India’s automobile industry is one of the fastest growing in the world and it is already the sixth largest globally. According to a Society of Indian Automobile Manufactures (SIAM) report, annual car sales could reach more than 9 million vehicles by 2020. Till about a decade ago, in the absence of organized players, more than 60 percent of all used car sales were C2C (customer to customer) among friends and relatives etc.

According to estimates in the US, for every new car sold, around three used cars are sold. In Europe, this ratio is 1:2, while currently in India it is 1:1.3. At present, the second hand car market in India is largely unorganized and fragmented. In India, organized dealers account for 19 percent of the total used car market, with the semi-organized segment contributing 52 percent and unorganized dealers 29 percent.

Let us discuss in this article the Impact of GST on Buying / Selling a Used Vehicle. Since the transactions happen in different ways, broadly as below, we shall discuss the impact of GST accordingly.

Individual Sells to Individual (C2C)

Individual Sells to Un-registered Dealer (C2C)

Individual Sells to Registered Dealer (C2B)

Registered Dealer Sells to Any Buyer (B2B / B2C)

Leasing of Vehicle

Exchange of Old Vehicle with New

Individual Sells to Individual (C2C):

As per Section 2(105) read with section 7 of CGST Act, even though the sale of old or used vehicle by an individual is for a consideration, it cannot be said to be in the course or furtherance of his business (as selling old vehicles is not the business of the said individual), and hence does not qualify to be a supply per se. Therefore sale by an individual to another individual is not a supply and no GST is applicable.

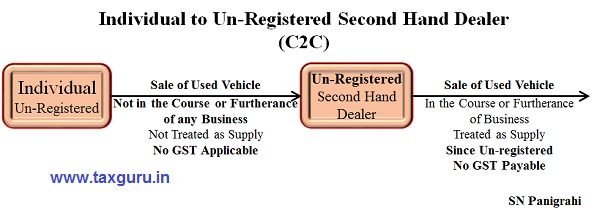

Individual Sells to Un-registered Dealer (C2C):

This type of Transaction is similar one in the previous case, except that the buyer is in the course or furtherance of business. Individual selling to un-registered second hand vehicle dealer is not a supply and therefore no GST is applicable. Though the unregistered buyer further makes resale of such vehicles is in the course or furtherance of business, GST is not payable as he is un-registered (may be by virtue of his turnover less than threshold limit of Rs 20 L / Rs 10 L)

Individual Sells to Registered Second Hand Dealer (C2B):

Individual (unregistered) selling to Registered, attracts payment of GST on Reverse Charge Mechanism under Sec 9(4) of CGST Act. section mandates that tax on supply of taxable goods (vehicle in this case) by an unregistered supplier (an individual in this case) to a registered person (the Second Hand Vehicle Dealer in this case) will be paid by the registered person (the Dealer in this case) under reverse charge mechanism.

This provision, however, has to be read in conjunction with section 2(105) read with section 7 of the said Act. Section 2 (105) defines supplier as a person supplying the goods or services. Section 7 provides that a supply is a transaction, for a consideration by a person in the course or furtherance of business.

Even though the sale of old vehicle by an individual is for a consideration, it cannot be said to be in the course or furtherance of his business (as selling old vehicle is not the business of the said individual), and hence does not qualify to be a supply per se.

Accordingly the sale of old vehicle by an individual to a registered dealer will not attract the provisions of section 9(4) and the dealer will not be liable to pay tax under reverse charge mechanism on such purchases.

Now let us discuss further resale of Vehicle by the Registered Dealer.

Margin Scheme: Normally GST is charged on the transaction value of the goods. However, in respect of second hand goods, a person dealing is such goods may be allowed to pay tax on the margin i.e. the difference between the value at which the goods are supplied and the price at which the goods are purchased. If there is no margin, no GST is charged for such supply. The purpose of the scheme is to avoid double taxation as the goods, having once borne the incidence of tax, re-enter the supply and the economic supply chain.

Valuation of Second Hand Goods: As per Rule 32(5) of the CGST Rules, 2017, where a taxable supply is provided by a person dealing in buying and selling of second hand goods i.e., used goods as such or after such minor processing which does not change the nature of the goods and where no input tax credit has been availed on the purchase of such goods, the value of supply shall be the difference between the selling price and the purchase price and where the value of such supply is negative, it shall be ignored.

The proviso to the above rule further provides that in case of the purchase value of goods repossessed from a unregistered defaulting borrower, for the purpose of recovery of a loan or debt shall be deemed to be the purchase price of such goods by the defaulting borrower reduced by five percentage points for every quarter or part thereof, between the date of purchase and the date of disposal by the person making such repossession.

GST is charged at the same rate it is charged on new vehicles, but on the dealer’s margins only.

Conditions to avail the benefit of the Margin Scheme

There are two conditions to avail the margin scheme for GST which are as follows:

- Goods should be supplied as it is (same goods) or after a minor processing which does not change the nature of goods.

- No input tax credit (ITC) should be availed on the purchase of such goods.

If both the above conditions are fulfilled then GST margin scheme can be availed.

Applicability of Reverse Charge: If an unregistered supplier of old vehicles sells it to registered supplier, the tax under RCM will apply.

In this regard, Notification No.10/2017-Central Tax (Rate) New Delhi, dated 28th June, 2017 exempts intra-State supplies of second hand goods received by a registered person, dealing in buying and selling of second hand goods and who pays the central tax on the value of outward supply of such second hand goods as determined under sub-rule (5) of rule 32 of the CGST Rules, 2017, from any unregistered supplier, from the whole of the central tax levied under the CGST Act, 2017. Similar exemptions are also there in respective SGST Acts.

However Tax applicability on Reverse Charge on Purchases from Un-registered Dealers is suspended till 31st March, 2018. Notification No. 38/2017–Central Tax (Rate), 13th October, 2017. So the Registered dealer buying from un-registered individual need not pay GST on RCM till 31st Mar’2018.

Registered Dealer Sells to Any Buyer (B2B / B2C):

If the supplier is a registered person and such supplier had purchased the Motor Vehicle prior to July 1, 2017 and has not availed input tax credit of central excise duty, Value Added Tax or any other taxes paid on such vehicles, then such vehicles when sold will attract GST of 65% of the applicable GST) rate, including compensation cess.

These rates would apply for a period of three years with effect from 1 July 2017 ie apply up to 30th June 2020.

Notifications:

- Notification No. 37/2017-Central Tax (Rate) dated October 13, 2017

- Similar notification is issued under the UTGST Act vide Notification No. 37/2017 – Union Territory tax (Rate) dated October 13, 2017.

- Similar notification is issued under the IGST Act vide Notification No. 38/2017- Integrated Tax (Rate) dated October 13, 2017.

- Similar notification is issued under GST (Compensation to the States) Act for Motor Vehicle falling under chapter heading 8702 & 8703 vide Notification No. 7/2017-Compensation Cess (Rate) dated October 13, 2017.

GST on Leasing of Vehicle:

Vehicle leasing is the leasing (or the use of) a motor vehicle for a fixed period of time at an agreed amount of money for the lease. It is commonly offered by dealers as an alternative to vehicle purchase but is widely used by businesses as a method of acquiring (or having the use of) vehicles for business, without the usually needed cash outlay. The key difference in a lease is that after the primary term (usually 2, 3 or 4 years) the vehicle has to either be returned to the leasing company or purchased for the residual value.

Leasing of vehicles purchased prior to 1 July will attract a tax equivalent to 65% of the current applicable goods and services tax (GST) rate for a period of 3 years.

Exchange of Old Vehicle with New:

Interestingly, sale of old and new cars is inextricably linked. It is estimated that about 27-28 percent of new car sales accrue through exchange of old models. So if new car sales are pegged at about 3 million, we could be looking at about 8,40,000 used cars being exchanged for new ones at pre-owned outlets.

In case exchange offers, the GST will be paid on the Transaction Value of the New Vehicle. For instance, if the new car costs Rs 10 lakh and exchange value of the old car is Rs 3 lakh, the customer will pay Rs 7 lakh but GST will be paid on Rs 10 lakh.

GST Rates on Motor Vehicles

| HSN Code | Description | Rate (%) | CESS (%) |

| 87 | Electrically operated vehicles, including two and three wheeled electric motor vehicles | 12 | |

| 8701 | Tractors (except road tractors for semi-trailers of engine capacity more than 1800 cc) | 12 | |

| 8702 | Motor vehicles for the transport of ten or more persons, including the driver (except 870210 ,870220, 870230, 870290 ) | 28 | |

| 870210 | Motor vehicles for the transport of 10 or more persons but not more than 13, including the driver | 28 | 16 |

| 870220 | Motor vehicles for the transport of 10 or more persons but not more than 13, including the driver | 28 | 16 |

| 870230 | Motor vehicles for the transport of 10 or more persons but not more than 13, including the driver | 28 | 16 |

| 870240 | Motor vehicles for the transport of 10 or more persons but not more than 13, including the driver | 28 | 16 |

| 8703 | Motor vehicles cleared as ambulances duly fitted with all the fitments, furniture and accessories necessary for an ambulance from the factory manufacturing such motor vehicles | 28 | NIL |

| 87031010 | Electrically operated vehicles, including three wheeled electric motor vehicles. | 28 | NIL |

| 870380 | Electrically operated vehicles, including three wheeled electric motor vehicles. | 28 | NIL |

| 8703 | Three wheeled vehicles | 28 | NIL |

| 8703 | Cars for physically handicapped persons, subject to the following conditions: a) an officer not below the rank of Deputy Secretary to the Government of India in the Department of Heavy Industries certifies that the said goods are capable of being used by the physically handicapped persons; and b) the buyer of the car gives an affidavit that he shall not dispose of the car for a period of five years after its purchase. | 18 | NIL |

| 870340 | Following Vehicles, with both spark-ignition internal combustion reciprocating piston engine and electric motor as motors for propulsion; a) Motor vehicles cleared as ambulances duly fitted with all the fitments, furniture and accessories necessary for an ambulance from the factory manufacturing such motor vehicles b) Three wheeled vehicles c) Motor vehicles of engine capacity not exceeding 1200cc and of length not exceeding 4000 mm. Explanation.For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. | 28 | NIL |

| 870350 | Following Vehicles, with both spark-ignition internal combustion reciprocating piston engine and electric motor as motors for propulsion; a) Motor vehicles cleared as ambulances duly fitted with all the fitments, furniture and accessories necessary for an ambulance from the factory manufacturing such motor vehicles b) Three wheeled vehicles c) Motor vehicles of engine capacity not exceeding 1200cc and of length not exceeding 4000 mm. Explanation.For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. | 28 | NIL |

| 870360 | Following Vehicles, with both compression -ignition internal combustion piston engine [ diesel-or semi diesel ) and electric motor as motors for propulsion; a) Motor vehicles cleared as ambulances duly fitted with all the fitments, furniture and accessories necessary for an ambulance from the factory manufacturing such motor vehicles b) Three wheeled vehicles c) Motor vehicles of engine capacity not exceeding 1500 cc and of length not exceeding 4000 mm. Explanation.For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. | 28 | NIL |

| 870370 | Following Vehicles, with both compression -ignition internal combustion piston engine [ diesel-or semi diesel ) and electric motor as motors for propulsion; a) Motor vehicles cleared as ambulances duly fitted with all the fitments, furniture and accessories necessary for an ambulance from the factory manufacturing such motor vehicles b) Three wheeled vehicles c) Motor vehicles of engine capacity not exceeding 1500 cc and of length not exceeding 4000 mm. Explanation.For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. | 28 | NIL |

| 8703 | Hydrogen vehicles based on fuel cell tech and of length not exceeding 4000 mm. Explanation.For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. | 28 | NIL |

| 870321 | Petrol, Liquefied petroleum gases (LPG) or compressed natural gas (CNG) driven motor vehicles of engine capacity not exceeding 1200cc and of length not exceeding 4000 mm. Explanation.For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. | 28 | 1 |

| 870322 | Petrol, Liquefied petroleum gases (LPG) or compressed natural gas (CNG) driven motor vehicles of engine capacity not exceeding 1200cc and of length not exceeding 4000 mm. Explanation.For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. | 28 | 1 |

| 870331 | Diesel driven motor vehicles of engine capacity not exceeding 1500 cc and of length not exceeding 4000 mm. Explanation.For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. | 28 | 3 |

| 8703 | Motor cars and other motor vehicles principally designed for the transport of persons (other than those of heading 8702), including station wagons and racing cars [other than Cars for physically handicapped persons ,other than those mentioned at S. Nos. 1308 to 1320 above | 28 | 15 |

| 8704 | Refrigerated motor vehicles | 18 | |

| 8704 | Motor vehicles for the transport of goods [other than Refrigerated motor vehicles] | 28 | |

| 8705 | Special purpose motor vehicles, other than those principally designed for the transport of persons or goods (for example, breakdown lorries, crane lorries, fire fighting vehicles, concrete-mixer lorries, road sweeper lorries, spraying lorries, mobile workshops, mobile radiological unit) | 28 | |

| 8706 | Chassis fitted with engines, for the motor vehicles of headings 8701 to 8705 | 28 | |

| 8707 | Bodies (including cabs), for the motor vehicles of headings 8701 to 8705 | 28 | |

| 8708 | Following parts of tractors namely: a. Rear Tractor wheel rim, b. tractor centre housing, c. tractor housing transmission, d. tractor support front axle | 18 | |

| 8708 | Parts and accessories of the motor vehicles of headings 8701 to 8705 [other than specified parts of tractors] | 28 | |

| 8709 | Works trucks, self-propelled, not fitted with lifting or handling equipment, of the type used in factories, warehouses, dock areas or airports for short distance transport of goods; tractors of the type used on railway station platforms; parts of the foregoing vehicles | 28 | |

| 8710 | Tanks and other armoured fighting vehicles, motorised, whether or not fitted with weapons, and parts of such vehicles | 28 | |

| 8711 | Motorcycles (including mopeds) and cycles fitted with an auxiliary motor, with or without side-cars; side-cars (engine capacity not exceeding 350cc) | 28 | |

| 8711 | Motorcycles of engine capacity exceeding 350 cc. | 28 | 3 |

| 8712 | Bicycles and other cycles (including delivery tricycles), not motorised | 12 | |

| 8713 | Carriages for disabled persons, whether or not motorised or otherwise mechanically propelled | 5 | |

| 8714 | Parts and accessories of bicycles and other cycles (including delivery tricycles), not motorised, of 8712 | 12 | |

| 8714 | Parts and accessories of vehicles of headings 8711 and 8713 | 28 | |

| 8715 | Baby carriages and parts thereof | 18 | |

| 8716 | Trailers and semi-trailers; other vehicles, not mechanically propelled; parts thereof [other than Self-loading or self-unloading trailers for agricultural purposes, and Hand propelled vehicles (e.g. hand carts, rickshaws and the like); animal drawn vehicles] | 28 |

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner, Corporate Trainer & Author

Author Bio

Dear Sir,

I am planning to sell my car to cars24. Just wanted to know whether I will need to pay GST post sale. Please note my car is registered on my personal name & I have taken depreciation in my company for the same. Please note my company is a proprietor ship firm & I am the proprietor.

Awaiting your valued response

For a Registered Person who is not into the business of sale and purchase of used cars. Sale His car to un register dealer .

Can u guide me weather he pay GST or not.

If he have to pay GST what is the Rate of Tax

our Company is registered in GST. We are seling an old Inova Car to a registered Car sale purchase Company at a price of Rs 4.50 lakh which is below the WDV of the car purchased in 2010. What shall be the GST applicable?

Dear Sir,

I am planning to sell my car to my friend. Just wanted to know whether I will need to pay GST post sale. Please note my car is registered on my personal name & I have taken depreciation in my company for the same. Please note my company is a proprietor ship firm & I am the proprietor.

Awaiting your valued response.

We have purchased 6 transport vehicles for business purposes & have not taken any input VAT for determining the VAT payable during the month & year of purchase.

Now we have sold 2 vehicles during July, 2018.

Please advise us whether we have to raise GST invoice or not in the light of of non availment of input VAT?

If your advise is to pay GST, we have to raise GST bill & to pay GST on before 20the August, 2018.

Please advise us

13

book of accounts moter sales gst aplicable

We are in C & F agents for a paints company. As part of agreement, we are supposed to supply paints to the registered dealers with the co., for which we bought Tata Mobiles prior to 2017 for supply of Co., products.

Now during this month, we have sold 2 Tata Mobiles (transport vehicle) to an unregistered dealer.

Will the sale has to be invoiced in the normal procedure & what will be the GST on sale of Transport vehicles to an unregistered dealer.

Dear Sir/ Madam,

Trading of Second Hand Vehicles:

Sale Value 30Lakhs

Purchase Value 20Lakhs

Margin Amount 10Lakhs

Now What will be the Turnover for calculation of GST Registration 30 Lakhs or 10 Lakhs

we are registered company engaged in cabs & buses passanger transport service provider

please confirm

if we sale the bus to individual person, please confirm can we liable to pay GST of Sale value or not

for example bus value in our books Rs 350000/- and we have sold this vehicle in Rs 320000/-

what is gst

Very useful and insightful artilce.

Dear Sir,

we are register dealers we will sales of motor vehicle how much of gst rate please give me

I have sold an old car to an individual and also bought a new car in the same year. Kindly let me know the effect of GST on both the cases.

Dear Sir

3 Year Old Truck Sold On 06.02.2018 GST Rate Applicable

In an otherwise good article there is an error:

In the case of a registered person selling an old vehicle to anyone, the notifications quoted above

wherein the applicable rate and cess are reduced to 65% are incorrect. The reductions only affect “leasing”, not sale of, vehicles till 31/03/2020,

Thus with the changes notified on 25/01/2018 though there is no cess, the rate of 18% or 12% will need to be paid for such a sale of an older vehicle – NOT 65% of the revised rate.

I AM REGISTERED FIRM IN GST. WE HAVE SOLD OLD CAR TO REGISTERED DEALER

Sale of old vehicle as scrap – what should be rate of tax. Rate applicable would be normal vehicle rates or rates as applicable to scrap.

I am a GST Registered civil contractor. Selling or buying of vehicle is not my business. will the sale of my car attract gst.

I am GST registered person (proprietorship) and own a TAXI. I am in process to sell that Taxi to another person (individual) GST registered having Taxi Business. Is GST apply in this case?

Sir,

I am a GST Registered dealer. Selling or buying of vehicle is not my business. What is the GST Rate for sale of old Mini Lorry?

Sale through auction

1. if Sale to registered dealer

2. if sale to individual

Corporate employer transfer the vehicle to its employee ( who is already actual user) under its conveyance scheme is liable for GST or not ?

In our organization, Vehicle in the name of company is transferred to employee under a board approved scheme. Even WDV after specified period is not recovered but added to Annual Salary for Income tax purpose. whether this attracts GST ? if yes Valuation ?

Dear Sir,

We a Pharmaceutical company would like to self old company private cars to registered/unregistered dealers/individuals. What will be the impact of GST on such sale.

Excellent Article .

Small query – how to enter this transaction (Sale of Used Motor car ) under concessional rate in GSTR 1 .There is no provision to enter concessional rate in GSTR1

What is the GST Applicability if any government department sells their old vehicle in auction.

Sir if a company( manufacturing machines) not in business of vehicles sold a car to its employee, will gst be attracted

what about a registered company, selling it to any individual?

if Material sold @ april -17 and return in current month (Oct-17) how to show goods returns in GST Return, In how to take credit Excise duty and Vat??.

if company owned old car sales to register delear / un registered, GST applicable or not ?? and GST Rate ??

What about if regiztered dealer sells to un registered dealer

As per Notification No. 7/2017-Compensation Cess (Rate) dated October 13, 2017, 65% of Cess Rate payable subject to conditions

Pl. read the article with Picture

Thank you for very good article

Very nice article Sir..Many Thanks..

One query Sir, in case of GST on Leasing of Vehicles.. Is GST payable on Transaction Value i.e. Lease rentals? Will GST payable be same for both Operating and Finance Lease?

Best Regards

Nice article

Whether Compensation Cess is Payable by Used Car dealer ? Is exemption available as per Notification 4/2017 dated 20.07.2017 for Used Car dealer from Compensation Cess

Dear Sir,

employers lets out a used car after 4 years to employee at a nominal cost. Will it attract GST and the rate for the same

Article is useful. I have a query

A car is provided by employer to employee for office use. Its in the name of co. On retirement car is handed over to employee free of cost.

Whether this will attract GST and perquisite tax.

Pl advise.

Wonder full article. Its very useful. Thank you very much sir.

Queries :

1) whether the dealer have to pay 1% on sale value or margin in case used car dealer opted for composition scheme. Further , for “turnover” calculation whether sale value will be considered or Margin value.

2) what invoice used car dealer will issue on sale opting for Margin scheme.( by composition dealer and non composition dealer both )

Dear Sir

We are filed and Remitted our return(GSRT1 & GSRT3B) for the month of July’2017, And we have noticed and got feedback from our Receiver that our invoices or reflected with a status of counter party submit status NO in receiver GSTR2A and therefore they are not able to accept/modify our filed invoices. (receiver GSTR2)

We further wish to clarify that we have fully filed our return.

We seeking your response in this regards