The introduction of Form GST ITC-04: Details of goods/capital goods sent to job worker and received back sheds light on the intricate processes and regulations governing the movement of goods and capital goods to and from job workers within the GST framework. This guide aims to demystify the complexities associated with definitions, job work procedures, relevant rules, and filing requirements. As businesses navigate the nuances of sending goods to job workers, understanding the fundamental aspects of Form ITC-04 becomes imperative for compliance. Delving into the definitions of job work, principal entities, and the procedural intricacies, this guide serves as a comprehensive resource for businesses seeking clarity in the realm of goods sent to job workers under GST.

Relevant Definitions:

1) JOB Work: Section 2(68) of CGST Act, 2017 “job work” means any treatment or process undertaken by a person on goods belonging to another registered person and the expression “job worker” shall be construed accordingly;

2) Principal: S.2(88) “principal” means a person on whose behalf an agent carries on the business of supply or receipt of goods or services or both; ( In our discussion the principal means a Manufacturer)

Job work procedure.- S. 143

Allows a registered person to send any inputs or capital goods, without payment of tax, to a job worker for job work and from there subsequently send to another job worker and likewise.

(a) Also provide the time period to bring back the goods:

i) Inputs within 1 Year.

ii) Capital Goods within 3 Years.

b) Also allows to supply goods directly from the place of job worker within period as applicable 1 year or 3 years.

Subject to conditions as :

I. To declare the place of job worker as his additional place of business.

Exceptions to declare additional place:

I) Job worker is registered

II) Supply as notified by the commissioner.

2) responsibility for keeping proper accounts for the inputs or capital goods shall lie with the principal.

3) & 4) If inputs/Capital Goods not received back or sold within applicable time, it shall be deemed as supplied to a job worker on the date of delivery challan. And principal has to pay tax along with interest and declare in his GTSR-1 accordingly.

5) Notwithstanding anything contained in sub-sections (1) and (2), any waste and scrap generated during the job work may be supplied by the job worker directly from his place of business on payment of tax, if such job worker is registered, or by the principal, if the job worker is not registered.

Rule 45.

Conditions and restrictions in respect of inputs and capital goods sent to the job worker.-

(1) The inputs, semi-finished goods or capital goods shall be sent to the job worker under the cover of a challan issued by the principal, including where such goods are sent directly to a job-worker,

What if further, goods sent by a job worker to another job worker?

Inserted w.e.f. 23/03/2018 Notification no 14/2018 CT: and where the goods are sent from one job worker to another job worker, the challan may be issued either by the principal or the job worker sending the goods to another job worker:

Provided: That the challan issued by the principal may be endorsed by the job worker, indicating therein the quantity and description of goods where the goods are sent by one job worker to another or are returned to the principal:

Provided: further that the challan endorsed by the job worker may be further endorsed by another job worker, indicating therein the quantity and description of goods where the goods are sent by one job worker to another or are returned to the principal.]

(2) The challan issued by the principal to the job worker shall contain the details specified in rule 55.

(3) The details of challans in respect of goods dispatched to a job worker or received from a job worker [during the specified period] shall be included in FORM GST ITC-04 furnished for that period on or before the twenty-fifth day of the month succeeding [the said period] [or within such further period as may be extended by the Commissioner by a notification in this behalf:

Rule 45.- Period for furnishing details

Explanation. – For the purposes of this sub-rule, the expression “specified period” shall mean. :-

(a) the period of six consecutive moths commencing on the 1st day of April and the 1st day of October in respect of a principal whose aggregate turnover during the immediately preceding financial year exceeds five crore rupees; and

(b) a financial year in any other case.

(Inserted vide Notification No. 35/2021-CT dated 24.09.2021 w.e.f. 01.10.2021.) Before this the filing period was Quarterly basis.

In simple words:

1) Yearly for turnover less than 5Cr.

2) Six Monthly for turnover more than 5Cr.

3) Yearly in any other case

Rule 45.- Tax Liability

(4) Where the inputs or capital goods are not returned to the principal within the time stipulated in section 143, it shall be deemed that such inputs or capital goods had been supplied by the principal to the job worker on the day when the said inputs or capital goods were sent out and the said supply shall be declared in FORM GSTR-1 and the principal shall be liable to pay the tax along with applicable interest.

Late Fees and Penalty

There is no any specific penalty or late fees prescribed in the act. However, Section 125 of the GST Act provides for a general penalty of up to Rs. 25,000 for contravention of the provisions of the Act and rules made thereunder.

(CGST – 25000 + SGST 25000)

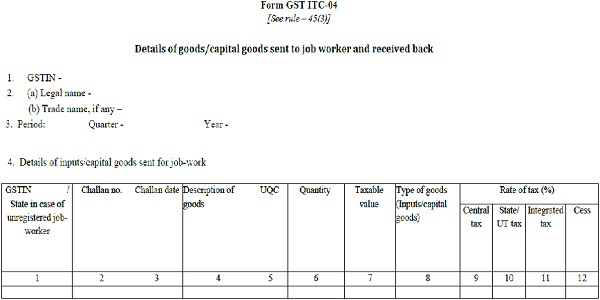

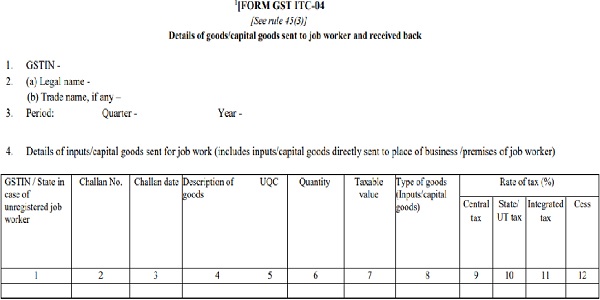

Rule 45.- Details to furnish in ITC-4

–

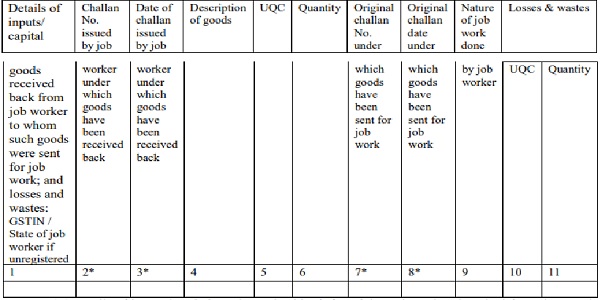

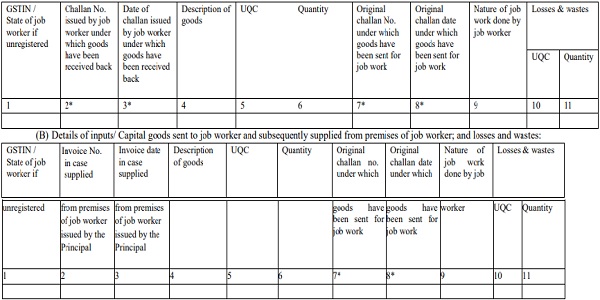

5. Details of input/capital goods received back from job worker or sent out from business place of job work

(A) Details of inputs / capital goods received back from job worker other than the job worker to whom such goods were originally sent for job work; and losses and wastes:

Instructions:

1. Multiple entry f items for single challan may be filled.

2. Columns (2) & (3) in Table (A) and Table (B) are mandatory in cases where fresh challan are required to be issued by the job worker. Otherwise, columns (2) & (3) in Table (A) and Table (B) are optional.

3. Columns (7) & (8) in Table (A), Table (B) and Table (C) may not be filled where one-to-one correspondence between goods sent for job work and goods received back after job work is not possible.

*****

Adv. D.J. Gaikwad Email: gaikwaddj77@gmail.com Address: Office No.01, Kalash Plaza, 3rd Lane, Advocate Colony, Near District Court. Sangli.416416

Disclaimer: Nothing contained in this document is to be construed as legal opinion or view of author whatsoever and the content is to be used strictly for informational and educational purposes. While due care has been taken in preparing this article, certain mistakes and omissions may creep in. The author does not accept any liability for any loss or damage of any kind arising out of any inaccurate or incomplete information in this article nor for any action taken in reliance thereon.

Author Bio

Material send for repair etc (Other than regular manufacturing related job work) also need to report or only job work related outward & inward.

Pl advise

Yes. It is applicable to goods sent for repair. The answer is based on below provided legal interpretation:

1. What is Job Work? :- As per Section 2(68) of CGST Act, 2017 “job work” means any treatment or process undertaken by a person on goods belonging to another registered person and the expression “job worker” shall be construed accordingly;

2. Section 143(1) specifies that a registered person may under intimation and subject to such conditions as may be prescribed, send any inputs or capital goods, without payment of tax, to a job worker for job work and(…..*)

3. Rule 45 (1) prescribes the conditions as “The inputs, semi-finished goods or capital goods shall be sent to the job worker under the cover of a challan issued by the principal, including where such goods are sent directly to a job-worker(….*)”

on combine reading of above stated references, it seems that the goods sent for repair are also covered under the above stated provisions. Although you have sent the goods for job work which is other than regular manufacturing job work, it is covered under the definitions of job work as stated above, which provides as ” “job work” means any treatment or process undertaken by a person on goods belonging to another registered person(…*).

It means any treatment undertaken on the goods sent by you will be construed as Job work and all the relevant provisions are applicable to your transaction.

Thank You.

Please Note the reply is solely based on interpretation of provisions referred above. It may be different from any other interpretation or view. You are advised to consult you legal adviser before using this information.

Very clear and perfect Sir. Thank you.