CA Vipul Khandhar

♠ GST TRAN 1 is a declaration to be filed electronically, to claim various transitional credits admissible. The same is to be filed on or before 28.09.2017. On the recommendations of the GST Council, the time can be extended by another ninety days.

♠ There are no provisions enabling filing of revised GST TRAN 1.

♠ Being a manufacturer service provider registered under Excise law and not availing SSI exemption; having turnover during 2016-17 was Rs. 75 lakhs and intends to opt for composition scheme under GST. Then one cannot carry forward the cenvat credit balance as per last E-1 return to GST.

♠ GST TRAN 1 can be filed, only after filing last 6 months returns of Excise, Service tax and VAT law.

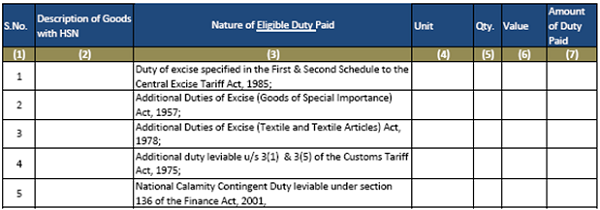

♠ Education CESS Credit and Secondary and Hither Education CESS credit as per ER 1 / ST 3 return will not be carried forward in GST as it is not covered by definition of “eligible duties and taxes” under Section 140 of the CGST Act.

♠ The closing balance in the returns of earlier laws would not be automatically transferred to GST regime. For this purpose, we have to file a Declaration GST TRAN 01, within 90 days from 01.07.2017, i.e. on or before 28th September 2017.

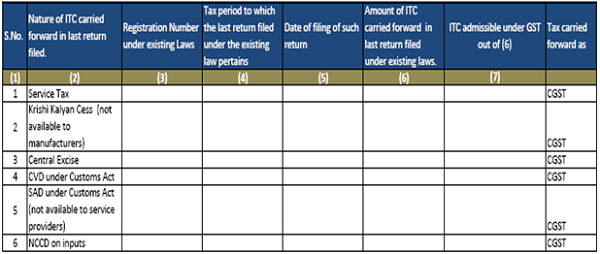

♠ The details of closing balance as per the last return under the existing laws shall be indicated in column 5 (a) of GST TRAN 01. Upon filing of the said GST TRAN 01, the credit would be closing balance of credit under ER-1 / ST-3 would be credited to the Electronic Credit Ledger under GST, as CGST credit. Similarly, the credit under VAT return would be credited to the Electronic Credit Ledger under GST, as SGST Credit. Section 140 (1).

SECTION 140 (1):

♠ ITC is available for Normal Goods and Services

♠ ITC of only those taxes which are shown as carried forward in the last return filed by the dealer.

♠ This Part is to be filed in respect of only those taxes for which the dealer is registered under exisitng laws. (eg. VAT/Excise/Service Tax etc.)

♠ This section applies to all Persons registered under GST (EXCEPT Composition dealers under GST laws.)

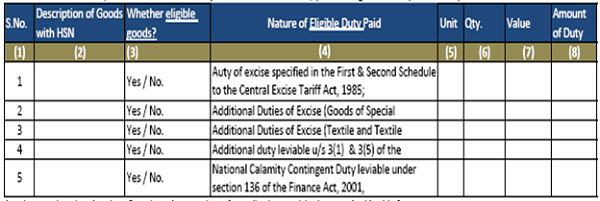

♠ Clause – 5 (a):

It reflects closing balance of cenvat credit as per last ST-3 return or ER-1/ER-3 excise return for the month/quarter ended june-2017.

AS PER SECTION 140 (1):

(1) A registered person, other than a person opting to pay tax under section 10, shall be entitled to take, in his electronic credit ledger, credit of the amount of Value Added Tax, and Entry Tax, if any, carried forward in the return relating to the period ending with the day immediately preceding the appointed day, furnished by him under the existing law in such manner as may be prescribed.

The following conditions have to be satisfied.

(i) The said amount of credit is admissible as input tax credit under this Act;

(ii) The claimant has to furnish all the returns required under the existing law for the period of six months immediately preceding the appointed date;

(iii) The said amount of credit should not relate to goods manufactured and cleared under such exemption notifications as are notified by the Government.

- In Column 5 (b) of GST TRAN 1, the details of various forms (Form C / F / H / I) received from April 2015 to March 2017 have to be declared. It may be noted that mere details of the forms received have to be declared here, which means that to this extent ITC is protected.

- In column 5 (c) of GST TRAN 1, the total amount of ITC available as per the last VAT return has to be indicated. From that the following amounts have to be reduced.

- Differential tax payable for the Forms pending as on 01.07.2017.

- Proportionate ITC attributable to such pending forms.

- The balance credit can be carried forward.

- As and when the pending forms for which ITC has been reversed / differential tax has been paid as above, refund can be claimed.

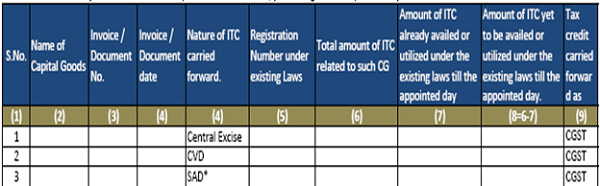

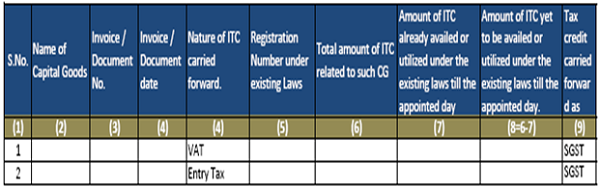

SECTION 140 (2):

- It covers unavailed ITC on Capital Goods

- ITC of only those taxes which are shown as carried forward in the last return filed by the dealer.

- This Part is to be filed in respect of unavailed tax credit of Capital Goods which is not shown in last return filed.

- This section applies to all Persons registered under GST (EXCEPT

- Composition dealers under GST laws.)

- If one has not availed any cenvat credit for the capital goods received during April 2017 to June 2017, then the entire duties paid on such capital goods can be claimed in July 2017, by filing GST TRAN 01.

- Purchase of Goods Transport Vehicle (Lorry) fall under Chapter heading 8704 of the Central Excise Tariff and are not eligible for credit under existing law. In order to claim transitional credit under Section 140 (2) for capital goods under GST, such credit should be admissible under both existing law and GST law.

- One of the conditions for availing ITC under GST is that no depreciation should be claimed under Income Tax, on the duty portion which is claimed as ITC. If anyone has not claimed cenvat credit earlier, one would have already claimed depreciation, by including the duty portion also in the value of such capital goods. Hence, one would not be entitled to avail any ITC on such capital goods, under GST.

- Being a manufacturing unit; if anyone has availed 50 % of the duties paid on capital goods received during April-June 2017 already in ER-1 returns; then one can take the remaining 50 % of the credit in July 2017. The details of such credit has to be indicated in column 6 (a) of the GST TRAN 01 in respect of Excise duties / CVD / SAD and in column 6 (b) of the GST TRAN 01 in respect of VAT paid on such capital goods.

CLAUSE 6 (a):

CLAUSE 6 (b):

SECTION 140 (3):

- It covers ITC on Normal Goods

- ITC of only those taxes which are shown as carried forward in the last return filed by the dealer.

- This Part is to be filed all by Persons registered under GST laws, who were:

– not liable to be registered under the existing law; or

– exclusively engaged in the manufacture of exempted goods ; or

– exclusively engaged in the provision of exempted services; or

– providing works contract service and was availing of the benefit of service tax notification No. 26/2012; or

– first stage dealer; or

– second stage dealer; or

– registered importer; or

– depot of a manufacturer; or

– exclusively engaged in the supply of exempted goods (SGST Act)

i.e. persons who were not eligible to claim ITC in respect of their inputs under one or the other existing laws.

AS PER SECTION 140 (3):

- A registered person, who was not liable to be registered under the existing law or who was engaged in the sale of exempted goods or tax free goods, by whatever name called, or goods which have suffered tax at the first point of their sale in the State and the subsequent sales of which are not subject to tax in the State under the existing law but which are liable to tax under this Act or where the person was entitled to the credit of input tax at the time of sale of goods, if any, shall be entitled to take, in his electronic credit ledger, credit of the value added tax and entry tax in respect of inputs held in stock and inputs contained in semi finished or finished goods held in stock on the appointed day subject to the following conditions, namely:–

(i) such inputs or goods are used or intended to be used for making taxable supplies under this Act;

(ii) the said registered person is eligible for input tax credit on such inputs under this Act;

(iii) the said registered person is in possession of invoice or other prescribed documents evidencing payment of tax under the existing law in respect of such inputs; and

(iv) such invoices or other prescribed documents were issued not earlier than twelve months immediately preceding the appointed day:

- Provided that where a registered person, other than a manufacturer or a supplier of services, is not in possession of an invoice or any other documents evidencing payment of tax in respect of inputs, then, such registered person shall, subject to such conditions, limitations and safeguards as may be prescribed, including that the said taxable person shall pass on the benefit of such credit by way of reduced prices to the recipient, be allowed to take credit at such rate and in such manner as may be prescribed.

SECTION 140 (4):

- ITC on Normal Goods

- where such goods or services which are though now exempt BUT would be liable to tax under GST. i.e. credit reversed under Rule 6(3) of Cenvat

- Credit Rules 2004, can be reclaimed in respect of goods held as on appointed date.

- This Part is to be filed all by Persons registered under GST laws, who were:

– engaged in the manufacture of partly taxable & partly exempted goods under the Central Excise Act, 1944.

– engaged in the provision of partly taxable & partly exempted services under Chapter V of the Finance Act, 1994,

CLAUSE 7 (a):

CLAUSE 7 (b): Available only to trader (On Inputs only)

SECTION 140 (5):

- ITC on Normal Goods and Services

- This Part is to be filed all by Persons registered under GST laws, where:

Goods or Services received on or after the appointed day but the duty or tax in respect of which has been paid by the supplier under the existing law.

SECTION 140 (6):

- ITC on Normal Goods

- For Composition dealers under VAT & Excise

- This Part is to be filed all by Persons registered under GST laws, who:

who was either paying tax at a fixed rate or who was paying a fixed amount in lieu of the tax payable under the existing law (Excise, Customs, National calamity contingent Duty, VAT)

SECTION 140 (8):

- Cenvat Credit by person having Centralized registration

- Who are claiming Cenvat credit held under centralized registration of existing laws as on the appointed day.

SECTION 141:

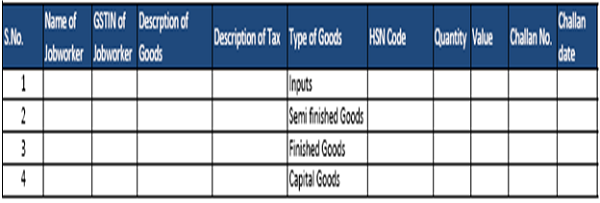

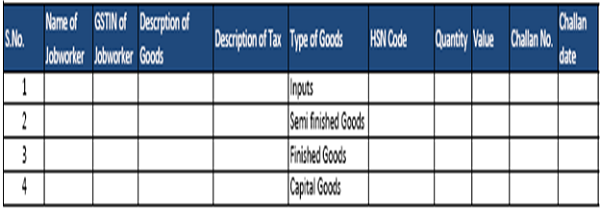

- Statement of goods including Capital goods lying with job worker as on appointed day.

- To be filed by both Principal and Job worker.

- Details by Principal:

Details by Jobworker:

SECTION 141 (14):

- Statement of goods including Capital goods lying with agent as on appointed day. (only SGST).

- To be filed by both Principal and Job worker.

SECTION 142(11)(c):

- Tax paid on advance received for Composite Supply under existing law. (Only VAT + Service Tax)

- To be filed by supplier of goods and services

SECTION 142 (12):

- Goods sent on approval or return as on appointed day.

- To be filed by supplier of goods.

In case of manufacturing goods availing SSI exemption under Central Excise and registered under VAT:

- Under Section 140 (3), you can take credit of the Excise duties paid on the raw materials in stock, contained in work in progress and contained in finished goods, as on 01.07.2017. For this purpose, you have to file GST TRAN 1.

- Such credit has to be taken on the basis of purchase invoices evidencing Excise duty payment. Such invoices should not be more than one year old. Since one would have already availed VAT credit, one cannot take any transitional credit in respect of VAT.

In case of manufacturing goods availing SSI exemption under Central Excise and not having proper excise invoices for purchase of raw materials lying in stock as on 01.07.2017:

- As per proviso under Section 140 (3), manufacturers and service providers are not entitled to take any transitional credit for stock, if they do not have invoices evidencing payment of taxes.

- As a trader, if you have proper excise invoices, you can take credit of Excise duties paid on such stock. Such invoices should not be more than one year old. If you do not have Excise invoices, while selling the goods, you would be entitled to deemed credit @ 40 % of CGST paid by you, if the CGST rate is 6 % or less; 60 % of the CGST paid by you, if the CGST rate is 9 % or more.

- Such facility would be available for the sales made up to 31.12.2017. For this purpose, every month you have to file GST TRAN 2.

- Construction service providers, who were paying service tax on 30 % of the value, including land value, as per Notification 26/2012 ST Dt. 20.06.2012 are specifically covered under Section 140 (3). Section 140 (3) also covers persons who were not liable to be registered under the earlier laws and since you are not registered under Excise law, you can take transitional credit of excise duties paid on your inputs in stock. Since you would not have availed VAT credit, having opted for composition scheme, you are entitled to avail credit of VAT paid on your inputs in stock also. You would require proper invoice copies to claim such credit and such invoices must be less than one year old.

ILLUSTRATIVE SITUATIONS:

- Unsold / under construction flats are work in progress / stock in trade for a construction service provider. So you would be entitled to avail transitional credit for the inputs contained in such unsold / under construction flats also, subject to the invoices for purchase of such inputs are less than one year old.

- If a manufacturer’s depot was registered under Central Excise for passing on the credit of excise duty to the buyers; excise duty paid on the goods lying in stock can be claimed as transitional credit on the basis of Excise invoices which are less than one year old. As the goods would have only been stock transferred from the factory to the Depot, no VAT would have been paid and hence no VAT credit can be claimed under transitional provisions.

- On goods purchased from Second Stage Dealers registered under Central Excise, one could not pass on the benefit of cenvat credit of excise duties, as it was permitted only up to Second Stage Dealer. If anyone is having stock of excise duty paid goods in this situation with duly supported by invoices issued by the Second Stage Dealer, then in respect of the stock for which one is not in possession of Excise invoices, you can claim deemed credit, as per provision to Section 140 (3).

In case of a dealer in various electronic goods and not in possession of any Excise invoices:

One option is that you can claim deemed credit 40 % of CGST if CGST rate is up to 6 %; 60 % of CGST if the CGST rate is 9 % or more. If IGST is paid on such goods, the above percentages shall be 20 % of IGST if IGST rate is up to 12 %; 30 % of IGST if IGST rate is 18 % or above.

Or, if the goods dealt with by you are having unique serial numbers and are having price of more than Rs.25,000 per piece, you can approach the manufacturer of the goods, to issue a Credit Transfer Document to you, on the basis of which you can avail credit of the actual excise duty paid on such goods.

Example:

A dealer is dealing with Product A, attracting 12 % GST and Product B, attracting 18 % GST. On 01.07.2017, he has stock of 1000 Nos. of A and 750 Nos. of B. The Selling price of A is Rs.1200 per unit and B is Rs.2,500 per unit.

PRODUCT: A

| MONTH | NO.OF UNITS SOLD | SALE PRICE @ 1200 | CGST @ 6% & IGST @ 12% | DEEMED CREDIT @ 40% OF CGST |

| JULY 17 | 200 | 2,40,000 | 14,400 | 5760 |

| AUG 17- SOLD INTERSTATE | 50 | 60,000 | 7,200 – IGST | 1440 (20% OF IGST) |

| SEP 17 | NIL | 0 | 0 | 0 |

| OCT 17 | NIL | 0 | 0 | 0 |

| NOV 17 | 250 | 3,00,000 | 18,000 | 7200 |

| DEC 17 | 100 | 1,20,000 | 7,200 | 2880 |

| JAN 180 | 200 | 2,40,000 | 14,400 | No more credit for sales made after six months |

PRODUCT:B

| MONTH | NO.OF UNITS SOLD | SALE PRICE @ 1200 | CGST @ 6% & IGST @ 12% | DEEMED CREDIT @ 40% OF CGST |

| JULY 17 | 100 | 2,50,000 | 22,500 | 13,500 |

| AUG 17- SOLD INTERSTATE | 50 | 1,25,000 | 22,500 | 6,750 (30% OF IGST) |

| SEP 17 | NIL | 0 | 0 | 0 |

| OCT 17 | NIL | 0 | 0 | 0 |

| NOV 17 | NIL | 0 | 0 | 0 |

| DEC 17 | 100 | 2,50,000 | 22,500 | 13,500 |

| JAN 180 | 200 | 5,00,000 | 45,000 | No more credit for sales made after six months |

- In respect of the cotton yarn available in the factory, which you intend to use in your manufacturing of fabric, no transitional credit would be allowed, as the said yarn is not supported by any duty paying document. But, if you intend to sell the yarn, on payment of GST, then you would be entitled to avail deemed credit @ 40 % the CGST (2.5 %) paid on such sale. It may be noted that though the deemed credit facility is not available to a manufacturer, when you sell the yarn as such, you are acting as a trader and hence entitled for deemed credit. Such deemed credit would be allowed for the sale out of the stock, made up to 31.12.2017.

- In respect of the cotton fabric available in your depot, though the same is exempted from payment of duty, since the said exemption is not an unconditional exemption, you would be entitled to deemed credit of 40 % of the CGST (2.5%) paid on sale of such fabrics. Such deemed credit would be allowed for the sale out of the stock, made up to 31.12.2017.

- In case of goods purchased from a manufacturer situated in North East State, which were cleared without payment of excise duty, availing area based exemption:

Since the goods are not unconditionally exempt, you are entitled to claim transitional credit on deemed credit basis (@ 40 % of CGST paid by you, if the CGST rate is 6 % or less; 60 % of the CGST paid by you, if the CGST rate is 9 % or more).

- A person who was registered under the earlier law is not entitled for deemed credit, as per Rule 117 (4) of the GST Rules, 2017. The proviso to Section 140 (3) bars deemed credit only for manufacturers and service providers, the restriction of deemed credit to all persons who were registered under earlier law, by virtue of this rule, is ultra vires the rule and hence not sustainable.

Example:

We are manufacturers of Pipes. We clear our pipes on payment of excise duty and also clear them without payment of excise duty for drinking water supply projects, against District Collectors Certificate. We were availing credit of the excise duties paid on our major raw materials, steel sheets. The pipes supplied to the drinking water projects are applied as special coating and we have stock of such coating materials as on 01.07.2017, on which we have not availed any cenvat credit, as these are exclusively used for the pipes cleared without payment of excise duty. We also have stock of steel sheets. What are the provisions relating to transitional credit for us ?

- Section 140 (4) is applicable. Since we are manufacturing both dutiable and exempted final products, we would be following the provisions of Rule 6 of the Cenvat Credit Rules, 2004. We would have availed cenvat credit for the common inputs, viz., steel sheets and would not have availed credit on the coating materials, as they are exclusively to be used in exempted goods. The pipes cleared for drinking water projects are not entitled for any exemption under GST.

- The question of reversal of proportionate credit / payment of 6 % of the price of the exempted goods under Rule 6 of the CCR, 2004 would arise only post clearance of the pipes claiming excise exemption. The stock of steel sheets lying in stock, contained in work in progress and finished goods, would henceforth be cleared as pipes only payment of GST and you would have already availed credit of the Excise duty paid on such steel sheets. The Cenvat Credit balance as per your last ER 1 return could be carried forward to GST return, under Section 140 (1). Since we have not availed any credit on the coating materials, we can avail the same in respect of such coating materials lying in stock and contained in work in progress and finished goods under Section 140 (3).

- As per section 140 (5), if the goods are accounted and booked in your books of accounts on or before 30.07.2017 (subject to extension of another 30 days by the Commissioner) you can take credit of the Excise duty as CGST and VAT as SGST. CST, which is not entitled for credit under earlier law, cannot be availed as credit.

- The Service tax charged by the service provider can be availed as per Section 140 (5). The GST charged by him after 01.07.2017, ITC can be availed in normal course.

- If one has received certain goods during the last week of June 2017, but the invoice for the same, which was dated in June 2017, was received only in July 2017;

- If you have not filed your ER 1 / ST 3 return for the month / quarter ending June 2017, you can avail such credit in June and file the returns accordingly and the credit balance as per this returns could be carried forward as per Section 140 (1). If you have already filed these returns, you can file a revised return claiming such credit, if you are a service provider. But if you are a manufacturer and filed your ER 1 return for the month of June 2017 you would not be entitled to avail credit of the duties paid on such goods received prior to 01.07.2017, for which invoice was received by you after 01.07.2017.

- The quantum of credit available in respect of the goods procured from 100 % EOUs should be determined as per the formula prescribed under Rule 3 (7) of the Cenvat Credit Rules, 2004.

- Under section 140 (7) of the Act, the service tax can be distributed as CGST credit by the ISD.

- One has obtained centralized registration under Service Tax and availing all cenvat credit at registered place. Now, one has obtained registration in 10 States, where he is executing various projects. How, the balance of cenvat credit as per our last ST 3 return could be distributed to these 10 registrations.

- There is no basis of such distribution. Either you can retain the entire credit in your main office or distribute among one or more of the 10 registered units, in whatever manner you wish. Section 140 (8). The credit transferred to other registrations should be deducted from the credit at main office.

- One has availed cenvat credit for certain input service, based on the invoice dated 01.01.2017 in the month of January 2017 and not made payment for the said invoice until 31.03.2017, the said credit was reversed in the month of April 2017. If you make payment for the bill on or before 30.09.2017, you can take re credit of such service tax as CGST. If the payment is not made on or before 30.09.2017, the credit could not be taken. Section 140 (9). But, the manner in which such credit could be taken is not prescribed in the Rules and the GST TRAN 1 is not having any columns for this purpose.

- If you have not yet filed your ST 3 return for April-June 2017 (Last date 15.08.2017) you can avail credit of invoices which were not considered by oversight before filing the return. Even if you have filed the ST 3 return for April-Jun 2017, you can file a revised return, after availing such credits, on or before 45 days from the date of filing the return.

In case of manufacturing unit, writing down the value of our inventory based on the age of the inventory; reversal of cenvat credit availed on such goods, when the value is written down for the first time:

- As per Rule 3 (5B) of the Cenvat Credit Rules, 2004 re credit can be taken only when such goods are subsequently used. When you use such goods post GST, there are no specific provisions available either in the GST Act / GST Rules, for taking back such credit.

- The three months time limit under CCR, 2004 for making payment would expire on 01.07.2017. But under GST law, the time limit for making payment has been enhanced to six months, vide second proviso under Section 16(2). So you need not reverse the credit, till the expiry of 180 days from the date of invoice.

- One has imported goods prior to 01.07.2017 and paid customs duties and the goods are still lying in the warehouse and would be received in factory over a period of time and it would take about two to three months to receive the entire goods in factory. As per Section 140 (5), once you account for the goods in the books of accounts on or before 30.07.2017 (subject to another 30 days extension by the Commissioner), credit would be allowed. It is not necessary that the goods much be received in your factory within this date. You can avail the credit by filing GST TRAN 01 – Column 7 (b).

- The facility of deemed credit in respect of VAT would be admissible only in cases, where the goods have suffered VAT at the first point and all subsequent stages of sale are exempted from payment of VAT.

- For transactions between associated enterprises, the point of taxation as per Service tax law is date of accounting in the books of accounts, i.e. 30.06.2017 and hence one is liable to pay Service tax on or before 06.07.2017. There are no explicit provisions enabling availment of ITC of such service tax paid after 01.07.2017 for the services received prior to 01.07.2017. If you account for in your books of accounts on 01.07.2017, GST is payable by considering the date of accounting as the time of supply {Section 13 (3) of the CGST Act} and ITC of such GST could also be availed.

Different situations for Sales return in respect of goods sold prior to GST:

| SITUATION | CONSEQUNCES | REMARKS |

| Goods sold to unregistered persons on or after 01.01.2017 and up to 30.06.2017, returned on or before 31.12.2017 | The taxes paid under earlier law, could be claimed as refund | Section 142 (1) |

| Goods sold to registered persons (GST registered) on or after 01.01.2017 and up to 30.06.2017, returned on or before 31.12.2017 | Deemed as supply and the person returning the goods shall charge GST. | Proviso under Section 142 (1) |

| Goods sold to unregistered persons before 01.01.2017 and returned on or after 01.07.2017 | Being return by unregistered person no GST payable by him. The receiver of the goods (original seller) should pay GST under RCM, as he receives supply of goods from unregistered person. | Not provided for explicitly anywhere but this is the consequence. |

| Goods sold to registered persons (GST registered) before 01.01.2017 and returned on or after 01.07.2017 | The returning person shall pay GST. | Not provided for explicitly anywhere but this is the consequence. |

- One has received certain services in the month of April 2017 from a service provider and due to lack of quality of service discussions were going on with him about billing. Finally one has agreed to pay him 50 % of the originally agreed amount and he has raised his invoice after 01.07.2017

- Though invoice has to be raised within 30 days from the completion of service, in this case, the service provider was not able to raise his invoice {CircularNO. 144/13/2011 ST Dt. 18.07.2011}. So, when he raises an invoice after 01.07.2017 he is liable to charge GST which can be availed as ITC by one in normal course.

- The goods on which 2 % ED was paid under notification 1/2011 are considered as “exempted goods”as per CCR, 2004. Further, as per Rule 3 (1) of the CCR, 2004, such 2 % duty cannot be claimed as cenvat credit by the person receiving such goods. With the above back ground, it has to be seen whether any transitional credit could be availed on such goods lying in stock with a person who purchased such goods.

- It may be noted that unlike Section 140 (1) for transition of credit as per the last return, for claiming transitional credit for stock under section 140 (3), there is no condition that the credit which is being claimed must be available as credit under the earlier law also. Further, the term“eligible duties” for the purposes of Section 140 (3), covers all excise duties. So, if a person who is having stock of goods purchased on payment of 2 % ED is possession of Excise invoices for such stock, he can claim transitional credit of such 2 % duty, in respect of such goods, lying in stock, contained in work in progress and finished goods.

- If a trader, who was not registered under earlier law, is having stock of such goods as on 01.07.2017 and is not in possession of Excise invoices, he would be entitled to deemed credit as per proviso to Section 140 (3). In this connection, it may be observed that though the said goods are defined as “exempted goods” under CCR, 2004, that is not an absolute exemption, but a conditional exemption.

- The goods manufactured by you were “exempted goods”under the earlier law and hence you were not entitled to cenvat credit under earlier. Now, as per Section 140 (3) of the CGST Act, you can claim transitional credit for the duties paid on your inputs lying in stock, contained in work in progress and finished goods.

- There are no provisions to transfer the balance available in erstwhile PLA to Electronic Cash Ledger.

- Clean Energy Cess is not specifically mentioned as one of the eligible duties, either under the Cenvat Credit Rules, 2004 or under the Transitional provisions. But, as per the ratio laid down by the Hon’ble High Court of Karnataka in the case of CCE VS Renuga Sugars Ltd –2014-TIOL-98-HC-KAR-CX you can avail the credit. But the issue is debatable.

- GST TRAN 2 is applicable for a person, other than manufacturer or service provider, who was not registered under earlier law, and claiming transitional credit for the stock held by him on deemed basis, who is not having proper excise invoices to claim actual credit. This has to be filed for the first six months from July 2017. For the sales made out of the stock as on 01.07.2017, during the first six months, deemed transitional credit @ 40 % / 60 % of the CGST would be admissible.

(CA Vipul Khandhar, Khandhar & Associates, 311, Dhiraj Avenue, Opp.: Chhadawad Police Chowky, Ambawadi , Ahmedabad – 380006, (O) 26469500, 26469600)

plz upload the gst treatment with example and with sections…cover all topics cgst, sgst, igst

PLZ sir upload the gst reatment with example