Byrapuneni Venkata Krishna Rao

The article ‘Impact of Service Tax on Cab arrangements in a Hotel/Restaurant’ published on 08th March, 2016 (i.e., https://taxguru.in/service-tax/impact-service-tax-cab-arrangements-hotelrestaurant.html) is modified in terms of GST and re-published as ‘Impact of GST on Cab arrangements in a Hotel/Restaurant’

The article ‘Impact of Service Tax on Cab arrangements in a Hotel/Restaurant’ published on 08th March, 2016 (i.e., https://taxguru.in/service-tax/impact-service-tax-cab-arrangements-hotelrestaurant.html) is modified in terms of GST and re-published as ‘Impact of GST on Cab arrangements in a Hotel/Restaurant’

In India, the Hotel & Restaurant Approval & Classification Committee (HRACC), a division under Ministry of Tourism is entrusted with the activity of classification of the Hotels into either Star Category Hotels (5 Star Deluxe, 5 Star, 4 Star, 3 Star, 2 Star & 1 Star) or Heritage Category Hotels (Heritage Grand, Heritage Classic & Heritage Basic) by inspecting & assessing the hotels based on the facilities and services offered.

As per ‘Guidelines for Classification of Hotels’ issued by Ministry of Tourism (Hotel & Restaurant Division), ‘Paid Transportation on call’ is compulsory in hotels of 3 Star & above and Heritage Hotels. However, in order to provide the customer a greater luxury and to stay ahead in the competition, even hotels below 3 star rating are also providing transportation on call that is facility of making the cab available on call.

Here, in this article I would like to discuss the different options available for a Hotel to provide cab facilities to their guests and respective implications under Goods and Services Tax law.

Different options available to a Hotel for providing Cab services:

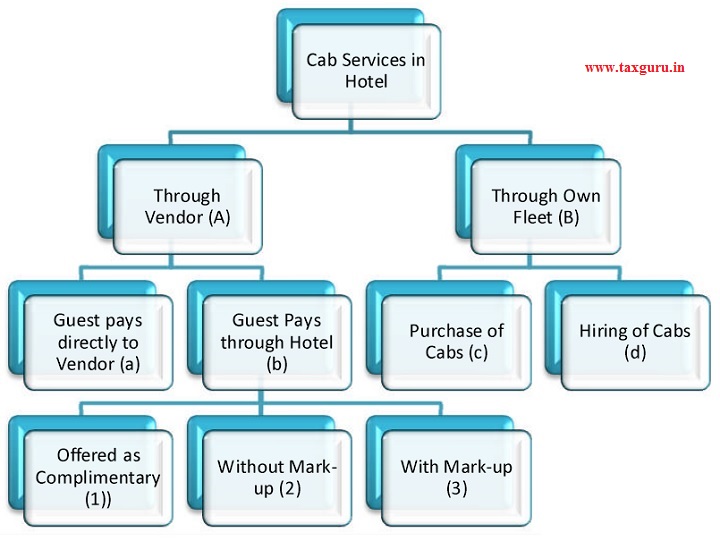

Any Star Hotel and other establishment alike Hotel business may have an option to choose one of the following ways for providing cab services to their Guests.

From the above picture, it is clearly evident the various alternatives available for the hotel for provision of cab to their guests. The hotel may appoint a vendor through which such services are provided or the hotel may maintain own fleet of vehicles either by purchasing or hiring of such cabs. Now that we have understood the various alternatives available, we shall proceed with discussion regarding the implications under Goods and Services tax law.

A. Through Vendor:

In this model, the hotel/restaurant appoints a vendor who sits at the reception for facilitating the booking of cab to the customers. It may also happen in certain cases, the hotel/restaurant books the cab using the online facility of the vendor. It is important to note that the hotel/restaurant only facilitates the provision of booking the cab but does not have any ownership/possession of such cabs.

There might be two instances regarding the payment of cab charges by the guest. In some hotels/restaurants, the guest pays the cab charges directly to the vendor. In other cases, it might happen that, the hotel/restaurant recovers such cab charges through their bill and pays the same at actuals to the vendor. Now, let us see the implications under GST under the two said instances.

a) Guest pays directly to Vendor:

In this methodology, as stated above, hotel/restaurant does not charge any amount in their billings made to the guest (i.e., just acts as a facilitator between vendor and Guest). And also, hotel/restaurant shall not charge any amount for such facilitation service between vendor and guest. The guest pays cab charges directly to the vendor.

Implications under GST on such model:

Since there is no revenue generated by such facilitation provided by the hotel/restaurant, there shall not be any implications under GST for the hotel/restaurant. However, if the hotel/restaurant is charging any rentals from the vendor for the space provided at the reception, the same shall be subjected to GST under ‘supply of service’ as per Part (2) of Schedule II of the Act.

b) Guest pays through Hotel:

In this methodology, the hotel/restaurant provides the facility of on call booking and charges the guest towards the cab charges in the bill along with the accommodation services. Or it also might happen that the guest does not pay any specific amount towards cab services (in cases of complimentary services).

Implications under GST on such model:

In such a methodology, there might be different instances which require examination under GST laws. The hotel/restaurant might offer the facility of cab to the guest as complimentary (as a part of the package), or charge the actuals from the guest and pay the same to the vendor or pay to the vendor after deducting the commission/fee. Now, we shall proceed with the implications under GST for the instances mentioned above.

1) Offered as Complimentary:

It is the need of the hour for the hotels/restaurants to come up with various complimentary packages to attract the guests and stay ahead in the business. So, the hotel/restaurants might offer facility of pick and drop as part of the package taken by the guest. In such cases, there shall not be any specific consideration towards the cab services. However, the hotel/restaurant ends up paying to the vendor such cab charges.

Taxability:

In such methodology, since the hotel/restaurant is providing one or more services to the guest as a mixed supply, the taxability of the consideration shall be decided based upon the principles of interpretation as provided in Section 8 of the Central Goods and Services Act, 2017. Vide sub-section (74) of Section 2, if two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply then such supply is considered as Mixed and shall be treated as supply of that particular service which attracts the highest rate of tax. In the instant case, the accommodation service assumes the highest rate of GST and accordingly the rate of GST applicable to the accommodation service shall be applied on the entire consideration received from the guest.

Reverse Charge:

Further, the hotel/restaurant shall be subjected to GST on the expenses paid to the vendor under the reverse charge mechanism subject to the conditions specified under section 9(4) of the CGST Act, 2017.

However, it is worth noting that the hotel/restaurant can absolve from payment of GST under reverse charge mechanism, if such hotel/restaurant takes a stand that they receive the service from registered person.

2) Without Mark-Up:

In this methodology, the hotel/restaurant books the cab for the guest and collects the cab charges from the guest in addition to the accommodation bill. However, the hotel/restaurant shall reimburse the same to the vendor without charging or retaining any amount. It is only to facilitate the guest a single point of payment is being provided.

Taxability:

In such a methodology, the consideration for cab service shall be taxed at 5% of GST (if Renting of motorcar where the cost of fuel is included in the consideration charged from the service recipient) and Input Tax Credit shall not be available or at 18% of GST (if Renting of motorcar where the cost of fuel is not included in the consideration charged from the service recipient) and Input Tax Credit shall be available.

Reverse/Partial Charge:

Further, the hotel/restaurant shall be subjected to GST on the expenses paid to the vendor under the reverse charge mechanism subject to the conditions specified under section 9(4) of the CGST Act, 2017.

However, it is worth noting that the hotel/restaurant can absolve from payment of GST under reverse charge mechanism, if such hotel/restaurant takes a stand that they receive the service from registered person.

3) With Mark-Up:

In this methodology, the hotel/restaurant books the cab for the guest and collects the cab charges from the guest in addition to the accommodation bill. The hotel/restaurant shall charge an additional amount apart from what is required to be paid to the vendor from the guest for provision of service.

Taxability:

In such a methodology, the taxability shall be same as mentioned in without mark-Up.

Through Own Fleet:

In this model, the hotel/restaurant instead of sourcing cabs from a 3rd party, may maintain own fleet of vehicles either by purchase of motor vehicles or hiring the motor vehicles from 3rd party. Now, let us see the implications under GST under the two said instances.

c) Purchase of Motor Vehicles:

In this model, the hotel/restaurant purchases motor vehicles for provision of cab facility to their guest. The hotel/restaurant shall obtain registration under GST and file returns accordingly.

Taxability:

In such a methodology, the taxability shall be same as specified in ‘without mark-Up’.

d) Hiring of Motor Vehicles:

Under this model, the hotel/restaurant instead of purchasing the motor vehicles, opt for hiring of the same from 3rd party. The vendor shall leave the car at the disposal of the hotel/restaurant and collects periodical rentals from the later.

Taxability:

In such a methodology, the taxability shall be same as specified in ‘without mark-Up’.

(Author can be reached at venkatakrishna.byrapuneni@

If i am transporter who is giving service to a restaurant., How they can avail GST benefit., In RCM

Do the transport need to rise a tax invoice of 18% or not coz its states as follow.,

the hotel/restaurant can absolve from payment of GST under reverse charge mechanism, if such hotel/restaurant takes a stand that they receive the service from registered person.

Hi

I want to know that supposed to be as travel agent I purchased room on net 2000 (500 Markup) and I raise bill 2500 to my client. How much I pay the GST.

If I purchase a air ticket @ 5000 from local trading partner and I sold it 5200 (200 Markup) what would be the GST rate.

why can’t Govt may simplify GST in this transportation? The slogan ‘simplicity of GST’ is useless.

I would like to comment on case b point no 2:

Why isn’t it possible to consider it as a pure agent case??