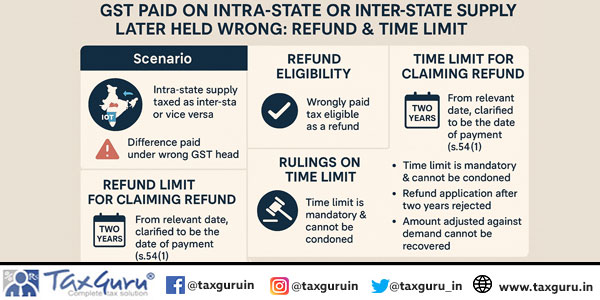

Tax wrongfully collected and paid to Government on transaction considered by taxpayers to be an intra-State supply, but which is subsequently held to be an inter-State supply and vice versa

In a case where Intra-State supply [means supply where location of supplier and place of supply within the same state] subsequently held to be an inter-State supply [means supply where location of supplier and place of supply is between two different states] and vice versa = Tax already paid is eligible for refund.

- A registered person who has paid the Central tax and State tax/UT Tax on a transaction considered by him to be an intra-State supply, but which is subsequently held to be an inter-State supply, shall be refunded the amount of Central tax and State tax/UT Tax so paid. [Section 77 of the CGST Act].

[Example : A Ltd situated in Noida supplied Engineering services to B Ltd situated in Noida in relation to immovable property situated in PATNA and at the time of issuance of invoice A Ltd levied CGST Rs 500 and SGST Rs 500 assuming it as intra state supply subsequently during GST audit it has been held that such transaction is interstate supply as location of supplier is in Noida and place of supply is in PATNA that is location of supplier and place of supply is within two different states hence it was liable for IGST of Rs 1000/-in this case A Ltd who paid the CGST and SGST is eligible for refund of CGST Rs 500 and SGST Rs 500 as per section 77 of the CGST Act 2017]

- A registered person who has paid integrated tax on a supply considered by him to be an inter-State supply, but which is subsequently held to be an intra-State supply, shall be granted refund of the amount of integrated tax so paid. [Section 19 of the IGST Act].

[Example : A Ltd situated in Noida supplied Engineering services to B Ltd situated in Patna in relation to immovable property situated in Noida and at the time of issuance of invoice A Ltd levied IGST Rs 1000/- assuming it as interstate supply subsequently during GST audit it has been held that such transaction is intra state supply as property in relation to which services is performed is located in Noida hence place of supply is in Noida and Location of supplier is also in Noida hence it was liable for CGST Rs 500/- & SGST Rs 500/-in this case A Ltd who paid the IGST is eligible for refund IGST Rs 1000/- as per section 19 of the IGST Act 2017].

A registered person who has paid integrated tax on a transaction considered by him to be an inter-State supply, but which is subsequently held to be an intra-State supply, shall not be required to pay any interest on the amount of central tax and State tax or, as the case may be, the Central tax and the Union territory tax payable.

[Example : A Ltd situated in Noida supplied Engineering services to B Ltd situated in Patna in relation to immovable property situated in Noida and at the time of issuance of invoice A Ltd levied IGST Rs 1000/- assuming it as interstate supply subsequently during GST audit it has been held that such transaction is intra state supply as property in relation to which services is performed is located in Noida hence, place of supply, is in Noida and Location of supplier, is also in Noida hence it was liable for CGST Rs 500/- & SGST Rs 500/-in this case A Ltd who already paid the IGST is not liable for payment of interest on fresh liability of CGST and SGST as per section 77 of the CGST Act 2017.

- A registered person who has paid central tax and State tax or Union territory tax, as the case may be, on a transaction considered by him to be an intra-State supply, but which is subsequently held to be an inter-State supply, shall not be required to pay any interest on the amount of integrated tax payable.

[Example : A Ltd situated in Noida supplied Engineering services to B Ltd situated in Noida in relation to immovable property situated in PATNA and at the time of issuance of invoice A Ltd levied CGST Rs 500 and SGST Rs 500 assuming it as intra state supply subsequently during GST audit it has been held that such transaction is interstate supply as location of supplier is in Noida and place of supply is in PATNA that is location of supplier and place of supply is within two different states hence it was liable for IGST of Rs 1000/-in this case A Ltd who already paid the CGST and SGST is not liable for interest in liability of IGST as per section 77 of the CGST Act 2017]

TIME LIMIT FOR FILLING OF REFUND IN RESPECT OF A TRANSACTION CONSIDERED TO BE AN INTRA-STATE SUPPLY, WHICH IS SUBSEQUENTLY HELD TO BE AN INTER-STATE SUPPLY

Any person, claiming refund under section 77 of the CGST Act of any tax paid by him, in respect of a transaction considered by him to be an intra-State supply, which is subsequently held to be an inter-State supply, may, before the expiry of a period of two years from the date of payment of the tax on the inter-State supply, file an application electronically in FORM GST RFD-01 through the common portal.

[Example : A Ltd situated in Noida supplied Engineering services to B Ltd situated in Noida in relation to immovable property situated in PATNA and at the time of issuance of invoice A Ltd levied CGST Rs 500 and SGST Rs 500 assuming it as intra state supply subsequently during GST audit it has been held that such transaction is interstate supply as location of supplier is in Noida and place of supply is in PATNA that is location of supplier and place of supply is within two different states hence it was liable for IGST of Rs 1000/-in this case A Ltd who paid the CGST and SGST is eligible for refund of CGST Rs 500 and SGST Rs 500 and refund application would be filed before the expiry of a period of two years from the date of payment of the tax on the inter-State supply (that is date of payment of IGSR Rs 1000/-)

CLARIFICATION ON SUBSEQUENTLY HELD COVERS BOTH THE CASES WHERE THE INTER-STATE OR INTRA-STATE SUPPLY MADE BY A TAXPAYER HIMSELF AS INTRA-STATE OR INTER-STATE RESPECTIVELY OR WHERE THE INTER-STATE OR INTRA-STATE SUPPLY MADE BY A TAXPAYER IS SUBSEQUENTLY FOUND/ HELD AS INTRA-STATE OR INTER-STATE RESPECTIVELY BY THE TAX OFFICER.

“subsequently held” mentioned in section 77 of CGST Act and 19 of the IGST Act covers both the cases

- where the inter-State or intra-State supply made by a taxpayer, is either subsequently found by taxpayer himself as intra-State or inter-State respectively or

- where the inter-State or intra-State supply made by a taxpayer is subsequently found/ held as intra-State or inter-State respectively by the tax officer (in any proceeding such as scrutiny/ assessment/ audit/ investigation, or as a result of any adjudication, appellate or any other proceeding)

Accordingly, refund claim under the said sections can be claimed by the taxpayer in both the above-mentioned situations, provided the taxpayer pays the required amount of tax in the correct head and claim the refund within two years from the date of payment under correct head , i.e. integrated tax paid in respect of subsequently held inter-State supply, or central and state tax in respect of subsequently held intra-State supply, as the case may be

Refund under section 77 of the CGST Act / section 19 of the IGST Act would not be available where the taxpayer has made tax adjustment through issuance of credit note under section 34 of the CGST Act in respect of the said transaction.

IN THE HIGH COURT OF JUDICATURE AT PATNA Civil Writ Jurisdiction Case No.13163 of 2024 in case of M/S Sai Steel

- Court held that the relevant date for counting the period of limitation (2 years) would start from the date when tax is paid under correct head.

*****

It is hereby declare that this is for academic purpose only for any professional advise please contact CA Rajnish Kumar, Email carajnishkumarca@gmail.com, +91-8130883807

nicely articulated

what would happen at recipient end if they claimed ITC of IGST instead of CGST and sgst