Income Tax E-Proceedings FAQs

Q.1 What is e-Proceedings?

Ans. e-Proceedings is an electronic platform for conducting proceedings in an end to end manner using the e-Filing portal. Using this service, any registered user (or his Authorized Representative) can view and submit response to any notice / intimation / letter issued by the Income Tax Department.

Q. 2 What are the benefits of e-Proceedings?

Ans. e-Proceedings is a simple way to respond electronically to all notices / intimation / letters issued by Income Tax Department. It reduces the compliance burden of the taxpayer as there is no need to visit the Income Tax Office. Further, it is easy to keep track of the submissions and record keeping for future reference.

Q.3 Can I view my response once I have submitted my response to the notice issued to me?

Ans. Yes, you can view the response submitted by you or by your Authorized Representative.

Q. 4 Where can I see if any query has been raised against my response given on Adjustment u/s 143(1)(a) issued to me?

Ans. You can view the queries raised by the Income Tax Department under e-Proceedings.

Q.5 I have 4 days left prior to the Proceeding Limitation Date. Why am I unable to submit my response?

Ans. If your proceeding status is open, the Submit Response option will be available only till 7 days prior to the Proceeding Limitation Date, till 6 PM. If there is no Proceeding Limitation date, the Income Tax Authority can close the e-submission option. However, at the option of the Income Tax Authority, the submission window can be re-enabled till the Proceeding Limitation Date.

Q.6 Can I edit my response after responding to a notice on the e-Filing portal?

Ans. No, you cannot edit your response once submitted on the e-Filing portal.

Q.7 What are the notices/orders can I respond to under e-Proceedings?

Ans. All notices / intimations / letters issued by the Income Tax Department and CPC are made available under e-Proceedings where you can view and submit the response along with attachments by uploading the same on the e-Filing portal. You can view and submit response to the following notices through this service

- Defective Notice u/s 139(9)

- Intimation u/s 245 – Adjustment against demand

- Prima Facie Adjustment u/s 143(1)(a)

- Suo-moto Rectification u/s 154

- Notices issued by Assessing Officer

- Seek for Clarification communication

Q. 8 In the respond to notice issued by AO, the number/size of attachments is more than the permitted size, what should I do?

Ans. The maximum size permitted of a single attachment should be 5 MB. In case you have more than 1 document to upload, you can put them together in a zipped folder and upload the folder. The maximum size of all attachments in a zipped folder should be 50 MB. If the size of the single document or the zipped folder exceeds the permitted limit, you can optimize the document/folder by reducing the file size.

Q. 9 What is intimation u/s 245 and is it mandatory to respond to 245 intimation issued to me by the Income Tax Department?

Ans. Intimation u/s 245 is issued by the Income Tax Department to intimate taxpayers that the Department proposed to adjust the previous year’s pending tax payable (demand) with the current year’s refund. In case no response is received within 30 days of the issue of this intimation, the return of income will be processed after making necessary adjustment(s).

Q. 10 What is a Defective Return?

Ans. A return may be treated as defective on account of incomplete or inconsistent information in the return or in the schedules or for any other reason.

Q. 11 How do I know if my return is defective?

Ans. If your return is found defective, the Income Tax Department will send you a defective notice u/s 139(9) of the Income Tax Act via email on your registered email ID and the same can be viewed by logging in to the e-Filing portal.

Q. 12 Can I update or withdraw my response after submitting the response on the e-Filing portal?

Ans. No, you cannot update or withdraw your response once submitted on the e-Filing portal.

Q. 13 Can I authorize another person to respond to my Defective Notice?

Ans. Yes, you can authorize another person to respond to the defective notice u/s 139(9).

Q. 14 Can I correct the defect in the ITR Form online?

Ans. Yes, you can submit the response by online correcting the defect in the ITR Form.

Q. 15 What is the time limit within which I can respond to a Defective Notice sent by Income Tax Department?

Ans. If your return is found defective, you will get 15 days of time from the date of receiving the notice or as the time duration specified in the notice to rectify the defect in the return filed by you. However, you may Seek Adjournment and request for an extension.

Q. 16 What if I don’t respond to a Defective Notice?

Ans. If you fail to respond to the defective notice within stipulated period then your return may be treated as invalid and therefore consequences such as penalty, interest, non-carry forward of losses, loss of specific exemptions may occur, as the case may be in accordance with the Income Tax Act.

Q. 17 I have been notified about defective returns u/s 139(9). Can I file the return as fresh return for that Assessment Year?

Ans. Yes, you can either file the return as a fresh / revised return incase the time provided for filing the return in a particular Assessment Year has not lapsed or alternatively you can also choose to respond to Notice u/s139. However, once the time provided for filing the return for a particular Assessment Year has lapsed, you will not be able file the return as a fresh / revised return and you will have to respond to Notice u/s 139(9). If you are unable to respond to the notice, the return will be treated as invalid or not filed for that Assessment Year.

Q. 18 What are some of the common errors that make a return defective?

Ans. Some of the common errors that make a return defective are as follows:

- Credit for TDS has been claimed but the corresponding receipts/income has been omitted to be offered for taxation

- The gross receipts shown in Form 26AS, on which credit for TDS has been claimed, are higher than the total of the receipts shown under all heads of income, in the return of income.

- Gross Total Income and all the heads of income is entered as nil or 0 but tax liability has been computed and paid.

- Name of taxpayer in ITR does not match with the name as per the PAN database.

- Taxpayer having income under the head Profits and Gains of Business or Profession but has not filled Balance Sheet and Profit and Loss Account.

Q.19 What is Seek for Clarification communication?

Ans. Seek for Clarification communication is sent to the taxpayer, if there are instances where the information provided under a schedule or annexures of the return is insufficient or inadequate and clarification is required on certain claims made by the taxpayer.

Q. 20 Do I need to log in to e-Filing portal to view and submit response using e-Proceedings service?

Ans. Yes, you will be required to log in to the e-Filing portal to view and submit response using e-Proceedings service.

Q. 21 Do I need to e-Verify the response / submission made using the e-Proceedings service?

Ans. Yes, you will be required to e-Verify the response submitted by you using the e-Proceedings service.

Q. 22 Can I respond to a Seek for Clarification Notice without logging on to the e-Filing portal?

Ans. No, you will be required to log in to respond to a Seek for Clarification communication. You will not be able to either view the notice or submit the response to the notice issued to you.

Q.23 Can somebody else respond to the notices issued to me by the Income Tax Authority on my behalf using the e-Proceedings service?

Ans. Yes, you can add an Authorized Representative to respond to a notice on your behalf using the e-Proceedings service except in case of Intimation u/s 245.

Q. 24 Can I remove an already added / existing Authorized Representative?

Ans. Yes, you can remove or withdraw the representative authorized by you.

Q. 25 Can I add two Authorized Representatives to respond to the notice issued to me?

Ans. No, you can only have one Authorized Representative active at a time for a proceeding.

Q. 26. I have filed a revised return. Do I still need to respond to the Seek for Clarification communication issued to me?

Ans. No, it will not be allowed to submit a response in case you have already filed a revised return for the same assessment year. A message stating ‘Revised Return has been filed against this notice; no further action is required’ will be displayed.

Q. 27 Is it mandatory for me to respond to the Seek for Clarification communication issued to me? If yes, then what is the time limit within which I should submit my response?

Ans. You should submit / provide your response as per the due date mentioned in the communication issued to you. In case the due date has passed and no response has been provided, CPC will process the return with the information available with them.

Q. 28 I am not able to add an Authorized Representative for the Intimation u/s 245. What should I do?

Ans. For the Intimation u/s 245, you cannot add an Authorized Representative. An Authorized Representative may on your behalf respond to the following notices:

- Defective Notice u/s 139(9)

- Prima Facie Adjustment u/s 143(1)(a)

- Suo-moto Rectification u/s 154

- Notices issued by Assessing Officers (ITBA Notices)

- Seek for clarification communication

Income Tax E-Proceedings Manual

1. Overview

The e-Proceedings service is available to all registered users to view and submit a response to the notices / intimations / letters issued by Assessing Officer, CPC or any other Income Tax Authority. Following notices / intimations / letters can be viewed and responded to, using the e-Proceedings service:

- Defective Notice u/s 139(9)

- Intimation u/s 245 – Adjustment against Demand

- Prima Facie Adjustment u/s 143(1)(a)

- Suo-moto Rectification u/s 154

- Notices issued by Assessing Officer or any other Income Tax Authority

- Seek for Clarification communication

Additionally, a registered user can also add or withdraw an Authorized Representative to respond to any of the above listed notice / intimations / letters.

2. Prerequisites to Avail This Service

- Registered user on e-Filing portal with a valid user ID and password

- Active PAN

- Notice / intimation / letter from the Department (AO / CPC / Any other Income Tax Authority)

- Authorized to act as Authorized Representative (in case Authorized Representative wants to respond on behalf of taxpayer)

- Active TAN (in case of TAN proceedings)

3. Step-by-Step Guide

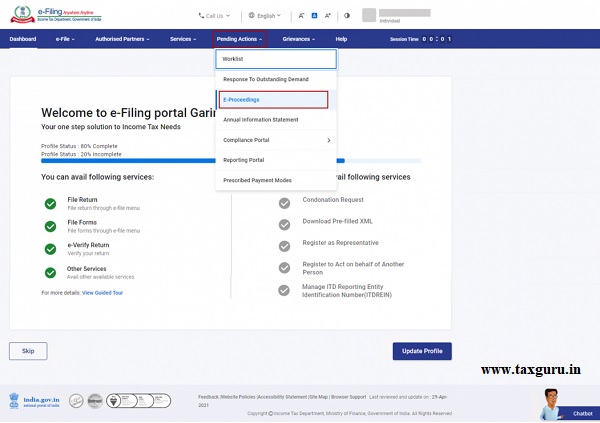

Step 1: Log in to the e-Filing portal using your user ID and password.

Step 2: On your Dashboard, click Pending Actions > e-Proceedings.

Step 3: On the e-Proceedings page, click Self.

Note:

- If you log in as an Authorized Representative, click As Authorized Representative, and you will be able to view details of the notice.

- If you required to respond to a notice that has been issued as part of compliance under notice section 133(6) or 131 to self -PAN/TAN, click Of Other PAN/TAN.

| Defective Notice u/s 139(9) | Refer to Section 3.1 |

| Intimation u/s 245 – Adjustment against Demand | Refer to Section 3.2 |

| Prima Facie Adjustment u/s 143(1)(a) | Refer to Section 3.3 |

| Suo-moto Rectification u/s 154 | Refer to Section 3.4 |

| Notices issued by Assessing Officer or any other Income Tax Authority | Refer to Section 3.5 |

| Seek for Clarification Communication | Refer to Section 3.6 |

| To add/withdraw Authorized Representative | Refer to Section 3.7 |

3.1. To view and submit response to Defective Notice u/s 139(9):

Step 1: Click View Notice corresponding to the Defective Notice u/s 139(9) and you can:

| View and Download Notice | Follow Step 2 and Step 3 |

| Submit Response | Follow Step 4 to Step 7 |

To View and Download Notice

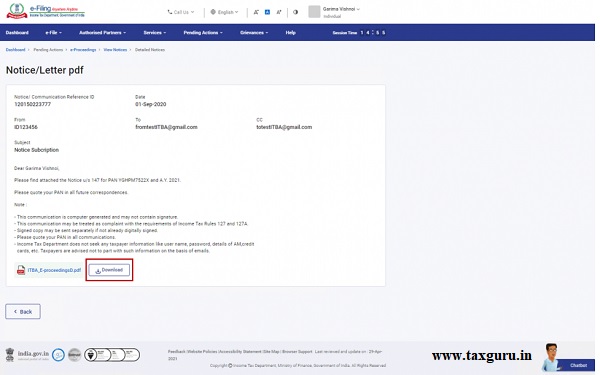

Step 2: Click Notice/Letter pdf.

Step 3: You will be able to view the notice issued to you. If you wish to download the notice, click Download.

To Submit Response

Step 4: Click Submit Response.

Step 5: You can either select Agree or Disagree.

Step 5a: If you select Agree, then select Mode of Response as Online (Click Proceed with ITR and you will be able to open the ITR form online for the correction of defect) or Offline (upload the correct XML/ JSON file as applicable) and click Continue.

Note: If you select Offline Utility, you will be required to click Download and then upload the correct XML/ JSON file as applicable.

Step 5b: If you select Disagree, then select the reason from the list of options given in the dropdown and click Continue.

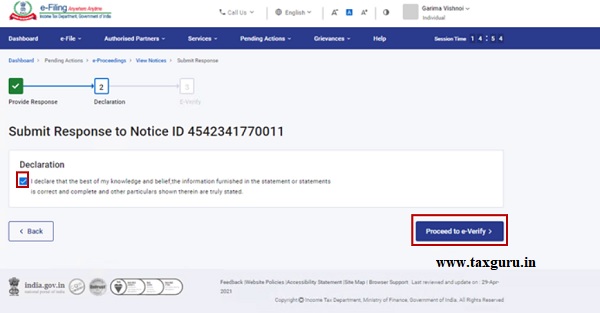

Step 6: Select the Declaration checkbox and click Proceed to e-Verify.

Note: Refer to the How to e-Verify user manual to learn more.

After successful e-Verification, a success message is displayed along with a Transaction ID. Please keep a note of the Transaction ID for future reference. You will also receive a confirmation message on your email ID registered on the e-Filing portal.

Step 7: If you wish to view the response submitted, click View Response on the Successful Submission page. You will be able to view the details of notices, response / remarks provided.

3.2. To view and submit response for Intimation u/s 245 – Adjustment against Demand:

Step 1: Click View Notice corresponding to Adjustment u/s 245 and you can:

| View and Download Notice | Follow Step 2 and Step 3 |

| Submit Response | Follow Step 4 to Step 7 |

Note: In case you have been issued Intimation u/s 245 in previous Assessment Years as well, you can search for the most recent Intimation u/s 245 issued based on Assessment Year or Demand Reference Number.

Step 2: Click Notice/Letter pdf.

Step 3: You will be able to view the notice issued to you. If you wish to download the notice, click Download.

To Submit Response

Step 4: Click Submit Response.

Step 5: Details of Outstanding Demand related to 245 demand will be displayed. You can either select Demand is correct or Disagree with Demand (Either full or Part) or Demand is not correct but agree for adjustment.

Step 5a: If you select Demand is correct, you will be required to select the checkbox and provide an answer to Have you already paid the demand amount and add the challan details, if already paid and click Save and go to Step 6.

Note: Once you agree that the demand is correct, you cannot disagree with demand later on.

Step 5b: If you select Disagree with Demand (Either full or Part), you will be required to add reason(s) for disagreement and click Save and go to Step 7.

Step 5c: If you select Demand is not correct but agree for adjustment, a message will be displayed, click Continue and add a reason for disagreement and go to Step 6.

Step 6: Enter Set Priority for the order in which the adjustment is favoured and click Submit Response.

Note: You can set priority for adjusting demand in case you have more than one outstanding demand to be paid / adjusted.

Step 7: Select the Declaration checkbox and click Proceed to e-Verify.

Note: Refer to the How to e-Verify user manual to learn more.

On successful e-Verification, a success message is displayed along with a Transaction ID and Acknowledgment Number. Please keep a note of the Transaction ID and Acknowledgment Number for future reference. You will receive a confirmation message on your email ID registered on the e-Filing portal.

3.3. To view and submit response to Prima Facie Adjustment u/s 143(1)(a)

Step 1: Click View Notice corresponding to Adjustment u/s 143(1)(a) and you can:

| View and Download Notice | Follow Step 2 and Step 3 |

| Submit Response | Follow Step 4 to Step 11 |

Step 2: Click Notice/Letter pdf.

Step 3: You will be able to view the notice issued to you. If you wish to download the notice, click Download.

To Submit Response

Step 4: Click Submit Response

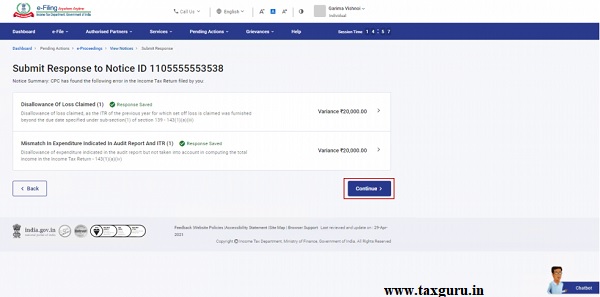

Step 5: You will be able to view the details of the Prima Facie Adjustments found by CPC in your filed ITR. Click on each variance to provide responses.

Step 6: On clicking the variance, details of the variance will be displayed. To provide response for the particular variance, click Provide Response.

Step 7: Select the relevant response from the dropdown and click Save after responding to each Prima Facie Adjustment.

Step 8: Once all the responses have been provided, click Back.

Step 9: On clicking Back, you will be taken back to the details of Prima Facie Adjustment found by CPC in your filed ITR. After responding to each variance, the responses will be saved. Click Continue.

Step 10: Select the Declaration checkbox and click Proceed to e-Verify.

Note: Refer to the How to e-Verify user manual to learn more.

On successful e-Verification, a success message is displayed along with a Transaction ID. Please keep a note of the Transaction ID for future reference. You will also receive a confirmation message on your email ID registered on the e-Filing portal.

Step 11: If you wish to view the response submitted, click View Response on the Successful Submission page. You will be able to view the details of notices, response / remarks provided.

3.4. To view and submit response to Suo-moto Rectification u/s 154

Step 1: Click View Notice corresponding to the proceedings u/s 154 and you can:

| View and Download Notice | Follow Step 2 and Step 3 |

| Submit Response | Follow Step 4 to Step 7 |

Step 2: Click Notice/Letter pdf.

Step 3: You will be able to view the notice issued to you. If you wish to download the notice, click Download.

To Submit Response

Step 4: Click Submit Response.

Step 5: Details of the mistakes proposed to be rectified will be displayed. Select the response for each mistake proposed to be rectified. You can either select Agree and proceed with rectification or Disagree and object to the rectification.

Step 5a: If you agree with the proposed rectification, select Agree and proceed with rectification and click Continue.

Step 5b: If you disagree with the proposed rectification, select Disagree and object to the rectification, select the reason from the dropdown and click Continue.

Step 6: Select the Declaration checkbox and click Proceed to e-Verify.

Note: Refer to the How to e-Verify user manual to learn more.

Note: Refer to the How to e-Verify user manual to learn more.

On successful e-Verification, a success message is displayed along with a Transaction ID. Please keep a note of the Transaction ID for future reference. You will also receive a confirmation message on your email ID registered on the e-Filing portal.

Step 7: If you wish to view the response submitted, click View Response on the Successful Submission page. You will be able to view the details of notices, response / remarks provided.

3.5. To view/submit response or seek adjournment of response due date to notice issued by Assessing Officer or any other Income Tax Authority (including respond as part of compliance related to other PAN/TAN)

Step 1: Click View Notice corresponding to the notice issued by Income Tax Official and you can:

| View and Download Notice | Follow Step 2 and Step 3 |

| Submit Response | Follow Step 4 to Step 10 |

| Respond as part of compliance – Of other PAN / TAN | Follow Step 4 to Step 10 |

Step 2: Click Notice/Letter pdf.

Step 3: You will be able to view the notice issued to you. If you wish to download the notice, click Download.

To Submit Response

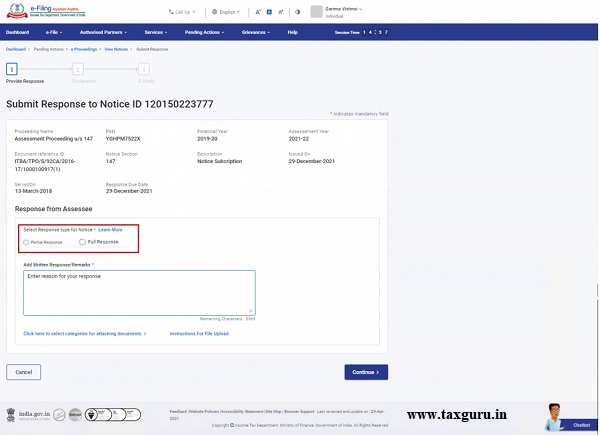

Step 4: Click Submit Response.

Step 5: Read the instructions for attaching documents and click Continue.

Note: If you are responding to a notice which requires you to submit the ITR, a message will be displayed for filing the ITR. Click Proceed and select the ITR type from the dropdown and click Continue.

Step 6: You can select Partial Response (if you wish to submit response in more than one submission, or if the number of categories exceed 10) or Full Response (if you wish to submit response in single submission, or if the number of categories is less than 10).

Step 7: Enter Add Written Response/Remarks (up to 4000 characters), select the categories for attaching the documents and click Add Document to upload the required attachment. Click Continue.

Note:

- You will be required to attach the required document for each category selected.

- The maximum size of a single attachment should be 5 MB.

- If you have multiple documents to upload, put them together in a zipped folder and upload the folder. The maximum size of all attachments in a zipped folder should be 50 MB.

Step 8: Select the Declaration checkbox and click Proceed to e-Verify.

Note: Refer to the How to e-Verify user manual to learn more.

On successful e-Verification, a success message is displayed along with a Transaction ID and Acknowledgment Number. Please keep a note of the Transaction ID and Acknowledgment Number will be displayed, and you will receive a confirmation message on the email ID registered on the e-Filing portal.

Step 9: If you wish to view the response submitted, click View Response on the Successful Submission page. You will be able to view the details of notices, response / remarks provided.

To View / Seek Adjournment

Step 1: If you wish to seek or view adjournment, click Seek/View Adjournment.

Step 2: Select Adjourned date sought up to, Reason for seeking Adjournment, enter remark/reason, attach file (if any) and click Submit.

On successful submission, a Transaction ID will be displayed. Please keep a note of the Transaction ID for future reference. You will also receive a confirmation message on the email ID registered on the e-Filing portal.

To Seek Video Conferencing

Step 1: If you want to request for video conferencing, click Seek Video Conferencing.

Note: This will be available only if Assessing Officer has flagged the notice for raising a video conferencing request.

Step 2: Select the Reason for Seeking Video Conferencing, enter Reason/Remarks, Attach File (if any) and click Submit.

On successful submission, a Transaction ID will be displayed. Please keep a note of the Transaction ID for future reference. You will receive a confirmation message on the email ID registered on the e-Filing portal.

3.6. To view and submit response to Seek for Clarification Communication

Step 1: Click View Notice corresponding to Seek for Clarification and you can:

| View and Download Notice | Follow Step 2 and Step 3 |

| Submit Response | Follow Step 4 to Step 7 |

Step 2: Click Notice/Letter pdf.

Step 3: You will be able to view the notice issued to you. If you wish to download the notice, click Download.

To Submit Response

Step 4: Click Submit Response.

Step 5: On the Submit Response page, click Provide Response.

Step 6: Select the reason from the dropdown and click Continue.

Step 7: Select the Declaration checkbox and click Proceed to e-Verify.

Note: Refer to the How to e-Verify user manual to learn more.

On successful e-Verification, a success message along with a Transaction ID will be displayed. Please keep a note of the Transaction ID for future reference. You will also receive a confirmation message on your email ID registered on the e-Filing portal.

Step 8: In case you want to view the response submitted by you, click View Response on Successful Submission page and your response will be displayed.

3.7. To Add / Withdraw Authorized Representative to respond to a notice

(You can add an Authorized Representative for responding to various kinds of e-Proceedings on your behalf, except for Intimation u/s 245)

Step 1: Log in to the e-Filing portal using your valid user ID and password.

Step 2: On your Dashboard, click Pending Actions > e-Proceedings.

Step 3: Select the notice / intimation / letter and click Add / View Authorized Representative.

| View and Download Notice | Refer to Section 3.7.1 |

| Submit Response | Refer to Section 3.7.2 |

3.7.1 To add an Authorized Representative to respond to a notice:

Step 1: If there are no Authorized Representatives added previously, click Add Authorized Representative.

Note: In case you already have an Authorized Representative added of your choice, select Make Active and click Confirm.

Step 3: A 6-digit OTP is sent on your primary mobile number and email ID registered on the e-Filing portal. Enter the 6-digit mobile or email OTP and click Submit.

Note:

- OTPs will be valid for 15 minutes only.

- You have 3 attempts to enter the correct OTP.

- The OTP expiry countdowntimer on screen tells you when the OTP will expire.

- On clicking Resend OTP, a new OTP will be generated and sent.

After successful validation, a success message is displayed along with a Transaction ID. Please keep a note of the Transaction ID for future reference. You will also receive a confirmation message on your email ID and mobile number registered on the e-Filing portal.

3.7.2. To withdraw Authorized Representative

Step 1: Click Withdraw against the details of the respective authorized representative and the status will change to Cancelled.

Note: You will only be able to withdraw an active Authorized Representative. In case the status is changed to Request Accepted, you will be required to provide the reason and the Authorized Representative will be removed.

e-proceedings portal is not working since its inception.I am unable to file the e-proceedings reply in connection with penalty notice issued. Whether the date will be extended by the department or not

The e proceedings tab is not working as of now, what options we have?