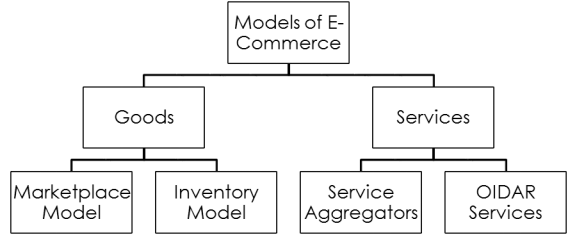

E-commerce is a very wide term. It includes in its ambit all the different models in which the business is carried out electronically.

MARKETPLACE MODEL/FULFILMENT MODEL

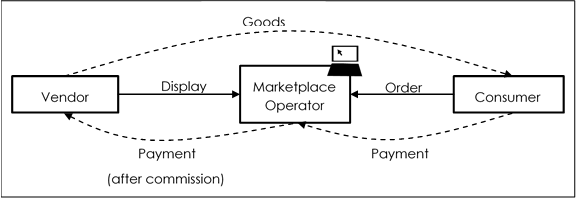

The website / application acts as a platform or a facility for the buyers and sellers. The goods are sold by third parties. The marketplace operator only processes the transactions and provides the platform where the product can be displayed by the seller and ordered by the buyer. In this model, the vendor earns profit whereas the operator earns a commission. Therefore, three parties are involved:

Common examples are Amazon, Flipkart and Ebay, though they also work on inventory model in a limited manner.

INVENTORY MODEL

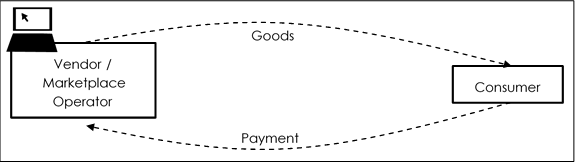

Here, the marketplace operator and the seller are not different parties. This means that the online platform is used by the operator to sell his own products. The inventory of such products is maintained by the operator itself. Therefore, only two parties are involved:

This is commonly seen as being followed by brands which want to sell their own products in an online mode.

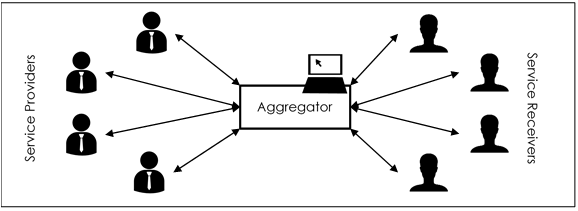

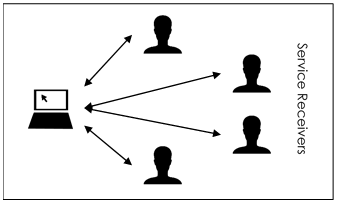

This is the latest developments in the field of e-commerce. It is similar to marketplace model. Aggregator is the person who owns an online platform or a facility in the form of a website or mobile application or any other mode. Such platform acts a facilitator in connecting the service providers and service recipients.

Common examples are Ola and Uber.

ONLINE INFORMATION AND DATABASE ACCESS OR RETRIEVAL SERVICES

This has been in existence for many years now. This simply means making some information or data available electronically on a website or application, which can be accessed on making payment.

Common examples are e-books, music, movies and advertising.

In GST, “electronic commerce” has been defined to mean the supply of goods or services or both, including digital products over digital or electronic network.

The term “electronic commerce operator” has been defined to mean any person who owns, operates or manages digital or electronic facility or platform for electronic commerce. These definitions include each of the above discussed models.

Certain specific provisions have been introduced in GST for e-commerce.

SERVICE AGGREGATORS

It has been provided that notified categories of service aggregators shall be liable to pay tax on services provided through the aggregator.

This in effect means that the entire tax liability in case of service aggregator model of e-commerce shall have to be discharged by the aggregator, instead of the actual service provider. This will ensure that the tax is paid in full, and will also considerably reduce the administration hassles for government.

It has been further provided that in case such operator does not have a physical presence in the taxable territory (i.e. India except Jammu and Kashmir), any person representing such operator for any purpose in the taxable territory shall be liable.

Further, where the electronic commerce operator does not have such representative, it shall appoint a person in the taxable territory for the purpose.

Such provisions have been made to ensure that aggregators which operate from other countries do not escape tax.

It may be noted here that two types of services are involved in the service aggregator model – one is the service rendered by various service providers to the customers through the aggregator, other is the service rendered by the aggregator by way of provision of platform or facility. The above discussed provision is with respect to the first kind of services. Needless to say, the aggregator shall also be liable for tax on its service as an aggregator.

COLLECTION OF TAX AT SOURCES

This provision is applicable to all electronic commerce operators where the consideration for the supply is collected by operator, except notified service aggregators (discussed above) and agents.

This provision is applicable to the e-commerce operators working under the marketplace model. The operator shall be liable to deduct tax at source (at a rate yet to be notified, but not exceeding one per cent) as and when it remits the payments received from the customers to the respective suppliers.

This will ensure that all the transactions are mapped and routed through the GST Network. Again, this will make administration easier and tax collection more efficient. But at the same time, the compliance requirements on part of the e-commerce operators are bound to increase. This is being taken as a blow by the e-commerce industry, which is still believed to be in its nascent stages.

ONLINE INFORMATION AND DATABASE ACCESS OR RETRIEVAL (OIDAR SERVICE)

Such services, shall include:

- Advertising on the internet

- Cloud services

- Provision of e-books, movie, music, software, other intangibles through telecommunications network or internet

- Providing data or information in electronic form through a computer network

- Digital data storage

- Online gaming

The above list is not exhaustive. It is only indicative of the kind of services included here.

As a general rule, the place of provision of such services shall be location of the recipient of services. However, the recipient shall be deemed to be located in the taxable territory, if any two of the following conditions are satisfied:

- Address given by the recipient through internet is in taxable territory

- The card which is used for settlement of payment has been issued in taxable territory

- Billing address of the recipient is in taxable territory

- IP address of the device used by the recipient is in taxable territory

- Bank in which the bank account used for payment is maintained is in taxable territory

- Country code of the SIM card used by the recipient is in taxable territory

- Location of the fixed landline through which service is received by the recipient is in taxable territory.

In case OIDAR services are supplied by a person located in non-taxable territory to a non-taxable online recipient (discussed below), the supplier of services shall be liable for payment of tax. He shall take a single registration under the Simplified Registration Scheme (yet to be notified).

A non-taxable online recipient means any

- Government, local authority, governmental authority, an individual or any other person

- not registered and

- receiving OIDAR services

- in relation to any purpose other than commerce, industry or any other business or profession

- located in taxable territory.

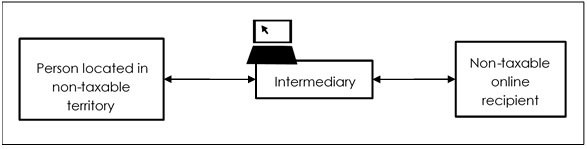

In case such services are rendered by person located in non-taxable territory to a non-taxable online recipient through an intermediary, it shall be deemed that such intermediary is a service recipient for the supplier located in non-taxable territory and a service provider to such non-taxable online recipient.

However, it shall not be deemed so, when such intermediary satisfies the following conditions:

- The invoice issued by the intermediary clearly identifies the service in question and its supplier in the non-taxable territory

- The intermediary does not collect or process payment in any manner, nor is responsible for the payment between the parties

- The intermediary involved in the supply does not authorize delivery

- General terms and conditions of the supply are not set by the intermediary.

REGISTRATION

Every electronic commerce operator, and every person supplying goods and services through electronic commerce operator (except service providers rendering services through service aggregators notified as discussed above) shall not be eligible for threshold exemption.

Author Bio

I am acc=ting as a mediator between two foreign countries. I am running a marketplace E-commerce Model Platform In India in which only Foreign Sellers and Buyers can register and trade and the Payment is processed through the portal I.e. First received by me(My Portal) from the Non Resident Foreign Buyer in Convertible Forex In INR and then it is processed through me and then Paid to the ultimate seller in his Domestic currency.

What will be the GST Implications on me?

What is Taxable Event for me and Taxable Value ?

I am running a marketplace E-commerce Model Platform In InDia in which only Foreign Sellers and Buyers can register and trade and the Payment is processed through the portal I.e. First received by me(My Portal) from the Non Resident Foreign Buyer in Convertible Forex In INR and then it is processed through me and then Paid to the ultimate seller in his Domestic currency.

What will be the GST Implications on me(I.e. Portal)?

What is Taxable Event for me and Taxable Value ?

Please Answer my query with provisions of GST Law ?

Well Structured with flow charts to easily understand

Madam

well prepared.

VERY INFORMATAORY