Shushant Singhal

Broken Input tax credit chain across India majorly calls for the tax reform “GST”. In the pre GST scenario, cascading of tax remained significant due to non availability of ITC at various stages. Like ITC of CST, Entry Tax, Luxury Tax etc never been available for payment of other taxes. Under GST law, ITC Facility is available across the supply chain in all intra-state and inter-state transactions. Lesser the cascading effect, better the taxation system. Let’s understand types of taxes under GST first.

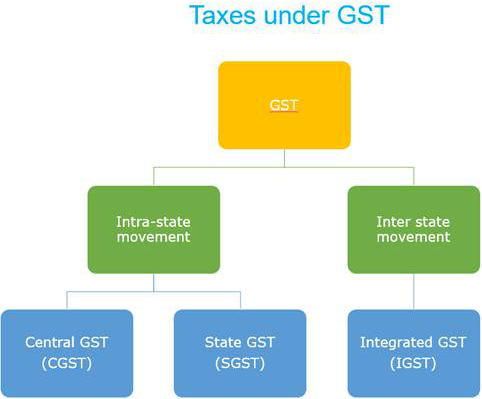

There are 3 types of taxes under GST

SGST – State GST

CGST – Centre GST

IGST – Integrated GST

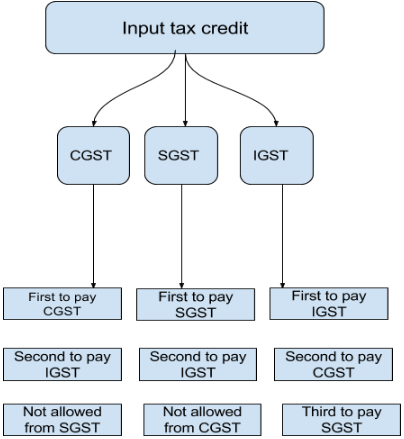

Now let’s understand how INPUT CREDIT works under GST

Input Tax Credit

- Input of CGST—————à Firstly Set off against CGST——————–à Balance against IGST

- Input of UTGST————-à Firstly Set off against UTGST——————à Balance against IGST

- Input of SGST————–à Firstly Set off against SGST———————-à Balance against IGST

- Input of IGST————–à Firstly Set off against IGST———à Balance against CGST———-à Balance against SGST/UTGST

Input of Business is divided into three types which is being used procured for the purpose of use or intended to be used in the course of business or furtherance of business.

- Input Services- This term denotes any service used by a supplier during his business to generate supplies outwards.

- Capital Goods- This term means the value of which is capitalised in the books of account of the person claiming the input tax credit and which are used or intended to be used in the course or furtherance of business

- Input Goods other than Capital Goods- Under GST law, the term input denotes goods except capital goods used by a supplier during his business to make outward supplies

Pre requisite for claiming ITC

A registered person will be eligible to claim Input Tax Credit (ITC) on fulfilment of the following conditions:

1. Possession of a tax invoice or debit note or bill of entry or other document evidencing payment

2. Receipt of goods and/or services

3. Goods delivered by supplier to other person on the direction of registered person against a document of transfer of title of goods

4. Furnishing of a return

5. Where goods are received in lots or instalments ITC will be allowed to be availed when the last lot or instalment is received.

6. Full credit on capital goods will be allowed in the year of purchase itself.

Limitation on availing ITC

No ITC beyond September of the following FY to which invoice pertains or date of filing of annual return, whichever is earlier.

No Input Tax credit on Advance Payments

To claim ITC, you must be in possession of a valid document may be invoice , debit note etc. and you (including your job worker or direct recipient etc. ) must have actually received the goods or services[Section 16(2)]. Where the goods against an invoice are received in lots or instalments, the registered person shall be entitled to take credit upon receipt of the last lot or instalment. [First Proviso to section 16(2)]. So it is clear from the above provisions that ITC ON ADVANCE PAYMENTS shall not be available.

To claim ITC, you must be in possession of a valid document may be invoice , debit note etc. and you (including your job worker or direct recipient etc. ) must have actually received the goods or services[Section 16(2)]. Where the goods against an invoice are received in lots or instalments, the registered person shall be entitled to take credit upon receipt of the last lot or instalment. [First Proviso to section 16(2)]. So it is clear from the above provisions that ITC ON ADVANCE PAYMENTS shall not be available.

Input Tax credit on supplies in regard of which payment is not made within 180 days

Where a recipient fails to pay to the supplier the amount towards the value of supply along with tax payable thereon within a period of 180 days from the date of issue of invoice by the supplier, an amount equal to the input tax credit availed by the recipient shall be added to his output tax liability, along with interest thereon. Registered person shall furnish the details of such supply and the amount of input tax credit availed of in FORM GSTR-2 for the month immediately following the period of one hundred and eighty days from the date of issue of invoice. [Rule 2(1)]. The registered person shall be liable to pay interest at the rate notified under sub-section (1) of section 50 for the period starting from the date of availing credit on such supplies till the date when the amount added to the output tax liability in Form GSTR-2 is paid

Items on which credit is not allowed

1. Motor vehicles and conveyances except the specified circumstances given below:-

- Used for making further taxable supply of vehicles or conveyance

- Used for making further taxable supply of transportation of passengers

- Used for making further taxable supply of imparting training on driving, flying navigating.

- Used for providing transportation of goods

2. Food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery but if the goods and/or services are taken to deliver the same category of services or as a part of a composite supply, credit will be available.

3. Sale of membership in a club, health, fitness centre.

4. Rent-a-cab, health insurance and life insurance except the following:

- Government makes it obligatory for employers to provide it to its employees

5. Travel benefits extended to employees on vacation such as leave or home travel concession.

6. Works contract service for construction of an immovable property (except plant & machinery or for providing further supply of works contract service)

7. Goods and/or services for construction of an immovable property whether to be used for personal or business use

8. Goods and/or services where tax have been paid under composition scheme

9. Goods and/or services used for personal use/ exempt supplies

10. Goods or services or both received by a non-resident taxable person except for any of the goods imported by him.

11. Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples

12. ITC will not be available in the case of any tax paid due to non payment or short tax payment, excessive refund or ITC utilized or availed by the reason of fraud or willful misstatements or suppression of facts or confiscation and seizure of goods.

I am doing manufacturing of goods and Job work. Can I utilize my input credit of purchases in output of Job work.

Succinct & informative article

Will you please make me clear on “when, where and how the closing stock as on 30/6/17’s excise refund claims? Will you please inform me the website and format to be uploaded?