Analysis of various aspects of Dividend Distribution Tax (DDT), TDS on Dividend as per Income tax Act, 1961 or DTAA

Till FY 2019-20 the Company was required to pay Dividend Distribution Tax on Dividend declared or paid or distributed as per provision of section 115-O of Income tax Act, 1961 at the prescribed rate of 17.65% (excluding surcharge and cess). And the Company is required to make the payment of DDT within 14 days of the earliest event:

(a) declaration of any dividend; or

(b) distribution of any dividend; or

(c) payment of any dividend,

Vide Finance Act, 2020 amendments have been made in Section 10(34), Section 115-O and Section 194 of the Income tax Act, 1961. to brought Dividend within the ambit of income tax in the hands of recipient.

However, in many of the cases it has been observed that Dividend is being declared at board meeting/ annual general meeting held for adopting or approving audited financial statement and provision for such Dividend has already been made in the financial statement to be adopted or approved. Accordingly, in such scenario Company should pay DDT instead of deducting TDS as per Section 194 or any other section as may be applicable.

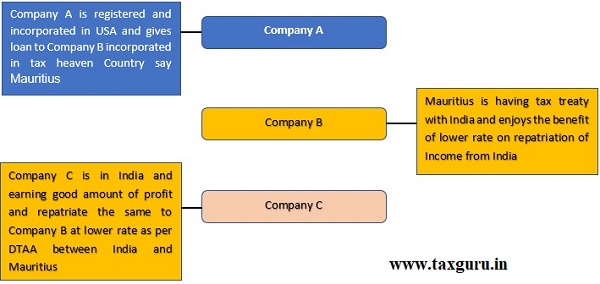

Now major concern arises when foreign company is holding shares of Indian Companies i.e. MNCs incorporated in India. Let us take example: Company A is incorporated in USA and wants to do business in India. But due higher tax impact on income earned in India and on repatriation of income from India Company A incorporates Company B in tax heaven Country say Netherlands or Mauritius by giving Loan to Company B and which in turn subscribe to share capital of Company C in India.

In this example Company B holds more than 50% shares of Company C.

Section 115A(1)(a)(i) of the Act, provides that Dividend Income received by foreign Company will be taxable in India at the rate of 20% which will further be increased by applicable surcharge and cess.

Majority of DTAAs entered between India and other countries provides for lower rate of either 10% or 15% with a condition that recipient is “beneficial owner” of the dividend.

Few of the DTAAs defined “Beneficial Owner” as under:

- 5% / 10% / 25% shares are held by recipient Company

- 10% / 25% of voting power is held by recipient Company

- 5% / 10% / 25% of capital is held by recipient Company

The term “Beneficial Owner” has also not been clearly defined under the Income tax Act, 1961, accordingly we will restrict our discussion on meaning of “Beneficial owner” to direct tax laws and judicial pronunciation.

To understand the meaning of the term beneficial ownership it is important to understand the rationale behind the introduction of the concept. The concept of beneficial ownership was introduced by the OECD in 1977 as a safeguard to prevent abuse of DTAAs by undertaking treaty shopping and primarily applies to passive incomes like dividend, interest and royalties.

In DTAA parlance treaty shopping refers to interposition of entities in jurisdictions that has a more advantageous DTAA as compared to the home jurisdiction. This is achieved by setting up entities in low / favourable tax jurisdiction and shifting the assets that confer the right to collect these dividends, interest and / or royalties 7 to such jurisdictions.

Accordingly, the concept of beneficial ownership was introduced in the DTAA articles dealing with the aforesaid sources of passive income to clarify the meaning of the word “paid to a resident”. The objective was to clarify that the source state was not obliged to give up taxing rights over passive income merely because the recipient was a resident of a DTAA jurisdiction unless he was also the beneficial owner of such income. The term ‘beneficial ownership’ is applied to distinguish legal ownership from economic ownership in circumstances where the legal owner is not the economic owner of an asset (owing to contractual or legal obligations or by conduct). In strict legal / technical sense with respect to any asset of a company / body corporate all rights in the asset, by operation of law, typically belongs to in absolute terms to the legal owner being such company / body corporate.

Section 2(32) of the Income tax Act, defines “person who has a substantial interest in the company”, in relation to a company, means a person who is the beneficial owner of shares, not being shares entitled to a fixed rate of dividend whether with or without a right to participate in profits, carrying not less than twenty per cent of the voting power;

The lifting of corporate veil to identify the beneficial owner, even under the Income tax Act, is not new. In certain circumstances of alleged tax avoidance through complex corporate structures, the Revenue Authorities have looked through a transaction in order to determine substance of the transaction. One of the most controversial instances of lifting of the corporate veil in the context of tax assessments was Vodafone International Holdings B.V. v/s Union of India [2009] 311 ITR 46 wherein the Supreme Court disregarded Revenue Authorities claim of taxing an indirect transfer of shares of an Indian entity caused by a transaction between multiple offshore entities as capital gains tax in India.

However, the Supreme Court in the case of Juggilal Kamlapt v. CIT [(1969) 73 ITR 702 (SC)] has held that that the doctrine of lifting the corporate veil ought to be applied only as a matter of exception and not as a routine matter. In several cases, there has been a litigation on levying the tax on the actual taxpayer or the beneficial owner of such taxpayer.

Tax Residency Certificate (‘TRC’) would serve as a valid document for establishing ‘beneficial ownership’ as well as status of residency for applying the DTAA – Circular No. 789 dated 03rd April, 2000, issued in the context of India-Mauritius DTAA, but widely used for other DTAAs.

In case of ADIT v Universal International Music B.V [TS-56-HC-2013(BOM)-O], the Bombay High Court placed reliance on the Circular 789 and, in view of the certificate of beneficial ownership issued by the Revenue authorities in Netherlands, held that the assessee was a ‘beneficial owner’ of royalty income received from Universal India. The ITAT also held that royalty income would be taxed at beneficial tax rate of 10% as per India-Netherlands treaty since the assessee was a ‘beneficial owner’ of the income.

Conclusion:

One must obtain “Beneficial Owenership” certificate complying with the requirement of applicable DTAA along with other documents such as TRC, NO PE Certificate and declaration in Form 10F in order to apply lower deduction rate as per applicable DTAA, however the said compliance will not rule out litigation or proceedings before lower authorities of Income tax.

Author Bio