Preamble

Corporate India today serves global needs and brings in overseas income which is chargeable to Indian tax net as a resident of India. Flip side of this paves way for claim for taxes paid at foreign jurisdiction based on the source of income. Without clear guidelines on the credit mechanism, there were uncertainty on determination of quantum of credit eligibility, which had led to lots of litigation. The attempt which CBDT has made to settle the dust by notifying rules for foreign tax credit was come into force from 1.4.2017.

This article attempts to brief the concept of Foreign Tax Credit (FTC), various methods of relief practiced across the globe and touches upon few important judgments on FTC while pointing out the essence of the notified FTC rules.

Page Contents

A. Concept of Double Taxation

When the same income is taxed more than once, it suffers double taxation. This may be due to jurisdictional reasons or economic reasons

(1) Jurisdictional Double Taxation:

If a person is taxed in more than one Jurisdiction for the same income which he had earned it leads to double taxation. This can arise on the following circumstances:-

a) Worldwide income which becomes taxable in more than one State (Country)

b) The same income is taxed under residence rule in one state and taxed under source rule in another state

c) Triangular Taxation eg. PE taxed in one state which receives income from various other states and it is consolidated at company level in a state.

(2) Economic Double Taxation:

This arises where the same income is taxed in the hands of more than one person under different capacity. A classic example is dividend which is declared out of taxed profits in one state is once again taxed in the hands of shareholders in other state when they receive it. Similarly income taxed on a partnership firm in one state may be taxed again in the hands of partners in other.

Elimination of Double Taxation

Double taxation hampers free trade and commerce across the globe as the income earned overseas has to suffer tax in more than one state. This in turn makes the cross border investors to relook their investment decision. Hence, to encourage overseas income that helps to build foreign exchange reserve of the country, nations have taken various steps to eliminate double taxation. (Ref. Fig A.1 below)

B. FTC and its History:

The concept of giving credit for the taxes paid in foreign country against the income earned in that country first seems to have emanated in USA during 1918 after World war-I. After technical amendments, the Act was passed in 1958 where tax payers were allowed to carry their unused foreign taxes forward five years or back by two years. Latter on countries have started signing in DTAA’s with other countries to address this double taxation issue specifically to ease out the tax burden of their residents. Thus, relief for taxes paid in foreign country is given to tax payer while taxing the same income in the home country and this is termed as Foreign Tax Credit (FTC). The relief is given under various methods (Ref. Fig. A.2 below).

1) Exemption Method:

Under Exemption method the income that is taxed in source country (foreign country) is exempted in Resident country either fully or progressively. The provisions to this effect is

T Outlow(b) r Out2l inco(b) in(b) 7l incosidl incon

stated in the DTAA entered between the two countries.

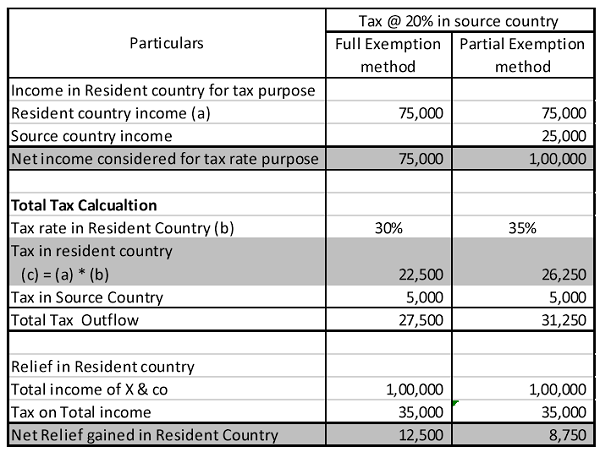

a. Full Exemption : Under this method income taxed in the source country exempt from taxation in the Resident Country. Here the income is not at all considered for the purpose of tax calculation by the Resident Country while calculating the tax on the rest of the income.

b. Progressive Exemption: Though the income from the source country is exempted from tax in the country of residence the same is however considered for tax purpose for arriving the tax rates.

Difference between the two methods can be best understood with an example. Let us take X & co who is a Resident of country R have source of income of Rs. 75,000 in country R and Rs. 25,000 from Country S. Where the income is taxed in the source country @ 20% and in the Resident country at progressive method where for a total income up to Rs. 75,000 the tax rate is 30% otherwise it is 35% flat.

Table 1.1

Note: Difficulty in this method is that when the tax rate in the source country is higher than the tax slab in the resident country, the tax payer does not get any tax break for the excess tax paid in the source country. This is essentially because, both the income as well as the tax payment in the source country is not considered for the purpose of relief in the resident country.

2) Credit Method:

Under this method the income which is taxed in the source country is also considered in the total income of the country of residence to arrive the tax base, but, deduction is allowed from its taxes paid in the source country. This may be again under different methods

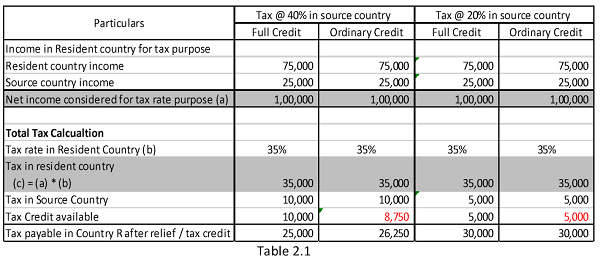

a. Full Credit Method: The Resident country grants credit for the taxes paid in the Source country without any restriction or limits.

b. Ordinary Credit Method: This is generally adopted in many DTAA where allowance of credit is given against tax payable in the resident country. The credit may be given only if the income is subjected to tax in the overseas jurisdiction. If the tax paid in overseas jurisdiction is in excess to the tax chargeable in the resident country it is ignored and no credit is given for the same. Further it may be restricted against the tax paid in the overseas jurisdiction against each head of income as well.

Let us take the same illustration with the variable that in scenario 1 the tax rate is @ 40% in the source country and in scenario 2 the rate is 20% and work out the relief under full credit and ordinary credit methods

Note: It can be seen in the above illustration that there is no difference between the methods if the rate of tax in source country is lesser than the resident country. When the tax rate in the source country is higher than the resident country the credit is restricted to that of the resident countries tax on that income.

3. Underlying Credit Method:

Underlying tax credit method attempts to mitigate the economic double taxation. Economic double taxation occurs where the same income is taxed more than once in the hands of different person in the same tax jurisdiction. Eg. The profits earned by the corporates are taxed at their hand and the same is again taxed when it is distributed to shareholders as dividend. Under underlying credit method, credit is allowed to resident not only for the taxes withheld against the dividend income but also for the taxes paid on the underlying profits out of which the said dividend is paid by a company in the overseas jurisdiction. For this there are specific provisions brought in certain DTAA E.g Article 24 of India – UK DTAA, Article 23 of India – Mauritius DTAA and Article 25 of India – Singapore DTAA. However, underlying credit may only apply if satisfaction of substantial shareholding requirement is met.

d. Tax sparing credit Method: This is by arrived by way of granting a tax credit in the resident country for the amount of tax that would have been payable in the overseas jurisdiction. This comes to play when the tax incentives offered by a particular overseas jurisdiction are deemed to have been paid as a foreign tax for the purpose of computing and granting foreign tax credit in the resident country. Thus it denotes the tax spared by the foreign jurisdiction based on the tax incentive programs for the taxes on the income earned in its jurisdiction, which is normally carried out to encourage bringing foreign investments into the country. Tax Sparing will be more relevant to income such as interest, royalties, foreign branch / permanent establishment income etc. The concept of tax sparing may lead to double non-taxation. Article 23 of UN Model Convention supports tax sparing by the developed countries. Many Indian tax treaty contains tax sparing clauses which are now being renegotiated to eliminate treaty abuse by structuring transactions.

C. Foreign Tax credit – Indian perspective

India has recognized the concept of Foreign Tax Credit in the Act, it is specifically addressed by Sec.90 and Sec.91 of the Income Tax Act, 1961. Sec. 90 governs the tax credit for countries where India has entered into a DTAA and Sec. 91 addresses credit for those cases where no DTAA is in force with that overseas jurisdiction. Though these provisions were prevailing in the Act for a long time, no specific guidelines or rules governing the computation mechanism for determining the eligibility of foreign tax credit were in place all these days. This in turn had led to uncertainty on foreign tax credit position and litigations. Rule 218 has been introduced in 2016 aiming to put rest of uncertainties.

Before going into FTC Rules it would be interesting to see few judicial precedents which had triggered the declaration of the rules

Case 1 : WIPRO Limited F TS – 565 – HC – 2015 (KAR) ]

The judgment of WIPRO provides that merely because the taxpayer’s income is exempt from tax due to a limited tax holiday provided under the ITA, does not mean that foreign tax credit can be simply denied.

Facts of the case:

Wipro Limited (“Wipro”), is an Indian company engaged in the business of exporting computer software and services. It is also eligible to tax holidays for its STP (software technology parks) undertakings under Section 10A of the ITA. Wipro’s on-site development of software is carried out through its permanent establishments (“PEs”) in countries such as the USA, UK, Canada, Japan and Germany. Therefore, Wipro paid income tax in overseas jurisdiction on the profits attributable to those PEs. Wipro receives consideration from some foreign clients after withholding of tax for which it had claimed credit in India where its global income is taxed.

The tax officer refused Wipro’s claim for foreign tax credits for taxes paid in the foreign countries on the ground that credit could only be claimed for taxes actually paid in both countries. Although the Commissioner of Income-tax (Appeals) held in favour of Wipro, the Income Tax Appellate Tribunal ruled that no foreign tax credit can be claimed in respect of income that is exempt from tax in India. Wipro approached the High Court against the order of the Tribunal

Question before the HC is whether credit for taxes paid in a country outside India in relation to income eligible for deduction in India under Section 10A from total income would be available under Section 90 of the Income tax Act, 1961 read with relevant DTAA

Highlights of the Judgment

- Income under Section 10A is chargeable to tax under Section 4 and is includible in total income under Section 5, but no tax is payable due to the exemption provided. Hence it cannot be said that the tax payer is exempted from tax but the income earned from that particular STP undertaking is exempted for certain specified period. But for this exemption the income is chargeable tax and therefore includable under total income under Sec. 5.

- As per the Amendment in 2004, tax relief was extended even to income tax chargeable under the ITA irrespective of payment of such taxes (s.90(1)(a)(ii)). This provision was introduced as a policy measure by the Government to promote mutual economic relations, trade and investment. Further, section 90(2) states that to the extent that provisions of the Treaty are more beneficial to the taxpayer, they shall apply.

- The court highlighted the distinction between the India US treaty and India Canada treaty. While provisions of Article 23 of the India-Canada Treaty, provides credit for the tax paid in Canada against the Indian tax paid in respect of such income only if income has been subjected to tax both in India and Canada, Article 25 of US Treaty is in conformity with Section 90(a)(ii) of the ITA as the provision does not speak of taxes being paid by the Indian resident under the ITA as a condition precedent to claiming tax credit. Therefore, under Article 25, Wipro is entitled to such tax credit in respect of that income, which is taxed in the USA.

- Credit on state level taxes: In so far as non-federal taxes are concerned, the High Court has interpreted the provisions of section 91 to mean that if the taxpayer has paid income tax in a foreign country at state level, the income tax paid at state level, is also eligible for credit being given to the taxpayer in India. This is because Section 91 covers tax credits in cases where no agreement has been entered by India

Case 2: Infosys Technologies V. JCIT [2007] 108 TTJ 282 (BANG)

Facts of the case:

Infosys received certain income by way of royalty with respect to its software from Canada. The receipt by way of royalty was subjected to tax in Canada and tax was deducted at source by the payee. The same income received also formed part of total turnover. Thus, the income arising from such royalty receipt is also chargeable to tax in India. Since the income was already taxed in Canada, it claimed relief of Rs. 46,02,248/- in respect of tax doubly charged such income as per art. 23 of the DTAA between India and Canada. Infosys contended that the entire royalty income taxed in Canada is to be treated as taxed in India as well as it forms part of the total income in India. Accordingly, whatever tax is paid in Canada is to be given as rebate while computing tax payable by it in India.

The above claim by Infosys was not agreed by the AO. Since Infosys is also eligible for deduction u/s 80HHC, AO held that the entire receipts by way of royalty from Canada have not been subjected to tax in India and accordingly, only proportionate income can be considered to be doubly taxed and only such tax which has been levied in India is eligible for relief under DTAA and therefore given relief of only Rs.28,58,624/-. However, on appeal Learned CIT(A) went a step further and compared the royalty income with the total turnover and income including those turnover and income in respect of which exemption u/s. 10A of the Act was claimed and restricted the relief to Rs.13,98,768/-.

Decision of ITAT

On appeal by Infosys against the order of CIT(A) before ITAT, ITAT had gone into the DTAA with Canada and held that methodology prescribed under the treaty is “ordinary credit” mechanism. The commentary to the model conventions (both the OECD and the UN model conventions) acknowledges that there may be a lot of difficulties in the application of the article on “relief double taxation”. It therefore recommends that the domestic legislation should provide for solutions for all the difficult areas/issues. There are no rules in the domestic statute in India dealing with the manner of granting relief from double taxation. Relief from double taxation is thus to be calculated on the basis of the provisions of the treaty read with the domestic legislations in India.

As per s. 90[2] where the treaty exists for granting relief of tax in relation to the assessee to whom such agreement applies, the provisions of the Act shall apply to the extent they are more beneficial to the assessee. Thus, though the chargeable provision of the IT Act is applicable to the assessee for its global income, yet as per s. 90, if the income is taxed both in India and Canada, the assessee is entitled to relief as per art. 23 of the DTAA with Canada and proportionate tax credit is available.

The fact remains that the royalty income in Canada is billed from the STP unit the assesse had not claimed any benefit u/s 10A but it form part of total turnover of units eligible for deduction under s. 80HHE. It is also an admitted fact that the total turnover or gross receipts of eligible units cannot be considered as income, which has been subjected to tax in India. The expenses for earning such income have been allowed as deduction. On the balance profit, deduction has been allowed under s. 80HHE. Thus, the receipt taxed in Canada is not equal to the income taxed in India. It is settled law that relief under DTAA is available only when same income has suffered tax in both the countries. Accordingly the method adopted by AO was upheld with the modification adopted in the figures to arrive the receipts suffered tax in India so as to claim credit for such doubly taxed income.

Other interesting decisions on FTC in Indian context:

- CIT O.VR.SV.VR. Arunachalam Chettiar [1963] 49 ITR 574 (Mad)

“the expression such doubly taxed income in s. 49D indicates that it is only that portion of the income on which tax has in fact been imposed and been paid by the assessee that is eligible for the double tax relief”

- TATA Sons [2011] 43 SOT 27 (Mum AT)

Though DTAA with USA provides credit only the tax paid with the Federal Government, credit was extended to the Taxes paid to State taxes as well. It has considered the relief u/s 91 which was beneficial to the assesse than that of the DTAA.

- Vijay Electricals [2015] 54 com 19 (Hyd AT)

Tax credit is available even if the same is not deposited with the overseas Government in the year in which the income is taxable.

D. Introduction of FTC Rules in India – A step forward on clarity but still a long way to go

I. Brief analysis of Rule 128 introduced under Indian Income Tax Rules

In line with various decisions of the court and to put rest to the ambiguity on the subject, CBDT had notified Rule 128 in June 2016 to prescribe the method of allowing the foreign tax credit and this rules was effective from 1.4.2017. Salient features of the rule are given below:-

1. Applicability of the rules

- Comes into force with effect from 1.4.2017

- Available only for residents for the amount of foreign taxes paid by him in a foreign country

- Credit is available only if income corresponding to the taxes is offered for tax or assessed to tax in India during the year in which the credit is claimed.

- In the cases where the income for which the foreign taxes paid or deducted is offered to taxes for more than one year, the credit will be given across the years in the same proportion to which the income is offered to tax in India.

2. Foreign Tax Credit Defined under sub-rule 2:

In case of DTAA countries “taxes that are covered under the said agreement”.

Other countries “the tax payable under the law in force in that country in the nature of income-tax referred in clause (iv) of the Explanation to Sec. 91”.

3. Utilization of FTC:

- FTC is eligible for adjustment against the tax, surcharge and cess payable under the IT Act

- FTC cannot be adjusted against interest, fee or penalty payable under the IT Act

- FTC is not available in case foreign tax or part thereof is disputed by the assesse in any manner.

Exception & Conditions:

Credit is allowed in the year in which the income is offered/assessed in India upon the assesse within six months from the end of the month in which dispute is finally settled furnishes

a) Evidence of settlement of dispute

b) Evidence that the liability for payment of such foreign tax has been discharged and

c) Undertaking that no refund in respect of such amount is directly or indirectly been claimed

4. Determination of FTC quantum :

a) FTC under Normal provisions:

- Calculate credit for each source of income separately for a specific country and aggregate

- The rate of exchange to be taken for this purpose is TT buying rate on the last day of the month immediately preceding month in which the tax is paid or deducted.

- The tax payable under the act on such income or the foreign tax paid whichever is lower is eligible as FTC. However, while considering the foreign tax paid, it cannot exceed the amount arrived as per DTAA with that country.

- Aggregate credit eligible for each country arrived above to calculate total FTC eligibility.

b) FTC under MAT:

- FTC is to be calculated similar to that of normal provisions

- FTC adjusted against MAT cannot exceed tax credit available under normal provisions

5. Documents requirement for claiming FTC:

- Furnish Form 67 dully verified and certified by a Charted Accountant on or before furnishing return of income u/s 139(1)

- Produce Certificate or statement specifying (a) Nature of income and (b) amount of TDS given by

i) Tax authority of that country, or

ii) Person responsible for deduction of such tax, or

iii) Signed by the assesse: In this case, it should be accompanied with –

(a) An acknowledgment of online payment or challan or bank counterfoil for proof of payment of tax, if tax is paid by the assesse

(b) In case of deduction, proof of TDS

Note: Form 67 is also required to be submitted when the carry backward of loss of the current year results in refund of foreign tax for which FTC has been already claimed in earlier year(s).

II. Issues needed to be addressed

Though FTC rules had plugged most of the uncertainties which were looming over the past, it has failed to address few issues in totality, such as:-

- Proviso to Rule 4 gives the option for the assesse to claim FTC within six month of settlement of dispute, it does not clearly addresses those cases where assessment is already completed before settlement of dispute is reached in the overseas jurisdiction. Explicit provision similar to that of 154/155 for giving effect to the orders of the previous years, is required to be inserted to ensure that FTC is not lost in those cases where the dispute in foreign jurisdiction is settled later than the orders passed by AO.

- Rule 5 contemplates to calculate FTC for each source of income separately form a particular country and then aggregate the same. There might be situation where a particular income in the overseas jurisdiction may be classified under a different head than that of Indian IT Act. Further, there will be inconsistency between method of taxing adopted in the overseas territory from that of India for different head of income may which may also pose challenges in arriving the quantum of FTC.

- When the return is loss under the normal as well as the MAT provisions, it seems that no credit will be eligible under FTC, therefore there is no question of filing Form 67 as well as for claiming FTC at the time of filing returns. However, at the time of assessment / reassessment, additions were made to turn losses into a taxable income, no provision is available for the assesse to claim FTC by submitting the relevant documents or AO to allow FTC at that point of time afresh.

- Method to distribute FTC to partners if they are taxed at the Firm level in overseas jurisdiction. Rule 1 addresses proportionate distribution of FTC over the years in which the income is offered but the distribution of FTC among different persons is not stated.

Conclusion:

FTC in Indian context is becoming more critical and important determinant factor to arrive group tax rate in cross border business horizons. Especially with Indian corporates going global by expanding its business presence across borders, the rules notified is a positive step and gives certain clarity on the foreign tax credit eligibility. While it is a light of hope to the corporate to firmly estimate its global tax liability with some certainty, let’s hope that issues untouched and those crop up out of the new rules will be addressed in the due course by necessary amendment to ensure a better visibility of tax liability on global operations.

(The discussions made and opinions expressed in this article are purely of that of the author and the readers are requested to make their own assessment and consult the experts before deciding on any of the subject matter. The writer cannot be held responsible in any manner for the decisions taken based on this article)

(k. Srinivasan is Taxation professional and can be reached @ sreeka.srini@gmail.com)

Disclaimer: The contents of this article are for information purposes only and does not constitute advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer to relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

(Republished with Amendments by Team Taxguru)

Excellently and comprehensively presented. I congratulate and thank the author for a good job done