Page Contents

- A. FAQs on GST Registration by Input Service Distributor

- Q.1. Who are Input Service Distributors?

- Q.2. How do I obtain a registration as an Input Service Distributor?

- Q.3. Can ISD take multiple registrations in a State?

- Q.4. My place of business is not fixed. What should I mention in the Registration Application?

- Q.5. What document shall I need to upload in my Principal Place of business?

- Q.6. Which place will be my Principal place of business?

- Q.7. I have opened my shops at different locations on same PAN. Shall I need to apply separately for Registration?

- Q.8. Can an ISD opt for Composition?

- B. Manual on filing of GST Registration Application by Normal Taxpayer/ Composition/ Casual Taxable Person/ Input Service Distributor (ISD)/ SEZ Developer/ SEZ Unit

A. FAQs on GST Registration by Input Service Distributor

Q.1. Who are Input Service Distributors?

Ans. Input Service Distributor (ISD) under GST includes

♣ an office of the supplier of goods and / or services which

♣ receives tax invoices issued by the supplier towards receipt of input services and/ or goods and

♣ issues a prescribed document for the purposes of distributing the credit of CGST (SGST in State Acts) and / or IGST paid on the said services to a supplier of taxable goods and / or services having same PAN as that of the office referred to above.

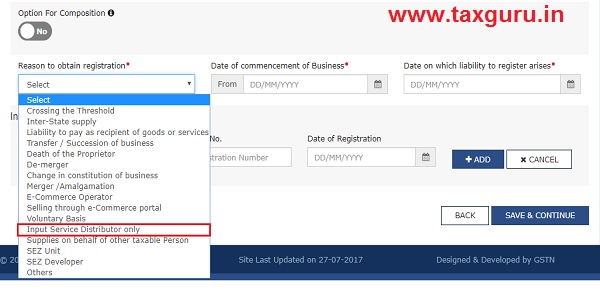

Q.2. How do I obtain a registration as an Input Service Distributor?

Ans. The registration for an Input Service Distributor can be applied through the New Registration Application of a normal taxpayer. All you need to do is select Input Service Distributor only under Reason to obtain registration in the Business Details section of PART B of the New Registration Application.

Please refer to screenshot below:

For other form-filling related queries, refer to the FAQs for New Registration Applications

Q.3. Can ISD take multiple registrations in a State?

Ans. ISD cannot take multiple registrations in a State.

Q.4. My place of business is not fixed. What should I mention in the Registration Application?

Ans. It is mandatory to provide Principal place of business in the application form, so you need to mention address of the place from where you are conducting your business. In case of any change, you can change the address by filing application for Amendment. However, the address can be changed only within the State.

Q.5. What document shall I need to upload in my Principal Place of business?

Ans.

| Proof of Principal Place of Business | |||

| Sr. No | Nature of possession of premises | Minimum No. of attachments | Proof of Principal Place of Business |

| 1. | Own | Any 1 attachment | Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

| 2. | Leased | Rent/ Lease agreement OR Rent receipt with NOC (In case of no/expired agreement) AND any 1 attachment | Rent/ Lease agreement OR Rent receipt with NOC (In case of no/expired agreement) AND Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

| 3. | Rented | Rent/ Lease agreement OR Rent receipt with NOC (In case of no/expired agreement) AND any 1 attachment | Rent/ Lease agreement OR Rent receipt with NOC (In case of no/expired agreement) AND Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

| 4. | Consent | Consent letter AND any 1 attachment | Consent letter AND Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

| 5. | Shared | Consent letter AND any 1 attachment | Consent letter AND Property Tax Receipt OR Municipal Khata copy OR Electricity bill copy OR Legal ownership document |

| 6. | Others | Legal ownership document | Legal ownership document |

Q.6. Which place will be my Principal place of business?

Ans. The primary location from where you are conducting your business will be your principal place of business.

Q.7. I have opened my shops at different locations on same PAN. Shall I need to apply separately for Registration?

Ans. If the additional places of business are in same state then you do not need to apply for registration separately. These additional places of business can be shown in the additional places of business tab while filling of the registration application. However, if the additional places of business are in different states then you need to apply for registrations separately for each state.

Q.8. Can an ISD opt for Composition?

Ans. ISD cannot opt for composition.

B. Manual on filing of GST Registration Application by Normal Taxpayer/ Composition/ Casual Taxable Person/ Input Service Distributor (ISD)/ SEZ Developer/ SEZ Unit

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.