Refund of Unutilized Input Tax Credit (ITC) on Zero Rated Outward Supply of Exempted Goods

As per Section 17(2) of CGST Act, 2017–

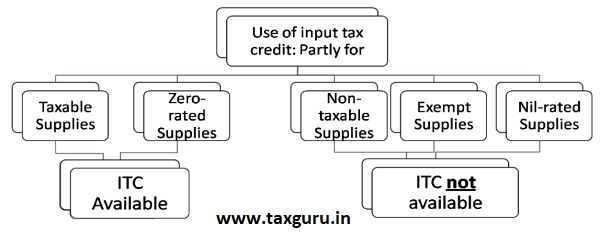

’Where the goods or services or both are used by the registered person partly for effecting taxable supplies including zero-rated supplies under this Act or under the IGST, and partly for effecting exempt supplies under the said Acts, the amount of credit shall be restricted to so much of the input tax as is attributable to the said taxable supplies including zero-rated supplies.’

The above section clearly specifies that we can’t claim ITC on the goods used, if we are making Non taxable supplies, exempted supplies, nil rated supplies.

♠ Am I eligible to take ITC on supplies used, for making zero rated supply of exempted goods?

As per Section 16 (2) of IGST Act, 2017 –

‘’Subject to the provisions of section 17(5) ineligible credit of the CGST Act, credit of input tax may be availed for making zero-rated supplies; notwithstanding that such supply may be an exempt supply’’.

- Meaning thereby, even if the goods or service which are either exported or supplied to SEZ unit developer are exempted goods or services, input tax credit is still available for making such zero rated supplies, provided that is not covered under section 17(5) blocked credit.

- The requirement to reverse ITC in relation to exempted supplies is not warranted if it is zero rated. This can also be inferred from Section 16(2) of the IGST Act 2017 which states that the input tax credit is eligible notwithstanding that such supply is exempted.

♠ Am I eligible for Refund of Unutilized Input Tax Credit on Zero Rated Outward Supply of Exempted or Non-GST Goods?

As per Section 54(3) of CGST Act, 2017

‘’ A registered person may claim refund of any unutilized input tax credit at the end of any tax period in below mentioned cases:

(i) zero rated supplies made without payment of tax

(ii) where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies).

Provided further that no refund of unutilized input tax credit shall be allowed in cases where the goods exported out of India are subjected to export duty:

Provided also that no refund of input tax credit shall be allowed if the supplier of goods or services or both avails of drawback in respect of central tax or claims refund of the integrated tax paid on such supplies’’.

- Therefore, from the above provisions it is opined that Refund of Unutilized Input Tax Credit can be claimed on Zero Rated Outward Supply (Exports) of Exempted Goods if :

- Export Duty is not leviable on Exported Goods or

- Duty Drawback is not claimed by the Exporter or

- Refund of the IGST paid on such supplies is not claimed.

- Moreover, this provision is clarified by CBIC wherein it is stated that as per section 16(2) of the IGST Act, credit of input tax may be availed for making zero rated supplies, notwithstanding that such supply is an exempt supply.

♣ Whether bond or Letter of Undertaking (LUT) is required in the case of zero rated supply of exempted goods?

As per Section 16(3) of IGST, 2017-

‘’A registered person making zero rated supply shall be eligible to claim refund under either of the following options, namely: ––

(a) he may supply goods or services or both under bond or Letter of Undertaking, subject to such conditions, safeguards and procedure as may be prescribed, without payment of integrated tax and claim refund of unutilized input tax credit; or

(b) he may supply goods or services or both, subject to such conditions, safeguards and procedures as may be prescribed, on payment of integrated tax and claim refund of such tax paid on goods or services or both supplied, in accordance with the provisions of section 54 of the Central Goods and Services Tax Act or the rules made thereunder’’.

- Further, as per section 16(3) of the IGST Act, a registered person making zero rated supply shall be eligible to claim refund when he either makes supply of goods or services or both under bond or letter of undertaking (LUT) or makes such supply on payment of integrated tax. However, in case of zero rated supply of exempted goods, the requirement for furnishing a bond or LUT is not required.

It is also categorically stated that the requirement of Bond/LUT cannot be insisted upon in such cases. (Circular No 45/2018 dated 30.05.2018). F. No. CBEC/20/16/4/2018-GST

Relevant definitions

“Zero rated supply” means any of the following supplies of goods or services or both, namely:

(a) export of goods or services or both; or

(b) supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit.

“Exempt supply” means supply of any goods or services or both which attracts nil rate of tax or which may be wholly exempt from tax under section 11, or under section 6 of the Integrated Goods and Services Tax Act, and includes non-taxable supply.

Author Bio

should we need to raise tax invoice or bill of supply for the same and who we will file or show in gstr1 and 3b

Our 50% sales is Zero Rated Supply (export sales) is exempt supply. Can we claim ITC on inputs like packing materials, fumigation servies, shipping agents services and quality certification services.

Yes, you can claim a refund proportionately.