This is the world of digitalization, with accessible internet, tech savvy citizens, and keeping in mind the perks of it, administrative departments in the country are on a pathway of digitalization. Physically operated administration practices are continuously being upgraded to computerized version to improve efficiency and resource utilization.

Taxpayers are also on the same hand required to be proactive in terms of technological infrastructure. Following are the digital implementations to be made by taxpayers to be compliant of rapidly drifting tax laws towards digitalization.

Page Contents

- Implementation 1: Providing facility for accepting payment through the prescribed electronic modes

- Implementation 2: E-Invoice

- Implementation 3: QR Code on invoices

- Implementation 4: E-Assessment scheme 2019

- Implementation 5: Document Identification Number (DIN)

- Implementation 6: Standard operating procedure in case of non-filers of GST returns.

Implementation 1: Providing facility for accepting payment through the prescribed electronic modes

https://taxguru.in/income-tax/cbdt-fine-businesses-rs-5000-day-digital-payment-facilities.html

Effectively applicable from: 1st day of February, 2020

Eligible tax payers: Every person, carrying on business if his total sales, turnover or gross receipts, as the case may be, in business exceeds fifty Crore rupees during the immediately preceding previous year. (Section – 269SU of Income Tax Act 1961)

Penalty for non-compliance: Rs. 5000 (Rupees Five Thousand), for every day during which such failure continues (Section – 271DB)

Prescribed Electronic modes: (Rule 119AA via. Notification No. 105/2019-Income Tax) In addition to the facility for other electronic modes of payment following modes are prescribed:

(i) Debit Card powered by RuPay;

(ii) Unified Payments Interface (UPI) (BHIM-UPI); and

(iii) Unified Payments Interface Quick Response Code (UPI QR Code) (BHIM-UPI QR Code)

Implementation 2: E-Invoice

https://taxguru.in/goods-and-service-tax/e-invoicing-gst-important-points.html

Effectively applicable from: voluntary from January 2020 and mandatory from April 2020.

Eligible tax payers: Registered person, whose aggregate turnover in a financial year exceeds one hundred crore rupees. (Notification No 68/2019 CT to 71/2019 – Central Tax)

An invoice issued by a registered person to another registered person (B2B invoice) shall be prepared by taxpayer in his regularly employed software, from there JSON file would be generated which would be uploaded on Invoice registration portal (IRP). IRP then shall generate unique Invoice Reference Number (IRN), digitally sign the invoice, generate QR code and send it to the recipient’s mail id provided in the invoice.

Implementation 3: QR Code on invoices

Effectively applicable from: 1st day of April, 2020.

Eligible tax payers: A registered person, whose aggregate turnover in a financial year exceeds five hundred crore rupees (Notification No. 72/2019 – Central Tax)

An invoice issued by a registered person to an unregistered person (B2C invoice), shall have Quick Response (QR)code

Implementation 4: E-Assessment scheme 2019

Eligible tax payers: Every assessee served with notice u/s 143(2)

Traditionally proceedings of assessment, right from selection and serving notice to completion of assessment were carried in physical manner. Digitalization swept in and e assessment was thought of. Department now eyes to make assessments completely faceless, nameless and jurisdiction less.

On 12th September 2019 notifications were issued by CBDT regarding e-assessment scheme 2019, which is to be launched in phased manner.

E-assessment is not a special type of assessment; just that current assessments are being made electronic. Reassessment u/s 147 is not covered.

All communication between assessee or any other person and all units and centres, including internal communication amongst them shall be mandatorily through NeAC and be exclusively through electronic mode.

Every notice/ order/ other communication shall be delivered to assessee by placing it on assessee’s registered account or sending to his/AR’s registered email address or uploading on assessee’s mobile app followed by a real time alert in all cases.

Mobile numbers and email ids should be regularly checked to avoid mistake of ignoring any communication by department.

Recently, it has been announced that over 58,322 cases have been picked under this scheme and e-notices for the AY18-19 have been served before 30/09/2019.

Implementation 5: Document Identification Number (DIN)

Taxpayers are required to examine genuineness of all communications sent by CBDT and CBIC tax officers by cross checking number quoted on them, on the respective portal.

No communication would be issued without DIN except only if exceptional circumstances require.

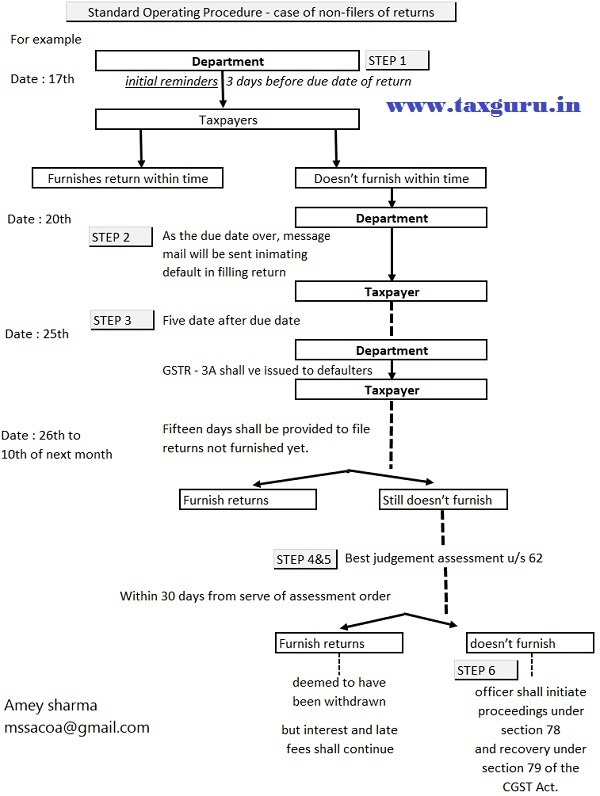

Implementation 6: Standard operating procedure in case of non-filers of GST returns.

https://taxguru.in/goods-and-service-tax/sop-case-non-filling-gst-returns-analysis.html

As you have seen in the procedure all communications shall be electronic. Hence it is required by taxpayers to regularly keep a track of communications on Mobile numbers and email ids to avoid mistake of ignoring any communication by department.

As to check return filling status, there exists no need to login to account to taxpayers, so by the help of automated tools or applications, both consultants and taxpayers can be proactive by generating timely reports.

Author Bio