There was great Euphoria, Enthusiasm & Excitement in Export Community when a flash news thrashed in the media after the 22nd meeting of GST Council on 6th October 2017 that recommended release of Refunds and other beneficial proposals for exporters as a boon for them and to normalize the working of exporters and to ensure the inflow of foreign exchange for the exchequer.

The prominent proposals are as under :

EXPORT REFUND

The phase wise refund will commence as below:

Refund of July– From 10.10.2017 the held-up refund of IGST paid on goods exported outside India in July would begin to be paid.

Refund of August– The August backlog would get cleared from 18.10.2017 onwards.

Other refunds– Refund of IGST paid on supplies to SEZs and of inputs taxes on exports under Bond/LUT, shall be processed expeditiously from 18.10.2017 as well.

Let us understand in this article whether this is a reality or simply a myth.

Before proceeding to analyze, first let us understand the Export & Refund Procedure.

Exports : Zero-Rated Supply: Eligible to Claim Refund

As per Sec 2(23) of IGST Act: “zero-rated supply” shall have the meaning assigned to it in section 16;

Sec 16. (1) of IGST Act : “zero rated supply” means any of the following supplies of goods or services or both, namely:––

(a) export of goods or services or both; or

(b) supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit

That means direct exports or supplies to SEZ Developer / SEZ Unit is treated as Zero Rated Supply and as per Sec 16. (3) of IGST Act :

A registered person making zero rated supply shall be eligible to claim refund under either of the following options, namely:––

a) he may supply goods or services or both under bond or Letter of Undertaking, subject to such conditions, safeguards and procedure as may be prescribed, without payment of integrated tax and claim refund of unutilised input tax credit; or

b) he may supply goods or services or both, subject to such conditions, safeguards and procedure as may be prescribed, on payment of integrated tax and claim refund of such tax paid on goods or services or both supplied,

in accordance with the provisions of section 54 of the Central Goods and Services Tax Act or the rules made thereunder.

That means on account of zero rating of supplies, the supplier will be entitled to claim input tax credit in respect of goods or services or both used for such supplies even though they might be non-taxable or even exempt supplies. Every person making claim of refund on account of zero rated supplies has two options. Either he can export under Bond/LUT and claim refund of accumulated Input Tax Credit or he may export on payment of integrated tax and claim refund of thereof as per the provisions of Section 54 of CGST Act, 2017.

As per Explanation to Sec 54 of CGST Act, “refund” includes refund of tax paid on zero-rated supplies of goods or services or both or on inputs or input services used in making such zero-rated supplies, or refund of tax on the supply of goods regarded as deemed exports, or refund of unutilized input tax credit as provided under sub-section (3).

Option – 1 : Export without Payment of Tax – Claim ITC Refund

Refund of 90% will be granted provisionally within seven days of acknowledgement of refund application. (Sec 54(6) & Rule 91(2))

Remaining 10% will be paid within a maximum period of 60 days from the date of receipt of application complete in all respects (Sec 54(7) of CGST Act)

As per Notification No. 13/2017 – Central Tax, 28th June, 2017, issued under Sec 56 of CGST Act, Interest @ 6% is payable if full refund is not granted within 60 days.

- Procedure of Export Under Option – 1:

- Procedure of Claiming ITC Refund under Option – 1:

- Option – 2 : Export on Payment of Tax – Claim IGST Refund

- Procedure of Claiming IGST Refund on Export under Option 2

- No Refund of Un-utilised Input Tax Credit in Certain Cases

- Myth – 1 : The claim and Sanctioning Procedure will be Completely Online and Time Bound – 90% of Refund shall be Granted within 7 Days

- Myth – 2 : Interest is Paid for Delayed Payment of Refund @ 6%

- Myth – 3 : IGST Refunds for Exports made in July 2017 start by 10.10.2017 – as Recommended GST Council in its meeting on 06-10-2017.

- Myth – 4: All Exporters are Cover under Auto Filling of Refund Applications (ie Shipping Bill is Treated as Application for Refund)

Page Contents

- Procedure of Export Under Option – 1:

- Procedure of Claiming ITC Refund under Option – 1:

- Option – 2 : Export on Payment of Tax – Claim IGST Refund

- Procedure of Claiming IGST Refund on Export under Option 2

- No Refund of Un-utilised Input Tax Credit in Certain Cases

- Myth – 1 : The claim and Sanctioning Procedure will be Completely Online and Time Bound – 90% of Refund shall be Granted within 7 Days

- Myth – 2 : Interest is Paid for Delayed Payment of Refund @ 6%

- Myth – 3 : IGST Refunds for Exports made in July 2017 start by 10.10.2017 – as Recommended GST Council in its meeting on 06-10-2017.

- Myth – 4: All Exporters are Cover under Auto Filling of Refund Applications (ie Shipping Bill is Treated as Application for Refund)

Procedure of Export Under Option – 1:

The detailed Procedures are prescribed in Rule 96A of CGST Rules.

Rule 96A of CGST Rules : Refund of integrated tax paid on export of goods or services under bond or Letter of Undertaking.-

Rule 96(A)(1) Any registered person availing the option to supply goods or services for export without payment of integrated tax shall furnish, prior to export, a bond or a Letter of Undertaking in FORM GST RFD-11 to the jurisdictional Commissioner, binding himself to pay the tax due along with the interest specified under sub-section (1) of section 50 within a period of —

(a) fifteen days after the expiry of three months from the date of issue of the invoice for export, if the goods are not exported out of India; or

(b) fifteen days after the expiry of one year, or such further period as may be allowed by the Commissioner, from the date of issue of the invoice for export, if the payment of such services is not received by the exporter in convertible foreign exchange.

Rule 96(A)(2) The details of the export invoices contained in FORM GSTR-1 furnished on the common portal shall be electronically transmitted to the system designated by Customs and a confirmation that the goods covered by the said invoices have been exported out of India shall be electronically transmitted to the common portal from the said system.

Rule 96A (6) of CGST Rules : The provisions of sub rule (1) shall apply, mutatis mutandis, in respect of zero-rated supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit without payment of integrated tax”

Procedure of Claiming ITC Refund under Option – 1:

Where the application relates to Refund of Input Tax Credit, the Electronic Credit Ledger shall be Debited by the applicant by an amount equal to the refund so claimed. (Rule 89 (3) of CGST Rules)

As per Rule 89(4) of CGST Rules, in the case of zero-rated supply of goods or services or both without payment of tax under bond or letter of undertaking in accordance with the provisions of sub-section (3) of section 16 of the Integrated Goods and Services Tax Act, 2017 (13 of 2017), refund of input tax credit shall be granted as per the following formula –

Refund Amount = (Turnover of zero-rated supply of goods + Turnover of zero-rated supply of services) x Net ITC ÷Adjusted Total Turnover

Where,-

(A) “Refund amount” means the maximum refund that is admissible;

(B) “Net ITC” means input tax credit availed on inputs and input services during the relevant period;

(C) “Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking;

(D) “Turnover of zero-rated supply of services” means the value of zero-rated supply of services made without payment of tax under bond or letter of undertaking, calculated in the following manner, namely:-

Zero-rated supply of services is the aggregate of the payments received during the relevant period for zero-rated supply of services and zero-rated supply ofservices where supply has been completed for which payment had been received in advance in any period prior to the relevant period reduced by advances received for zero-rated supply ofservices for which the supply of services has not been completed during the relevant period;

(E) “Adjusted Total turnover” means the turnover in a State or a Union territory, as defined under clause (112) of section 2, excluding the value of exempt supplies other than zero-rated supplies, during the relevant period;

(F) “Relevant period” means the period for which the claim has been filed.

As per Sec 54. (1) of CGST Act, Any person claiming refund may make an application before the expiry of two years from the relevant date in such form and manner as may be prescribed:

Exporter after export may file an application electronically in FORM GST RFD-01through the common portal (Rule 89 of CGST Rules)

The proper officer who shall, within a period of fifteen days of filing of the said application, scrutinize the application for its completeness and where the application is found to be complete in terms of sub-rule (2), (3) and (4)of rule 89, an acknowledgement in FORM GST RFD-02 shall be made available to the applicant through the common portal electronically, clearly indicating the date of filing of the claim for refund and the time period specified in sub-section (7) of section 54 shall be counted from such date of filing (Rule 90(2) of CGST Rules)

Where any deficiencies are noticed, the proper officer shall communicate the deficiencies to the applicant in FORM GST RFD-03 through the common portal electronically, requiring him to file a fresh refund application after rectification of such deficiencies. (Rule 90(3) of CGST Rules)

Grant of Provisional Refund : The provisional refund in accordance with the provisions of sub-section (6) of section 54 shall be granted subject to the condition that the person claiming refund has, during any period of five years immediately preceding the tax period to which the claim for refund relates, not been prosecuted for any offence under the Act or under an existing law where the amount of tax evaded exceeds two hundred and fifty lakh rupees. (Rule 91(1) of CGST Rules)

The proper officer, after scrutiny of the claim and the evidence submitted in support thereof and on being prima facie satisfied that the amount claimed as refund under sub-rule (1) is due to the applicant in accordance with the provisions of sub-section (6) of section 54, shall make an order in FORM GST RFD-04, sanctioning the amount of refund due to the said applicant on a provisional basis within a period not exceeding seven days from the date of the acknowledgement under sub-rule (1) or sub-rule (2) of rule 90. (Rule 91(2) of CGST Rules)

The proper officer shall issue a payment advice in FORM GST RFD-05 for the amount sanctioned under sub-rule (2) and the same shall be electronically credited to any of the bank accounts of the applicant mentioned in his registration particulars and as specified in the application for refund. (Rule 91(3) of CGST Rules)

Order Sanctioning Refund : Where, upon examination of the application, the proper officer is satisfied that a refund under sub-section (5) of section 54 is due and payable to the applicant, he shall make an order in FORM GST RFD-06 sanctioning the amount of refund to which the applicant is entitled, mentioning therein the amount, if any, refunded to him on a provisional basis under sub-section (6) of section 54, amount adjusted against any outstanding demand under the Act or under any existing law and the balance amount refundable . (Rule 92(1) of CGST Rules)

Option – 2 : Export on Payment of Tax – Claim IGST Refund

In the case of refund of IGST paid on exports: Upon receipt of information regarding furnishing of valid return in Form GSTR-3 by the exporter from the common portal, the Customs shall process the claim for refund and an amount equal to the IGST paid in respect of each shipping bill shall be credited to the bank account of the exporter.

Procedure of Claiming IGST Refund on Export under Option 2

As per Rule 96 (1) of CGST Rules, the shipping bill filed by an exporter shall be deemed to be an application for refund of integrated tax paid on the goods exported out of India and such application shall be deemed to have been filed only when:-

(a) the person in charge of the conveyance carrying the export goods duly files an export manifest or an export report covering the number and the date of shipping bills or bills of export; and

(b) the applicant has furnished a valid return in FORM GSTR-3or FORM GSTR-3B, as the case may be;

The details of the relevant export invoices contained in FORM GSTR-1 shall be transmitted electronically by the common portal to the system designated by the Customs and the said system shall electronically transmit to the common portal, a confirmation that the goods covered by the said invoices have been exported out of India. (Rule 96 (2) of CGST Rules)

Upon the receipt of the information regarding the furnishing of a valid return in FORM GSTR-3or FORM GSTR-3B, as the case may be from the common portal, the system designated by the Customs shall process the claim for refund and an amount equal to the integrated tax paid in respect of each shipping bill or bill of export shall be electronically credited to the bank account of the applicant mentioned in his registration particulars and as intimated to the Customs authorities. (Rule 96 (3) of CGST Rules)

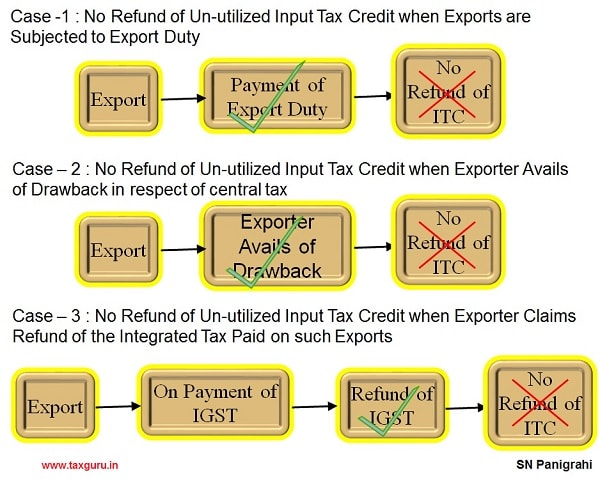

No Refund of Un-utilised Input Tax Credit in Certain Cases

As per Sec 54(3) of CGST Act : Subject to the provisions of sub-section (10), a registered person may claim refund of any unutilised input tax credit at the end of any tax period:

Provided that no refund of unutilised input tax credit shall be allowed in cases other than––

(i) zero rated supplies made without payment of tax;

(ii) where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies), except supplies of goods or services or both as may be notified by the Government on the recommendations of the Council:

Provided further that no refund of unutilised input tax credit shall be allowed in cases where the goods exported out of India are subjected to export duty:

Provided also that no refund of input tax credit shall be allowed, if the supplier of goods or services or both avails of drawback in respect of central tax or claims refund of the integrated tax paid on such supplies.

Having understood the Legal Provisions and Procedures, let us now discuss about Myths of Time Bound Export Refunds.

Myth – 1 : The claim and Sanctioning Procedure will be Completely Online and Time Bound – 90% of Refund shall be Granted within 7 Days

GST law provides for grant of provisional refund of 90% of the total refund claim (Sec 54(6) of CGST Act), in case the claim relates for refund arising on account of zero rated supplies. The provisional refund would be paid within 7 days after giving the acknowledgement (Rule 91(2). The acknowledgement of refund application is normally issued within a period of 15 days (Rule 90(2).

Let us now understand the timelines. As per the provisions of Rule 96A(2), after filling of Export Related Invoice Details in GSTR -1, GST Portal recognizes those Export Invoices and then Transmits the Data to Customs EDI system for Confirmation. Only after Confirmation that Goods Exported out of Country, the Verification Process starts by the concerned officer who issues the acknowledgement within 15 Days. Clock now starts for the count of Seven Days for Release of 90% of Refund.

That means before the issue of acknowledgement there are many other conditions to be fulfilled such as all Export Invoice details and Shipping Bill details shall be filed in GSTR -1 Return. Then such details are verified in the EDI system of Customs. As a customary practice updating EGM details in Shipping Bill usually taking any time between 15 days to 30 days (sometimes more in some ICDs for reasons that Shipping Line is not providing timely EGM information to Customs). Then after the Proper Officer takes his leisure time as provided in statute up to 15 days. Only after the proper officer issues acknowledgement, the Myth of 7 Days opens.

Reality – 1:

In short of all these processes takes any time between 3 – 4 Months. That means Refund of 90% of claim within 7 days is only a Myth and not reality. This leads to blockage of funds for working capital that is what exporters are worried about. This may cost 3 – 4% (assuming annual interest of 12% blocked for 3-4 months) extra to the exporters. Alternatively adding this cost to our exports to that extent loosing Export Competiveness.

Myth – 2 : Interest is Paid for Delayed Payment of Refund @ 6%

As per Notification No. 13/2017 – Central Tax, 28th June, 2017, under Sec 56 of CGST Act and Rule 94, Interest @ 6% is payable if full refund is not granted within 60 days.

Reality – 2 :

However there is no relief to the Exporters in case the 90% of claim amount delayed for any reason beyond 7 Days from the date of Acknowledgement of Application. He has to wait till 60th day to be eligible at all for any claim of interest on delay. That means from 8th day till 60th day interest on 90% of the claim has to be foregone, thanks to the wisdom of Govt. to cover up delays from official side. On the other hand if any delay happens by the tax payer on account of payment of tax 18% interest is charged while paying for delay from Govt side only 6% interest is paid to the Tax Payer. This against the Natural Justice and equitable treatment.

Myth – 3 : IGST Refunds for Exports made in July 2017 start by 10.10.2017 – as Recommended GST Council in its meeting on 06-10-2017.

The Committee on Exports setup by the GST Council has recommended that IGST refunds for exports made in July 2017 must start by 10.10.2017. This recommendation has been endorsed by GST Council in its meeting on 06-10-2017. Necessary background work is being done by the Directorate General of Systems. GSTN and Controller General of Accounts (PFMS). In order to ensure that refunds start smoothly guidelines are issued for the field formations vide Instruction No. 15/2017- Customs, dated the 9th October 2017.

The guidelines are :

Export General Manifest :

Filing of correct EGM is a must for treating shipping bill or bill of export as a Refund Claim.

Exporters may be advised that they should follow up with their carriers to ensure that correct EGM/export reports are filed in a timely manner.

Details of Export Supplies in Table 6A of GSTR-1

The details of zero rated supplies declared in Table 6A of return in Form GSTR-1 are matched electronically with the corresponding details available in Customs Systems as per details provided in shipping bills/ bill of export.

Thus exporters must file their GSTR-1 very carefully to ensure that all relevant details match. For their convenience, the details available in the Customs System have been made available for viewing in their ICEGATE login.

For month of August 2017 and subsequent months. facility of filing GSTR- I has not been made available by GSTN at present. In order to facilitate processing of refunds, GSTN is making available a separate utility for filing details in Table 6A of GSTR-1 on the GSTN Web portal. Exporters may be advised to submit the requisite details once GSTN develops the utility.

Valid return in Form GSTR-3 or Form GSTR-3B

Filing of valid return in GSTR-3 or GSTR-3B is another pre- condition for considering shipping bill/ Bill of export as claim for refund. Exporters may be advised that they must file these returns expeditiously without waiting for the last date. to ensure that their refund is processed in a timely manner.

Bank Account Details:

As per Rule 96 of CGST Rules 2017, the refund is to be credited in the bank account of the applicant mentioned in his registration particulars. As a practice, exporters have been declaring details of bank account to Customs for the purpose of drawback etc. There is a possibility that bank account details available with Customs do not match with those declared in the GST registration form. In order to ensure smooth processing and payment of refund of IGST paid on exported goods, it has been decided that said refund amount shall be credited to the bank account of the exporter registered with Customs even if it is different from the bank account of the applicant mentioned in his registration particulars. However, exporters may be advised to either change the bank account declared to Customs to align it with their GST registration particulars or add the account declared with Customs in their GST registration details.

Further. as the refund payments are being routed through the PFMS portal. the bank account details need to be verified and validated by PFMS. The status of validation of bank account with PFMS is available in ICES. Exporters may be advised that if the account has not been validated by PFMS, they must get their details corrected in the Customs system so that their bank account gets validated by PFMS. Exporters are also advised not to change their bank account details frequently to avoid delay in refund payment.

Processing of refund claims

Proper officer of each jurisdiction shall generate a payment scroll of eligible IGST refunds in the same manner as RoSL scrolls are generated. The scroll shall be transmitted electronically to PFMS system for onward payment into their hank accounts. Unlike RoSL where paper scrolls are to be sent by field formations, in this case, electronic verification will be done centrally by a DDO appointed in this regard. Detailed EDI procedure for processing of claims and generation of refund scrolls is being circulated by Directorate of Systems. DG- Systems is also laying down the procedure for payment and accounting in consultation with Pr. CCA CBEC and CGA of India.

Proper officers may be designated in each Commissionerate, who should be in readiness to start generating refund scrolls from 10.10.2017 on wards.

Reality – 3 :

All is well, but the Euphoria is short lived. On the same day of issue of the above guideline vide Instruction No. 15/2017- Customs, another instructions vide Instruction No. 16/2017- Customs, dated the 9th October 2017 was issued expressing difficulties of process of disbursement of IGST refund through PFMS portal and instead advised to field formations to continue with issue of cheques presently being used for refund payments. We all know how efficient our India Bureaucracy in handling processes’ manually.

Myth – 4: All Exporters are Cover under Auto Filling of Refund Applications (ie Shipping Bill is Treated as Application for Refund)

Exporters who first paid IGST on exports and then claiming for refund amount of IGST paid as covered under Rule 96 need not file separate application for refund but the shipping bill itself shall be treated as an application for such refund following the process as explained already.

Reality – 4

That means majority of exporters who follow other option (Option – 1) of making exports without payment of Tax and filing refund claims for proportionate ITC on inputs are not covered under this and accordingly the announcements made in the GST Council meeting on 06-10-2017 for early disbursement of Export Refunds starting from 10.10.2017 are not applicable.

Moreover the Exporters who make Exports Without Payment of Tax and Claim Refund of ITC has to File Separate Application in FORM GST RFD-01, in the GST Portal which is not yet Ready for Filling. That means they have to wait for some more indefinite time (Till Date no Announcement), thanks for their wisdom to opt for the scheme (Simply because we can’t blame the authorities and poor preparedness of the system – GST Portal)

Disclaimer :

The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner & Trainer

Can be reached @ snpanigrahi1963@gmail.com

The clarity given by you is very excellent

Thankyou

Dear sir,

the article is deeply informative and very important. thanks a lot.

Effort of the author in explaining the issue lucidly is highly appreciated.

Superb Article Thank you