshold limits specified under Section 44AB, the tax payers would have got their books of accounts and audited.

4. Since the tax payers failed to do so, the department has levied penalty under Section 271B amounting to .5% of the receipts.

5. The tax payers contention was that they were not carrying any profession in individual capacity but they were acting as partner and hence tax audit requirements does not attract.

Both the Tribunals relying on Amar Ganguly judgment, stated that the tax audit will be applicable despite the individual is receiving amounts from firm. Hence, such amounts being in excess of threshold limit, the books of accounts need to be audited and confirmed the penalty.

Our Inference from the above judgments:

Based on the above judgments, the question that whether the salary, remuneration, profit, interest on capital and others received by partner from a partnership firm can be called as gross receipts for the purposes of 44ADA is answered in positive. If such amounts are not to be called as gross receipts, then there is no requirement for the Tribunals to state that such individuals would fall under ambit of Section 44AB.

In light of the above, the amounts received from the firm can be considered as gross receipts and accordingly provisions of Section 44ADA will be applicable. Hence, the benefit of 50% of gross receipts offering to income tax is possible.

Further, one more question that is to be answered is whether the provision of Section 44ADA is optional or mandatory, that is to say, is it mandatory for the partner whose gross receipts is less than 50 lakhs to apply the provisions of Section 44ADA or is it optional. Once the gross receipts are less than Rs 50 lakhs, the partner has to mandatorily offer 50% of such gross receipts for tax. In a case, where the partner thinks his expenditure is more than 50% or want to offer lower amounts of gross receipts for tax, he should then get his books of accounts audited as per provisions of sub-section (4) of Section 44ADA.

G. Presumptive Taxation in case of Partnership firms

Resident Partnership Firms are eligible to opt for presumptive taxation u/s 44AD or 44ADA or 44AE. Sec 44AD and 44AE were amended in 1997 w.e.f 01/04/1994 to allow remuneration and interest to partners (subject to conditions and limits specified in section 40(b)) after determination of profits as per sec 44AD or 44AE. However, by Finance Act, 2016, second proviso to Section 44AD(2) has been omitted which provided for deduction under section 40(b) with regard to the salary and interest to partners. However, sec 44AE has not been amended. Hence, remuneration and interest to partners will not be allowed in sec 44AD and 44ADA. However, remuneration and interest to partners will be allowed if income is declared u/s 44AE.

Example : RSK & Associates, a firm of Chartered Accountants provides the following information:

| Receipts | Net Profit | 50% of receipt | Allowability of remuneration |

| Rs.40,00,000 | Rs.20,00,000 | Rs.20,00,000 | No remuneration and interest will be allowed as expense. |

| Rs.40,00,000 | Rs.24,00,000 | Rs.20,00,000 | Remuneration and interest can be allowed up to Rs. 4,00,000, subject to sec 40(b) |

| Rs.40,00,000 | Rs.18,00,000 | Rs.20,00,000 | Sec 44ADA not applicable as profit is claimed to be less than 50% of receipts. RSK & Associates will be required to get their books of account audited u/s 44AB(d). Remuneration may allowed as per sec 40(b). |

H. Changes in Tax Audit Turnover Limit under section 44AB by Finance Act 2020

Currently, businesses having turnover of more than one crore rupees are required to get their books of accounts audited by an accountant. In order to reduce the compliance burden on small retailers, traders, shopkeepers who comprise the MSME sector, the Finance Act 2020 has raised the limit of audit by five times the turnover threshold for audit from the existing Rs. 1 crore to Rs. 5 crores.

Further, in order to boost less cash economy, it has been provided that the increased limit for mandatory tax audit shall apply only to those businesses which carry out less than 5% of their business transactions in cash. But in this connection, following points are to be noted

1. This threshold limit for the applicability of mandatory tax audits is applicable to business entity only and limit for a professional assessee shall continue to be at Rs. 50 lacs even if he receives entire consideration in non-cash mode.

2. It is not provided that who will certify the margin of transactions in cash mode of 5 percent. It appears that the assessee is himself require to declare the percentage of receipt in cash mode and non-cash mode.

3. The provision to increase the turnover limit for a mandatory tax audit is amended to benefit the MSME sector.

4. The amendment is carried out only in section 44AB. No amendment is made in section 44AD and thus the turnover limit of Rs. 2 crores shall continue. Suppose an assessee is having a turnover of 180 lacs for the financial year 2020-21 and all the transactions of business are by non-cash modes. The net profit of the assessee is Rs.7 lacs. which less than 6% of turnover of the assessee. Now as per the provisions of sec 44AD, the assessee is required to maintain books of account and get them audited u/s 44AB of the Act.

5. The term ‘aggregate of all receipts and aggregate of all payments’ is very wide and covers not only the receipts and payments on account of turnover or sales but all other business transactions. Capital introduction, receipt and repayment of a loan, etc., partners’ drawings, payment of freights, etc. Even payment of taxes made in cash will come within the purview of cash transactions.

CA R.S. Kalra (98889-27000, ca.rskalra@yahoo.com)

CA Jasmeet Singh (86997-01271, jasmeetsingh1699@gmail.com)

Author Bio

If a sole proprietor opt for presumptive taxation scheme and his turnover exceeds 1 crore then its compulsory to deduct TDS ? Whether he should apply for TAN ?

sir, if an assessee declare income u/s 44AD in f.y. 2019/20 and 2020/21, and had paid advertisement exps of Rs 80 lacs in each year, and the assesse had not deducted TDS on advertisement , what is action for Income Tax Department. and what is remedy for the assessee

Sir

Say the Turnover of a partnership claiming income under 44AD is 1.5Cr and income is Rs 1.00 Cr ie only 50 Lakhs expenses..firm is paying tax at 12L being 8% of Turnover..so if the firm is a partnership firm having 2 partners so can each of such partners get 44L free of tax(1.Cr -12.Lakhs/2). Since the actual profit will be transfered to partners current account and thus 44L can be withrawn by each partners as drawings to his or her account without any payment of tax. please reply or contact me at 7012649663

Sir ,

my concern under works contract and IT filling under sec 44AD. I prepare P&L B/S in every year. what is the limitation of salary total 8.50Lakhs ?

Hello sir. In 44 ADA it has been specified that if the professional has shown net profit less than 50%, then he’s subject to audit u/s 44ab. But Let’s take a case of a CA partnership firm with a turnover of 40 lakhs. Even if they don’t claim any expenditure but for partner’s remuneration u/s 40(b) still the net profit will be less than 50% as 40(b) allows for 60% of net profit (+90000). So does it imply that all professional firms enjoying full 40(b) limits are subjected to tax Audit? Thanks in advance

Excellent work sir , I feel almost criminal to read this for free . Kudos .

My turnover is Rs.40 lakhs, actual profit is Rs.36 lakhs and file my return of income u/s.44AD showing profit of 3.2 lakhs. However I have made investments of Rs.35 lakhs in the year. Can AO invoke section 69?

Also now if I say I’d made profit of Rs.36 lakhs doesn’t that amount to “Claiming” higher profit?

Sir

The provison which says that if 44AD is not opted for in any 5 consecutive years then the assessee will not hav the option to avail the benefit of presumptive taxation in the next 5 years…is it also there in 44ADA or onoy for 44AD

I am a salaried person. My employer deducts TDS under section 192b. Can I opt for presumptive taxation under section 44ADA?

Tuition income is not covered u/s 44ADA For detiail study you can download my book on Practical Approach To Presumptive Tax

whether tution income can be covered u/s 44ADA

Sir,

A query

Even section 40A starts with,

“The provisions of this section shall have effect notwithstanding anything to the contrary contained in any other provision of this Act.”

Can you please highlight on the meaning of this phrase

Thanks and regards

Animesh Agrawal

good informative

Very good educational, informative material

very good article.. covered mostly all points and pratical issues regarding presumptive taxation except the new entry and exit provisions in reference to tax audit.