DEFECTIVE RETURN NOTICE U/S. 139(9) OF I.T. ACT – ASKING TO FILE BALANCE SHEET AND P & L ACCOUNT ETC. IN PRESUMPTIVE INCOME SECTION 44AD, 44AE ETC. CASES

As we all aware that in current scenario, so many assesses who are filing their return mainly under head of business income. They are receiving the notices under section 139(9) i.e. notice for filing defective return. The main reason for issuing notices are missing the information of balance sheet and profit and loss accounts details in return. In this article the author is discussing on this issue in detail and covering all small aspects of this topic along with relevant examples and helpful screenshots of the concerned Income Tax Forms.

Page Contents

- i. Introduction

- ii. Probable Error Resulting In Above Requirement For Balance Sheet and Profit and Loss Account

- iii. Probable Error Resulting In Requirement For Statement Of Gross Turnover, Gross Profit etc.

- iv. Other Errors Resulting In Issuance of Notice U/s. 139(9)

- v. Correct Manner of Filing Return To Avoid Errors Due To Which The Return May Become Defective

- vi. Examples for better understanding

i. Introduction

There are various sections in the Income Tax Act, 1961 (“Act”) e.g., Section 44AD, Section 44AE, Section 44ADA etc., (popularly known as Presumptive Income sections) according to which, the profits and gains from eligible / prescribed businesses / professions carried by the prescribed categories of assessee (known as eligible assessee) are required to be computed for taxation, at least at the minimum rates prescribed in these sections. However, the assessee can voluntarily offer higher amount of profit / gain for taxation.

In cases where the profits and gains from such business / profession are computed and offered for taxation at the minimum prescribed rate or at any higher amount, there is no liability to mandatorily keep and maintain the regular books of accounts as per the provisions of Section 44AA of the Act. Thus, in such cases the assessee may not have balance sheet and profit and loss account.

The formats of the concerned Income Tax Return forms also takes care of the provisions of these sections and as such do not mandatorily requires the assessee to fill therein the figures of balance sheet and profit and loss account regarding such business / profession.

Despite that it is often seen that even in presumptive income cases, notice / Intimation U/s. 139(9) is send by the Income Tax Department to many assesses mentioning therein that their return has been considered as defective due to non filing of Balance Sheet and Profit and Loss account in the return (despite having no legal requirement).

ii. Probable Error Resulting In Above Requirement For Balance Sheet and Profit and Loss Account

The notice / intimation for above defect contains error description such as “Taxpayer having income under the head “Profits and gains of Business or Profession” but has not filled Balance Sheet and Profit and Loss Account as required in explanation (d) under section 139(9) read with section 44AA” (Error Code 31).

This error generally occurs in the cases of ITR forms like ITR 3, ITR 4 and ITR 5 etc. ( For AY 2018-19 and A.Y. 2019-20) wherein both presumptive as well as non presumptive income can be filled. However, the same may also be used where there is only presumptive business income.

The probable reason for occurrence of the above error may be incomplete / improper filing of information in the return. Due to that the departmental computer system may not be recognizing the presumptive income as such and may be treating the same as income from non presumptive business etc. The provisions of Section 44AA are applicable to non presumptive businesses etc. They require to mandatorily keep and maintain books of account when the income, turnover etc. of non presumptive business exceeds the prescribed limit. They are not applicable to presumptive business. However, since the departmental computer system may be considering the income from presumptive business as income from non presumptive business (due to improper information in return) it may, consequently be asking for Balance Sheet and Profit and Loss Account in cases where the presumptive business income, turnover etc. is over limits prescribed U/s. 44AA for mandatory keeping of books of accounts (by wrongly treating the same as non presumptive business).

One of the instance of such improper / incomplete filing of information may be that, in the return, only the Statement of Gross Receipt, Gross Profit etc. (which remains below Profit and Loss Account) is filled (as required in no books of account cases) and necessary adjustments as required in Schedule BP (i.e., Computation of Income From Business and Profession) are not made (later discussed in detail).

iii. Probable Error Resulting In Requirement For Statement Of Gross Turnover, Gross Profit etc.

It is mentionable here that in presumptive income business etc., though there is no liability U/s. 44AA to mandatorily keep and maintain regular books of accounts, but there is mandatory requirement under the provisions of Explanation (f) of Section 139(9) that where the books of account are not maintained, at least the amount of turnover / gross receipt, gross profit, expenses (along with basis of computation of above amounts ) and the amount of total sundry debtors, sundry creditors, stock-in-trade and cash balance as at the end of the previous year, are to be given in the return.

In many cases, the statements of Gross Receipts etc. are not filled in the return and the presumptive income is directly inserted in the Schedule BP against the concerned place for relevant presumptive income section 44AD, 44AE etc. This is not correct. In such cases the return may treated as defective due to non filling of the statement of Gross Receipts etc.

This error may not occur where the books of account are voluntarily kept and maintained and Balance Sheet and Profit and Loss Account are voluntarily filled in the return even in the presumptive income cases. In such cases, the Statements of Gross Receipts etc. are not required to be filed.

This error may occur in the cases of all the returns wherein the presumptive income can be filled e.g., ITR-4 (exclusively for Presumptive Business / Profession Income) and ITR-3 and ITR-5 for other than presumptive income for Assessment Year 2018-19 and 2019-20.

iv. Other Errors Resulting In Issuance of Notice U/s. 139(9)

The notices U/s. 139(9) are also issued in presumptive income cases for some other reasons / errors. For example- (a) In PART-A General the nature of business etc. mentioned is such which is not covered by presumptive income sections e.g., the income is offered U/s. 44AD but the nature of business is mentioned as Commission, Brokerage, Agency business, Sec. 44AE covered business or any Profession which are not eligible for benefit of Section 44AD. (b) Similarly, the income is offered under any presumptive income section but the same is less then that the minimum prescribed rate e.g., income offered U/s. 44AD is below minimum 8% or 6%. (c) An another example is that the turnover (in Section 44AD, 44ADA) exceeds the given turnover criteria of Rs. 2 Crore etc.

v. Correct Manner of Filing Return To Avoid Errors Due To Which The Return May Become Defective

STEP-1 : Before computing and offering income under presumptive income sections, ensure eligibility for the same as per the concerned section.

STEP-2 : Fill correct return form e.g., if there is only presumptive business etc. income then fill form ITR-4 (AY 2018-19 and AY 2019-20), use form ITR-3 and ITR-5 (AY 2018-19 and AY 2019-20) only where apart from presumptive business income there. This will eliminate chances of errors. However, if ITR-3 or ITR-5 etc. are used in the cases of pure presumptive business etc. income then the return will not be defective merely due to this sole reason itself.

STEP-3 : Where ITR-3, ITR-4 and ITR-5 (for AY 2018-19 and AY 2019-20) are used and the income is merely from presumptive income business etc., then in PART-A General, mention that there is no liability for maintaining books of account.

![]()

(Note : In cases where there are both presumptive and non presumptive business income, fill the information on the basis of liability U/s. 44AA in respect of non presumptive income business.)

STEP-4 : Fill correct nature of business (and its code). Ensure that the business etc. mentioned is by its nature covered under the respective presumptive income section (Detailed discussion is already made in earlier para).

STEP-5 : If there is only presumptive income and the regular books of accounts are kept voluntarily and Balance Sheet is available then it may be filled voluntarily. If Balance Sheet is not filled voluntarily, then mandatorily fill Statement of Total Sundry Debtors etc. (which remains below balance sheet).

It is possible in some cases that the assessee may not have any debtor, creditor, cash, stock as at the end of the year. Therefore, in such cases “Nil” or “0” may be validly mentioned in all points in this part of return.

STEP-6 : If there is only presumptive income and the regular books of accounts are kept voluntarily and Profit and Loss Account is available, then it may be filled voluntarily. If it is not filled voluntarily then mandatorily fill Statement of Gross Receipts / Turnover etc. (which remains below Profit and Loss Account).

The figures filled above are only illustrative. The assessee may fill it in his own manner e.g., he may compute gross profit and then mention expenses and then may compute net profit. The Net Profit in this part may be more or less than the minimum presumptive income. However, adjustment for the same will have to be made in later part.

(Note : In cases where there are both presumptive as well as non presumptive business etc. income, fill Balance Sheet and Profit & Loss Account or above two Statements as per the liability U/s. 44AA in respect of non presumptive business).

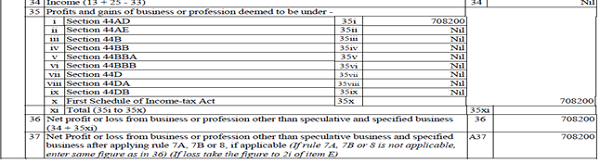

STEP-7 : Carry the net profit as per the above statement / profit and loss account (as the case may be) to Schedule BP and then deduct the presumptive income in point no. 4 (illustrative only and may differ in different return forms) as shown in picture below.

STEP-8 : Now, compute and fill the amount of presumptive income in the prescribed column in Schedule BP as mentioned in point no. 35 (illustrative only-and may differ in different return forms) in the picture below.

vi. Examples for better understanding

There may be different circumstances which may require different amounts to be mentioned in point no. 4, 35 and other relevant points. Some examples are given below.

CASE-1: If there is only presumptive income and the Net Profit as per Profit and Loss Account / Statement is Rs. 1,00,000/-, minimum presumptive income at prescribed rates is Rs. 1,10,000/-, then in point no. 4 Rs. 1,00,000/- will be deducted and in Point no. 35, Rs. 1,10,000/- will have to be added.

CASE-2: Suppose in the above case, the Net Profit as per Profit and Loss Account / Statement is Rs. 1,00,000/-, minimum presumptive income at prescribed rates is Rs. 90,000/-, then in point no. 4 Rs. 1,00,000/- will be deducted and in Point no. 35, Rs. 1,00,000/- will have to be added.

CASE-3: If there is only presumptive income, books of account are voluntarily maintained, profit and loss account is voluntarily filled but some disallowable items and other claims are also there, then the amounts in above point 4 and 35 shall be filled after making adjustments for disallowable items and claims e.g., Net Profit Rs. 1,00,000 + depreciation as per books disallowed Rs. 25,000- depreciation as per IT Rs. 20,000 + other disallowable Rs.5,000/-, then in point no. 4 the amount deductible shall be Rs. 1,10,000/-. Then in point no. 35, the above adjusted amount of Rs. 1,10,000/- or minimum prescribed presumptive income (whichever is higher) will have to be added.

CASE-4: Where both presumptive as well as non presumptive business and other income are also there and books of account are maintained and disallowable items and other claims are there, then the adjustments for amounts in above point no. 4 and 35 may be as under :

| Particulars | Other Head Income | Non Presumptive Business Income | Presumptive Business Income | Total |

| Net Profit as per profit and loss account | 1,00,000 | 2,00,000 | 1,00,000 | 4,00,000 |

| Less : Deductions for other head income | 1,00,000 | Nil | Nil | 1,00,000 |

| Nil | 2,00,000 | 1,00,000 | 3,00,000 | |

| Add : Depreciation as per books | Nil | 50,000 | 10,000 | 60,000 |

| Nil | 2,50,000 | 1,10,000 | 3,60,000 | |

| Less :

Depreciation |

20,000 | 5,000 | 25,000 | |

| Nil | 2,30,000 | 1,05,000 | 3,35,000 | |

| Less : presumptive inome (point 4) | Nil | Nil | 1,05,000 | 1,05,000 |

| Nil | 2,30,000 | Nil | 2,30,000 | |

| Nil | 2,30,000 | Nil | 2,30,000 | |

| Add : Presumptive Income (point no. 35 (Say 8% of turnover Rs.20 lacs) | Nil | Nil | 1,60,000 | 1,60,000 |

| Nil | 2,30,000 | 1,60,000 | 3,90,000 |

There are merely few illustrative cases. There may be other cases also in respect of which the information may be filled in the return on the above concept and basis. Similarly, the above analysis has been made mainly for presumptive incomes U/s. 44AD, 44ADA and 44AE and mainly for few ITR forms. The same analogy can also applied to other presumptive income sections and other ITR forms.

Disclaimer: The information contained in the above article are solely for informational purpose after exercising due care. However, it does not constitute professional advice or a formal recommendation. The author do not owns any responsibility for any loss or damage caused to any person, directly or indirectly, for any action taken on the basis of the above article.

(Republished with Amendments)

Author Bio

Taxpayer is offering Income under the head Profits and gains from Business or Profession. Hence, as per the provisions of Sec.44AA, the taxpayer is required to maintain books of accounts. However, as seen from the return, the taxpayer has not filled up Part A of the Profit and Loss Account and Balance Sheet. Further, income from business has not been offered under presumptive taxation, if eligible.

I want to know for following business and profession which ITR should be filed.

for MR. A

Home tuition Income

Mr. B

Civil Contractor

Mr. C

Beauty Parlour

Mr. D

Income from coaching Income

Plase assume all assessee is not liable to tax audit

I disagree with the author. Nowhere in the section, it is mentioned that the provisions of Section 44AA are applicable to non presumptive businesses etc. In fact Sec 44A (2) starts with ‘every person carrying on business or profession’ & u/s 44A(2)(i), the income & turnover limit is specified.

The misconception arises because of Sec 44AA(2)(iv) which says that person offering income lower than deemed income is required to maintain books of a/c’s. Now just because you are offering higher income than the deemed income, it does not mean you are exempted from maintaining books of a/c’s & Sec 44AA(2)(i) continues to apply.

Hence, if the Balance Sheet and P&L are not filled, notice u/s 139(9) will come.

Very good and nice helpful useful article

How to show for 44ADA income along with the remuneration from Firm i.e. my client is partner and also having the income from 44ADA.

Very good article. Great. Very informative & useful.

Thanks to author & TAXGURU.