Sandeep Insan

Here we are discussing some generally asked questions about GST. These questions and given answers surely will help you to understand GST, its main specification, features, components, benefits etc.

Here we are discussing some generally asked questions about GST. These questions and given answers surely will help you to understand GST, its main specification, features, components, benefits etc.

What is GST and its current Status?

The GST is a taxation system where there is a single tax in the economy for goods and services. This Taxation System is meant to create a single taxation system in the entire country for all goods and services. GST is destination based tax. The GST is called Single biggest tax reforms after independence. According to our honorable Finance Minster Mr. Arun Jately GST will boost the economic growth of country and will reduce the prices in long run. Now after being passed in Lok Sabha on 6th May 2015 the GST constitutional amendment bill required to be passed with 2/3 majority in Rajya Sabha as well followed by its ratification by at least 50% of the states before it becomes law of the land. And its effectiveness can be measured through by knowing that globally more than 140 countries have implemented GST.

On Which Goods and Services GST will be apply?

Goods and Service tax will be apply on all goods and services. But some exceptions are provided, these are given as follows:

A) Alcoholic liquor for human consumption

B) Tobacco

C) Petroleum & Petroleum Products shall not be subject to levy of GST till notified at future date on the recommendation of GST council. Till that future date same rate will be applicable.

What are the Components of GST and Its Collection?

The GST has three components.

Central Goods and Services Tax: This component of GST will be collected by Central government and this tax will levy when sale is made within state.

Central Goods and Services Tax: This component of GST will be collected by Central government and this tax will levy when sale is made within state.

State Goods and Services Tax: This component of GST will be collected by State Government and this tax will levy when sale is made within state.

Integrated Goods and Services Tax: This component of GST will be collected by Central Government and this tax will levy on all interstate supplies. Proceeds of IGST will be apportioned among the States.

In other words we can say that under the new system a transaction of sale within state shall have two types of taxes CGST and SGST. That means these taxes will levy simultaneously. IGST is only one type of tax and will be levy on Interstate sale.

Cental Taxes subsumed under GST

- Central Excise Duty

- Service Tax

- CVD-Additional Custom Duty

- SAD-Special Additional Duty

- Central Surcharge and Cess

State Taxes subsumed under GST

- Value Added Tax

- Central Sale Tax

- Octroi and Entry Tax

- Purchase Tax

- Luxury Tax

- Taxes on Lottery, Betting & Gambling

- State Cess and Surcharge

- Entertainment Tax

NOTE: Basic Custom Duty will continue to be charged even after introduction of GST. Other Indirect taxes such as Stamp Duties etc. shall also be continue.

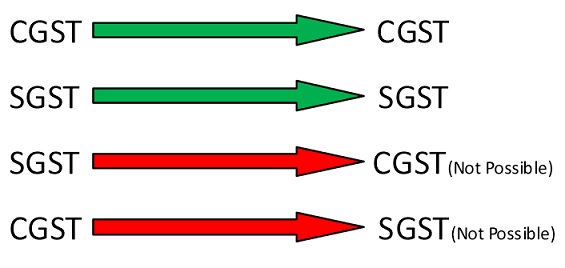

How the Input Tax Credit will be utilize:

Input of CGST can be utilized for making payment of CGST and like this input of SGST can be utilized to make payment of SGST. Input of SGST cannot be utilize to make payment of CGST and vice-versa.

But here is an exception In case of interstate supply of Goods and services under the IGST model. In IGST both the input taxes are taken as credit. But we see that SGST never went to the Central government, still the credit is claimed. This is the crux of GST. Since this is a loss to the Central government, the state governments will compensate the central government by transferring the credit to the central government.

But here is an exception In case of interstate supply of Goods and services under the IGST model. In IGST both the input taxes are taken as credit. But we see that SGST never went to the Central government, still the credit is claimed. This is the crux of GST. Since this is a loss to the Central government, the state governments will compensate the central government by transferring the credit to the central government.

The existing problem with the GST is that credit of VAT is not available against excise duty or vice versa. We all know that VAT is computed on a value which includes excise duty and cenvat credit is allowed only for excise duty paid on inputs and not on the VAT paid on input raw material. This shows that there is tax on tax.

What is Registration Limit and what is Taxpayer Identification No.:

A Uniform state GST threshold across states is describe and therefore it is considered that a threshold of annual gross turnover of Rs. 10 Lacs both for Goods and Services in all states and union territories may be adopted with adequate compensation for the state. The issue is still not resolved, like there is no clear cut limit about this.

All the taxable entities in the above prescribe limit will be require to get register and obtain GST registration no. and also for other option to register. GST identification no. will be linked with PAN and it may have 13 to 15 digits. There will be Single registration no. for all branches in a state. Therefore a dealer having branches outside or across the states will have as many GST registration no. as the no. of states in which it is going to operate.

What are the benefits of GST?

For Central and State Government: By Implementing the GST India will earn Rs.15 Billion in a year. This is because it will promote more export. It will create more employment opportunity and boost the growth.

For Individuals And Companies: In the GST System taxes for both centre and state will be collected at point of sale .Both will be charged on the manufacturing cost. Individuals will be benefited by this as prices are likely to come down and lower prices means more consumption and more consumption means more production thereby helping in the growth of the companies.

And another biggest benefit will be that multiple taxes like octroi, CST, State sale tax, Entry tax, License fee, turnover tax etc. will no longer be present as these will be brought under GST. Doing business now will be easier and more comfortable as various hidden taxes will not exist.

Author Bio

I want to add to your point ”There will be Single registration no. for all branches in a state”. In the GST draft it has been mentioned that an assessee may have multiple registration within a State.

It is very simple to understand.