Brief Background of Input Tax Credit and it’s provision

“Input Tax” in relation to a registered person, means the central tax, State tax, integrated tax or Union territory tax charged on any supply of goods or services or both and includes

1. the integrated goods and services tax charged on import of goods;

2. the tax payable under the provisions of sub-sections (3) and (4) of section 9;

3. the tax payable under the provisions of sub-sections (3) and (4) of section 5 of the Integrated Goods and Services Tax Act;

4. the tax payable under the provisions of sub-sections (3) and (4) of section 9 of the respective State Goods and Services Tax Act; or

5. the tax payable under the provisions of sub-sections (3) and (4) of section 7 of the Union Territory Goods and Services Tax Act, but does not include the tax paid under the composition levy;

Once the above analogy is met, next comes the provision of set off of ITC, section 49, 49A, 49B and new Rule 88A deals with set off rules which are explained in detail below with version 1, version 2 and version 3

Version 1 of old provision

Utilisation of Input Tax Credit under old proviso 49 (Version 1)

In version 1 of set off rules read with section 49, it was clear that ITC on IGST shall be used first used against ITC, then against Net CGST tax payable and balance against net SGST tax payable

Version 2 of old provision

With effect from 01/02/2019, CBIC issued a notification/clarification against usage of Input tax Credit and introduced section 49A and 49B which is envisaged below

Section 49A:-

Notwithstanding anything contained in section 49, the input tax credit on account of central tax, State tax or Union territory tax shall be utilised towards payment of integrated tax, central tax, State tax or Union territory tax, as the case may be, only after the input tax credit available on account of integrated tax has first been utilised fully towards such payment.

Section 49B:-

Notwithstanding anything contained in this Chapter and subject to the provisions of clause (e) and clause (f) of sub-section (5) of section 49, the Government may, on the recommendations of the Council, prescribe the order and manner of utilisation of the input tax credit on account of integrated tax, central tax, State tax or Union territory tax, as the case may be, towards payment of any such tax.”.

Referring to the above version 2 of provision 49A and 49B the set off rules were drastically changed and industries were left in dark which had a impact on cash outflow and arising working capital crunch and blockage of funds due to draconian provision

Version 2 of Set off provision is carved out below

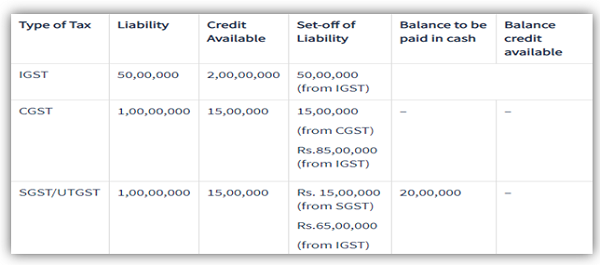

Utilisation of Input Tax Credit under new proviso 49A & 49 B (Version 2)

Referring the above version 1 and version 2 of example reader should have understood that, earlier IGST ITC could be utilised against net tax payable of C/S GST, but the amended provision envisage that

1. Input ITC shall be first used against IGST

2. Balance IGST ITC shall be used to set off “GROSS OUTPUT TAX LIABILITY OF CGST” in above example 1 crore shall be set off before availing ITC of CGST

3. BALANCE if any IGST ITC shall be utilised against State Tax

From the above example it is clear that ITC on CGST get’s accumulated and SGST at any cost need to be discharged which effects the working capital of a “Business Entity” as well as “Registered Person”

Version 3 of current provision[1]

The new order of ITC utilization, rule 88A is brought vide Notification No. 16/2019, dated 29-3-2019. This may bring some relief to the business community, which has anticipated increase in there working capital requirements due to blockage of credit by the amendment made to section 49 vide First Amendment Act made to effective from 1st FEB, 2019.

Per current regime of Set Off proviso

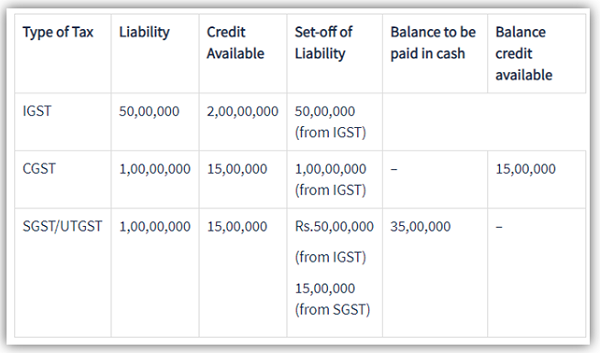

Vide circular no. 98/17/2019-GST dated April 23, 2019, CBIC has clarified that order of utilization of input tax credit wherein ITC available on account of IGST shall be first utilized only towards payment of IGST and if any amount remains, it may be utilized towards the payment of CGST or SGST/UTGST, in any order and in any proportion at the option of a registered person.

The following illustration would further amplify the impact of newly inserted rule 88A of the CGST Rules:

Illustration:

Amount of Input tax Credit available and output liability under different tax heads

Can the IGST credit after utilization of IGST liability be utilized partly from CGST or SGST?

As the rule 88A provides that-“integrated tax shall first be utilized towards payment of integrated tax, and the amount remaining, if any, may be utilized towards the payment of Central tax and State tax or Union territory tax, as the case may be, in any order” but it does not mention that balance IGST can be utilized partly from CGST or SGST. It does not prohibit as well.

However even after referring supra version’s and in the said circular department has stated

Presently, the common portal supports the order of utilization of input tax credit in accordance with the provisions before implementation of the provisions of the CGST (Amendment) Act i.e. pre-insertion of Section 49A and Section 49B of the CGST Act. Therefore, till the new order of utilization as per newly inserted Rule 88A of the CGST Rules is implemented on the common portal, taxpayers may continue to utilize their input tax credit as per the functionality available on the common portal.

Concluding word:

So the concluding words is still SGST need to be paid at a minimal value but the accumulation of CGST will be a relief for the industry.

Wishing you a happy reading!!

[1] https://taxguru.in/goods-and-service-tax/cbic-clarifies-manner-utilization-gst-input-tax-credit.html

shall i utilise igst output tax from sgst input tax credit

I am IGST Credit of RS.100, CGST Credit of Rs. 200 and SGST Credit of Rs. 200, and I am having Liability of IGST- NIL, CGST Rs. 500 and SGST RS. 500. Advise me how to setoff under new ITC Rule.

Conclusions of everything very well article sir.

You nailed it the differentiation of each amendment taken in due course… very informative and nicely presented