Practical FAQs on applicability of TDS under section 194Q & TCS under section 206C(1H) w.e.f. 1st July 2021

Sub-section (1H) was inserted in Section 206C by Finance Act, 2020 for collection of tax at source (TCS) by the seller on sale of any goods and was made operative with effect from 1st October 2020. On similar lines, Finance Act, 2021 has inserted section 194Q to provide for deduction of tax at source (TDS) by buyer on purchase of goods with effect from 1st July 2021.

Both the provisions target same transaction of purchase/sale of goods and may seem to be running parallel to each other because of which significant ambiguities have arisen in the minds of the taxpayers. We have critically analyzed both the provisions in depth and have prepared detailed FAQs covering possible practical scenarios and seek to address all the ambiguities that have creeped in the minds of the taxpayers.

Provisions of Section 194Q and 206C(1H) in brief:

| Particulars | TDS u/s 194Q | TCS u/s 206C(1H) |

| Responsible Person | ‘Buyer’ of Goods | ‘Seller’ of Goods |

| Meaning | ‘Buyer’ is a person whose total sales, gross receipts or turnover > ₹ 10 crore in the immediately preceding FY | ‘Seller’ is a person whose total sales, gross receipts or turnover > ₹ 10 crore in the immediately preceding FY |

| Rate | 0.1% of Value of Goods purchased | 0.1% of Value of Goods sold |

| Threshold Limit | Total Purchase Value > ₹ 50 Lakh | Total Sale Value > ₹ 50 Lakh |

| Timing of Deduction/ Collection | At the time of payment or credit, whichever is earlier | At the time of receipt |

| Exceptions |

|

|

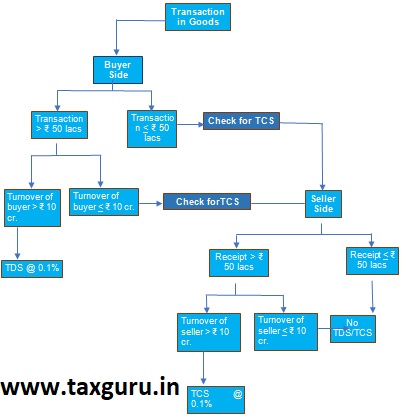

A transaction flow chart reflecting the applicability of Section 194Q or Section 206C(IH) is given at Appendix-1. Further TDS/ TCS applicability on various scenarios are given in Appendix-2 and draft templates of communication to be sent to buyer/ seller for TDS/ TCS applicability are given at Appendix-3 & 4.

Practical Frequently Asked Questions [FAQs] on applicability of Section 194Q or 206C(1H):

1. What is the meaning of the term ‘Turnover’?

The term turnover has not been specifically defined under any of the sections. In the “Guidance Note on Terms used in Financial Statements” published by ICAI, “the expression “Sales Turnover” has been defined as: “The aggregate amount for which sales are affected or services rendered by an enterprise”.In the statement issued by ICAI on the CARO the word ‘turnover’ has been defined as under- “The term ‘turnover’ for the purposes of this clause may be interpreted to mean the aggregate amount for which sales are effected or services rendered by an enterprises.”

2. Whether TDS and TCS provisions shall be applicable simultaneously or any one of the provisions shall be applicable? If so, how to determine whether TDS provision or TCS provision should be applicable?

TDS and TCS provisions are mutually exclusive provisions i.e.only one of the provision shall be applicable on a single transaction of sale/ purchase of goods.

Applicability needs to be first checked of TDS u/s 194Q in the hands of buyer (since the provision specifically states that such TDS U/s 194Q shall not be deducted where TCS is deductible under any other provisions of the act other than section 206C(1H)). At the same time, section 206C(1H) states that such TCS shall not be collectible where TDS is deductible under any other provision of the Act and such TDS has been deducted.

Therefore, it is evident that priority shall be given to TDS U/s 194Q and in case, TDS is not deductible or deducted u/s 194Q, then TDS u/s 206C(1H) shall be checked for applicability.

Please refer to the flow chart and various scenarios given in Appendix-1 and Appendix-2, respectively for obtaining a clear understanding of the manner of application of either section 194Q or section 206C(1H).

3. Whether TDS to be deducted on the amount inclusive of GST component?

- As far as TDS U/s 194Q is concerned, CBDT vide Circular No. 13/2021, dated 30thJune 2021, has clarified that when tax is deducted at the time of credit of amount in the account of seller and in terms of the agreement or contract between the buyer & seller, the GST comprised in the amount payable to the seller is indicated separately, TDS u/s 194Q shall be deducted on the amount credited without including GST.

- However, if TDS is deducted on payment basis because the payment is earlier than the credit, the tax would be deducted on the whole amount as it is not possible to identify that payment with GST component of the amount to be invoiced in future.

4. Whether TCS to be collected on the amount inclusive of GST component?

CBDT has clarified on 29th September 2020 vide Circular No.17/2020 that TCS need to be discharged on sales consideration received and no adjustment on account of GST is to be done. Thus, TCS should be collected on gross sales consideration inclusive of GST.

5. Whether GST to be charged by the seller on the amount of sale including TCS?

CBIC vide Corrigendum to Circular No. 76/50/2018-GST issued on 7th March 2019 has clarified on the issue of valuation of supply U/s 15 of CGST Act, 2017 in case of TCS under Income Tax Act.

In this matter, it states that Section 15(2) of the CGST Act specifies that the value of supply shall include ‘any taxes, duties, cesses, fees and charges levied under any law for the time being in force other that GST Laws. For the purpose of determination of value of supply under GST, TCS under the provisions of Income Tax Act, 1961 would not be includible as it is an interim levy not having the character of tax.

6. Whether TDS or TCS to be deducted or collected, respectively on total sales value to the seller or buyer to whom sales in excess of ₹ 50 Lakhs has been made or only to the amount in excess of ₹ 50 Lakhs?

Section 194Q as well as section 206C(1H) envisages that TDS/ TCS at the rate of 0.10% of the purchase value/ sale consideration paid/ received in excess of ₹ 50 Lakhs shall be deducted/ collected by the buyer/ seller. As such, TDS/ TCS shall not be deducted/ collected on the threshold limit of ₹ 50 Lakhs available for each financial year.

7. What is the meaning of the buyer?

As per section 194Q, ‘Buyer means a personwhosetotal sales, gross receipts or turnover from the business carried on by him exceed ₹ 10 crore during the financial year immediately preceding the financial year in which the purchase of goods is carried out.

Further, section 206C(1H) defines buyer as any person who purchases any Goods but does not include:

- the Central Government, a State Government, an embassy, a High Commission, legation, commission, consulate and the trade representation of a foreign State;

- a local authority;

- a person importing goods into India.

8. What is the meaning of the seller?

As per section 194Q, ‘Seller’ means a person who is a ‘Resident’ of India and selling any goods.

Whereas section 206C(1H) defines seller as a person whose total sales, gross receipts or turnover from the business carried on by him exceed ₹ 10 crore during the financial year immediately preceding the financial year in which the sale of goods is carried out.

9. Whether TDS/ TCS shall be deducted/ collected on any kind of sales including sale of services?

No, as per section 194Q and 206C(1H), TDS/TCS shall be deducted/ collected on sale of goods only.

10. Whether the consideration amount will be at FOB/CIF?

It would depend upon the terms of the contract. If the contract is on CIF basis, the sales consideration will include insurance and freight and thus TDS/ TCS would need to discharged on that invoice value/ consideration itself.

11. Whether such provisions shall be applicable on export/ import of goods?

- Provisions of TDS u/s 194Q specifically states that TDS shall not be deducted on payments being made to non-residents. This means that no TDS shall be deducted on goods imported into India under this section. Such a transaction may be taxable u/s 195 which would depend upon the nature of transaction. Since the TDS is applicable only buyer of goods, the export transaction in any case would be out of its purview.

- TCS u/s 206C(1H) shall not be collected on export made outside India. Further, the importer of goods has also been excluded out of the definition of buyer. That means the provisions of section 206C(1H) shall not be applicable on import or export of goods.

12. Whether the provisions of Section 194Q shall be applicable on non-resident buyer of goods?

The CBDT has clarified vide Circular 13/2021 dated 30-06-2021 that section 194Q shall not apply to a non-resident whose purchase of goods from seller resident in India is not effectively connected with the Permanent Establishment of such non-resident in India.

13. For calculating the limit of ₹ 10 crore in the preceding financial year, whether sale of services to be included?

For calculating the threshold limit of ₹ 10 crore in the preceding financial year, section 206C(1H) as well as section 194Q provides that Total Sales, Turnover, Gross Receipts from the business shall be considered. As such, the receipts of sale of services shall also be considered.

14. Whether TCS is applicable for the amount collected against invoices raised before 1st July 2021, if all the conditions of section 206C (1H) are satisfied?

Since TDS is applicable only after 1stJuly 2021, TCS would be applicable for the amounts collected before 1st July 2021 is conditions given under 206C (1H) are satisfied. However, post 1st July 2021, first applicability of TDS u/s 194Q in the hands of buyer needs to be checked and if TDS provisions are not applicable.

15. In the case of non-availability of PAN or Aadhaar of the buyer, what shall be rate at which TDS or TCS shall be applicable?

- TDS shall be deducted at the rate prescribed by section 206AA (5%) in case PAN is not provided by the seller.

- Further, section 206C(1H) specifically provides that TCS shall be collected at the rate of 1% of sale consideration in case buyer of the goods fails to provide its PAN or Aadhar. Provisions of section 206CC have been specifically overruled by section 206C(1H).

16. Whether TCS shall be collected at the time of debiting the buyer with the sale value or at the time of collection?

Section 206C(1H) specifically provides that the seller shall collect from the buyer a sum equals to 0.1% of the sales consideration at the time of receipt of such amount. That means the liability to collect TCS will arise even in case of advance payment received though the goods will be physically delivered later.

Further, CBDT by way of press release dated 30th September 2020 has also clarified that in order to simplify and ease the compliance of the collector, it may be noted that this TCS provisions shall be applicable on the amount of all sale consideration received on or after 1st October 2020, without making any adjustment for the amount received in respect of sales made before 1st October 2020.

17. Whether TDS shall be collected at the time of crediting the seller with the purchase value or at the time of deduction?

Section 194Q provides that the buyer shall deduct from the payments made to seller a sum equal to 0.1% at the time of payment or credit of such amount to the account of the seller. That means the liability to deduct TDS will arise even in case of advance paymentsto the seller.

18. Since, TCS to be collected on advance payments, what shall be the course of action in case, the advance has to be refunded as the sale is not affected?

Where the seller receives an advance for selling the goods and he deposits the TCS thereon, however later on such transaction stands cancelled, in such a case, post month-end, no refund of the TCS can be made to a buyer. Even if it is collected on higher amount, the same will be deposited with the government. The buyer can claim credit for the TCS amount while depositing Advance Tax and/or determining the final tax liability.

CBDT has also clarified in its circular that no adjustment on account of sales return or discount or indirect taxes including GST is required to be made for collection of tax under sub-section (1H) of section 206C of the Act since the collection is made with reference to receipt of amount of sale consideration.

19. How and when to charge TCS from buyer?

- Alternative 1- The TCS can be collected by charging through invoice:

In this case, both buyer and seller need to do accounting as receivable and payable for these amounts. It may be noted that if the payment is being made in next financial year, TCS obligation may not be applicable on seller (due to turnover threshold) or may not be applicable on buyer due to not making payments breaching ‘collection’ threshold in that financial year. In those case, one need to keep track and write off and reconcile it with the liability.

- Alternative 2: The TCS can be collected by charging through debit note:

The logic for issuance of debit note may be that debit note to be issued at the time of payment so that it can be charged only on the eligible cases and no hassles of write off etc. (as mentioned in above points). But in that case, a specific series of debit note number may need to be used to make sure that these debit notes do not create issues in GST compliance.

20. Whether this TCS u/s 206C(1H) shall also apply on sale of motor vehicle?

The provisions of sub-section (1F) of section 206C of the Act apply to sale of motor vehicle of the value exceeding ₹ 10 Lakh. Further, Sub-section (1H) of section 206C of the Act exclude from its applicability goods covered under sub-section (1F). It may be noted the scope of sub-sections (1H) and (1F) are different. While sub-section (1F) is based on single sale of motor vehicle, sub-section (1H) is for receipt above ₹ 50 Lakh during a financial year against aggregate sale of good. While sub-section (1F) is for sale to consumer only and not to dealers, sub-section (1H) is for all sale above the threshold.

In this regard it CBDT has clarified that –

- Receipt of sale consideration of motor vehicle from a dealer would be subjected to TCS under sub-section (1H) of the Act, if such sales are not subjected to TCS under sub-section (1F) of section 206C of the Act.

- In case of sale to consumer, receipt of sale consideration for sale of motor vehicle of the value of ₹ 10 Lakh or less to a buyer would be subjected to TCS under sub-section (1H) of section 206C of the Act, if the receipt of sale consideration for such vehicles during the financial year exceeds ₹ 50 Lakh during the financial year.

- In case of sale to consumer, receipt of sale consideration for sale of motor vehicle of the value exceeding ₹ 10 Lakh would not be subjected to TCS under sub-section (1H) of section 206C of the Act if such sales are subjected to TCS under sub-section (1F) of section 206C of the Act.

21. Whether section 194Q & 206C(1H) are applicable on purchase of capital goods?

Yes, section 194Q & 206C(1H) applies to purchase or sale of all goods whether on capital or on revenue account.

22. Whether a transaction in securities through stock exchanges shall be subject to TDS under section 194Q?

Section 206C(1H) provides for the collection of tax (TCS) on the sale of goods. CBDT has, vide Circular No. 17 of 2020, clarified that provisions of Section 206C(1H) shall not be applicable in relation to transactions in securities (and commodities) which are tradedthrough recognized stock exchanges or cleared and settled by the recognized clearing corporation, including recognized stock exchanges or recognized clearing corporations located in International Financial Service Centre (IFSC).

One needs to wait and see if CBDT issues such clarification in the context of section 194Q also exempting such transactions in view of the fact that there no one-to-one contract between the buyers and sellers and this makes TDS provisions unworkable in such situation.

23. Whether TDS is required to be deducted on the transaction in electricity?

Section194Q provides for the deduction of tax on the payment made for the purchase of goods. The Apex Court in the case of State of Andhra Pradesh v. National Thermal Power Corporation (NTPC) (2002) 5 SCC 203, held that electricity is a movable property though it is not tangible. It is ‘goods’. Thus, it may be concluded that the tax should be deducted from the payment made in respect of the transaction in electricity.

A transaction in electricity can be undertaken either by way of direct purchase from the company engaged in generation of electricity or through power exchanges. The CBDT has clarified vide Circular No. 17 of 2020 that the transaction in electricity, renewable energy certificates and energy-saving certificates traded through power exchanges registered underRegulation 21 of the CERC shall be out of the scope of TCS under the provision of Section 206C(1H).

In respect of direct purchase from generating company, TDS will be deductible u/s 194Q. In respect of purchase through power exchanges, it remains to be seen whether similar exemption as granted from section 194-O and section 206C(1H) will be granted from section 194Q also.

24. Whether TDS should be deducted on the purchase of software?

It has been held by various judicial authorities that packaged/ canned software (off the shelf computer software) are ‘goods’. Therefore, purchase of Canned software (off the shelf computer software) is purchase of ‘goods’ and will be liable to TDS under section 194Q even if buyer-entity capitalizes the same in its books. Purchase of customized or tailor-made software may be “services” and liable to TDS under section 194J or section 194-O.

25. Whether TDS is liable to be deducted on purchase of Jewellery not connected with business?

Tax is required to be deducted by a buyer carrying on business whose total sales, gross receipts or turnover from the business exceeds Rs. 10 crores during the financial year immediately preceding the financial year in which such goods are purchased. There is no condition that the purchases should be connected with the business only. Thus, if a person is falling within the definition of the buyer, tax is required to be deducted even if such purchase is not connected with the business carried on by him. Jewellery, being a movable property, is covered within the term goods. There is no specific exclusion under Section194Q for deduction of TDS on purchase of jewellery. Thus, the tax shall be deductible on purchase of jewellery if other conditions are also fulfilled.

26. Whether additional, allied and out-of-pocket expenses form part of the purchase value of goods?

Where these expenses have been reflected in the purchase invoice itself, it should form part of purchase value and TDS will be deductible on the same. If they are charged through a separate invoice and on actuals basis and claimed as reimbursement being incurred on behalf of buyer, it should not form part of purchase value for deduction of TDS and for computing the Rs. 50,00,000 threshold limit.

27. Whether the amount advanced as a loan to the seller shall come within the ambit of this provision?

Loan advanced by buyers is not a payment towards the purchase of goods. Hence, there is no requirement to deduct TDS on loan advanced by the buyer. However, if at any future date, such loan amount is settled against purchased value, the liability to deduct TDS shall arise. The tax shall be deducted on the date on which parties agreed to adjust the loan amount against the outstanding liability.

28. Whether tax to be deducted on the purchase of goods by one branch from another?

The TDS under this section is required to be deducted by any person, being a buyer, responsible for making payment to the seller for the purchase of goods. Thus, the existence of two distinct parties as ‘seller’ and ‘buyer’ is a pre-requisite to construe a transaction as a purchase. The condition of purchase is not fulfilled in the context ofbranch transfer. Therefore, the provisions of this section shall not apply in the case of branch transfers.

29. What shall be the treatment of debit note for computation of TDS?

With respect to purchase return, CBDT has clarified vide Circular 13/2021 dated 30-06-2021 that as tax must have been deducted before purchase return happens. In such a case, if money is being refunded by seller then this TDS may be adjusted against the next purchase from the same seller.

Further, no adjustment is required if purchase return is replaced by the goods by the seller.

30. If the seller has multiple units, whether purchases made from different units need to be aggregated?

Where tax is required to be deducted at source, the deductee is required to furnish his PAN or Aadhaar number to the deductor failing which the tax is required to be deducted at higher rates. If the PAN or Aadhaar number is available, the threshold limit of Rs. 50 lakhs shall be computed in respect of each PAN or Aadhaar number. In other words, if different units of the seller are under the same PAN or Aadhaar number, the amount paid or payable to all such units shall be aggregated to compute the limit of Rs. 50 Lakhs.

31. Can a seller apply for the certificate for lower deduction of TDS?

Finance Act, 2021 has not made any consequential amendments to section 197/section 197A to extend the benefit to apply for a certificate for deduction of tax at lower rates or to file declaration for NIL deduction in respect of transactions covered under Section194Q. Hence, the seller does not have the option to approach the Assessing Officerto issue a certificate for a lower tax deduction or to file declaration for nil deduction in respect of transactions covered under section194Q. Further Section 206C(1H) also does not allow the buyer to apply for the lower or NIL TCS certificate.

32. For the purpose of Section 194Q, for calculating the amount of purchases of ₹ 50 Lakhs for the FY 2021-22, whether the purchases before 01-07-2021 shall be considered?

This section was introduced by way of Finance Act 2021 and will be made effective from 01-07-2021. As such, the pertinent question that arises is whether the amount of purchases up to 30-06-2021 shall be considered while determining the threshold of ₹ 50 Lakh or not.

It has been stated in section 194Q that TDS shall be deducted @ 0.1% of such sum exceeding ₹ 50 Lakh. This threshold of ₹ 50 lakh has to be determined for every financial year. Therefore, it is imperative that purchase of goods made from 01-04-2021 to 30-06-2021 should also be considered for calculating the threshold of ₹ 50 lakh. The CBDT has also confirmed this position by way Circular 13/2021 issued on 30-06-2021.

Also, it is to be noted that similar issue was also raised at the time of implementation of section 206C(1H) as this provision was also made effective from the middle of the financial year i.e. FY 2020-21. For clarifying the same, CBDT issued a circular and stated that since the threshold of ₹ 50 Lakh is with respect to the financial year, calculation of receipt of sale consideration for triggering TCS under sub-section (1 H) of section 206C shall be computed from 1st April 2020. Hence, if a person being seller has already received ₹ 50 Lakh or more up to 30th September 2020 from a buyer, the TCS under sub-section (1H) of section 206C shall apply on all receipt of sale consideration during the previous year, on or after 1st October 2020, from such buyer.CBDT has further issued a Press Note on 30-09-2020 to provide that TCS shall be applicable only on the amount received on or after 01-10-2020.

Here are some illustrations for obtaining better understanding of the threshold limits:

Illustration 1: Purchases made from a seller is less than ₹ 50 Lacs up to 30-06-2021:

| 1. | Purchases up to 30-06-2021 | ₹ 35 Lacs |

| 2. | Invoices booked on or after 01-07-2021 | ₹ 25 Lacs |

TDS shall be deducted beyond purchases of ₹ 50 Lacs. The purchases made up to 30-06-2021 shall be considered for calculating the threshold. Therefore, on the initial purchases of ₹ 15 Lacs after 30-06-2021, TDS shall not be applicable. Consequently, TDS shall be deducted as and when purchases of ₹ 10 Lacs [₹ 25 Lacs + ₹ 35 Lacs – ₹ 50 Lacs] are booked.

Illustration 2: Purchases booked from a seller is more than ₹ 50 Lacs up to 30-06-2021:

| 1. | Purchases up to 30-06-2021 | ₹ 65 Lacs |

| 2. | Invoices booked from on or after 01-07-2021 | ₹ 20 Lacs |

In this case, the threshold of ₹ 50 Lakh has already been breached. As such TDS shall be deducted on every purchase booked on or after 01-07-2021. Also, please note that no TDS is to be deducted on purchase of ₹ 15 Lakh [₹ 65 Lacs – ₹ 50 Lacs] out of purchases booked up to 30-06-2021.

Appendix – 1

Transaction Flow Chart

Appendix-2

Various Scenarios of Applicability of either Section 194Q or Section 206C(1H):

Communication Template to be shared with Seller by Buyer.

–For 194Q–

Dear Partner,

Finance Act, 2021 has introduced Section 194Q in the Income-tax Act, 1961 requiring the buyer of goods to deduct TDS @ 0.10% on amounts paid or payable to the seller of goods. These provisions are applicable on those buyers whose total turnover/ gross receipts/ sales in preceding financial year exceeds ₹ 10 crore. Further, the TDS shall be deductible on the amount paid/ payable in excess of ₹ 50 lacs in a financial year. Such tax shall be deducted at the time of credit of such sum to the account of the seller or at the time of payment thereof by any mode, whichever is earlieri.e. such TDS shall be deducted even on payments made in advance.

Your company being a seller was collecting TCS under section 206C(1H) that was introduced w.e.f. 01st October 2020 @ 0.10% on amounts received from us.

Now, since our company, being a ‘Buyer’, satisfies the conditions laid down by section 194Q, we are liable to deduct TDS on amounts paid or payable w.e.f. 01st July 2021 and therefore, in terms of clause (b) of sub-section (5) of section 194Q read with second proviso to section 206C(1H) of the Income Tax Act, 1961 request you not to collect tax on amounts received from us w.e.f. 01st July 2021.

Appendix – 4

Communication Template to be shared with Buyer by Seller

–For 206C(1H)–

Dear Partner,

Finance Act, 2021 has introduced Section 194Q in the Income-tax Act, 1961 requiring the buyer of goods to deduct TDS @ 0.10% on amounts paid or payable to the seller of goods. These provisions are applicable on those buyers whose total turnover/ gross receipts/ sales in preceding financial year exceeds ₹ 10 crore. Further, the TDS shall be deductible on the amount paid/ payable in excess of ₹ 50 lacs in a financial year. Such tax shall be deducted at the time of credit of such sum to the account of the seller or at the time of payment thereof by any mode, whichever is earlieri.e. such TDS shall be deducted even on payments made in advance.

Our company being a seller was collecting TCS under section 206C(1H) that was introduced w.e.f. 01st October 2020 @ 0.10% on amounts received from us.

Now, w.e.f. 01st July 2021, the buyer shall be required to deduct TDS if he satisfies the conditions laid down by section 194Q, and in such a case, the seller shall not be required to collect TCS in terms of clause (b) of sub-section (5) of section 194Q read with second proviso to section 206C(1H) of the Income Tax Act, 1961. Therefore, we request you intimate us by ________ whether you are satisfying the conditions for a ‘buyer’ u/s 194Q so that we shall refrain from collecting TCS 01st July 2021 onwards. Please note that in case we do not receive any reply, we shall continue to collect TCS as per section 206C(1H).

Prepared by:

CA Dinesh Singhal | Partner- Tax & Regulatory | SNR & Company

CA Saurabh Panwar | Manager-Direct Taxes | SNR & Company

(Republished with amendments)

Author Bio

Sir,

Please suggest in every financial year shall we have the benefit of 50 lacs threshold limit or it is applicable on the first year only.

The limit of 50 Lacs is available every year

I have a paty from which sale & purchase both transation and both are exceeds 50 lakhs, suggest me which section shall be apply with party or TCS & TDS both are applicable

Please suggest that Section 194C and 194Q both attract, which one prevail either any one or both or anything else.

Can you provide CBDT Source for particular this point 19.

19. How and when to charge TCS from buyer? Alternative 1- The TCS can be collected by charging through invoice: In this case, both buyer and seller need to do accounting as receivable and payable for these amounts. It may be noted that if the payment is being made in next financial year, TCS obligation may not be applicable on seller (due to turnover threshold) or may not be applicable on buyer due to not making payments breaching ‘collection’ threshold in that financial year. In those case, one need to keep track and write off and reconcile it with the liability. Alternative 2: The TCS can be collected by charging through debit note: The logic for issuance of debit note may be that debit note to be issued at the time of payment so that it can be charged only on the eligible cases and no hassles of write off etc. (as mentioned in above points). But in that case, a specific series of debit note number may need to be used to make sure that these debit notes do not create issues in GST compliance.

It will be very helpful.

If a company has 2 unites with different GST but SAME PAN. One unit is newly established in 2021 and another one is functioning from few years with more than 10 crore turnover. Shall the new unit be liable to deduct tds u/s 194Q from the suppliers exceeding Rs. 50 lac ?

Please help in clarifying this problem raised recently –

The Seller has 10 Crores> turnover & the buyer also has 10 Crores> turnover, the seller has charged TCS ( show in Invoice) by mistake, where as the buyer has submitted 194Q declaration that the TDS would be deducted while making the payment to the seller. The problem is, the buyer has made the payment by deducted the TDS amount and also paid the TCS amount charged by the seller(shown in Invoice). Now, the buyer should do TDS and seller also do TCS? or can the TCS amount be given back to the buyer by way of credit note by the seller? by which only buyer will file TDS. Kindly advice, Thank you.

If person taking any professional services from another person and also purchase goods from that person then how section 194J and 194Q applicable

194J shall be applicable on the amount of services and 194Q shall be applicable on the amount of goods purchased.

Is the buyer liable to deduct TDS u/s 194Q on services procured by him exceeding Rs. 50 Lacs?

no

I need clarification regarding advance payments. we are paying in advance to our vendors on the basis of purchase order which enables us to indentify gst component separately. despite of that do we require to deduct TDS on bill amount or amount exclusive of GST

Sir , Purchaser’s last years ( F.Y. 2019-20 ) Turnover is more than 10 Crores and suppliers Turnover is also more than 10 Crores ( F.Y. 2019-20 ) But puchaser’s declaration is not activated in Seller’s end ( or Sellers raising e-invoice) and Seller’s is charging TCS on Tax Invoices from 01/07/2021 around on Rs. 82 lacs but as per IT rules – purchaser should deduct TDS under section 194Q but sellers already charged TCS , now what will do by PURCHASER beyond purchases of Rs. 50 lac

Sir , Purchaser’s last years ( F.Y. 2019-20 ) Turnover is more than 10 Crores and suppliers Turnover is also more than 10 Crores ( F.Y. 2019-20 ) But puchaser’s declaration is not activated in Seller’s end ( or Sellers raising e-invoice) and Seller’s is charging TCS on Tax Invoices from 01/07/2021 around on Rs. 82 lacs but as per IT rules – purchaser should deduct TDS under section 194Q but sellers already charged TCS , now what will do by PURCHASER beyond purchases of Rs. 50 lac

we have charged TCS on sale invoices up to 30th June-2021, on making payment of those invoices they charging TDS also is it correct.

If the invoice date before 01.07.21 & process/credit is current after 01.07.21 then TDS (194Q) will apply to that transaction or not?

Assume Invoice ta 31.05.21 & we are processing on 26 July ’21 then TDS under 194 q will be deducted on such transaction or not?

Hi!

This is Vasanth, MD, KNM group of Mills, Coimbatore, TN.

I’ve a small clarification. It’s about the new rule under section 194Q.

From the section 194Q, it’s clear that if a transaction is eligible for both 194Q & 206C(1H), 194Q would supersede and the buyer only needs to deduct tds of 0.1% on the value of goods (without gst).

Is there any chance that the seller can continue charging tcs 0.1% like how it was done in the last 12 months?!

Hoping to get a clear reply from you on this. Thanks in advance.

In the Circular issued by CBDT on 30 June 2021, they have stated that a circumstance where Seller has already collected TCS on sale of goods, then buyer would not be required to deduct TDS. However in my view, it is a situation thought of for initial stage where 194Q is being introduced from July 2021 and TCS is already complied with, however it is not advisable to follow it as practice. In case buyer is obligated to deduct TDS, then it should ensure that it is deducted U/s 194Q itself and seller is informed accordingly to not collect TCS

Dear sir,

if two parties are both (seller & buyer also)in this situation, witch tax is applicable TDS or TCS

IN DOLLAR B2B BILLS HOW TO DEDUCT OR CALCULATE TDS ??

Clarification needed for old bills before 30th June booking in July, should we discontinue TCS & only select 194Q or both. Pls clarify.

As per my understanding, Electricity is not goods. SC decision was rendered for another reference and not for Income Tax. Explanation to section 28(va) defines service which includes supply of electricity or other energy. Though explanation is for this specific clause but law of interpretation suggest that if something is given in the Act itself than definition cannot be borrow from another law.

Actually it may be goods for the distribution companies who purchases goods from discom

I have started new firm in this fy.

I buy product from 10cr+ seller and sells to 10 cr+ buyer.

Seller wants to collect tcs and buyer wants to deduct tds do both applicable to me?

Yes in this situation, it would be applicable from both sides as stated by you

Can we get give some declaration sort of to income tax to not deduct from both sides?

is TCS is chargeble 5% if buyer not filed IT return?

is TDS to be deducted from total amount(ie with GST amount)

is TCS is chargeble 5% if buyer not filed IT return?

Yes, in case seller is required to collect TCS and the buyer has not filed his returns as per provisions of section 206CCA, then 5% TCS shall be collected

is TDS to be deducted from total amount(ie with GST amount)

No, It has been clarified by CBDT by circular dated 30th June 2021 that TDS U/s 194Q shall not be deducted on GST separately charged in invoice. Though TCS shall continue to be collected on gross sales consideration

Onus and responsibility to absorb 0.1% is on buyer or seller

TDS U/s 194Q would be deducted by buyer of seller. However it shall not be a cost on seller as TDS credit would be available to him

A VERY GOOD ARTICLE , WHICH MADE CONCEPT CLEAR .

Thanks Sanjay Ji