Case Law Details

Shri Ashok Khatri Vs M/s S3 Infra Reality Pvt Ltd (NAA)

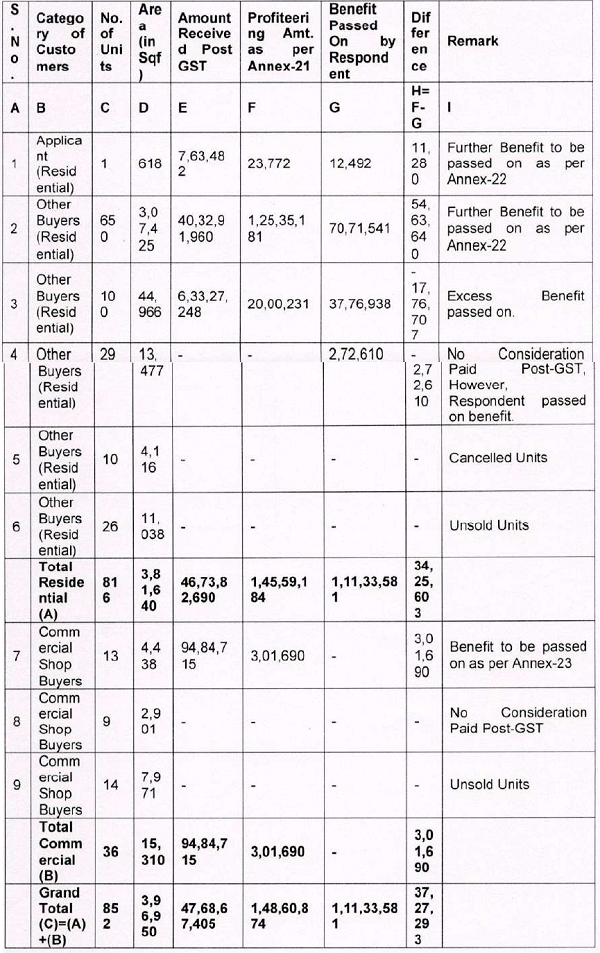

From the documents placed on record and the DGAP’s report it is evident that the Respondent has sold 780 units out of 816 residential units, out of which for 29 units there was no consideration paid after introduction of GST, hence the profiteered amount has to be calculated only for 751 units which have been sold and consideration received. Out of these 751 home buyers the DGAP has admitted that for 100 buyers the entire profiteered amount has already been paid. Hence in respect of 651 units as has been shown in the table below the profiteered amount comes to Rs. 1,45,59,184 which includes an amount of Rs. 23,772 for the Applicant No. 1 and Rs. 1,45,35,412 for all the other 650 home buyers. It has also been verified by the DGAP that in the case of the above Applicant, the Respondent has already paid an amount of Rs. 12,492, out of the profiteered amount of Rs. 23,772 hence the balance amount of Rs. 11,280 is to be paid. In the case of the balance 650 buyers, an amount of Rs. 70,71,541 has already been paid and balance amount of Rs. 54,63,640 is required to be paid. With regard to the commercial units only 13 units out of 36 units have been sold and an amount of Rs. 3,01,690 has been profiteered. Thus a total amount of Rs. 3,01,690 has to be paid to all the buyers of these commercial units. Accordingly out of total profiteered amount of Rs. 1,48,60,874 an amount of Rs. 90,84,264 has already been passed on as is evident from Annexure 17 of the DGAP’s Report where intimations have been filed by the Respondent stating the details of the payments regarding ITC benefit paid to their buyers. The balance amount of Rs. 57,76,610 is to be passed on to the identified buyers.

It is evident from the above that the Respondent has denied benefit of ITC to the buyers of the flats being constructed by him under the above Policy in contravention of the provisions of Section 171 (1) of the CGST Act, 2017 and has thus realized more price from them than he was entitled to collect and has also compelled them to pay more GST than that they were required to pay by issuing incorrect tax invoices and hence he has committed an offence under section 122 (1) (i) of the CGST Act, 2017 and therefore, he is liable for imposition of penalty. Accordingly, a Show Cause Notice be issued to him directing him to explain why the penalty prescribed under Section 122 of the above Act read with rule 133 (3) (d) of the CGST Rules, 2017 should not be imposed on him.

FULL TEXT OF ORDER OF NATIONAL ANTI-PROFITEERING APPELLATE AUTHORITY

1. This Report dated 28.11.2018, has been received from the Applicant No. 2 i.e. the Director General of Anti-Profiteering (DGAP), under Rule 129 (6) of the Central Goods & Services Tax (CGST) Rules, 2017. The brief facts of the present case are that a complaint dated 04.04.2018 was filed before the Haryana State Screening Committee on Anti-Profiteering by the Applicant No. 1 alleging profiteering by the Respondent in respect of purchase of a flat in the Respondent’s project “Auric City Homes” situated in Village Bathola, Sector-82, Faridabad, Haryana-121007. The above Applicant had alleged that the Respondent had not passed on the benefit of Input Tax Credit (ITC) to him by way of commensurate reduction in the price after implementation of the GST w.e.f. 01.07.2017 and charged GST on full amount of instalments. This Complaint was further referred to the Standing Committee on Anti-profiteering by the Screening Committee vide minutes of its meeting dated 20.06.2018 under Rule 128 of the above Rules.

2. The above Complaint was examined by the Standing Committee on Anti-profiteering in its meeting held on 07.08.2018 & 08.08.2018 and its minutes were forward to the DGAP for detailed investigation under Rule 129 (1) of the CGST Rules, 2017.

3. The DGAP on receipt of the above minutes had called upon the Respondent to submit reply as to the whether the ITC benefit was passed on by him to his recipients and also asked him to suo-moto determine the quantum of benefit which was not passed on. The Respondent had submitted replies vide letters dated 20.09.2018, 10.10.2018, 16.10.2018, 01.11.2018, 12.11.2018, 13.11.2018, 14.11.2018, 15.11.2018, 19.11.2018, 22.11.2018 and 26.11.2018 stating that he was in the business of construction of flats under the Affordable Housing Scheme sanctioned under the Haryana Affordable Housing Policy, 2013 in Sector-82, Faridabad. The Respondent had also stated that after implementation of the GST w.e.f. 01.07.2017, the ITC on purchase of materials during July. 2017 and August, 2017 was negligible and he had raised the first demand without giving the benefit of ITC by changing GST @ 12% on 14.08.2017. He had further stated that he had raised the next demand on 14.02.2018 by levying GST @ 8% due to change in the rate of tax as per the Notification issued on 25.01.2018 and had -7‘ given the benefit of ITC provisionally and informed the buyers that the benefit of ITC would be passed on to them at the time of handing over possession of the flats. The Respondent also submitted that the Applicant No. 1 had filed the complaint on 04.04.2018 in which he had mentioned about the demand raised by the Respondent in the month of August, 2017, but he had failed to mention the demand which was raised in the month of March 2018 which included the benefit of ITC which was passed on to the Applicant. He has further submitted that he had given the benefit of ITC to his customers and also assured them that such benefit would be passed on at the time of possession.

4. The DGAP’s investigation report has covered the period from 01.07.2017 to 31.08.2018.

5. The Respondent had also submitted the following documents along with their replies:-

(a) Copies of GSTR-1 returns for July. 2017 to August, 2018.

(b) Copies of GSTR-3B returns for July, 2017 to August, 2018 along with copies of challans for depositing the GST in Cash.

(c) Copies of Tran-1 returns for transitional credit availed.

(d) Copies of VAT & ST-3 returns for April, 2016 to June, 2017.

(e) Copies of all demand letters and sale agreement/contract issued in the name of Shri Ashok Khatri.

(f) Tax rates- pre-GST and post-GST.

(g) Copy of Balance Sheet for FY 2016-17 & FY 2017-18.

(h) Copy of Electronic Credit Ledger for 01.07.2017 to 31.08.2018.

(i) CENVAT/Input Tax Credit register for April, 2016 to August. 2018.

(j) Details of taxable turnover and input tax credit for the project “Auric City Homes”.

(k) List of home buyers in the project “Auric city Homes” along with buyers of commercial shops.

(l) Copy of Project Report of RERA.

(m) Reconciliation of turnover reported in GSTR-3B with list of home buyers.

(n) Details of unsold flats and unsold commercial shops.

(o) Copies of contract and demand letters for new bookings made during the period August, 2018 to October, 2018 reflecting passing of 2% benefit of GST input credit to new allottees.

(p) Details of Customer wise benefit passed on.

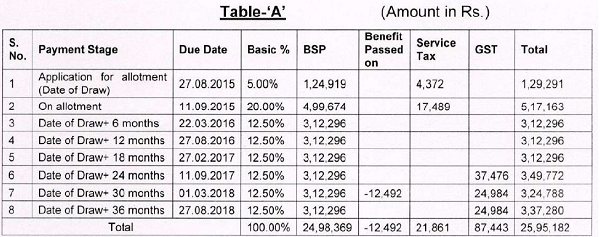

6. The DGAP in his report has submitted that as per the documents submitted by the Respondent, the payment schedule for the purchase of a flat measuring 618.24 square feet at the basic sale price of Rs. 4,000/- per square feet and the details of amounts and taxes paid by the Applicant No. 1 to the Respondent were as has been given below in the Table:-

Table-`A’ (Amount in Rs.)

7. The DGAP has also submitted that unlike other cases in which allegation of not passing on the benefit of ITC is generally contested but in the present case the Respondent had suo-moto admitted that there has been benefit of ITC post GST and he had passed on such benefit to the above Applicant by reducing the demand raised in the month of February, 2018 by Rs. 12,492/- which was 1.23% of the amount collected post-GST. The Respondent had also assured that the final input tax credit benefit would be provided at the time of possession.

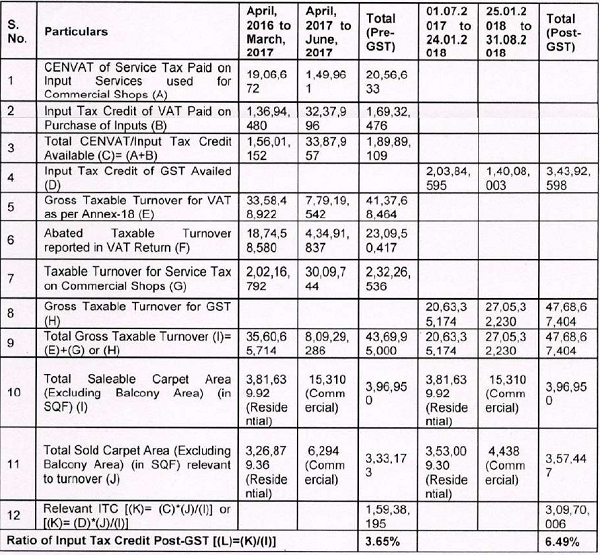

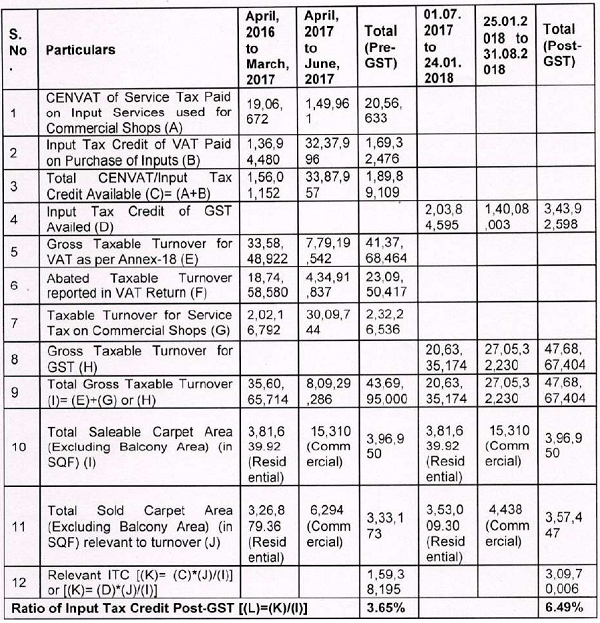

8. The DGAP in his Report has further submitted that prior to 01.07.2017, i.e., in the pre-GST era, the service of construction of affordable housing, provided by the Respondent, was exempted from the Service Tax under Notification No. 25/2012-ST dated 20.06.2012, as amended by Notification No. 9/2016-ST dated 01.03.2016 and hence the Respondent was not eligible to avail credit of Central Excise Duty paid on the inputs or Service Tax paid on the input services, however, the Respondent was eligible to avail CENVAT credit of Service Tax paid on input services for the commercial shops sold by him. He has also claimed that the Respondent was eligible to ITC on VAT paid on inputs but the CENVAT credit of Central Excise Duty paid on inputs was not available and post-GST, the Respondent was eligible to avail ITC of GST paid on inputs and input services including the tax paid by his sub-contractors. He has further claimed that from the data submitted by the Respondent duly verified from his returns filed during the pre-GST period (April, 2016 to June, 2017) and the post-GST period (July, 2017 to August, 2018), the details of the ITC availed and the taxable turnover during the above periods were as under:-

9. The DGAP has also contented that from the above Table, it was clear that the ITC as a percentage of the total turnover that was available to the Respondent during the pre-GST period from April, 2016 to June, 2017 was 3.65% and during the post-GST period w.e.f. July, 2017 to August, 2018, it was 6.49%. The Report has further claimed that this data duly confirmed that post-GST the Respondent had benefited from additional ITC to the extent of 2.84% [6.49% (-) 3.65%] of the taxable turnover. The DGAP has also noted that the Central Government, on the recommendation of the GST Council, had levied 18% GST, effective rate of which was 12% in view of 1 /3rdabatement on the value of land on construction service vide Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017. He has further noted that the actual GST rate on construction service in respect of affordable and low-cost housing was further reduced from 12% to 8%, vide Notification No. 1/2018-Central Tax (Rate) dated 25.01.2018. In view of the change in the GST rate after 01.07.2017, the DGAP has examined the issue of profiteering in two parts, i.e., by comparing the applicable tax rate and input tax credit available for the pre-GST period from April, 2016 to June, 2017 when only VAT was payable @5.25% with (1) the post-GST period from July, 2017 to 24.01.2018 when the effective GST rate was 12% and (2) with the GST period from 25.01.2018 to 31.08.2018 when the effective GST rate was 8%. Accordingly, on the basis of the above Table, the comparative figures of ITC available during the pre-GST and the post-GST period and the profiteered amount have been tabulated by the DGAP as per the Table given below:-

Table C

| S.

No |

Particulars | Pre-GST | Post- GST | |||

| 1 | Period | A | 01.0

4.20 16 to 30.0 6.20 17 |

01.07. 2017 to 24.01.

2018 |

25.01. 2018 to 31.08.

2018 |

Total 01.07. 2017 to 31.08.

2018 |

| 2 | Output tax rate (%) | B | 5. 25 ok | 1 02.00 o | 8.00% | |

| 3 | Ratio of CENVAT/ Input Tax Credit to Taxable Turnover asper Table — Babove (%) | C | 3.65 % | 6.49% | 6.49% | 6.49% |

| 4 | Increase in tax rate post-GST (%) | D | 6.75% | 2.75% | ||

| 5 | Increase in input tax credit availed post- GST (°/0) | E= 6.49% less 3.65% |

2.84% | 2.84% | 2.84% | |

| Analysis of Increase in input tax credit: (Amount in Rs.) | ||||||

| 6 | Base Price collected during July, 2017 to August, 2018 | F | 20,63,

35,17 4 |

27,05,

32,23 0 |

47,68,

67,40 4 |

|

| 7 | GST Collected over Basic Price | G= F*12%

or 8% |

4,64,0 | 2,47,6 0,221 |

2,16,4

2,578 |

2,799 |

| 8 | Total Demand collected | H=F+G | 23,10,

95,39 5 |

29,21,

74,80 9 |

52,32, 70.20 4 |

|

| 9 | Recalibrated Basic Price | 1= F*(1-E) or 97.16% of F | 20,04,

75,25 5 |

26,28,

49,11 5 |

46,33,

24,37 0 |

|

| 10 | GST @12% | J= I*12°/0 | 240,5

7,031 |

210,2 7,929 |

450.8

4,960 |

|

| 11 | Commensurate demand price | K= I+J | 22,45,

32.28 6 |

28,38,

77,04 4 |

50,84,

09,33 0 |

|

| 12 | Excess Collection of Demand or Profiteering Amount |

– L= H K | 65,63,

109 |

82,97,

765 |

1,48,6

0,874 |

|

10. The DGAP has also intimated that, it was quite clear from the above Table that the additional ITC of 2.84% of the taxable turnover should have resulted in commensurate reduction in the base price and therefore, in terms of Section 171 of the CGST Act, 2017, the benefit of the additional ITC that had accrued to the Respondent. was required to be passed on to the flat buyers. The DGAP has further intimated that the Respondent had admitted that any benefit of ITC would eventually have to be passed on to the recipients and in fact, he had passed on an amount of Rs. 1,11,33,581/- till 31.08.2018 which had been duly verified from the demand/intimation letters submitted by the Respondent.

11. The DGAP had also claimed that on the basis of the aforesaid availability of ITC pre and post-GST and the details of the amount collected by the Respondent from the Applicant and other home buyers during the period w.e.f. 01.07.2017 to 24.01.2018, the amount of benefit of ITC which needed to be passed on by the Respondent to the recipients, the profiteered amount came to Rs. 65.63,109/- which included 12% GST on the base profiteered amount of Rs. 58,59,919/-. He has further claimed that the amount of benefit of ITC that needed to be passed on by the Respondent to the recipients or in other words, the profiteered amount realised by him during the period between 25.01.2018 to 31.08.2018. come to Rs. 82,97,765/- which included 8% GST on the base profiteered amount of Rs. 76,83,115/- and therefore, the total profiteered amount during the period 01.07.2017 to 31.08.2018 was Rs. 1,48,60,874/- which included GST (@ 12% or 8%) on the base profiteered amount of Rs. 1,35,43,034/-. The home buyer and unit no. wise break-up of this amount was provided in Annex-21 by the DGAP attached with his report, which was inclusive of Rs. 23,772/-(including GST on the base amount of Rs. 21,683/-) which was the profiteered amount in respect of the Applicant No. 1, mentioned at serial No. 65 of Annex-21 of the DGAP’s report.

12. The DGAP has also submitted that on the basis of the details of the outward supplies of the construction service submitted by the Respondent, it was observed that the service was supplied in the State of Haryana only. It is also stated by him that the Respondent had suo-moto passed on the benefit of ITC in the month of February, 2018, even prior to the filing of the complaint by the above Applicant. The Respondent had passed on the benefit of Rs. 1,11,33,581/-which had been duly verified from the data submitted by the Respondent. A summary of category-wise profiteering & the benefit passed on is given in the Table below:-

Table D (Amount in Rs.)

13. The DGAP in his report has noted that as per the table given above the Respondent had passed on lesser benefit than what he should have passed in respect of 651 cases of residential flats (Sr. 1 & 2 of above table) amounting to Rs. 54,74,920/- and of Rs. 3,01,690/- in respect of 13 commercial shops as mentioned at Sr. 7 of above table. Further, he has noted that the Respondent had passed on higher benefit compared to what he should have passed to 129 buyers of residential flats (Sr. No. 3 & 4 of the above table) amounting to Rs. 20,49,317/-, however, this amount of excess benefit passed on couldn’t be set off against the additional benefit to be passed on to other recipients, but could be adjusted against the future demands from such 129 home buyers.

14. The DGAP has concluded that the benefit of additional ITC of 2.84% of the taxable turnover which had accrued to the Respondent was required to be passed on to the above Applicant and the other recipients and the provision of Section 171 of the CGST Act, 2017 had been contravened by the Respondent in as much as the additional benefit of ITC @2.84% of the base price received by the Respondent during the period w.e.f. 01.07.2017 to 31.08.2018, has not been passed on to the Applicant and other recipients by the Respondent. He has further claimed that on this account. the Respondent had realized an additional amount of Rs. 23,772/- (Sr. No. 1 of table- `D’ in para-19) from the above Applicant which included both the profiteered amount @2.84% of the taxable amount (base price) and GST on the said profiteered amount, however, the Respondent had suo-moto passed on Rs. 12,492/- as per the demand letter dated 10.02.2018 issued to the Applicant, and therefore, the Respondent had profiteered by an amount of Rs. 11,280/- (23,772/- (-) 12,492/-). Further, the Report has stated that the Respondent had also realized an additional amount of Rs. 57,65,329/- as mentioned at Sr. No. 2 & 7 of the Table- ‘D’ above which included both the profiteered amount @2.84% of the taxable amount (base price) and GST on the said profiteered amount from 663 other recipients who were not applicants in the present proceedings. The Report further admitted that these recipients were identifiable as per the documents on record as the Respondent had provided their names and addresses along with unit no. allotted to them, therefore, this additional amount of Rs. 57,65,329/- was required to be returned to such eligible recipients. The DGAP has also submitted that the present investigation covered the period from 01.07.2017 to 31.08.2018 and profiteering, if any, for the period post August, 2018 has not been examined as the exact quantum of ITC that would be available to the Respondent in future could not be determined at this stage when the construction of the project was yet to be completed.

15. The above report was considered by the Authority in its meeting held on 03.12.2018 and it was decided to hear the Applicants and the Respondent on 19.12.2018, which was postponed to 07.01.2019 on the request of the Respondent. On 07.01.2019 the Applicant No. 1 did not appear but the DGAP was represented by Shri Manoranjan, Assistant Commissioner while Mr. Ankur Agarwal, Authorised representative and Ms Alka Gupta, CA appeared on behalf of the Respondent. Further hearings were held on 13.02.2019 and 18.02.2019. The Respondent during the hearing submitted that the total turnover of his project was 175 Crores and the project was an affordable housing project. He also submitted that the project had started in August, 2015 and the possession of the flats would be given by July, 2019. The Respondent accepted the Report submitted by the DGAP and said that he was in the process of passing on the ITC benefits as had been mentioned in the DGAP’s report to all the recipients/buyers.

16. The Respondent further admitted that the amount of profiteering as calculated by the DGAP would be passed on to all the buyers for both the residential and the commercial units. He also reiterated that the major amount as calculated by the DGAP had already been passed on and the balance amount will be paid in due course. On 18.02.2019 the Respondent further submitted that with reference to the DGAP’s notice dated 20.12.2018, he had passed on the ITC to the customers as per the calculation given by the DGAP as has been calculated vide Annexure-22 of the DGAP’s Report along with interest @ 18%. In his letter dated 18.02.2019 he has also stated that the cheques have been sent to all the buyers along with the interest who have made full payment for their flat as on 31.08.2018. He also enclosed copies of the letters written to the flat buyers along with the copies of the cheque. It was also submitted that to all those buyers whose instalments were pending, letters have been issued to the effect that the ITC as per the DGAP’s calculation is being credited into their ledgers. He has also intimated that if any further benefit of ITC would be available to him it would be passed on at the time of possession of the flats. It has also been submitted that he had instructed his bank to take necessary action and cheques will be released as and when the bank NOC is issued to the buyers or to the Respondent.

17. On 18.02.2019 the Respondent further submitted that in respect of 188 home buyers of residential units out of the total profiteered amount of Rs. 42,30,691 an amount of Rs. 18.19,582 was passed on and the balance amount of Rs. 24,11,109 along with interest of Rs. 2,03,716 (total Rs. 26,14.825) had been paid through cheques which were filed by him as evidence. He also promised to pay all the 13 buyers of commercial units the entire profiteered amount of Rs. 3,01,690. In respect of 177 home buyers the Respondent stated that since the balance instalments were pending from these buyers the profiteered amount for each one of them will be adjusted against their pending instalments. In this regard he also produced letters to the effect that the amount will be adjusted against the payments due which had been sent to all these 177 home buyers by him. On 19.02.2019 the Respondent had sent details of the payments of the profiteered amount through various modes. Further on 25.02.2019 the Respondent has submitted a letter giving the breakup of payments made through various modes along with the Annexures.

18. We have carefully examined the DGAP’s report and written submission by both the Applicants and the Respondent placed on record and find that following issues are to be settled in the present proceedings:-

I. Whether there was reduction in the rate of tax on the service in question w.e.f. 01.07.2017 and w.e.f. 25.01.2019?

II. Whether there was any net additional benefit of ITC?

III. Whether there was any violation of the provisions of Section 171 of the CGST Act, 2017, by not passing on the benefits by the Respondent?

19. Rule 127 of the CGST Rules. 2017 reads as under:-

“It shall be the duty of the Authority-

(i) to determine whether any reduction in the rate of tax on

any supply of goods or services or the benefit of input tax credit has been passed on to the recipient by way of commensurate reduction in prices;

(ii) to identify the registered person who has not passed on the benefit of reduction in the rate of tax on supply of goods or services or the benefit of input tax credit to the recipient by way of commensurate reduction in prices;

(iii) to order;

(a) reduction in prices;

(b) return to the recipient, an amount equivalent to the amount not passed on by way of commensurate reduction in prices along with interest at the rate of eighteen percent. from the date of collection of the higher amount till the date of the return of such amount or recovery of the amount not returned. as the case may be, in case the eligible person does not claim return of the amount or is not identifiable, and depositing the same in the Fund referred to in section 57;

(c) imposition of penalty as specified in the Act; and

(d) cancellation of registration under the Act.

20. Accordingly, the Authority is to examine whether there has been any benefit of reduction in the rate of tax or ITC that needs to be passed on to the recipients by way of commensurate reduction in prices. From the various documents submitted by the Respondent it is apparent that the Respondent has constructed 852 units out of which 816 are residential and 36 are commercial units. The total saleable carpet area is 3,96,950 sq. ft.. out of which 3,81,640 sq. ft. is for the residential units while 15,310 sq. ft. is for the commercial units. Out of the 3,81,640 sq. ft. area of the residential units the Respondent has sold carpet area equivalent to 3,26,879.36 sq. ft., while out of 15,310 sq. ft. of the commercial units he has sold 6,294 sq. ft. For these sold units he has collected an amount of Rs. 46,73,82,690 on residential units and Rs. 94,84,715 on the commercial units thus a total amount of Rs. 47,68.67,405 after introduction of GST has been collected by him.

21. In the present case as has been noted by the DGAP the Respondent has availed benefit of additional ITC of 6.49% (post GST) as compared to 3.65% (pre GST) as can be seen from the table given below. Based on the data and the documents filed by the Respondent, this percentage has been rightly arrived at by the DGAP by taking into account the benefit of credit available during pre GST (April 2016 to June 2017) to the taxable turnover received during the said period. Similarly for the post GST period (01.07.2017 to 31.08.2018) the percentage of ITC has been arrived at by taking into account the credit available as against the taxable turnover received during the same period. Based on the above analysis it is clear that the Respondent had benefit of ITC of Rs. 1,59 38 195 (3.6%) in pre GST when compared to Rs. 3,09,70.006 (6.49%) in the post GST period thus providing him the net benefit of ITC of 2.84%:-

22. It is also evident that the Central Government had levied 18% GST (effective rate was 12% on account of 1/3rdabatement on the land value) on construction service vide Notification No. 11/2017- Central Tax (Rate) dated 28.06.2017. The effective GST rate of construction service in the case of affordable and low cost housing was further reduced from 12% to 8% vide Notification No. 1/2018-Central tax (Rate) dated 25.01.2018. Accordingly the profiteered amount has to be broken into two parts one for the period w.e.f. 01.07.2017 to 24.01.2018 where the effective rate of GST was 12% and for the period between 25.01.2018 to 31.08.2018 when the effective GST rate was 8% for affordable housing. Therefore taking into account 2.84% net benefit of additional ITC and 12% of GST this Authority is in agreement with the DGAP’s calculation as mentioned in Annexure 21 of his Report in which details of ITC benefit to be passed on by the Respondent have been calculated. The DGAP has also correctly calculated the profiteered amount as Rs. 65,63,109 from all the buyers for the period w.e.f. 01.07.2017 to 24.01.2018 and an amount of Rs. 82,97,765 for the period between 25.01.2018 to 31.08.2018 taking into account the GST effective rate of 8% and net benefit of ITC of 2.84%. Thus the Respondent has profiteered total amount of Rs. 1,48,60,875 for the period from 01.07.2017 to 31.08.2018 in respect of all the 651 residential units and 13 commercial units. The above calculations of the profiteered amount has been duly admitted to be correct by the Respondent and he has willingly accepted to pass on the benefit of additional ITC which had become due to him after coming into force of the ITC.

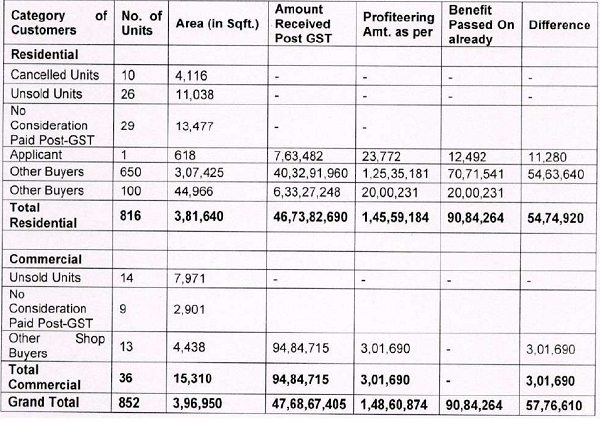

23. From the documents placed on record and the DGAP’s report it is evident that the Respondent has sold 780 units out of 816 residential units, out of which for 29 units there was no consideration paid after introduction of GST, hence the profiteered amount has to be calculated only for 751 units which have been sold and consideration received. Out of these 751 home buyers the DGAP has admitted that for 100 buyers the entire profiteered amount has already been paid. Hence in respect of 651 units as has been shown in the table below the profiteered amount comes to Rs. 1,45,59,184 which includes an amount of Rs. 23,772 for the Applicant No. 1 and Rs. 1,45,35,412 for all the other 650 home buyers. It has also been verified by the DGAP that in the case of the above Applicant, the Respondent has already paid an amount of Rs. 12,492, out of the profiteered amount of Rs. 23,772 hence the balance amount of Rs. 11,280 is to be paid. In the case of the balance 650 buyers, an amount of Rs. 70,71,541 has already been paid and balance amount of Rs. 54,63,640 is required to be paid. With regard to the commercial units only 13 units out of 36 units have been sold and an amount of Rs. 3,01,690 has been profiteered. Thus a total amount of Rs. 3,01,690 has to be paid to all the buyers of these commercial units. Accordingly out of total profiteered amount of Rs. 1,48,60,874 an amount of Rs. 90,84,264 has already been passed on as is evident from Annexure 17 of the DGAP’s Report where intimations have been filed by the Respondent stating the details of the payments regarding ITC benefit paid to their buyers. The balance amount of Rs. 57,76,610 is to be passed on to the identified buyers as per the following table:-

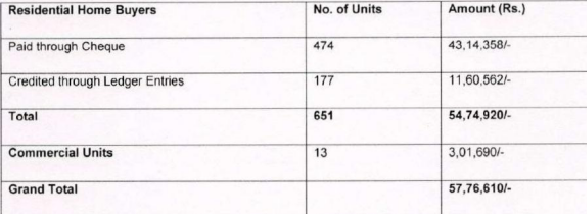

24. In view of the above facts this Authority under Rule 133 (3) (a) of the CGST Rules, 2017 orders that the Respondent shall reduce the price to be realized from the buyers of the flats commensurate with the benefit of ITC received by him as has been detailed above. Since the present investigation is only up to 31.08.2018 any benefit of ITC which accrues subsequently shall also be passed on to the buyers by the Respondent as and when the remaining residential/commercial units are sold. The Respondent’s Annexures dated 19.02.2019 and 25.02.2019 which comprise of the details of payments made through various modes are taken on record. As per this Annexure the Respondent has paid to the Applicant No. 1 and 473 other home buyers the entire profiteered amount through cheques as has been shown in the Annexures. The Respondent has also stated that to 177 home buyers the profiteered amount has been passed on through the credit notes and letters to this effect have been sent to all these home buyers. The Respondent has also submitted that in respect of the 13 commercial units where an amount of Rs. 3,01,690 has to be paid, he has credited the same into their accounts. Needless to mention that all such refunds adjustments shall be done by paying interest @ 18% from the date of the receipt of the amount by the Respondent from the buyers till the date the due amount is refunded/adjusted The details of payment of balance profiteered amount of Rs. 57,76,610 are shown below:-

25. It is evident from the above that the Respondent has denied benefit of ITC to the buyers of the flats being constructed by him under the above Policy in contravention of the provisions of Section 171 (1) of the CGST Act, 2017 and has thus realized more price from them than he was entitled to collect and has also compelled them to pay more GST than that they were required to pay by issuing incorrect tax invoices and hence he has committed an offence under section 122 (1) (i) of the CGST Act, 2017 and therefore, he is liable for imposition of penalty. Accordingly, a Show Cause Notice be issued to him directing him to explain why the penalty prescribed under Section 122 of the above Act read with rule 133 (3) (d) of the CGST Rules, 2017 should not be imposed on him.

26. Further the Authority as per Rule 136 of the CGST Rules 2017 directs the Commissioners of CGST/SGST Haryana to monitor this order under the supervision of the DGAP by ensuring that the amount profiteered by the Respondent as ordered by the Authority is passed on to all the buyers. A report in compliance of this order shall be submitted to this Authority by the commissioner CGST/SGST with in a period of 3 months from the date or receipt of this order.

27. A copy each of this order be supplied to the Applicants, the Respondent, Commissioners CGST /SGST as well as Principal Secretary (Town & Planning) Government of Haryana for necessary action. File be consigned after completion.

OFFHAND

“19. Rule 127 of the CGST Rules. 2017 reads as under:-

“It shall be the duty of the Authority- ….”

That seems to SAY IT ALL, the BUYER needs to know, to take on, if not done so already !