A) Definition

As per Notification-12/2017, Clause no-ze, Dt-28.06.17 (Central Tax Rate) a GTA is any person who provides service in relation to transportation of goods by road and issues a consignment note by whatever name called. Thus, it can be seen that issuance of a consignment note is an essential condition for a supplier of service to be considered as a Goods Transport Agency.

If such a consignment note is not issued by the transporter, the service provider will not come within the ambit of goods transport agency. If a consignment note is issued, it indicates that the lien on the goods has been transferred (to the transporter) and the transporter becomes responsible for the goods till its safe delivery to the consignee.

The use of the phrase ‘in relation to’ has extended the scope of the definition of GTA. It includes not only the actual transportation of goods, but any intermediate/ancillary service provided in relation to such transportation, like loading/unloading, packing/ unpacking, trans-shipment, temporary warehousing, etc. If these services are not provided as independent activities but are the means for successful provision of GTA Service, then they are also covered under GTA.

B) Position in GST

In terms of Notification- 12/2017-Central Tax (Rate) dated 28.06.2017 (Sr.no.18), the following services are exempt from GST

Services by way of transportation of goods (Heading 9965):

(a) by road except the services of:

(i) a goods transportation agency; (ii) a courier agency;

(b) by inland waterways.

Thus, it is to be seen that mere transportation of goods by road, unless it is a service rendered by a goods transportation agency, is exempt from GST.

Therefore, Individual Truck /Tempo Operators who do not issue a consignment note are also covered by above exemption.

C) Chargeability in GST

As per Notification No-13/2017-CGST(Rate)Dt-28.06.17, GTA was brought under the system of reverse charge tax mechanism where the whole of central tax leviable under section 9(3) of the CGST Act, shall be paid on reverse charge basis by the recipient of the such services. The Category of recipients who shall be liable to pay such tax under reverse charge basis has been discussed in Point-D below.

However, from 22nd Aug’2017 vide Notification-20/2017(CGST Rate) (Point No-iii) GTA has also been given the option to opt to pay GST in Forward Charge method “@6%CGST+6%SGST/UTGST=12%GST”. If the GTA opts for forward charge then it can claim ITC for the goods and services used in providing the GTA service.

Link: https://taxguru.in/goods-and-service-tax/cgst-reduction-rate-supplies-works-contract-services.html

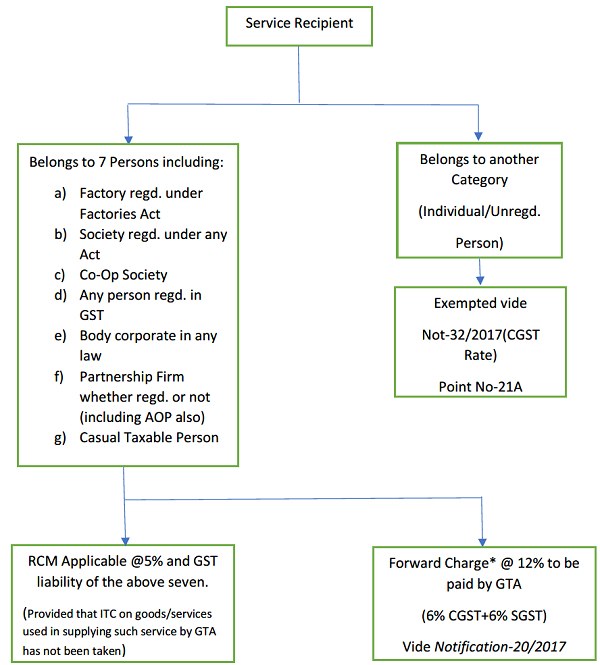

D) Steps to identify who is liable to pay GST in case of GTA Services

Step-1

Identify the service recipient.

It can be either the Consignor or the Consignee.

One who pays/is liable to pay the freight charges out of the above two will be considered as the service recipient. (Explanation “a” of the Notification No-13/2017-CGST(Rate))

https://taxguru.in/goods-and-service-tax/cgst-services-under-reverse-charge-mechanism.html

Step-2

Identify the category of service recipient:

Now, we will try to understand the above chart with the help of the Table below which talks about the “Person Liable to pay GST” in different scenarios

| Sl.

No |

Service Provider | Consignor | Consignee | Person liable to pay Freight | Person liable to pay GST |

| 1) | GTA | Company (Regd. or unregd) | Partnership Firm (Regd. or unregd) | Company | Company |

| 2) | GTA | Partnership Firm (Regd. or unregd) | Registered Dealer-Mr A | Mr A | Mr A |

| 3) | GTA | Partnership Firm (Regd. or unregd) | Registered Dealer-Mr A | Partnership Firm | Partnership Firm |

| 4) | GTA | Co-Op Society (Regd. or unregd) | Registered Dealer-Mr A | Mr A | Mr A |

| 5) | GTA | Co-Op Society (Regd. or unregd) | Registered Dealer-Mr A | Co-Op Society | Co-Op Society |

| 6) | GTA | Company-A (Regd or URD) | Company-B (Regd. or Unreg) | Company-B | Company-B |

| 7) | GTA | Unregd. Dealer-A | Regd. Dealer-Y | Unregd. Dealer-A | Exempt Supply** |

| 8) | GTA | Unregd. Dealer-A | Regd. Dealer-Y | Regd. Dealer-Y | Regd. Dealer-Y |

| 9) | GTA | Unregd. Dealer-A | Unregd. Dealer-B | Unregd. Dealer-B | Exempt Supply** |

| 10) | GTA(URD) | Company -C (Regd. or unregd) | Partnership Firm (Regd. or unregd) | Company-C | Company-C |

| 11) | GTA(URD) | Unregd. Dealer-A | Regd. Dealer-Y | Regd. Dealer-Y | Regd. Dealer-Y |

| 12) | GTA(URD) | Unregd. Dealer-A | Unregd. Dealer-B | Unregd. Dealer-B | Exempt Supply |

Note:

i) **Services provided by a GTA to an unregistered person other than the above seven entities shall be subjected to NIL Rate under GST and hence exempted. (As per Point No-c of Notification no-32/2017(CGST Rate),13.10.17 (Serial No-21A under Heading 9965))

ii) In case of Point no-10 & 11 Reverse Charge (As per Notification-13/2017-CGST Rate) will mandatorily apply and the option of forward charge will not be available as the GTA is unregistered. Point no -12 it will be covered by Notification no-32/2017(CGST Rate) and hence exempted.

iii) Also, for point no 1-9 it is assumed that the GTA has not opted the option of forward charge.

E) Place of Supply for Goods Transport Agency: Section 12(8)

a) If the supply is B2B then the Place of Supply will be the location of the Recipient

b) If the supply is B2C then the Place of Supply will be the location at which such goods are handed over their transportation.

F) GTA Services specifically Exempt

As per Notification-12/2017,Dt-28.06.17,(Central Tax Rate) the services provided by a GTA in respect of transport of following goods is exempt from payment of tax

1) Agricultural produce

2) Goods where the consideration charged is not more than 1500/- on a consignment in a single carriage

3) Goods where the consideration charged is not more than 750/- for a consignee for all such goods.

4) Milk, salt & Food grain including flour, pulses, rice.

5) Organic manure

6) Newspaper or magazines

7) Relief material for man-made disasters etc.

8) Defence or Military Equipment.

G) Conclusion

The above discussion shows that not all transport of goods by road is by a GTA. To qualify as services of GTA, the GTA should be necessarily issuing a consignment note. Only services provided by a GTA are taxable under GST. Services of transportation of goods by a person other than GTA are exempt. Moreover, in cases where the service of GTA is availed by the specified seven categories of persons in the taxable territory, the recipients who avail such services are the ones liable to pay GST and not the supplier of services unless the GTA opts for collecting and paying taxes @ 12% (6% CGST + 6% SGST). In all other cases where GTA service is availed by persons other than those seven specified such service will be exempt in GST. The GTA service supplier is not entitled to take ITC on input services availed by him if tax is being charged @ 5% (2.5% CGST + 2.5% SGST).

Author Bio

We are registered GTA,, and opted RCM. Now our concern is where do we need to show our turnover?

Dear sir,

Is GTA opt both reverse charge and forward charge mechanisam simultaneously. if not, then why and where it is mentioned, what is the procedure to opt, is any application is required to be filed for opting reverse charge or forward charge mechanism . waiting for your early response

Thanks

We got a GTA invoice without charging GST under RCM.

But GTA has paid 5% GST and the said bill is reflecting in our GSTR2A with GST.

Can we take the said GST which was paid by GTA as a ITC.Please advice.

Very good Article. only one thing is not clarified that if GTA needs to Opt for Forward Charge from Reverse Charge Mechanism, then from which date such option needs to be availed? is it mandatory to opt for such option from the beginning of the financial year?

Its very nicely written article but one confusion is there as we have observed that some truck owners having 5-10 trucks having attached their trucks with GTA (providing logistics services to corporate and charging 12% GST) are raising tax invoices and charging GST @ 12% on transportation bill with claiming input of Vehicle and expenses. Is this correct or wrong?

Vry nice article