Hello there, as we all know that GST has arrived and still there are various rumors and havoc regarding Invoicing under the GST regime. Through this post, I would like to share some important points regarding Invoicing.

1. There is “NO FORMAT PRESCRIBED”by the Government. Only a “FEW PARTICULARS”have been mandated in the format which is listed herein below –

- Serial number of tax invoice (serial number should not exceed 16 character and it should be consecutive serial number containing alphabets or numbers or special characters or any combination thereof, unique for a financial year);

- Name, address and GSTIN of the supplier;

- Date of issue of tax invoice;

- Name, address and GSTIN or UIN, if registered, of the recipient;

- Name and address of the recipient and the delivery address of the consignment, along with name of the State and State code, in case the recipient is unregistered person and the value of goods exceeds INR 50,000;

- Description of goods or services;

- HSN code of goods or Accounting code of services;

- Quantity of goods and units or unique quantity code needs to be mentioned correctly;

- Total value of supply of goods or services;

- Taxable value of supply of goods or services taking into account discount or abatement;

- Rate of tax i.e. central tax, state tax, integrated tax or union territory tax or cess;

- Amount of tax charged in respect of taxable goods or services (central tax, state tax, integrated tax or union territory tax or cess);

- In case of supply in the course of inter-state trade or commerce, place of supply along with name of the State and State Code has to be mentioned;

- In case delivery place is different from place of supply, address of the delivery needs to be mentioned;

- Whether tax is payable on reverse charge basis, has to be mentioned;

- Signature or Digital Signature of the supplier or the authorized representative.

2. There are mainly 3 types of Invoices under GST as:

- TAX INVOICE– For taxable supplies either within state or outside state and the person is required to collect and pay the the tax on such supplies.

- BILL OF SUPPLY– The supplies on which the person is not required to collect and pay the tax. These mainly comprise of ‘registered person supplying exempted goods or service or both’, ‘Composition Dealers’ and ‘Exporters’. Bill of Supply Format is give below.

- PAYMENT VOUCHER– This voucher is required to be issued when the tax is payable by the receiver of goods or services or both. It covers ‘Importers’ and ‘Reverse Charge Mechanism’ of paying taxes.

3. The manner of issuing Invoices in GST is as follows :-

- TAX INVOICE for Supply of Goods is to be issued in 3 copies as :

- Original Copy for the Recipient

- Duplicate Copy for the Transporter

- Triplicate Copy for the Supplier.

- TAX INVOICE for Supply of Services is to be issued in 2 copies as :

- Original Copy for the Recipient

- Duplicate Copy for the Supplier.

- BILL OF SUPPLY for both goods and services can be issued as:

- Original Copy for the Recipient

- Duplicate Copy for the Supplier.

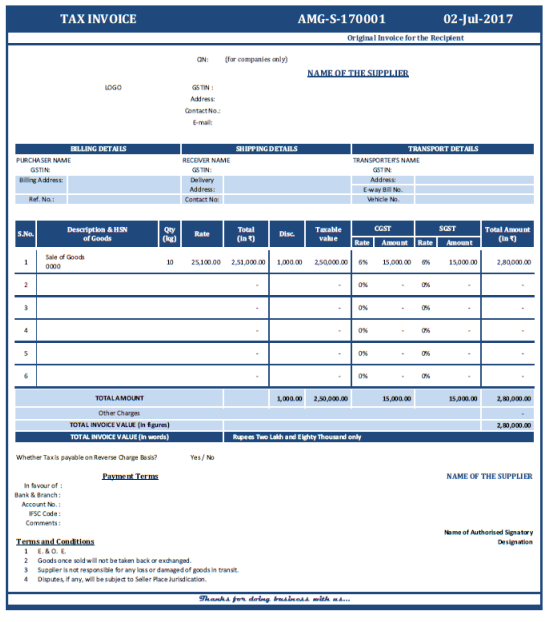

4. Format of TAX INVOICE under GST Regime for Local (State) Taxable Supply of Goods:-

5. Format of TAX INVOICE under GST Regime for Inter-State (National) Taxable Supply of Goods:-

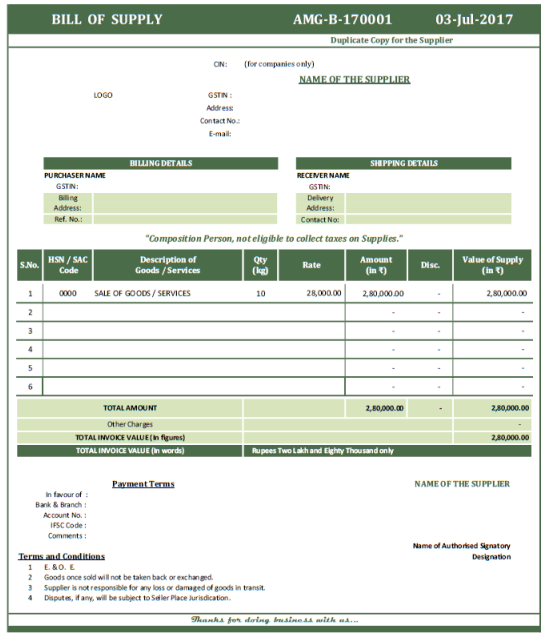

6. Format of BILL OF SUPPLY under GST Regime for Composition Dealers:-

In case of EXPORTERS, the declaration will read as follows: “SUPPLY MEANT FOR EXPORT ON PAYMENT OF INTEGRATED TAX” or “SUPPLY MEANT FOR EXPORT UNDER BOND OR LETTER OF UNDERTAKING WITHOUT PAYMENT OF INTEGRATED TAX”.

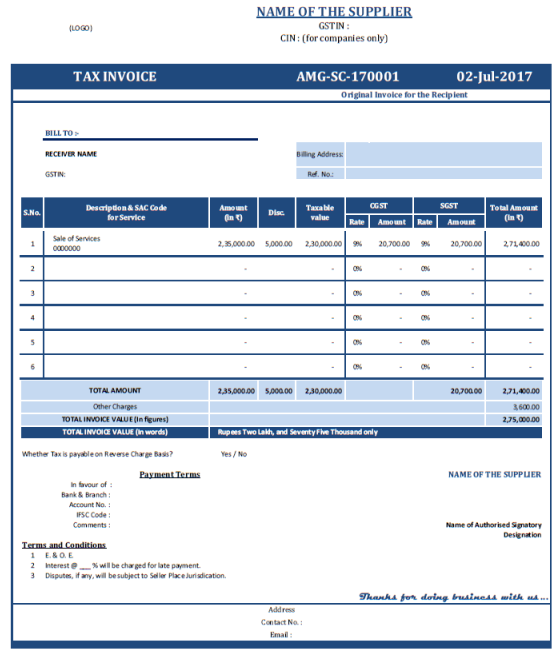

7. Format of TAX INVOICE under GST Regime for Local (State) Taxable Supply of Services :-

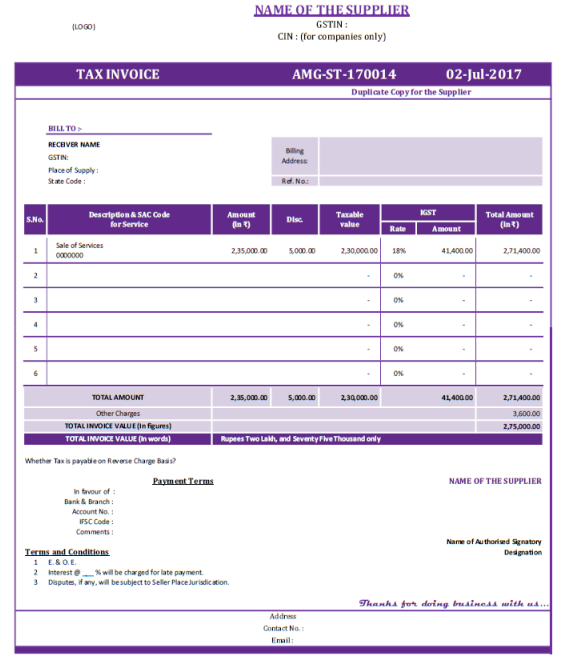

8. Format of TAX INVOICE for Inter-State (National) Taxable Supply of Services:-

9. HSN Codes in the invoices are to be shown as follows, referred in notification no. 12/2017 – central tax dated 28th June, 2017 :

- Turnover upto Rs. 1.50 Crore : Not Required

- Turnover more than Rs. 1.50 Crore up to Rs. 5.00 Crore : 2-digit Code (i.e. Chapter number only)

- Turnover more than Rs. 5 Crore : 4-digit Code (i.e. Chapter+Sub.Chapter)

(Republished With Amendments)

Author Bio