BACKGROUND

I would like to Owe to all the readers for providing good response & Appreciation to my article “GEAR UP FOR THE FIRST GST RETURN(GSTR-3B)”.

Various registered persons under GST Act have input credit balance of OLD LAWS (Excise, Service tax, Value Added tax, Entry Tax (In some cases)) which they want to be carried forward in GST. Hence government has come up with transitional provisions to entertain such credit to be carried forward.

However, over the period of two months we have witnessed various confusions, Ambiguity among businessmen, professionals regarding how the credit can be availed and how it would be available to us. With a goal to ensure the businessmen concentrates on his business and not worry about the credit after reading this article.

Government has released Form TRAN-1 (Which is available in the GST portal), whosoever wants to claim credit available under old law has to file TRAN-1.

It is to be understood that Excise, Service tax Credit would be available as Credit under GST as CGST Credit and VAT & Entry Tax (In case SGST allows) credit would be available as SGST Credit.

FILING OF TRAN–1

TRAN-1 has to be filed online, there is no offline utility available to complete the process.

In this article, we would be going through the form, and showing which table is applicable to concerned credit and important things to be noted while filling such table.

Log in to the GST Portal click on returns and select Transition Forms.

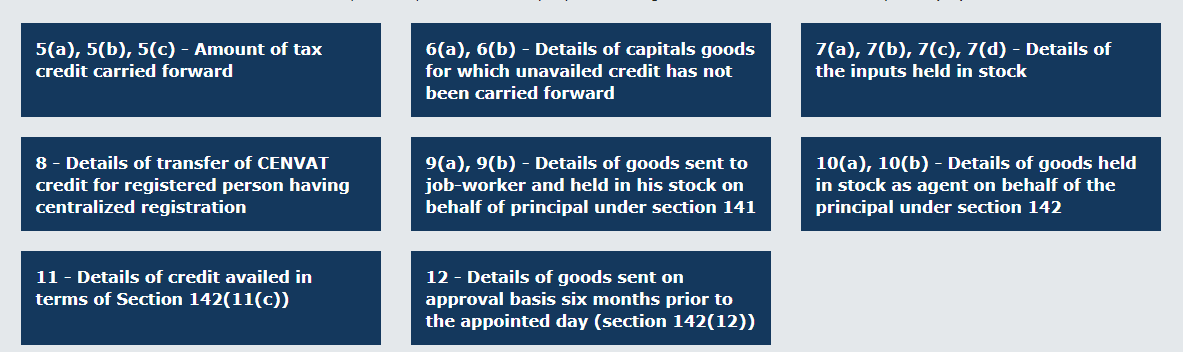

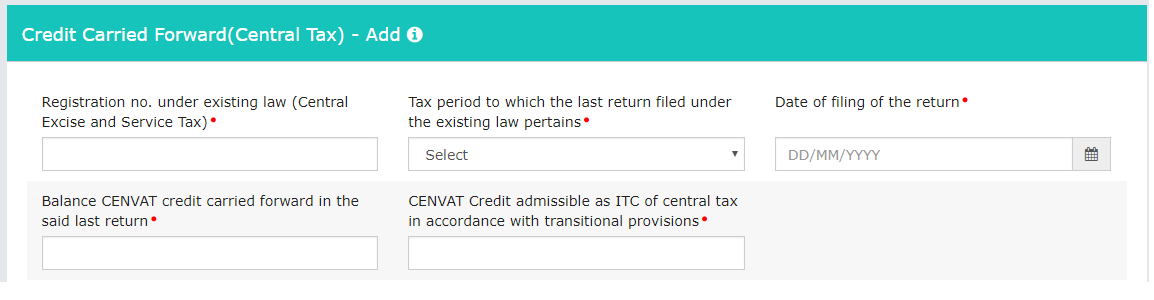

1. 5(a) – AMOUNT OF CENVAT CREDIT AVAILABLE AS CLOSING BALANCE In EXCISE/SERVICE TAX

1. Applicable: Every Manufacturer, Service Provider who has Cenvat credit balance in the return filed for the month of June (Quarterly or monthly).

2. Not Applicable: First Stage Dealer, Second Stage dealer, even though registered in Excise & dealer who is only registered in VAT is not required to mention details in this table.

3. Things to note: It only requires basic details, however while filling this table ensure the Cenvat credit carried forward matches with your return for or upto the month of JUNE, 2017.

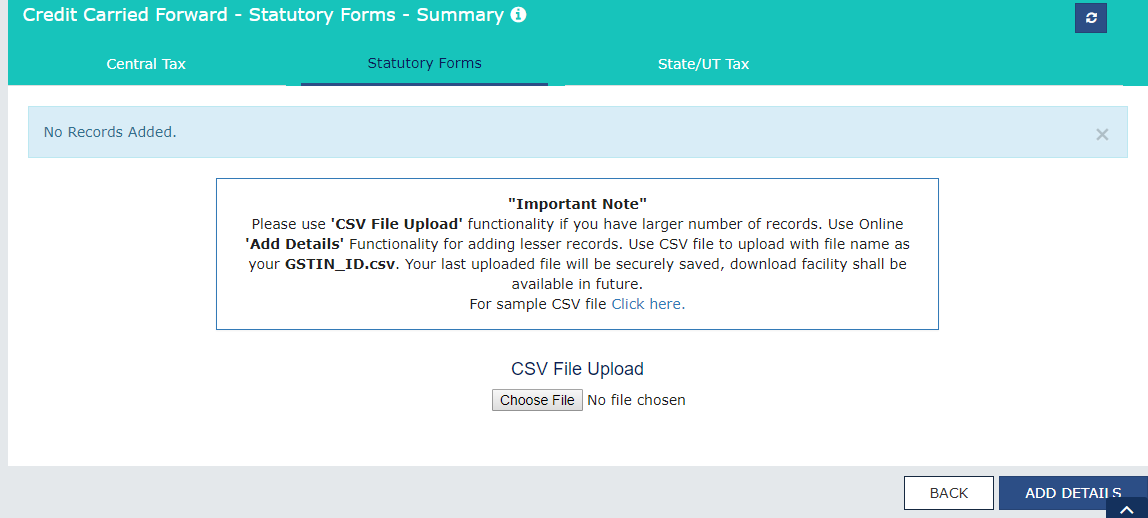

2. 5(b)-STATUTORY FORMS

1. Applicable: All the dealers who had made interstate sale (Form C)/stock transfer (Form F)/Deemed Export (Form H)/Sale to SEZ (Form I) at concessional rates for the period April-2015 to June-2017 and respective forms have been issued.

2. Not Applicable:

i. Dealer who has not affected any above-mentioned transactions.

ii. Dealer who has undertaken such transaction, however has not received the forms yet.

iii. Dealer who has undertaken such transactions and received the Forms, but does not want to claim any Credit under SGST (i.e. VAT Credit)

3. Important Point:

i. Taxpayer is required to provide details such as Name of the issuer of Form, Tin of the issuer, Serial Number of the form received and the amount of such Form Type of Form received.

ii. In case the volume of Such Forms is more than 100 the taxpayer is required to download csv, file mention the details and upload, else he can feed the details online.

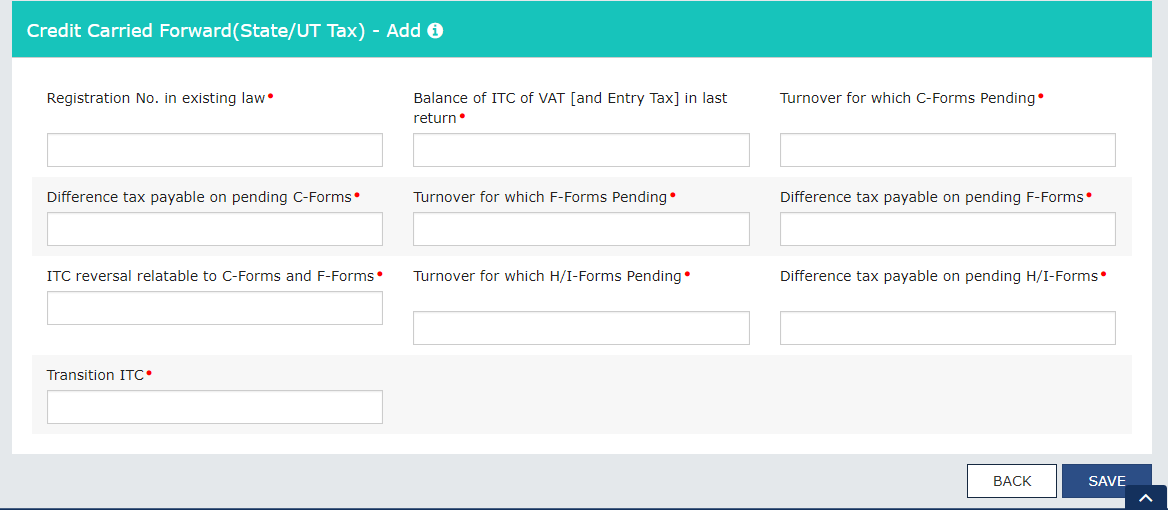

3. 5 (c)-AMOUNT OF TAX CREDIT CARRIED FORWARD OF VAT

1. Applicable: Dealers who were registered under Respective State Vat and after filing the return for the month of June-2017, had input credit to be carried forward.

2. Not Applicable: Composition Dealers under VAT or any person who were not registered under VAT.

3. Important Points:

i. Dealer registered under Vat needs to take his return filed for the month of June-2017 mention his Registration number (TIN NUMBER) in this table and provide Input tax credit carried forward amount shown in June month.

ii. With respect to Entry Tax, one needs to go through the respective State’s GST Act and find out whether Entry tax credit can be carried forward for instance: Karnataka GST does not allow credit of Entry Tax whereas Maharashtra GST Act allows credit of it.

iii. After mentioning the closing balance, Dealer is required to mention the total amount of sale which was done at concessional rate on which forms are not yet received and the differential tax payable (Vat rate:5.5%, C Form rate :2% C form not received then diff tax is (5.5% – 2% = 3.5%).

iv. After mentioning the differential tax, Dealer needs to mention (Total Input credit according to June-17, return and deduct differential tax on which forms are not received) in total SGST Credit admissible.

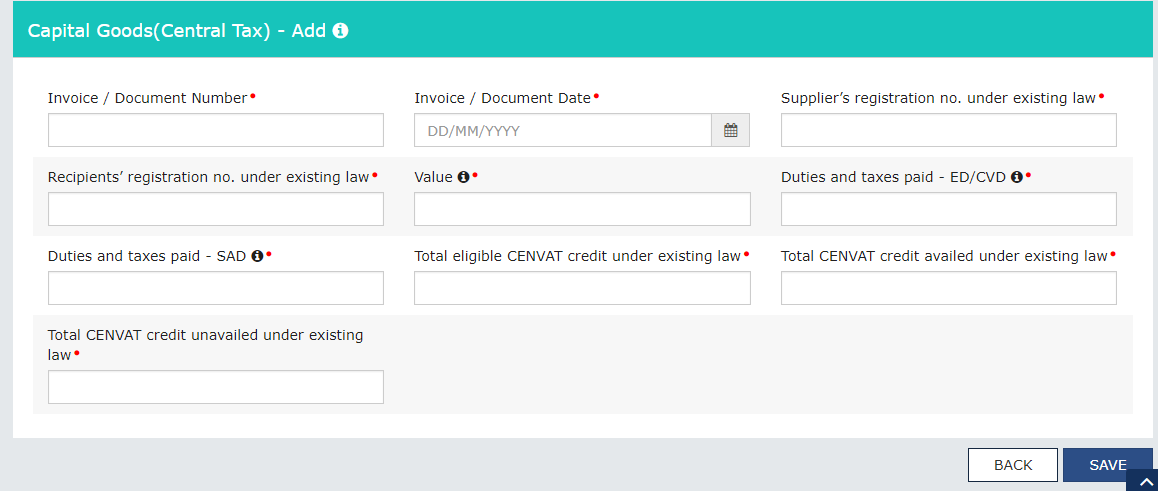

4. 6(A)-DETAILS OF CAPITAL GOODS FOR WHICH CREDIT HAS NOT BEEN CARRIED FORWARD (CENTRAL TAX).

1. Applicable: In case any person who was registered under Excise or Service tax and had purchased capital goods (According to rule 2(a) of CENVAT CREDIT RULES) on which upto 50% of the credit had been taken earlier and 50% or 100% is yet to be taken.

2. Not Applicable: It is not for any capital good of a person who was not registered under old laws.

3. Important Point: In case the Dealer has not claimed any credit under old law, he can still take full credit under this table, provided he was registered under the Said act (Excise/s.t to claim excise credit and under VAT to claim VAT Credit).

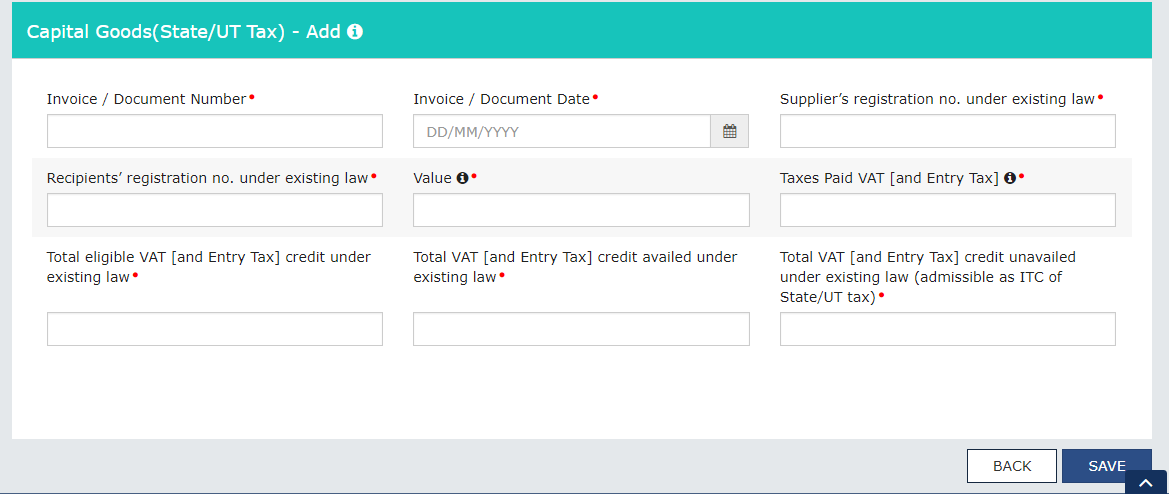

5. 6(b)-AMOUNT OF UNAVAILED CREDIT OF CAPITAL GOODS UNDER VAT/ENTRY TAX.

1. It is similar to 6(a) and only thing is it is related to SGST Act, however in most of the cases, dealers would have claimed VAT on capital goods in the month in which it was procured provided it was available as credit.

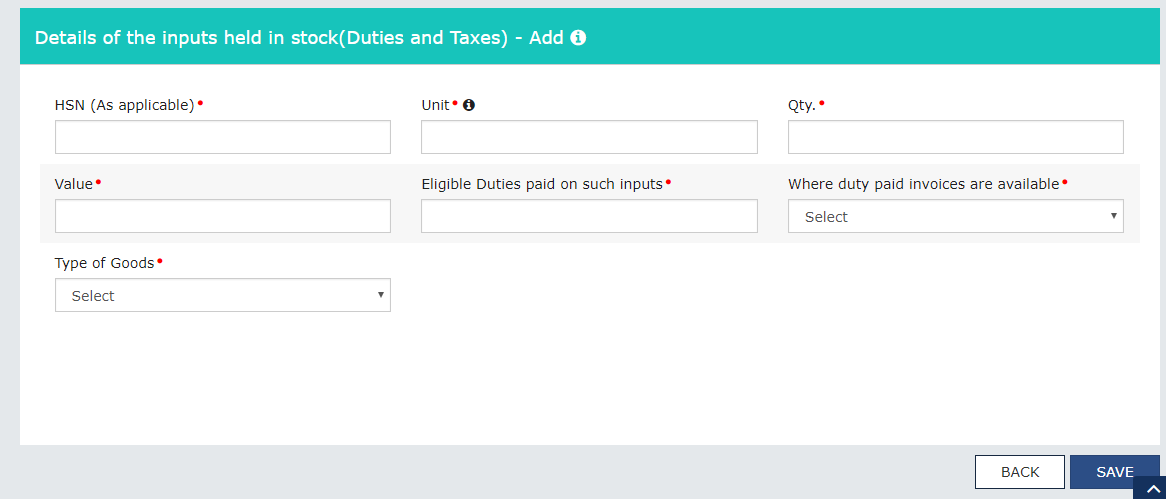

6. 7(a)-Duties & Taxes on Inputs.

1. Applicable: First Stage Dealer, Second Stage Dealer, Any Person who was earlier not registered under Excise and wants to claim credit of Duties which he has paid and not claimed credit and lying in Stock.

2. Not Applicable:

i. Composition dealer who wants to claim Credit of VAT,

ii. Registered Person who has already claimed Excise

iii. Any Credit related to Service Tax would not be allowed.

iv. Manufacturer or service provider not having tax paying document.

3. Important Points:

i. Manufacturer, First Stage Dealer, Second Stage Dealer, any person registered under GST not registered under earlier laws, in case has Invoice with him in relation to goods lying in stock he may provide consolidated figure of such in this table HSN Wise.

ii. In case of a trader, who deals in goods which were exempt earlier and in GST it is taxable or had procured goods on which excise or VAT was levied but he couldn’t claim credit as he was not registered and if he does not have tax paying document of such (HOWEVER PURCHASE INVOICE IS REQUIRED), he may provide the details of such stock in this column in HSN Wise and in the field of whether duty paid invoice available, he is required to mention NO, as soon as he mentions “NO” the field Eligible Duties would be blocked at “0”, as he would get Deemed Credit on the same according to the TRAN-2 filed by him for six tax periods (I.e. From JUNE-17 to Dec-17).

iii. 7(a) is not for claiming VAT Credit for Composition Dealers who on migration became regular taxpayers.

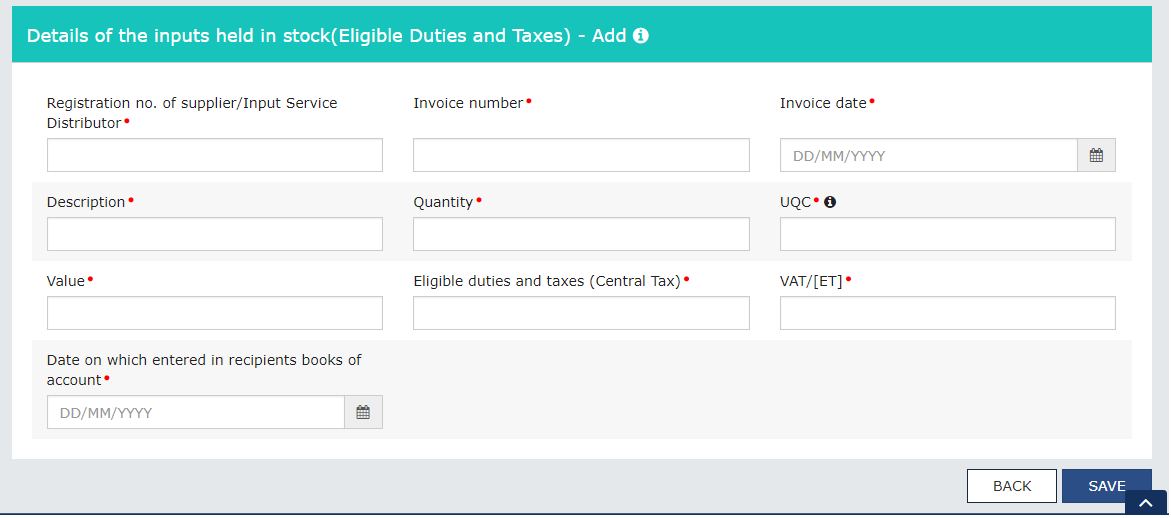

7. 7(b)-DETAILS OF INPUT HELD IN STOCK (ELIGIBLE DUTIES AND TAXES)

1. Applicability: 7(b) table is to be filled only where the taxpayer had ordered some goods prior to GST (before 1/7/2017) and such goods were delivered to the taxpayer premises after GST (on or after 1/07/2017). The Problem in this case would be that the supplier would have made an invoice with Excise and/or VAT, which is no more valid after GST. Hence in case any taxpayer has obtained any goods in the above-mentioned situation, he is required to fill this table. The Date to be mentioned in this table cannot be prior to 01/07/2017.

i. General Practice & Problems therein: It is noticed in various places in order to avoid this businessman are entering such purchase invoices in the books on 30/06/2017 itself, the problem therein is the Transporter gives you the L.R.Copy which would contain the date of July. I hope you have understood.

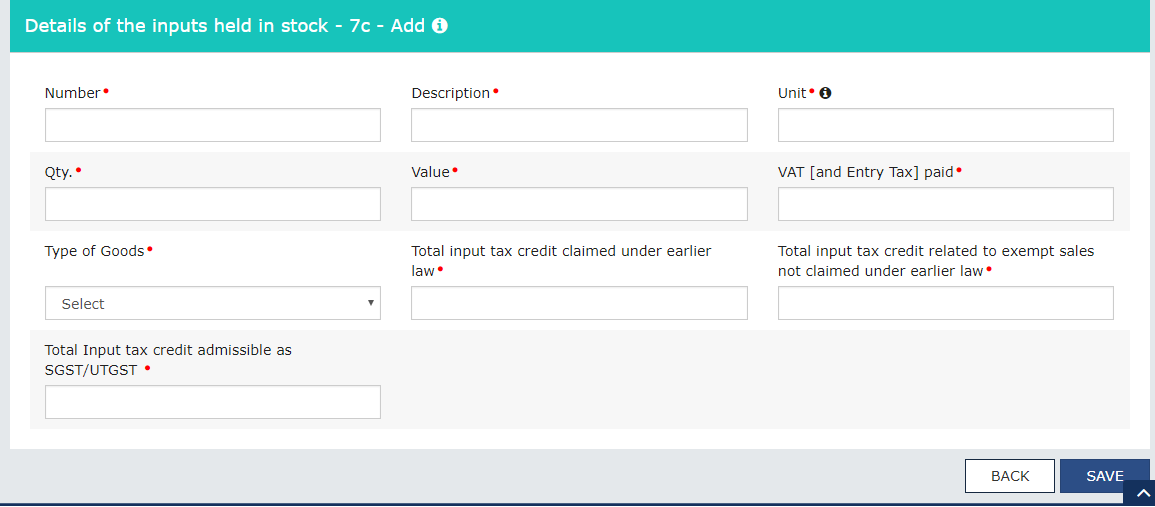

8. 7 (c)-DETAILS OF INPUTS HELD IN STOCK ON WHICH VAT & ENTRY TAX HAS BEEN PAID.

1. Applicable: Every Dealer who has Tax Paying Document with him and wants to Claim credit, Composition Dealers under earlier laws who couldn’t claim credit.

2. Important Point:

i. Any Person who wants to Claim deemed credit should not feed the details herein (he needs to mention either in 7(a) by mentioning NO document or 7(d)).

ii. Amount taken as Credit here would be available as SGST Credit.

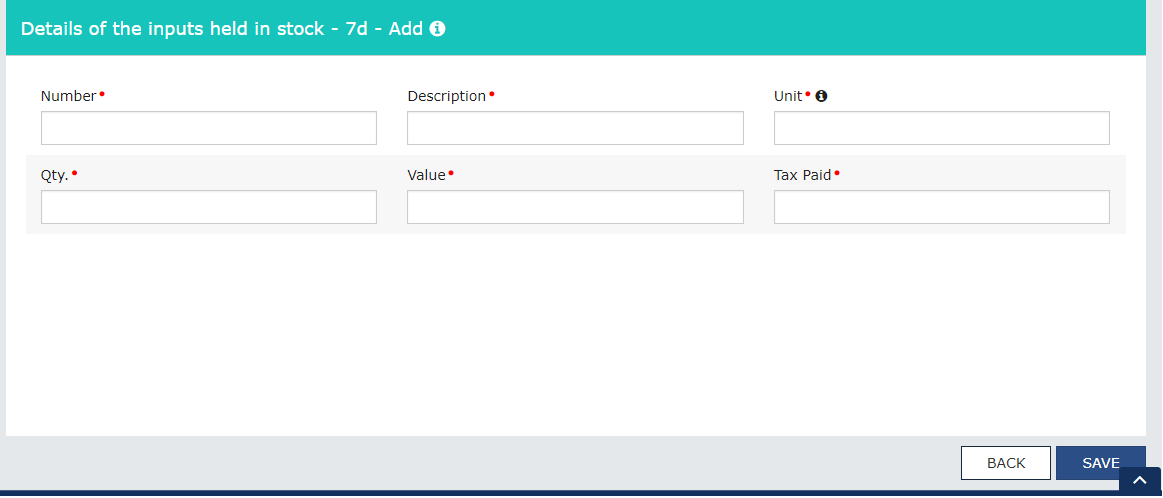

9. 7(d)-Stock of Goods

1. The Table is to be filled only by the dealers or traders with respect to Goods which are not supported by Invoice/Document which states that tax has been paid.

2. Manufacturer or Service Provider cannot claim Credit under this table.

3. This table is applicable only for those states which have VAT at single point and subsequent sale of such goods would be exempt.

4. E.g.: In Karnataka, it is multi Point tax, whereas in Rajasthan, VAT on medicine is single point in such a case the dealers in Rajasthan can claim credit on Stock available with them by filing this table.

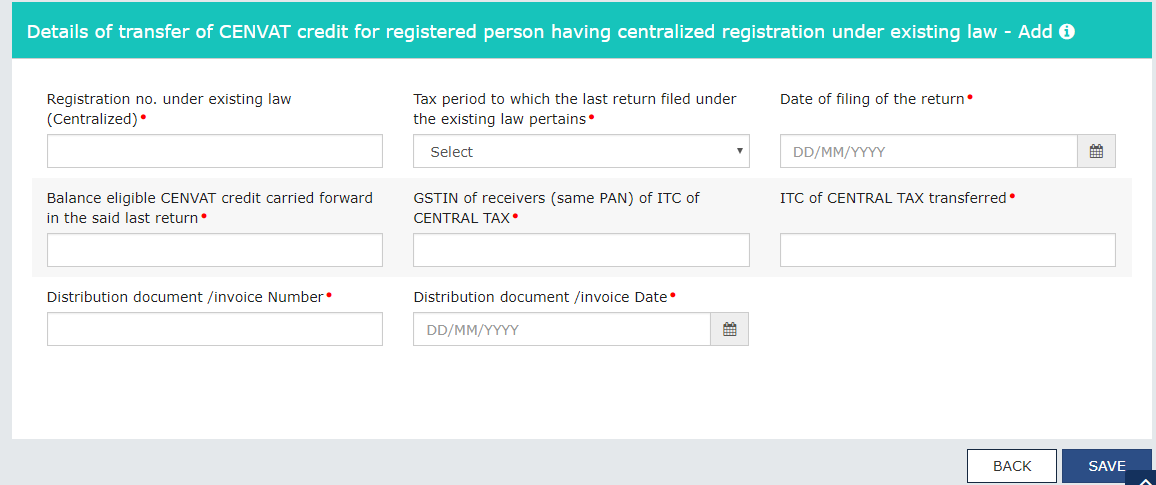

10. 8 – DETAILS OF SERVICE TAX CREDIT TO BE DISTRIBUTED FOR A PERSON HAVING CENTRALISED REGISTRATION.

1. It is applicable for assessee who have taken Centralised Service Tax Registration. Since under GST it is STATE Wise registration, The Service provider would take registrations in the respective states and in order to distribute credit, the place of centralized registration has to issue a document stating the amount of credit to be allocated. And hence the credit distributed in such a scenario has to be mentioned in this Table.

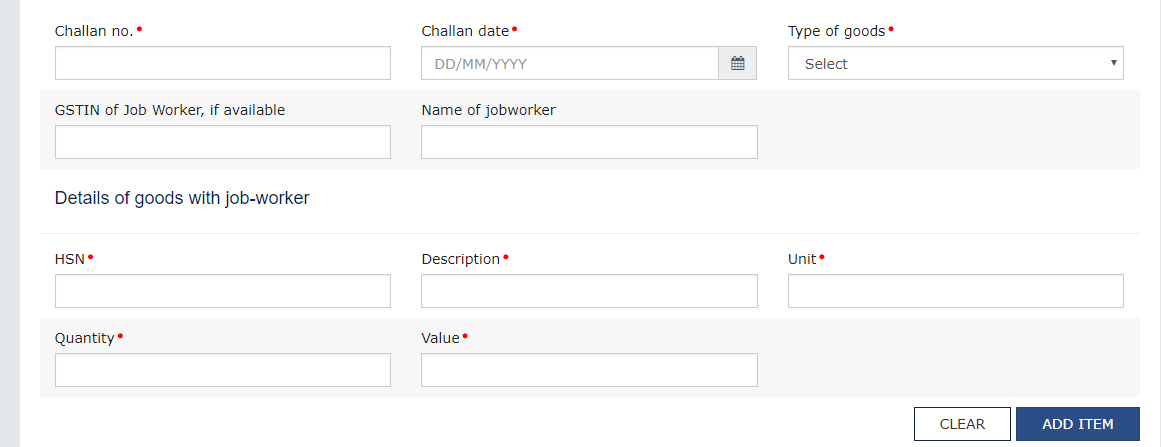

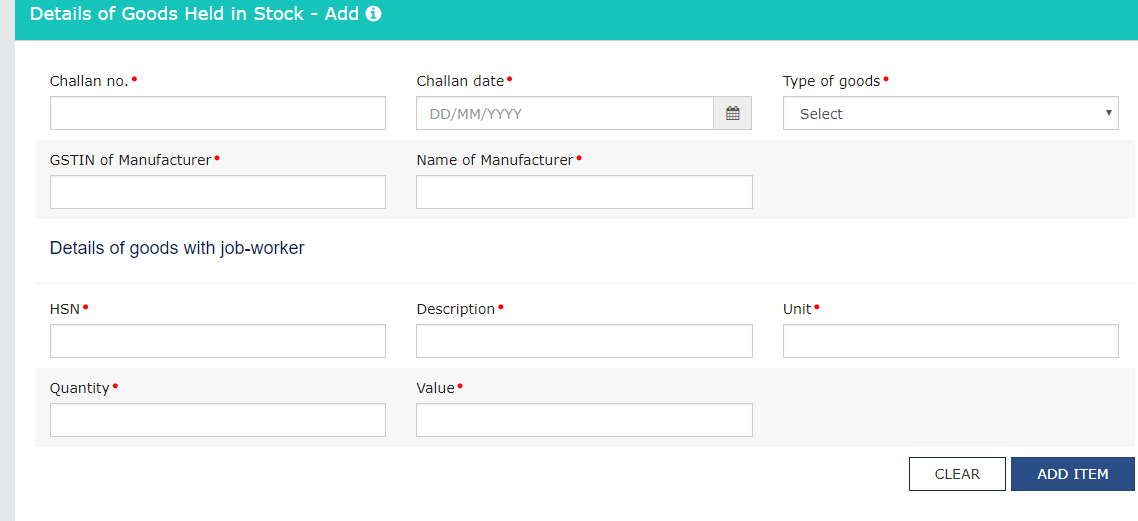

11. 9(a) – Details of Goods sent to Job worker (Applicable to person sending goods to job worker)

1. In case any taxpayer had sent any goods to Job worker before 01/07/2017 and they were still lying with the job worker, then the taxpayer is required to mention the details of the Job worker, Document generated to send the goods to him, and details of such goods

2. Major reason to ask for this detail is if the details have been mentioned in this table, then if the job worker sends back the goods within 6 months no TAX would be payable,

3. In case the taxpayer does not mention the details of goods sent to the job worker, then any goods returned would be considered as Deemed Supply and GST would have to be levied/Input tax credit taken on such goods would also be recovered.

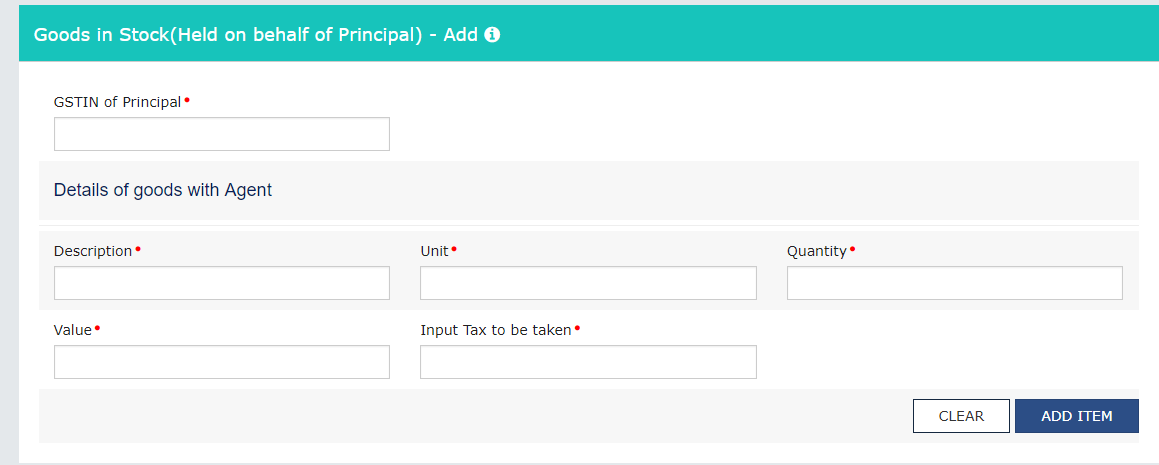

12. 9(b)-Details of Goods held of Principal (Applicable to Job worker who gets goods from Principal) (Held in Stock)

1. Job workers are required to mention the details in 9(b) regarding the GSTIN of principal with respect to the goods which are held by him and details of such goods.

2. This has been done to ensure cross verification of Goods available with Job worker and Goods as declared by principal to be with Job worker in 9(a)

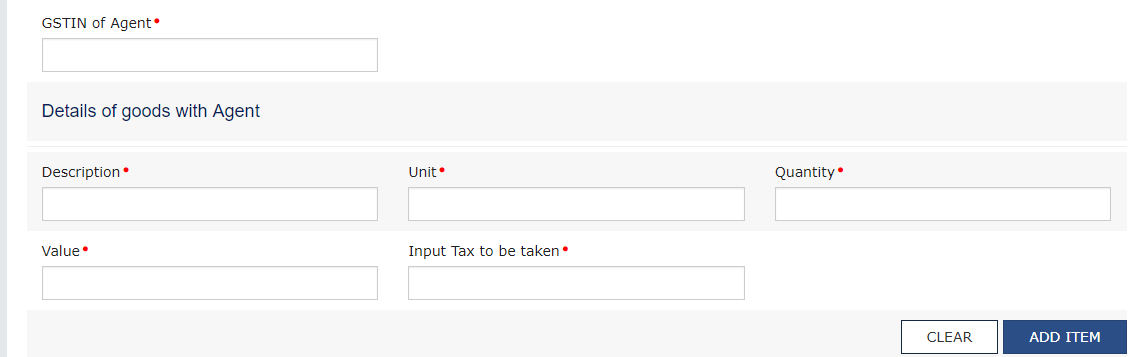

13. 10(a)-Details of Goods held of principal by AGENT (TO BE FILLED BY AGENT WHO WANTS TO CLAIM CREDIT ON GOODS HELD BY HIM UNDER SECTION 142)

1. Under GST, Agent can claim credit of stock held by him related to principal subject to conditions specified in 142 such as agent should be registered and input tax should be reversed by principal etc.,

2. Agent has to fill the table 10(a), provide details of Stock available along with the GSTIN of Principal whose stock is available with him in order to take credit.

14. 10(b)-Details of Goods available with AGENT (To be filled by principal whose goods are with AGENT who would be filling table 10(a))

1. Similar to Concept used in Job worker, here also the government would like to take double verification by stating to principal to also provide details of stock lying with Agent.

2. Kindly do consider that the input tax credit mentioned by you in your table 10(a) would only be allowed to the agent who correspondingly in his GST TRAN-01 would be claiming credit of this.

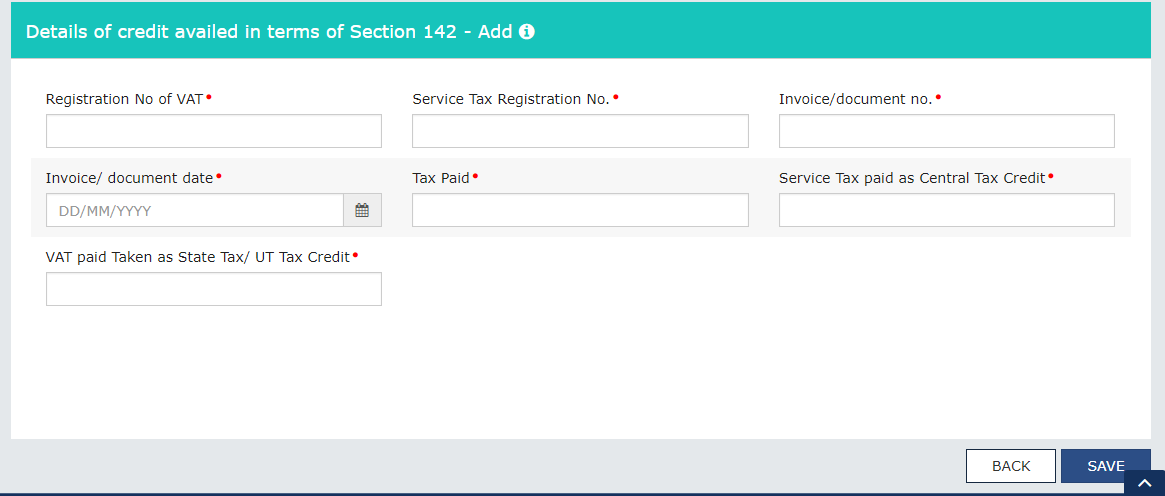

15. 11- Details of Credit to be taken of VAT & Service tax paid on any supply(SALE) under 142(11) (c)

1. First of all, this Legal Provision states that in case if any taxpayer has paid VAT & Service Tax on the sale made/to be made on or before 01/07/2017 and on the day of point of supply it appears that GST is to be levied, then such person would be entitled to take credit of VAT & Service tax paid by him earlier under Section 142(11) (C).

2. In simple words, if we take an example of a builder, if he takes consideration before certifying authority certificate he would be liable to charge Service tax and VAT, however when he provides the deal it might so happen that GST would have had come into force and hence in such a situation VAT & Service tax Collected and paid by him would be provided as Credit against such GST.

16. 12-Details of Goods sent on Approval Basis within 6 months prior to GST Implementation.

The Last table is for Taxpayers who would have had sent goods on approval basis on or after 01/01/2017 but before 01/07/2017.

1. The detail is to be provided by the taxpayer in order to ensure himself that in case the customer sends back the goods within 6 months from GST Date (I.e. within 31st December,2017) there would be no tax payable under GST Act.

2. The taxpayer would be required to provide details of the goods and GSTIN of the recipient in TRAN-1, he won’t be getting any credit by filling the table however he would be on safer side in case there is any sales returns or goods are not approved and sent back.

I hope I have tried to make GSTR TRAN-1 to be easy to be understood, however I would always suggest that since this return is one timer, businessmen should not be taking any risks of losing out credit and consult an expert.

Once the submit option is clicked, taxpayer would not be able to make any changes in the form. This also indicates that one needs to be careful while filing the form.

Note: The opinion mentioned in this article are personal Opinion and nothing of the same amounts to Professional Consultancy.

(Author CA YASH JAIN can be reached at +91-9980725175 or can be mailed on yashjainforu@gmail.com)

Author Bio