Case Law Details

Sh. Kumar Gandhary Vs. KRBL Limited (National Anti-Profiteering Authority)

We have carefully heard the Respondent and also perused the material placed on the record and it is revealed that the “India Gate Basmati Rice” sold by the Respondent was not liable for tax before the implementation of the GST and after coming into force of the CGST Act, 2017 it was levied GST @ 5% w.e.f. 22.09.2017. The Respondent was also made eligible to avail ITC w.e.f. the above date. However, the ITC claimed by the Respondent was not sufficient to meet his output tax liability and he had to pay the balance amount of tax in cash as is evident from the perusal of the table prepared by the DGSG. It is also apparent from the returns filed by the respondent for the months of September, 2017, October, 2017 and November, 2017 that the ITC available to him as a percentage of the total value of taxable supplies was between 2.69% to 3% whereas the GST on the outward supply of his product was 5% which was not sufficient to discharge his tax liability. Moreover in this case the rate of tax has been increased from 0% to 5% instead of reduction in the same. Therefore, there appears to be no reason for treating the price fixed by the Respondent as violation of the provisions of the Anti-Profiteering clause.

7. It is also revealed from the perusal of the tax invoices submitted by the Respondent that there was an increase in the purchase price of paddy in the year 2017 as compared to its price during the year 2016 which constitutes major part of the cost of the above product. It is further revealed from the record that the Respondent had increased the MRP of his product from Rs. 540/- to Rs. 585/- which constituted increase of 8.33% keeping in view the increase in the purchase price. Therefore, due to the imposition of the GST on the above product as well as the increase in the purchase price of the paddy there does not appear to be denial of benefit of ITC as has been alleged by the Applicant as there has been no net benefit of ITC available to the Respondent which could be passed on to the consumers. Accordingly there is no substance in the application filed by the above Applicant as there is no violation of the provisions of Section 171 of the CGST Act, 2017 and hence the same is dismissed.

FULL TEXT OF THE ORDER IS AS FOLLOWS:-

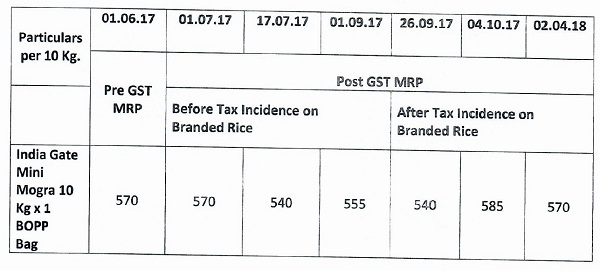

1. The brief facts of this case are that the above Applicant vide his application dated 27.11.2017 (Annexure-l), sent through e-mail had intimated that the benefit of reduction in the rate of tax on “India Gate Basmati Rice” had not been passed on to the consumers as it’s Maximum Retail Price (MRP) had been increased, and hence margin of profit had also been increased by the above Respondent. He had also attached images of the details printed on the 10 Kg. package of “India Gate Basmati Rice” (Mini Mogra) packed in the months of August, 2017 and October, 2017 showing the printed price of Rs. 540/- & Rs. 585/-respectively.

2. The above application was examined by the Standing Committee on Anti-Profiteering on 13.12.2017 and forwarded to the Director General Safeguards (DGSG) for detailed investigation on 12.2017.

3. The DGSG had issued notice to the above Respondent and after examining the record had reported that in this case the tax rate on the packed Basmati Rice carrying registered brand name of “India Gate Basmati Rice” had been increased from Nil to 5% after the implementation of the GST w.e.f. 01.07.2017, due to which input tax credit (ITC) had become available to the above Respondent. He had also reported that whether the benefit of ITC had been passed on to the consumers, had to be examined in case there was any net benefit of ITC to the Respondent after the GST liability on the outward taxable supplies had been discharged by him and if the ITC was available with him it was to be passed on to the consumers in terms of Section 171 of the CGST Act, 2017. He had further reported that the “India Gate” brand name was not registered by the Respondent and hence he was not paying GST on the outward supply of Basmati Rice and this product had been made taxable vide Notification No. 28/2017-Central Tax (Rate), dated 22.09.2017 (Annexure-II) since then the Respondent was paying GST @ 5%.

4. The DGSG had also intimated that the GSTR-3B returns of the Respondent pertaining to Haryana for the months of September, 2017 (Annexure-III), October, 2017 (Annexure-IV) and November, 2017 (Annexure-V) had been examined and it was found that the ITC available as a percentage of the total value of taxable supplies during these three months varied between 2.89% to 3% however, as the GST rate on taxable outward supply was 5%, the ITC available was insufficient to discharge the GST liability and thus, the balance amount of GST had been paid in cash during the above period and since the ITC available was less than the GST liability on the outward supplies, there was no net benefit of ITC which could had been passed on to the consumers and therefore there was no violation of the provisions of section 171 of above Act. He had also given details of the calculation of the ITC which was available to the above Respondent as has been shown in the table given below:

5. The above report was considered by the Authority in its sitting held on 20.03.2018 and it was decided to hear the Applicant as well as the Respondent on 11.04.2018. Sh. Anoop Aggarwal General Manager and Ms. Medini Aggarwal appeared for the Respondent on the given date however the Applicant did not put an appearance. After hearing the representatives of Respondent they were directed to supply further clarifications which were submitted by them on 17.04.2018 and it was contended that the GST rate on outward supply of their product was 5% and the ITC available to discharge the GST liability was not sufficient and the balance amount of GST was paid by the Respondent in cash therefore, there was no benefit of ITC which could be passed on to the consumers. They had further submitted that the prices of ‘rice’ being an agricultural product, changed frequently because of the market forces and the other cost factors and were not solely dependent on the tax rates. They had also contended that the price of paddy had increased by more than 30% in the year 2017 as compared to the year 2016 which constituted 75% of total cost of production, however, because of stiff competition in the market they had not passed on the total cost burden to the consumers and had increased the price of their product by 8% only from Rs. 540/- to Rs. 5841- in spite of increase in the raw material costs by more than 30%. They had further contended that the average price of paddy was Rs. 260/- per 10 Kg. in the year 2016 while it was Rs. 330/- per Kg. in the year 2017 due to which there was increase in the MRP and no other factor had influenced the price of their product. They had also produced the copies of the invoices of paddy purchases in their support. They had also submitted the following table to support their case:-

6. We have carefully heard the Respondent and also perused the material placed on the record and it is revealed that the “India Gate Basmati Rice” sold by the Respondent was not liable for tax before the implementation of the GST and after coming into force of the CGST Act, 2017 it was levied GST @ 5% w.e.f. 22.09.2017. The Respondent was also made eligible to avail ITC w.e.f. the above date. However, the ITC claimed by the Respondent was not sufficient to meet his output tax liability and he had to pay the balance amount of tax in cash as is evident from the perusal of the table prepared by the DGSG. It is also apparent from the returns filed by the respondent for the months of September, 2017, October, 2017 and November, 2017 that the ITC available to him as a percentage of the total value of taxable supplies was between 2.69% to 3% whereas the GST on the outward supply of his product was 5% which was not sufficient to discharge his tax liability. Moreover in this case the rate of tax has been increased from 0% to 5% instead of reduction in the same. Therefore, there appears to be no reason for treating the price fixed by the Respondent as violation of the provisions of the Anti-Profiteering clause.

7. It is also revealed from the perusal of the tax invoices submitted by the Respondent that there was an increase in the purchase price of paddy in the year 2017 as compared to its price during the year 2016 which constitutes major part of the cost of the above product. It is further revealed from the record that the Respondent had increased the MRP of his product from Rs. 540/- to Rs. 585/- which constituted increase of 8.33% keeping in view the increase in the purchase price. Therefore, due to the imposition of the GST on the above product as well as the increase in the purchase price of the paddy there does not appear to be denial of benefit of ITC as has been alleged by the Applicant as there has been no net benefit of ITC available to the Respondent which could be passed on to the consumers. Accordingly there is no substance in the application filed by the above Applicant as there is no violation of the provisions of Section 171 of the CGST Act, 2017 and hence the same is dismissed. A copy of this order be supplied to the Applicant and the Respondent free of cost. A copy be also supplied to the DGSG. File be consigned after completion.

While the increase of MRP due to increase in the price of paddy is understandable, ITC credit of 2.89-3% should have enabled reduction of MRP. Output Tax at 5% being higher than ITC credit of 2.89-3% does not justify MRP increase. It is only a cash effect and at the most, the MRP could have been increased by the cost of capital for funding the GST Outflow of 2-2.11%. Am I missing something here?