Guidebook for Faceless Assessment

Turant Customs Programme

Faceless, Contactless and Paperless Customs Clearance

October, 2020

Version 1.0

Disclaimer

The information, content, data etc. provided in this Guidebook is for general guidance of stakeholders. While CBIC will endeavour to update the content of this Guidebook from time to time, readers are advised to refer to the latest provisions of the relevant laws, rules, regulations, circulars, etc.

Foreword

Trade facilitation is a key enabler for simplification of procedures and reduction of barriers to the trade. In India, Central Board of Indirect Taxes and Customs (CBIC) has been at the forefront of taking initiatives aimed at catalysing economic development through transparency, harmonization, predictability and automation in trade. The aim has been to reduce time and cost for the EXIM community. This would help them become more competitive in the international arena.

In line with this momentum, CBIC has implemented next generation reforms through Turant Customs, strongly enabled by technology. This flagship initiative stands on the pillars of – Faceless, Contactless and Paperless Customs. This reform will help India take a substantial leap forward towards faster and cheaper Customs clearance of imported goods.

A key enabler in Turant Customs is Faceless Assessment. It is being rolled out in phases and is scheduled to cover the entire country by 31st October 2020. This would enable uniform, anonymous Customs assessments and reduce interface between the Trade and Customs officers.

The response of Custom officials to the dynamics of the worldwide changes in the ecosystem has been commendable. In this regard, the efforts of Indian Customs, in particular, have been notable, particularly the pace with which it has constantly adapted and evolved in this large and diverse country.

I commend the officers of CBIC for their commitment to the cause of regulatory reforms aimed at enhanced efficiency. Our efforts need to be complementary and synergized at all times to ensure that the reforms enable a conducive and transparent environment for businesses involved with cross-border trade in India.

M. Ajit Kumar

Chairman, CBIC

Contents

Foreword

Executive Summary

Chapter 1: Introduction to Faceless Assessment

Chapter 2: Institutional setup

Chapter 3: National Assessment Centres

Chapter 4: Process for Faceless Assessment

Chapter 5: Key Considerations for Faceless Assessment

Chapter 6: Performance Measurement

Chapter 7: Communication and Outreach

Chapter 8: Frequently asked Questions

Annexure 1: Implementation Phases for All India Roll-Out of Faceless Assessment

Annexure 2: National Assessment Centres

Annexure 3: Workflow for BE under Faceless Assessment

Annexure 4: Enablers of Faceless Assessment

Acronyms and Abbreviations

References

Executive Summary

The Central Board of Indirect Taxes and Customs (CBIC) is the apex body mandated for the Customs clearance of cross border trade (import, export and transhipment). Over the years, CBIC has been instrumental in improving overall business environment and our global rankings in the category of Trading Across Borders. Turant Customs is going to further this agenda in the coming years.

Recent years have seen India evidence significant improvement on multiple independent global indices which evaluating efficiency of the cross-border ecosystem. This includes the World Bank’s Logistics Performance Index and Doing Business assessment (on the Trading Across Borders indicator) as well as the UN global survey on digital and sustainable trade facilitation.

![]()

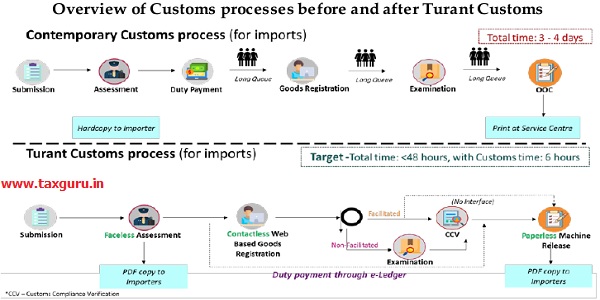

Previous Customs clearance processes involved myriad requirements that were manually operated, complex, sequential and time-consuming. 3rd February 1995 marked a watershed day for Indian Customs, on that day 25 years ago, India’s first electronic Bill of Entry (BE) was filed at New Customs House, New Delhi.

Migration of core Customs process to a technology platform opened-up a host of opportunities to reform the border clearance ecosystem. Earlier, the importers, exporters and other actors engaged in international trade (shipping lines, freight forwarders etc.) were required to prepare and submit large amount of information to border agencies to comply with various regulatory requirements. Also, this information had to be submitted separately to several different agencies, which their own specific automated or manual systems to process the data. This used to put a serious burden both on Government and trade. Thus, early initiatives by Customs focussed on expeditious transmission of documents between Participating Government Agencies (PGA) as well as parallel processing of documents. This led to the introduction, in 2016, of Single Window Interface For Facilitating Trade (SWIFT), which enabled traders to file their documents for clearance through a common entry point. SWIFT harmonized the regulatory compliance system by simplification of information flows between government and trade. Co-incidentally, creation of a single window facility is also a key obligation for signatories of the World Trade Organizations (WTO) Trade Facilitation Agreement (TFA).1

SWIFT enables traders to file a common electronic ‘Integrated Declaration’ on the ICEGATE portal replacing the separate forms required by PGAs, which include Food Safety and Standards Authority of India (FSSAI), Plant Quarantine (PQ), Animal Quarantine (AQ), Central Drugs Standard Control Organization (CDSCO), Wildlife Crime Control Bureau (WCCB) and Textile Committee. A ‘PGA Corridor’ within the platform’s Risk Management System (RMS) then routes the declarations automatically to concerned agencies. SWIFT is complemented by e-SANCHIT which allows traders to submit electronic digitally signed copies of supporting documents thereby dispensing with hard copies that were physically submitted earlier.

SWIFT enabling ‘Minimum Government, Maximum Governance’

SWIFT, Indian Customs EDI System (ICES) and Indian Customs Electronic Gateway (ICEGATE) have now become synonymous with the digital evolution journey of Indian Customs, making the Department a frontrunner of e-Governance initiatives in the country.

In recent times, the possibilities offered by technology to enhance trade facilitation have expanded exponentially. At the same time, the WTO’s TFA has spurred efforts to re-engineer the extant processes for expediting cargo clearance. The combination of applying technology to modern trust-based processes has led to the realization that trade facilitation can be significantly enhanced without compromising national interest (including economic, social and environmental). Further, recent uncertainty ushered by Covid-19 has fast tracked the move towards a ‘new normal’ based on the heightened use of technology.

Indian customs introduced the ‘Turant Customs’ programme as a key initiative of CBIC to enable faster clearance at lesser cost to the trade, transparent decision making leading to enhanced ease of doing business. Components of the programme are characterized by three key attributes i.e. a Faceless, Contactless and Paperless Customs clearance processes. The programme radically reimagines extant processes by leveraging technology for greater transparency, efficiency and accountability.

The most critical component of the Turant Customs programme is Faceless Assessment, which is set for an All India launch on 31st October 2020. Faceless Assessment (also referred to as virtual assessment or anonymised assessment) uses a technology platform to separate the Customs assessment process from the physical location of a Customs officer at the port of arrival. This measure will bolster efforts to ensure an objective, free, fair and just assessment.

Key objectives of Faceless Assessment include:

i. Anonymity in assessment for reduced physical interface between trade and Customs

ii. Speedier Customs clearances through efficient utilisation of manpower

iii. Greater uniformity of assessment across locations

iv. Promoting sector specific and functional specialisation in assessment

After running pilot programmes since August 2019, the first formal phase of Faceless Assessment commenced in Bengaluru and Chennai in June 2020. It primarily focused on cargo under Chapters 84 and 85 of the Customs Tariff Act, 1975. This was followed by other phases covering new Customs locations and new items of import.

The phased launch of Faceless Assessment helped CBIC evaluate the responsiveness of Customs officers and trade representatives as well as suitability of the technology platform in a real-world environment. Accordingly, based on the findings of this exercise, the pan India roll out of Faceless Assessment has now been firmed up paving the path for a more modern, efficient, and professional Customs administration.

It is estimated that the Faceless Assessment initiative will help slash release time to only few minutes and few hours, substantially lower than the present clearance times averaging three to four days. Accordingly, Faceless Assessment is expected to have considerable impact on India’s performance on various independent global assessments and boost the country’s trade competitiveness, including ease of doing business. Faceless Assessment also offers many other advantages to both trade and CBIC.

This Guidebook has been prepared to help the Customs officers and other concerned stakeholders in the successful implementation of Faceless Assessment across the country. It will act as a ready reckoner covering aspects of:

- Reforms undertaken by CBIC, especially those enabling Turant Customs

- Institutional set up for Faceless Assessment

- Roles and responsibilities of National Assessment Centres (NAC), their Co-Convenors, Convenors and Members

- Key Considerations for Faceless Assessment

- Processes/ procedures for Faceless Assessment

- Communication and outreach efforts for successful implementation of Faceless Assessment

- Performance measurement and impact analysis

————

Chapter 1: Introduction to Faceless Assessment

1.1 Faceless Assessment, a component of the Turant Customs programme, is a path breaking initiative aimed at introducing anonymity and uniformity in Customs assessments pan India.

1.2 Overview: The journey towards Faceless Assessment has been long. Decades ago, goods imported into India were assessed for Customs duty at the border by jurisdictional Customs officers on the basis of physical documents. Subsequent introduction of computers led to automation of assessment. This was followed by a robust digital risk management system (RMS) for Customs clearance with minimal checks, while interdicting risk-prone cargo for assessment and examination.

In 2012, the Customs Act 1962, was amended to introduce self-assessment by importers/ exporters themselves. While digitisation helped in streamlining of procedures, yet disparities in assessment prevailed due to interpretation issues. Customs officials recognised a dire need to provide uniformity and certainty in assessment practices. It was also clear that anonymity in assessment and load balancing of import documents that are required to be assessed would bring about more efficiency and help improve the speed of Customs clearances across India. This was the trigger for the conceptualization and development of Faceless Assessment.

1.3 Faceless Assessment a Balance between Anonymization and Specialization: Anonymity in assessment is a core feature of the Faceless Assessment initiative. This is aimed to reduce the unnecessary need of a face to face interaction with a Customs official.

This measure will also encourage specialization and uniformity in assessment of identified goods, as officers in a Faceless Assessment Group (FAG) would no longer be required to work on assessment of all goods.

1.4 At present, the Customs Zones and Commissionerates are organized in different ways, as follows:

a. Customs Zones with Customs Commissionerates for all Customs Functions: In these Zones, all the Customs functions in relation to import and export are done in a single Commissionerate. An example is Bengaluru Zone which has three self-contained Customs Commissionerates viz. Bengaluru Air Cargo Complex (ACC), Bengaluru, Inland Container Depot (ICD) and Mangalore Port. Likewise, Kolkata Zone has three self-contained Customs Commissionerates viz. Kolkata, Air Cargo Complex (ACC), Kolkata Port and Kolkata Preventive Commissionerate.

b. Customs Zones with Customs Commissionerates, both self-contained and otherwise: In these Zones, all the Customs functions in relation to import and export are done either in a single self-contained Commissionerate or only specific Customs functions are done in a particular Commissionerate. An example is Delhi Zone, which has Inland Container Depot (ICD) Patparganj as a full-fledged self-contained Commissionerate along with Inland Container Depot (ICD), Tughlakabad (Import) and Delhi Air Cargo Complex (Import) as only Import Commissionerates and Inland Container Depot (ICD), Tughlakabad (Export) and Air Cargo Complex (Export) as only Export Commissionerates.

c. Customs Zones without Full-Fledged Commissionerate combined with Import and Export Commissionerates: In these Zones, a Commissionerate performs partial Customs functions. Examples of such zones are Chennai Zone, Mumbai-I and II. In Chennai, Chennai-II Commissionerate does only assessment work in relation to imported goods whereas Chennai-IV has all the CFS under it where the examination of imported goods is done, and Chennai-VII is a self-contained Commissionerate for air cargo. In Mumbai-II Zone, NS-I Commissionerate is meant for Assessment group I and II and related functions, NS-III deals with Assessment group III and IV and NS-V does the work related to Assessment Group V, VA, VB and VI. Mumbai-I Zone also has similar distribution in terms of assessment groups between Import-I and Import-II Commissionerate.

d. GST Zones Having Customs Commissionerates: In these GST Zones, there are Customs Commissionerate. Examples of such zones are Hyderabad, Meerut, Cochin, Visakhapatnam, Bhopal and Shillong.

1.5 It was seen that despite a centralized automated IT framework for carrying out Customs assessment, the varying assessment structures in the Zones were not compatible with the CBIC’s mission of having uniform and standardized Customs assessment practices. Moreover, as the assessment was being done in the port of import itself, local assessment practices would invariably creep in, despite all attempts at standardization. The different structures were also found to contribute to differences in dwell time of cargo, thereby bringing down the overall efficiency. Thus, it was clear that a fundamental change is warranted to meet the objective of the CBIC in providing a most efficient, transparent and standardized Customs assessment experience.

1.6 The new Customs assessment structure moves away from the physical constraint of assessment by local Customs officers at the Port of Import. Faceless Assessment is being implemented taking into consideration the above mentioned different structures of Customs zones and commissionerates. It redefines the roles of Customs officers for assessment, examination and other related processes along with changes in ICES and creates a superstructure of Faceless Assessment Groups (FAGs), Port Assessment Group (PAG), National Assessment Centres (NACs) and Turant Suvidha Kendras (TSKs). The new dispensation virtually connects Customs assessment officers from different jurisdictions and provides for enhanced level monitoring of Customs assessments based on assignment of import clearance documents by the Customs Automated System (CAS) to officers of the FAGs irrespective of the port of import of the goods.

1.7 A pilot of the initiative was initiated last year by CBIC and post validation of the expected outcomes, it has been decided to roll out the programme nationally. These Pilot Programmes helped test Faceless Assessment first in the same zone, then across zones. Faceless Assessment is now being extended across all Customs ports in India to usher a more modern, efficient, and professional Customs administration, with resultant benefits for trade and industry.

Chapter 2: Institutional setup

2.1 Faceless Assessment is based on the Customs Automated System assigning a Bill of Entry (BE) that is identified for scrutiny (non-facilitated BE) to an assessing officer, who is physically located at a Customs station, which is not the port of import. As aforementioned, the objectives of the initiative are to:

- Anonymize the assessment process by removing the physical interface with Customs

- Ensure uniformity of assessment across locations by promoting sector specific and functional specialization

- Improve workload for efficient utilization of manpower and resources for Customs by

automation of the end-to-end clearance process

The Faceless Assessment institutional set up has two levels, i.e., (i) Local and (ii) Virtual

2.2 Faceless Assessment set up

A. Local Setup

- Port of Import: The port of import is the Customs station of import where the goods lie and the importer has entered a BE for home consumption or warehousing. Its functions are as follows:

- It will have one Port Assessment Group (PAG) to assess cases referred to by the FAG in specific circumstances.

- Turant Suvidha Kendra (TSK) to be set up at Port of Import for various document/ report submission/ generation for the assessment.

Dashboard for Port of Import Commissioner

–

- Port Assessment Groups: the equivalent of Appraising Group currently located in each port of import for verification of the assessment and other related functions as is the normal practice. Their functions include:

i. All functions pertaining to the BE which are not marked to the Faceless Assessment Group by the Customs Automated System.

ii. BEs that are referred by the Faceless Assessment Group to the port of import, for any reason.

iii. Handling of issues arising post assessment, relating to the BEs which were handled in the Faceless Assessment Group.

- Turant Suvidha Kendras: are facilitation centres which will handhold and facilitate trade, as it adapts to the new system. To reduce friction and to handhold stakeholders, TSK at the port of import will facilitate trade. Their functions illustratively include:

- Accept Bonds or Bank Guarantee;

- Carry out any other verifications that may be referred by FAGs;

- Defacing of documents/ permits licenses, wherever required;

- Debit of documents/ permits/ licenses, wherever required;

- Handle queries related to assessment; and

- Other functions determined by Commissioner to facilitate trade

The location and timing of the Turant Suvidha Kendras would need to be properly advertised and made known to all stakeholders. The Principal Commissioners/ Commissioners are advised to devise suitable procedures for numbering, handling and safekeep of documents handled in the TSK. This information is also available on CBIC’s website under Taxpayer Assistance under the head: Enquiry Points which is accessible through: https://www.cbic.gov.in/htdocs-cbec/enquiry-points .

B. Virtual Setup

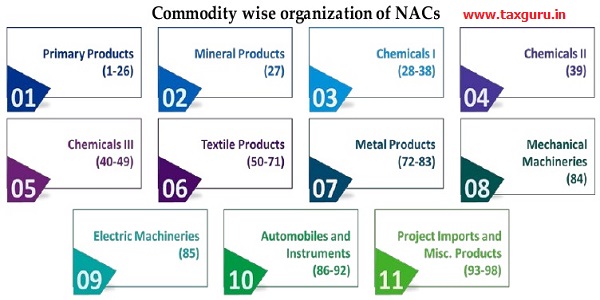

- National Assessment Centres: NACs have been created for the purpose of rollout of faceless assessment. 11 Customs Commissionerates have been partially re-organised as NACs, with all India jurisdiction. NACs are organized commodity-wise according to the First Schedule to the Customs Tariff Act, 1975.

Each NAC will include multiple FAGs. Their mandate will be to examine assessment practices of imported goods across Customs stations and suggest measures to increase uniformity and quality of assessments. Details of the 11 NACs are provided at Annexure 1.

- Faceless Assessment Groups: Officers from different jurisdictions will be brought together on a technology platform to form various FAGs2 for assessment of particular groups in an BE will be assigned to these set of officers who are from different customs locations but are virtually connected.

Their role will require them to verify assessment of any BE that is assigned to their group by the Customs Automated System. Each FAG would have an all India jurisdiction and it may or may not necessarily have a presence in all Customs formations.

The functions of the FAGs will include:

- As is the present practice, may accept the self-assessment or re-assessment of the BE and pass a speaking order3 (unless acceptance is confirmed in writing).

- Providing importers an opportunity of hearing through Query or via video conferencing in case the importer before proceeding with the re-assessment.

- Assessing any BE assigned to them by the Customs Automated System, irrespective of the port where the goods have arrived.

- With the introduction of FAG, the assessment part of the Customs clearance procedure would be delinked with the geographical location where the goods are available for examination.

- The presence of FAG in a Zone is decided based on the import commodities profile of Customs location, quantum of BEs and availability of officers at DC/AC and Appraiser/ Superintendent level.

The Principal Chief Commissioners/ Chief Commissioners of Customs may decide on the total number of officers to be placed in each FAG based on the volume of BEs for their respective zones.

Chapter 3: National Assessment Centres

3.1 This chapter details out the roles and responsibilities of the National Assessment Centres and the Convenors of the NACs. It also presents the coordination mechanism for internal communication as well as external communication, which requires coordination with multiple departments/ agencies.

3.2 Selection and Rationale of NAC: is based on the share of the volume of import of a particular commodity group(s) in its Zone as compared to all India imports and/or share contributed by the said commodity group(s) or the share of import of the particular commodity group(s) in their own Zones.

The rationale for the selection of Conveners for the NAC is its share of all India revenue contributed by the said commodity group(s) or the share of the revenue contributed by the particular commodity group(s) in their own Zones.

3.3 Organization Structure Of NAC

i. Each NAC shall be co-convened by Principal Chief Commissioners/ Chief Commissioners of the Zones.

ii. Each NAC shall consist of Principal Commissioners/ Commissioners of Customs from the Zones.

iii. For each NAC, the Principal Chief Commissioners/ Chief Commissioners, having jurisdiction over the Zones, shall nominate a nodal Principal Commissioners/ Commissioners.

iv. Chief Commissioners will be in charge of different zones. Nodal Commissioners will be responsible for performance of the FAG.

3.4 Functions of NAC include:

i. Monitoring of assessment practices adopted by FAGs

ii. Ensuring uniformity of classification, valuation, exemption benefit and compliance to import policy conditions. Illustratively, this includes:

a. Ensuring that queries raised by FAG are limited to essential queries and that the queries are not raised in a piecemeal manner.

b. Ensuring that First Check is resorted to sparingly. For e.g.:

-

-

- Old and used machinery/capital goods or Old and used goods where examination is integral to determine valuation, classification and other parameters

- Cases of re-import of goods under various exemption notification, which requires establishment of identity.

-

iii. Promotion of adoption of best practices (including international practices) among the FAGs aligned to them

iv. Examining audit objections and take necessary corrective action where required

v. Analysing RMS facilitated BEs pertaining to their industrial sector and advise, the Directorate General of Analytics and Risk Management (DGARM) on necessary interventions

vi. Liaising with Commissionerates on matters of interpretation pertaining to classification,

valuation, exemption and policy conditions

vii. Interacting with sectoral trade and industry for insights and issue resolution

viii. Functioning as a knowledge hub or repository for that industrial sector

ix. Promoting uniformity in assessment by examining orders/appellate orders on assessment practices pertaining to commodities assigned to each NAC and provide inputs for review of such orders

x. Suggesting for policy interventions on commodities assigned to the NAC

xi. Working with National Academy of Customs and Indirect Taxes (NACIN) for design and development of training modules and impart training to officers to promote sector specific specialization

xii. Constituting working groups for matters relating to:

a. Monitoring timely assessment of BE

b. Valuation and related issues

c. Classification and related issues

d. Restrictions and prohibitions and co-ordination with PGAs

e. Communication and outreach strategies

f. Any other matter relevant to uniform and timely assessment

xiii. The working group to monitor timely assessment shall meet virtually on a daily basis. All other working groups shall have weekly virtual meetings.

3.5 Co-convenors of NAC: shall monitor the functioning of the NACs and provide necessary leadership. Crucial responsibilities of NAC Co-conveners include:

i. Nomination of Principal Commissioners/ Commissioners as Members of the NAC from Zones mentioned in column 3 of Annexure 1.

ii. Establishing working groups within NACs for smooth functioning.

iii. Ensuring that NACs develop expertise over the assigned FAGs on different facets of assessment like classification, valuation, prohibitions and restrictions.

iv. Co-ordinating with other Directorates and NACs for functions elaborated subsequently.

v. Making timely recommendations to the Board for policy consideration.

3.6 Coordination among NAC Commissioners: As nodal officers are located in different geographies, institutional coordination is required to surmount teething issues. For this purpose, measures include web meetings to review ongoing performance and de-bottlenecking and weekly consultations to review technical matters of assessment.

Meeting schedule of working groups

In particular it is proposed:

1. Continuous Assessment:

- Endeavour to minimise delay in verification of assessment in case of a holiday for members of a particular FAG.

- This may be achieved by spreading work across multiple locations.

2. Daily Web Meets:

- Working Group on Timely Assessment is encouraged to virtually convene at a pre-scheduled time for a short duration on a daily basis. Particular emphasis must be given to review performance and identification of bottlenecks for appropriate action.

- Working group is encouraged to provide a meeting link to senior officers of CBIC the Chairman, Member Customs, Zonal Member(s), Joint Secretary (Customs), CBIC and co-convenors of concerned NAC, to enable their participation from time to time. Action points from meetings should be collated for compliance. Responsibility of compliance would lie with the relevant Joint Commissioner.

- As far as practically possible, the call should be scheduled at a time when all FAG officers are available and should not interfere with regular duties.

- Subject of each daily meeting should be unique so as to avoid confusion among users. This may include format such as “NAC-FAG-DPC-DD-MM-YYYY”.

3. Weekly Web Meeting: Working groups are encouraged to convene at a pre-determined time, preferably once a week, to review matters of classification, valuation, exemption notifications, prohibitions and restrictions. Focus must be to identify non-uniformity in assessment and encouraging greater uniformity on an on-going basis.

4. Monthly Web Meeting by Co-convenors: are encouraged to interact on a monthly basis, at a minimum, to review the functioning of NACs.

3.7 Coordination of NACs with Other Directorates: will be required on an ongoing basis to

achieve the project’s intended objectives. Given the propensity of teething trouble as the system transitions to a new mode, it is critical that intensity of coordination activities in initial days is high, to allow timely course correction.

- Directorate of Revenue Intelligence (DRI) and Directorate General of GST Intelligence (DGGI) on matters related to management of alerts.

- Directorate General of Valuation (DGoV) to enhance expertise related to sensitive commodities. DGoV shall appoint a nodal person per NAC for effective co-ordination.

- Directorate General of Analytics and Risk Management (DGARM) to provide feedback and enhance RMS and accuracy of Compulsory Compliance Requirements (CCR) instructions.

- NACIN to design and develop training modules and hold capacity building sessions for departmental officers.

- Directorate General of Taxpayer Services (DGTS) to aid in outreach measures by provision of content, faculty for holding webinars, workshops etc.

- Directorate General of Audit (DG Audit) and Audit Commissionerates in relation to audit objections and feedback.

- Directorate General of Systems and Data Management (DG Systems) for resolution of system issues and enhancements.

Faceless Assessment roll out schedule based on date of implementation

| Assessment Group | 1 | 1A | 2-I | 2-II | 2-III | 3 | 4 | 5 | 5A | 5B | 6 |

| Mumbai, Zone II | * | * | |||||||||

| Delhi | * | ||||||||||

| Chennai | * | ||||||||||

| Mumbai, Zone-III | * | ||||||||||

| Ahmedabad | * | * | |||||||||

| Bengaluru | * | ||||||||||

| Kolkata | |||||||||||

| Delhi (P) | |||||||||||

| Meerut | |||||||||||

| Mumbai, Zone I | * | ||||||||||

| Hyderabad | * | ||||||||||

| Tiruchirappalli (Prev.) | |||||||||||

| Patna | |||||||||||

| Thiruvananthapuram | |||||||||||

| Vishakhapatnam | * | ||||||||||

| Nagpur | |||||||||||

| Guwahati | |||||||||||

| Pune | |||||||||||

| Bhopal | |||||||||||

| Bhubaneswar |

NAC roll out schedule based on chapters and convenors

Chapter 4: Process for Faceless Assessment

4.1 Procedure for Verification of Assessment by FAG: From an importer’s perspective, there will be no changes to the process of filing a BE. He/ she will continue to file his/ her documentation including BE and supporting documents4 on the ICEGATE portal.

i. Customs Automated System will assign the BE to a FAG based on an inbuilt logic considering tariff entries in terms of either duty payable or highest assessable value, in that order.

ii. FAG will assess the BE for purposes of duty determination and compliance to restrictions.

Accordingly, it may opt to:

a. assess and verify BE basis documents available in e-Sanchit

b. seek additional information or documents

c. identify BE for examination or testing

iii. In cases where the FAG seeks additional information, communication to and from the importer shall be managed electronically through the system.

iv. On the basis of evaluation and clarification (if any), the FAG may either accept or re-assess

the BE. While re-assessing the BE, it may be ensured that the representation from the importer by way of query may be taken into account. The importer can if he desires waive this requirement.

v. When the FAG re-assesses the BE and an importer disputes such re-assessment, the FAG

shall issue a speaking order.5

vi. While accepting the self-assessment or re-assessing the BE, the FAG may provide instructions for 2nd check examination of goods along with directions to shed officers at the Port of Import.

vii. Illustratively, instructions may include verification of originals, defacement of documents, taking custody of certain documents, seeking NoC from PGAs etc.

viii. Where authenticity of a document is in doubt and verification by an external agency is required, the same shall be communicated to shed officers at the Port of Import, for necessary action.

ix. Requests for storage of imported goods in warehouse pending clearance or removal6 shall be processed via the TSK.

x. Any assessment/ speaking order passed by FAG, shall be appealable to the Commissioner of Customs (Appeals) at the Port of Import.

4.2 For Examination/ Testing

i. If the FAG deems it fit to order examination/ testing of goods for the purpose of assessment it shall coordinate the same with the shed officer at the Port of Import.

ii. Instructions for 1st check examination/ testing of the goods with specific directions of testing parameters should be communicated to the shed officers.

iii. Onus of sending samples to the laboratory (with the requisite test memo) would lie with the shed officers and the TSK.

iv. Results of examination/ test report would be fed by shed officer in the system and referred to concerned FAG.

v. In case goods are confirmed to be in violation of some restriction/ prohibition before or during assessment on the basis of examination/ test report or otherwise, the FAG shall refer such BE to the PAG at Port of Import for adjudication and assessment.

4.3 Re-Assessments: In case of the need for re-assessment, the re-assessment in different situations would be carried out in the following manner :

1. Before OOC, where request is made by Importer and change in assessment is requested, the same may be referred to FAG for consideration.

2. Before OOC, where request is made by Importer and change in details other than assessment is requested including consequential amendment related to short-shipments, changes in bond conditions, etc. may be carried out by PAG.

3. Before OOC, if reassessment to be done suo-moto by Customs for any reason, may be carried out by PAG.

4. After OOC, reassessment to be done for any reason may be carried out by PAG.

A graphic is placed at Annexure 3 which presents the cases of re-assessment including ones consequent to amendments.

4.4 First Check Examination: Faceless assessed BEs after 1st check examination will come back to the FAG on ICES only for completion of assessment. Examination officers in respective Port of Imports may be guided that 1st check BEs of FAGs may be marked back only to Virtual Assessment Officer(VAO)/ Virtual Deputy Commissioner (VDC)7, after examination, with detailed examination report to effectively assist FAG in assessment. Similarly, if any BE is to be sent back after 2nd check examination, the same may be marked only to the assessment group at the Port of Import, i.e. Appraiser as provided in the instructions.

Note: For the purpose of uniformity and ensuring timely assessment across FAGs, 1st Check should typically be resorted to in the following situations:

i. Old/ used machinery/ capital goods provided the inspection/ appraisement report from the country of export is unavailable in prescribed format/ is not produced at all/ is insufficient.8

ii. Old and used goods only where examination is essential to determine valuation, classification, and other parameters.9

iii. Articles of jewellery, precious metals, imitation jewellery where valuation must be ascertained by a jewellery expert.

iv. Cases of re-import of goods under various exemption notification, which requires establishment of identity to the satisfaction of Deputy Commissioner/Assistant Commissioner of Customs.

4.5 Provisional Assessment

i. If the requisite approval for provisional assessment as per the Customs Act 1962 and department guidelines has already been obtained, the FAG may assess the BE provisionally.

ii. In other cases, FAG may forward the BE citing reasons for the same and refer the BE to the PAG at the Port of Import.

iii. In case the importer opts to move the goods to a warehouse u/s 49, such request shall be processed by the TSK at the port of import.

iv. Shed officers at the Port of Import would conduct necessary verification / examination, as required by the FAG or required as per Compulsory Compliance Requirements (CCR) of RMS.

4.6 Exercise of powers in exceptional circumstances by the Commissioner of Customs and Assessment by PAG

i. In select cases of provisional assessment, Special Valuation Branch (SVB) valuation and multiple queries, the FAG may re-direct the BE to PAG using CAS with the approval of JC/ ADC and in exceptional circumstances with the approval of the Commissioner (explained in detail in Instruction 09/ 2020, para 5.3.2). The reasons for the same will be recorded in writing on the ICES application.

ii. In case of violation found after the assessment is completed (including second check examination), the BE may be directed only to PAG for adjudication and assessment.

iii. The Commissioner of Customs at Port of Import may override extant processes and direct the assessment to be conducted by the PAG at the port of import in certain cases. The reasons for the same will be recorded in writing. These may include cases where a specific alert/ intelligence is available pertaining to a consignment.

In ICES, a role VDN has been created which can be allotted to the JC/ ADC in-charge of FAG. The option to push a BE from FAG to Port of Import in exceptional circumstances as given in the Board’s Instructions is also available with the VDN role. The option to pull a BE from FAG to the Port of Import is available in the ADN role at the Port of Import. Both, the pull as well as push functionalities should be used only in exceptional scenarios and with due approval JC/ ADC in respect of situations stipulated in the Instruction and in any other case, with the approval of the Commissioner. For pulling BE out of FAG, Pr. Commissioner/ Commissioner is authorised and in case where OOC is yet to be given, FAG officers (Superintendent/ AO) are authorised for recall of BE. Further, the facility to reallocate BE from one officer to another officer is available in the VDN role.

4.7 Presenting Of Documents With TSK

i. If the importer is required to execute a bond or bank guarantee, the same be coordinated at the TSK at the Port of Import, preferably before filing of BE.

ii. Certain documents need to be presented in hard copy, beside uploading on e-Sanchit (such as Certificate of Origin) and the same be submitted to TSK for validation

ICES has been equipped to perform tasks associated with TSKs in implementing Faceless Assessment, A new role TSK_OFF is being introduced for assisting TSK officers in conducting designated tasks in System. The role currently can be used for Bond Registration, Bond Debit and Defacement of supporting documents, wherever required. While all the supporting documents will be available in System for the TSK officer to check, it may be ensured that physical copies are seen only for those documents where defacement is desired, like Country of Origin Certificates. The TSK officer can select such document in the System to see what has been uploaded by the importer in e-Sanchit and mark it as defaced in System after verifying and defacing the original paper copy. Once captured in the system, the same is also visible to OOC officer while granting OOC/ PCCV along with all other supporting documents.

4.8 Appellate Proceedings

Board has issued Notification No.85/2020-Customs (N.T.) dated 4th September 2020 by virtue of which the Commissioners of Customs (Appeals) are empowered to take up appeals filed in respect of Faceless Assessments pertaining to imports made in their jurisdictions even though the Faceless Assessment officer may be located at any other Customs station. To illustrate, Commissioners of Customs (Appeals) at Bengaluru would decide appeals filed for imports at Bengaluru though the Faceless Assessment officer is located at any other port of the country, say Delhi.

4.9 Review Proceedings

The review of any speaking order on re-assessment passed by a proper officer of Faceless Assessment Groups, under sub-section (2) of Section 129D of the Customs Act 1962, shall lie with the reviewing authority having administrative control over the that proper officer of the Faceless Assessment Group.

4.10 Electronic Communication

i. All communication whether (i) external i.e. between FAG and the importer or (ii) internal, i.e. between FAG and the officers of TSK or jurisdictional Commissionerate shall be exclusively by electronic medium.

ii. Electronic communication is to be authenticated by the originator by affixing his Digitally Signed Certificate( DSC).

iii. Communication initiated by a non-customs individual such as the assessee or his representative may use e-sign or other mode of electronic authentication.6F10

4.11 Amendments

i. Once amendments are filed online, the Customs Automated System would queue them before the proper officer of the FAG if the BE is pending for verification. In all other cases, the request would be queued to the proper officer of the PAG.

ii. The facility of online levy of amendment fees as per Levy of Fees (Customs Documents) Regulations, 1970 has also been enabled. The applicable fee would be included in the duty challan for payment.

iii. Requests for amendments11 and requests after the BE has been returned for payment by FAG shall be forwarded to FAG, if change in assessment parameters is requested, or otherwise continue to be dealt with by PAG. It is clarified that, all amendments after OOC may continue to be dealt with by PAG.

4.12 Demands under Section 28 of the Customs Act 1962

Issuing of demands under Section 28 of the Customs Act 1962, adjudication thereof and handling of audit objections shall be done by the officers of the port of import. In matters where clarifications and inputs are required to be given by the Faceless Assessment Groups to the Port of Import, the nodal Commissionerates as in para 4 above shall co-ordinate with the ports of import.

Chapter 5: Key Considerations for Faceless Assessment

The Nodal Commissioners in the NAC shall co-ordinate to ensure that Faceless Assessment is implemented smoothly and creates no disruption in the assessment and clearance of goods. The following measures may be undertaken by the NAC:

5.1 Identification of Location of FAG

i. NACs have identified Customs locations within each Zone, where Faceless Assessment pertaining to a group would be undertaken. The volume of import and availability and experience of officers was considered for this purpose.

ii. It is critical to note that setting up adequate number of FAGs in a zone with sufficient number of officers is one key area which will enable faster disposal and more timely assessment

5.2 Uniform Assessment Practices

i. Consider audit objections, judicial and quasi-judicial decisions accepted by the Department relating to the assessment of the goods to be handled by the FAG under the concerned NAC and circulate among the officers

ii. Identify variations, if any, in assessment practices and harmonise them for application across FAGs for uniformity of assessment.

iii. Ensure that imported items are properly declared along with full details to ensure proper classification and eligibility for notification benefit.

iv. Keep track of all instances where the description is falling short of requirement and report the same in a monthly bulletin for the benefit of importers and customs brokers.

v. Study present assessment practice concerning major commodities in the Groups being imported at customs station and being assessed by them.

vi. Ensure uniformity in classification, valuation, exemption benefits, and compliance with import policy conditions

vii. Endeavour to reduce incidence of queries and issue public/ trade notices from time to time to sensitise trade on good practices required to reduce incidence of queries. For e.g. sensitizing trade to provide complete details and description of a commodity such as brand name, model and any other specifications essential for the assessment

viii. FAG officers shall make use of WCO explanatory notes, Classification decisions, Classification opinions available on WCO website.

ix. Maintain valuation circulars issued by DGOV regarding goods covered under the Groups and ensure valuation is in line with issued alerts.

x. Access to the National Import Data Base (NIDB) should be taken by FAG officers and they may resort to verification of valuation and classification of an imported product in the National import database.

xi. List demands raised u/s 28 against an importer by DRI or other agency (apart from audit objections on classification, exceptions etc.) relating to goods covered under the group during the last 5 years and ensure that the assessment is done after considering the precedents contained in the said cases/ audit objections.

xii. RMS instructions may be complied with.

xiii. Whenever RMS instructions are not related to imported goods in a BE, same shall be recorded and shared with Commissioner on a daily basis.

5.3 Conference on Tariff and Other Customs Matters

Joint Secretary, Customs, CBIC would be responsible for coordinating with the NACs in organizing a Conference on Tariff and Other Customs Matters every 6 months to review the functioning of the NACs and FAGs. The Conference would be chaired by Member (Customs).

5.4 Exchange of Port Specific Practice and Procedures

i. FAG officers shall share the list of sensitive commodities and knowledge with regard to sensitive items that are traded from their respective port of jurisdiction with FAG officers of other zones to enhance uniformity and reduce dwell time of assessment.

ii. FAG officers shall share valuation practices among different FAGs of respective zones for clarity and uniformity in assessment processes.

iii. The Nodal Commissioners shall work in tandem with all nodal Commissionerates assessing the same chapter, to ensure that best assessment practices are in place for the group which will be the norm pan India.

iv. The knowledge management shall be kept at central level that will be accessible to all FAGs

5.5 Capacity-building Amongst Officers

i. Officers shall be selected based on experience in assessment and aptitude. Faceless Assessment Group is an expert group of officers in the chosen assessment group. Hence, officers shall be identified with domain experience and technical knowledge.

ii. Necessary training shall be imparted to the officers in consultation with NACIN. The objective of the Training is to ensure not only that they understand the EDI Protocol involved in Faceless Assessment but also to ensure that they take up the responsibility of development of the NAC for the group allotted to them.

iii. FAG assessing officers should be provided and encouraged to use listed tools regularly:

-

- Valuation Bulletins (issued by DGoV)

- NIDB data

- Valuation practice adopted at various ports

- Board circulars on classification

- Compendium of relevant case laws relevant for classification

- CAG paras on classification

- Advance rulings (especially on IGST matters), modus operandi/ alert circulars.

iv. Development of a compendium of assessment practices for easy access and reference of the officers.

5.6 Time sensitive consignments

i. The Port of Import shall monitor clearance of time-sensitive consignments (illustratively lifesaving drugs, items associated with national security matters or defence.)

ii. On a need basis, the Port of Import shall facilitate early assessment with concerned NAC for early release.

iii. Traders may be advised to indicate end use of such consignments in the BE for easier identification of such consignments.

iv. DG Systems will facilitate a functionality to alert relevant officers for FAG and PAG, if such consignments are pending for more than four hours.

5.7 Working days

i. All Saturdays (except second Saturdays) will be working days for all FAGs.

ii. Co-Convenors of the NACs must co-ordinate with the NACs for ensuring expedited assessment by the FAGs/PAGs across different zones to enable minimal delays in assessment and Customs clearance during holidays at all or some locations.

iii. Co-convenors of the NACs may require NACs to draw up official rosters among FAGs/ PAGs to ensure adequacy of officers on the basis of volume of BEs (for processing on Sundays and other holidays including second Saturdays.)

Chapter 6: Performance Measurement

This chapter lays downs the guidelines for performance management of Faceless Assessment and key metrics which are to be maintained by FAGs. The existing analytics view provided to them have also been discussed. Further, the impact analysis framework for continuous improvement has been laid down.

Principal Commissioners/ Commissioner of Customs shall be administratively responsible for monitoring and ensuring fast and uniform assessments in their respective zones. For this purpose of monitoring and measuring the impact of Turant Customs initiative, the following measures have been identified for monitoring impact of the initiative:

6.1 Monitoring Disposal Rate Through Dashboard:

- Disposal rate should be monitored ensuring nil pendency of BE having processing time of more than 5 hours

- JC in charge shall furnish clarification if assessments are pending for >5 hours

- Dashboard access will be provided in COM role for the Pr. Commissioner/ Commissioner to monitor pendency and processing of BE assigned by the CAS to FAG under their Jurisdiction.

- A virtual dashboard where status of BE pertaining to respective Port of Import but assigned to FAG at any port will also be accessible.

- The status reports are available in VDN, VDC and VAO roles also for the FAG officers to act accordingly.

Dashboard for NAC Commissioner

The monitoring mechanism established by PC/ CC is critical for timely and hassle-free implementation and fixing and monitoring timelines.

Virtual Assessment receipt and disposal

Target – Pendency Summary

–

6.2 Implementation Of Guidebook: The Joint Commissioner may be designated for ensuring the implementation of Turant Customs process and meeting Key Performance Indicators.

6.3 Maintenance Of Records – Indicative list of reports maintained by some FAGs to monitor the key performance indicators are given below for reference:

| S. No. | Description | Chapter |

| 1 | No. of BE Assessed By FAG | |

| 2 | No. of Bills in which the Assessment is modified by FAG | |

| 3* | No. of BE in S.No.2 above in which the importer agreed with re-assessment by FAG | |

| 4* | No. of BE in which Speaking Order is issued/ under process | |

| 5 | No. of BE in which query raised by FAG | |

| 6 | No. of BE ordered for first check | |

| 7* | No. of BE in which RMS instructions are not relevant | |

| 8 | No. of BE returned to PAG by FAG |

*These reports are currently not available on the system and have to be prepared manually

- In respect of S. No. 2, List of BE together with issue in brief to be furnished fortnightly to Commissioner together with remarks whether interdictions to be inserted in RMS as per following format

| S. No. | BE No. and BE date | Port of Import | Chapter | Issue in brief for which assessment was modified | Suggested interdiction in RMS |

| 1 |

- In respect of S. No. 5 and 6, Joint Commissioner ICD to review all BEs and reasons for query/ first check on a fortnightly basis.

- In respect of S. No. 7 fortnightly report along with details of each BE and issue in brief to be submitted to Commissioner as follows

| S. No. | BE No. and BE date | Port of Import | Chapter | No. of RMS instruction that are not relevant |

- In respect of S. No. 8, weekly report along with the details of each BE and issue in brief to be submitted to the Commissioner as per the following template:

| S. No. | BE No. and BE date | Port of Import | Chapter | Reasons for which BE is returned to PAG | Remarks |

| 1 |

6.4 Grievance Redressal Under Faceless Assessment: All TSKs to maintain record of incident raised regarding faceless assessment and furnish the same to Commissioner for the purpose of monitoring. The following template shall be maintained for record management:

A. Overall Grievance Record Management

| Description (Ref: cases pertaining to Faceless Assessment to be considered) | No. of Tickets |

| Total no. of Grievances raised | |

| Total no. of Grievances open | |

| Total no. of Grievances closed |

B. Monitoring of Grievances

| S. | Ticket | Ticket | Contact | Status | Pending | Resolution | Remarks, |

| No. | No. | Details | details (Name/ Email/ Phone) if available | (Closed/ Follow up) | with whom (in case of follow up case) | (in case of closed case) | if any |

| BE No. | Closed/ | ||||||

| Date | Open | ||||||

| Location |

6.5 Impact Analysis

The Board will review outcome of Faceless Assessment and all NACs every month. For this purpose, DG Systems will issue standard reports for reviewing measurable parameters. The Impact Analysis of the NACs shall be done in the following manner:

1. Benchmarking Through Mini TRS

- Ensure that Overall Clearance is in line with National Trade Facilitation Action Plan (NTFAP) targets – 48 Hours for Seaports/ ICDs – 24 Hours for Airports (for imports)

- Ensure that Faceless Assessment is undertaken in 5 hours (excluding 8 PM – 8 AM). NACs may be ranked on this criterion.

2. Turant Readiness Matrix

Identify parameters to reflect Readiness for Turant Customs including:

- % of Advance BE Filed

- % of Late Fee

- % of Multiple Queries

- % of Online Amendments

- % of Web based Goods Registration

- % of Disposal within time as FAG

3. Clearance Statistics

A dashboard shall be made available to NAC Conveners to monitor pendency and processing of BE assigned to FAGs under their jurisdiction and under other NAC Conveners.

Chapter 7: Communication and Outreach

This chapter showcases the communication and outreach steps to be taken by FAG and Zones with DGTS as the key coordinator. The chapter also presents the need for involvement all important stakeholders in adoption of Faceless Assessment and its improvement through social media platforms, continuous engagement, etc.

7.1 A robust outreach programme is essential to manage change brought in the new Customs system to ensure easy acceptance by stakeholders including – traders, customs brokers, port authorities, etc. For this purpose, NACs will work with DGTS for conducting an outreach programme.

Illustrative communication and outreach plan

7.2 Each Zone will create an annual outreach plan involving all relevant trade stakeholders.

As part of the outreach strategy, the following activities will be undertaken:

a. Organize workshops at Customs formations to generate awareness about Turant Customs – to explain the new structure, process, requirements and benefits.

b. Undertake online webinars to regularly engage with trade to share key information regarding the new customs process.

c. Prepare and share advertisements, leaflets, teasers, etc. related to Turant Customs with officers, importers, etc.

d. Engage with trade through CBIC’s social media handle using Turant Customs logo as a differentiator for wider outreach by sharing posts on Facebook/ tweets on Twitter and ensure re-tweets by key handles – Finance Minister, other concerned Ministries – Commerce and Industry, Shipping, Industry Associations etc.

e. Carry out quarterly surveys to access the difficulties faced by trade stakeholders and map the concerns raised over time

f. Include agenda of Turant Customs in Permanent Trade Facilitation Committee (PTFC)/ Customs Clearance Facilitation Committee (CCFC) meetings and ensure that every zone publishes performance figures for these on their respective portals

g. Conduct perception surveys using social media handles to analyse the impact of Turant Customs (by way of queries raised and feedback obtained on the initiative, social media analytics, etc).

Chapter 8: Frequently asked Questions- on Faceless Assessment

General Questions

Q.1 What is Faceless Assessment?

Ans. Faceless Assessment is a major Customs Reforms where a Bill of Entry that is identified for scrutiny (non-facilitated Bill of Entry) is assigned to an assessing officer who is physically located at a Customs station, which is not the Port of Import in the Customs Automated System. It separates the assessment process from the physical location of Port of Import, using a technology platform.

Q.2 What are the functions of the Faceless Assessment Group?

Ans. With the introduction of FAG, the assessment part of the Customs clearance procedure would be delinked with the geographical location where the goods are available for examination and instead be executed by the FAG. The functions of the FAGs will include:

- As is the present practice, may accept the self-assessment or re-assess the BE.

- Before Re-assessment, provide importers an opportunity of being heard via Query or video conferencing and in case the importer does not agree with the same, pass a Speaking Order.

Q.3 To whom can I raise grievances/ enquiries/ feedback related to Faceless assessments?

Ans. For system related issues, first point continues to be ICEGATE Helpdesk (https://www.icegate.gov.in/contact_us.html). For other issues, every Port of Import has to set up Turant Suvidha Kendra to redress grievances related to delay in clearances including Faceless Assessment. The contact details are available in https://www.cbic.gov.in/htdocs-cbec/enquiry-points. Further, an officer at the rank of Additional Commissioner/ Joint Commissioner is also designated at each port to take care of timely redressal of grievances and escalation.

Q.4 What is the jurisdiction of the Faceless Assessment Group?

Ans. There is no territorial jurisdiction assigned to FAG. Each FAG would have jurisdiction over the Bills of Entry assigned in the system to FAG, irrespective of the same being filed anywhere in India.

To illustrate, a Bill of Entry pertaining to NAC on primary products can be assigned to any of the FAG officer of the Zones listed in Annexure II of Circular No. 45/2020-Customs dated 12.10.2020.

Q.5 What is the target time for faceless assessment of a Bill of Entry?

Ans. All FAGs will aim to ensure that Faceless Assessment is undertaken in 5 hours (excluding 8 PM – 8 AM).

Q.6 What are the functions of the Port Assessment Group at the Port of Import under faceless assessment?

Ans. The PAG will be responsible for all functions which were earlier carried out prior to faceless assessment, except the assessment functions and approvals of assessments impacting amendments which would be carried out by FAG.

Q.7 What are the functions that can be carried out at a Turant Suvidha Kendra?

Ans. Turant Suvidha Kendras at the Port of Import will be responsible for all documentary processes requiring physical submission / verification at the Port of Import. Illustratively, their functions include:

- Accept bonds or Bank Guarantee;

- Carry out any other verifications that may be referred by FAGs;

- Defacing of documents/ permits licenses, wherever required;

- Debit of documents/ permits/ licenses, wherever required;

- Handle queries related to assessment; and

- Other functions determined by Commissioner to facilitate trade

Q.8 Is there a mechanism for monitoring grievances in TSK ?

Ans. All TSKs are required to maintain a record of grievances raised regarding Faceless Assessment and furnish the same to concerned Additional/Joint Commissioner for the purpose of monitoring. The template of grievance management is provided in chapter 6 of this guidebook.

Q.9 How will different NACs coordinate?

Ans. NACs will coordinate through a robust institutional coordination across levels by means of:

i. Daily web meetings of Working Group on Timely Assessment to review performance and identification of bottlenecks for appropriate action

ii. Weekly web meetings of working groups to review matters of classification, valuation, exemption notifications, prohibitions and restrictions to identify non-uniformity in assessment and encouraging uniformity on an ongoing basis.

iii. Monthly web meetings by co-convenors to review functioning of NACs.

Q.10 How can I minimise the queries for my Bills of Entry ?

Ans. Providing complete description of the Goods imported along with catalogue/ technical literature, if needed while filing Bill of Entry would reduce the need for query.

Assessment related

Q.11 During assessment, if FAG determines the requirement of first check examination of cargo, verification of documents or testing how will the same be undertaken?

Ans. FAG may seek First Check and send it to in the Port of Import with appropriate Examination order. The officers of the Port of Import shall be responsible for carrying out such activities as per instructions provided by FAG and reporting their findings on the system to FAG.

Q.12 Who will finalize the provisionally assessed bills of entry assessed by faceless assessment groups? FAG or PAG?

Ans. This is covered in para 5.8 III of instruction no. 09/2020 Customs dated 05 June 2020. The finalisation of Provisional Assessment will be done by PAG.

Q.13 In case testing of consignment is required, who will be responsible for the same?

Ans. If FAG communicates the need for testing, shed officers shall be responsible for sending samples to the laboratory along with the required test memo.

Q.14 Where will my appeal against any assessment order heard?

Ans. An appeal against an assessment/ speaking order shall lie before the Commissioner (Appeals) having jurisdiction over the Port of Import, irrespective of the officers assessing the Bill of Entry. For example, Commissioners of Customs (Appeals) at Bengaluru would decide appeals filed for imports at Bengaluru though the FAG is located at Delhi.

Q.15 What is the procedure to be followed by FAG for effecting changes in the self-assessment?

Ans. The FAG will provide the importer an opportunity of being heard through Query or via video conferencing before proceeding with the re-assessment.

In case the importer does not agree with the re-assessment, a Speaking Order will be passed by FAG as per Section 17(5) of the Customs Act, 1962.

Q.16 If my BE is pending at FAG and the concerned officer is on leave, who will take up the assessment in his absence, and can the trade be assured that the Bill of Entry will not be pending in his absence?

Ans. The Supervisory Officers at FAG location will ensure that the BE is attended to by other officer in his absence. The Dashboards/ SMS Alerts have been put in place for timely action.

Amendment related

Q.17 What is the process of amendment in Bill of Entry before assessment?

Ans. An amendment request by Importer can be filed directly either through ICEGATE Portal or through service centre at the Port of Import, which will be routed to the concerned FAG for approval/ rejection. No prior approval of PAG is required in these cases.

Q.18 What is the process of amendment of Bill of Entry when requested by Importer after assessment?

Ans. There can be two situations:

Before OOC, once amendments are filed through ICEGATE/Service Centre, the Customs Automated System would queue them before the proper officer of the FAG if it impacts Assessment. In all other cases, the request would be queued to the proper officer of the PAG.

Further, In case of any difficulty, PAG officer will look into it, including recalling the and sending it to FAG.

The cases of amendment which are filed after issuance of OOC shall be handled by PAG.

The graphic below presents the case for easy understanding:

Q.19 If case of short-shipment/ short landing, where will the amendment be done ?

Ans. The PAG will do the amendment of the same. The submission of amendment requests may be done either through ICEGATE or Service Centre.

Q.20 What is the mechanism for FAG to view the BE pending for assessment which is to be amended?

Ans. The list of Bills of Entry pending in Amendment Queue is available in the dashboard of the officer. Additionally, periodical SMS Alert is also being sent for timely action.

Others

Q.21 How is disposal rate of faceless assessment being monitored?

Ans. Disposal rate should be monitored ensuring nil pendency of BE having process time of more than 5 hours. A dashboard is made available to Principal Commissioner/ Commissioner of the FAG to monitor pendency and process of BE. The summary statistics is also available in VDN, VDC and VAO roles for the FAG officers to act accordingly.

Q.22 What is the procedure in case Bill of Entry has to be deleted? Who will be responsible for the same?

Ans. As clarified in Q6, the PAG would continue to handle all such requests pertaining to the Bills of Entry.

Q.23 Who will recall RMS facilitated bill of entry?

Ans. As clarified in Q6, the PAG would continue to handle all such requests pertaining to the Bills of Entry.

Q.24 If I need to request Customs to condone delay in filing Bill of Entry as per Section 48, who should I approach and what is the procedure

Ans. As clarified in Q6, the PAG would continue to handle all such requests pertaining to the Bills of Entry.

Q.25 Who will accept my Bond/ BG in case it is needed ?

Ans. In case of Export Promotion Schemes, Project Imports, National Bond/ BG will be accepted at any Customs location across India for subsequent utilisation at any other locations. In all other cases, the Bond/ BG will be accepted at the Port of Import.

Q.26 Who will determine the value of BG in cases it is needed? Who should be for change in in the Bond Conditions ?

Ans. The PAG will be responsible for determining the value of BG and also carry out any changes in the Bond conditions of Bill of Entry including change in BG value/ rate. However, it is clarified that, if the Bond details are provided correctly in the Bill of Entry, there would be no requirement for changes subsequently.

Q.27 Are importers required to submit hardcopies of original Certificate of Origin (COO) issued under Free Trade Agreements?

Ans. Yes. It should be submitted to TSK for defacing in addition to uploading the same in e-Sanchit. It is clarified that, in general, submission of hardcopies of supporting documents has been done away with. However, since COO is required as part of International Agreements, the same may be presented in TSK for defacement or validation. (refer Circular No.45/ 2020-Customs, dated 12th October 2020).

Download Full Text of Guidebook for Faceless Assessment with Annexures