Sharad Aggarwal

All Taxation laws define an event, called in legal language “Taxable Event”, on the happening of which, one becomes taxable. Eg., in Excise, manufacturing is the Taxable event, However, liability arise on “Removal” of Goods. In GST, Supply is proposed to be the Taxable Event, however, liability to pay shall arise at Time of Supply as determined under section 12/13.

“Supply” is a much wider Term than “Sale”. Definition of Supply in section 3 is inclusive and sweeps into its fold all forms of supply such as Sale, transfer, exchange, license, lease, rental, disposal etc. Essentially, anything that can be said to have be supplied by one person to another shall be covered under “Supply”. In plain terms, if an item is given by you to your friend, it is a supply.

A transaction shall become a supply if it satisfy any one of the three conditions as given in Sec 3(1)

1. Any form or kind of supply which involves consideration and takes place in course or furtherance of business shall be supply.

2. If a service is imported, for consideration, it will be supply whether it is for business or not. For example, if a celebrity is invited for performance in a marriage in India and he is paid Rs. 20 crores, the transaction should be treated as Supply even if the transaction is not for business.

3. Notified supplies are transactions as specified in Sch-I which shall be treated as Supply whether consideration is involved or not. It is immaterial whether it is for business or non-business. Sch-I has listed following transactions

a. Disposal of business assets where ITC has been availed.

b. Supply between related persons or distinct persons as defined u/s 10, when such supply is made in course or furtherance of business

c. Supply of Goods by principal to agent or vice-versa

d. Import of services by a Taxable Person from related person or other establishment outside India, when such import is in course or furtherance of business

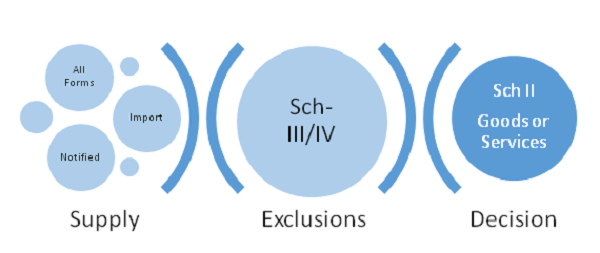

A typical decision involving whether a transaction is Supply or not, and if it is a Supply then weather it is Supply of Goods or Supply of Services has been explained through above chart. First, we shall decide whether a transaction is Supply or not. Second, if it is a supply, is it covered under exclusion list as specified under Schedule III &IV. If transaction is a supply and not covered in exclusions, then in third and final step, we shall determine whether it is a Supply of Goods or Supply of Service using Schedule II. (Sch-II has been explained in a different chapter to ensure focus remains on term “Supply”)

Sch-II is extremely important as basis the decision under Sch-II, provisions of Time of Supply, Place of Supply and Value of Supply shall be applicable. For example, if a transaction is decided to be “Supply of Goods”, section 12 shall apply for determining “Time of Supply”. However, if a transaction is decided to be “Supply of Supply”, section 13 shall apply for determining “Time of Supply”.

New draft has defined in detail, the Composite Supply – When two or more supplies of goods or services are delivered in a bunch, it shall be treated as “Composite Supply”. Basic test of a composite supply are that a) supplies should be naturally bundled b) supplied in concurrence of each other and c) one supply among the supplies should be Principal Supply.

Principal Supply has been defined one which is predominant element of the transaction and other supplies are ancillary to Principal Supply for better enjoyment of Principal Supply. Taxability of Composite Supply shall be basis the Principal Supply.

One more type of Supply has been introduced called Mixed Supply Where two or more INDIVIDUAL supplies of goods or services are delivered in a bunch. Basic test of a Mixed supply are that a) it should not be a composite Supply b) and the product should be capable of being supplied Individually.

In next, article we will discuss Schedule II