CA Subhash Srinivasan

Is it Thumbs Up or DOWN ? Lets find out

- Sec 2 , Sec 9 and Sec 195 have been amended and it clarifies “ Property includes any rights in or in relation to an Indian company,including rights of management or control or any other rights whatsoever. This was retrospectively ammended from 01.04.1962. This ll open up VODOFONE case

- Sec 10 D and 80 C : any sum received under an insurance policy issued on or after the 1st day of April, 2012 in respect of which the premium payable for any of the years during the term of the policy exceeds ten per cent. of the actual capital sum assured

A the result any payment of insurance premium which is more than 10 % of Capital sum assured , then 80 C deduction is not available for that payment of Insurance premium

- Sec 35AD Where any specified business has commenced its operations on or after the 1st day of April, 2013, the deduction under sub-section (1) shall be allowed of an amount equal to one and one-half times of the expenditure referred to therein for setting up and operating an inland container depot or a container freight station notified or approved under the Customs Act, 1962; on or after the 1st day of April, 2012,where the specified business is in the nature of bee-keeping and production of honey and beeswax; on or after the 1st day of April, 2012, where the specified business is in the nature of setting up and operating a warehousing facility for storage of sugar

- Sec 35CCC & CCD– New Section Insertion – Sec 35 CCC Expenditure on agriculture extension project and 35 CCD Expenditure on any Silk Development project .

- Sec 44AB Tax Audit only if Business income is more than once crore rupees instead of 60 Lakhs and for profession if the income is more than 25 Lakhs instead of 15 Lakhs

- Sec 54B applicability have been redifined as the words “the assessee being an individual or his parent, or a Hindu undivided family” shall besubstituted with effect from the 1st day of April, 2013

- Sec 54GB (posted as per replica of the act ) After section 54GA of the Income-tax Act, the following section shall be inserted with effect from the 1st day of April, 2013, namely:— ‘54GB. (1) Where,—(i) the capital gain arises from the transfer of a long-term capital asset, being a residential property (a house or a plot of land), owned by the eligible assessee (herein referred to as the assessee); and (ii) the assessee, before the due date of furnishing of return of income under sub-section (1) of section 139, utilises the net consideration for subscription in the equity shares of an eligible company (herein referred to as the company); and (iii) the company has, within one year from the date of subscription in equity shares by the assessee, utilised this amount for purchase of new asset, then, instead of the capital gain being charged to income-tax as the income of the previous year in which the transfer takes place, it shall be dealt with in accordance with the following provisions of this section, that is to say,— (a) if the amount of the net consideration is greater than the cost of the new asset, then, so much of the capital gain as it bears to the whole of the capital gain the same proportion as the cost of the new asset bears to the net consideration, shall not be charged under section 45 as the income of the previous year; or(b) if the amount of the net consideration is equal to or less than the cost of the new asset, the capital gain shall not be charged under section 45 as the income of the previous year. (2) The amount of the net consideration, which has been received by the company for issue of shares to the assessee, to the extent it is not utilised by the company for the purchase of the new asset before the due date of furnishing of the return of income by the assessee under section 139, shall be de posited by the company, before the said due date in an account in any such bank or institution as may be specified and shall be utilised in accordance with any scheme which the Central Government may, by notification in the Official Gazette, frame in this behalf and the return furnished by the assessee shall be accompanied by proof of such deposit having been made

- Sec 68 Where assessee is a comopany and where sum received consists of application money and share premium by whatever name called, any explanation offered by such assessee-company shall be deemed to be not satisfactory, unless— (a) the person, being a resident in whose name such credit is recorded in the books of such company also offers an explanation about the nature and source of such sum so credited; and (b) such explanation in the opinion of the Assessing Officer aforesaid has been found to be satisfactory: Provided further that nothing contained in the first proviso shall apply if the person, in whose name the sum referred to therein is recorded, is a venture capital fund or a venture capital company as referred to in clause (23FB) of section 10.”.

- Sec 80C Additional Investment in Infrastructure Bonds was available earlier. In the prev years it have been extended year on year. But in this Finance BILL THERE IS NO MENTION OF EXTENTION OF DEDUCTION AVAILABLE FOR Infra structure Bonds. So Pranab has circulated Newtons law. “ Every action has equal and opposite reaction. Tax reduction on Rise in Basic Exemption is eradicated by not extending the prov on infra structure bonds.So Infra Bonds no longer Tax deductible

- Sec 80D – Limit not changed but Rs.5000 can b spend on preventive health check up for the family of the assessee or to parents of the assessee. LIMIT NOT CHANGED ( limit is within the earlier deduction )

- Sec 80DDB Age limit is changed. Instead of 65 years it is substituted by 60 years

- Sec 80 G and 80 GGA Insertion : No deduction shall be allowed under this section in respect of donation of any sum exceeding ten thousand rupees unless such sum is paid by any mode other than cash

- Sec 80 TTA new provision : Interest received from Savings Bank or post office deposits not being a time deposit , upto 10000 Rs. Is allowed as deduction.

( Earlier 10 years back this was U/s 80L )

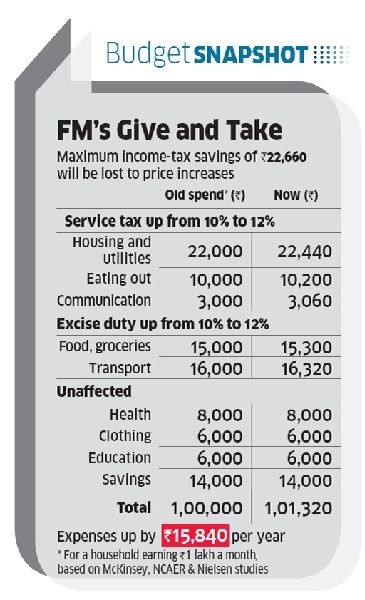

Conclusion : From this Budget its clearly we can find there ll be increase in prices of products and services as the service tax and Excise duty have been increased. The Savings in increase in exemption limit ll be cascaded by removal of infrabods investment, increase in tax rates in service tax and excise duty. Your Telephone , Train / Air Tickets , Food ll increase due to increase in service tax . If you are planning for a purchase of new apartment it ll also cost more by 2% and also there ll be increase in purchase price of the car and other capital goods as the Excise duty also increased.

In the end , Common Man ll always suffer for Everything . Corporate and politicians are enjoying a lot in the name of common man or aam adhmi whatever it may be.

(Author can be reached at subiin54@gmail.com)

Sir — I.T. Exemption limit for senior citizens should have been increased from 2.5 Lakhs to 3

Lakhs minimum and interest on FDs Should have been exempted minimum Rs. 50000/- . Thanks. Ca. K H Mahajan KHARGONE ( M.P.)