With the implementation of GST, trade and exporters are eager to know how will our exports be treated under the Goods and Services Tax (GST) regime? In this article an attempt is made to guide step by step procedures for export under GST.

Universally the general moto is taxes should not be exported. In line with this in mind in the GST regime also exports are not made to tax. As GST is primarily a tax on consumption in India, it is not intended to apply to supplies that are not consumed in India, such as exports. Most exports are therefore GST-free provided certain conditions are met.

Exports & Imports : Treated as Deemed to be in the course of Inter State Trade or Commerce

As per Section 2(c) of IGST Act, 2016,

“Integrated Goods and Services Tax” (IGST) means tax levied under this Act on the supply of any goods and /or services in the course of inter State trade or commerce.

Explanation 1 – A supply of goods and/or services in the course of Import into the territory of India shall be deemed to be a supply of goods and/ or services in the course of inter-state trade or commerce.

Explanation 2 – An export of goods and / or services shall be deemed to be a supply of goods and/ or services in the course of inter-state trade or commerce.

From explanation 2 of the above section it is clear that Exports are Treated as Inter-State transaction and most of the provisions related to Exports are dealt in the IGST Act.

Definition of Exports :

Exports may be either Goods or Service or both and are defined as follows in the IGST Act.

Sec 2(5) of IGST Act : “export of goods” with its grammatical variations and cognate expressions, means taking goods out of India to a place outside India;

Sec 2(6) of IGST Act : “export of services” means the supply of any service when,––

(i) the supplier of service is located in India;

(ii) the recipient of service is located outside India;

(iii) the place of supply of service is outside India;

(iv) the payment for such service has been received by the supplier of service in convertible foreign exchange; and

(v) the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with Explanation 1 in section 8;

All Exporters Need to Register ??

Exports being inter-State supply, All Exporters would be required to obtain GST registration irrespective of threshold limit. (Sec 24 of CGST Act – Mandatory Registration). However, Importers and exporters of goods, that are exempted from GST, do not need to obtain a GST registration number and can clear their consignments by quoting PAN, the customs department said.

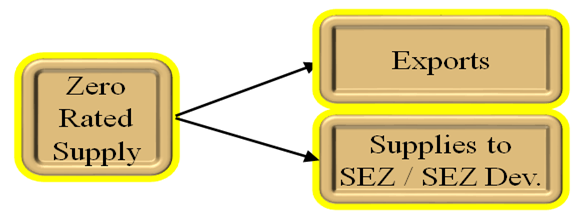

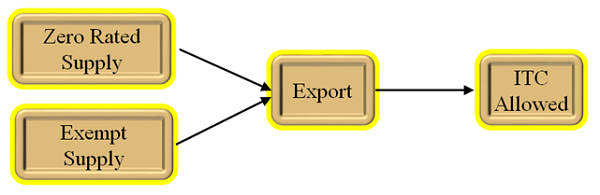

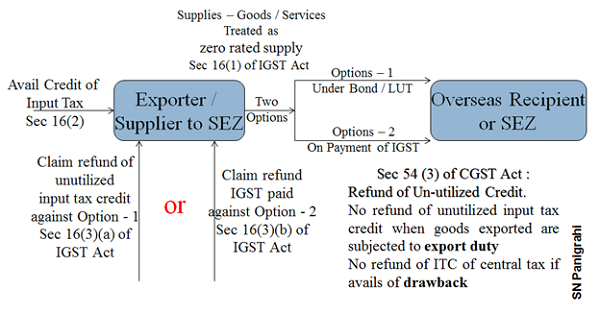

Exports – Considered as Zero-Rated Supply:

The export of Goods and Services is considered as Zero Rated Supply. GST will not be levied on exports. Zero-rated supply refers to items that are taxable, but the rate of tax is nil on their supplies and – credit of input tax relating to them can be availed.

As per Sec 2(23) of IGST Act: “zero-rated supply” shall have the meaning assigned to it in section 16;

Sec 16. (1) of IGST Act : “zero rated supply” means any of the following supplies of goods or services or both, namely:–

(a) export of goods or services or both; or

(b) supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit.

Zero-rated Supply – Input Tax Credit Allowed

Sec 16. (2) of IGST Act : Subject to the provisions of sub-section (5) of section 17 of the Central Goods and Services Tax Act, credit of input tax may be availed for making zero-rated supplies, notwithstanding that such supply may be an exempt supply.

Please note that ITC credit also allowed in case of Exempted supplies, when such items are exported.

Difference between Exempted Supplies & Zero Rated Supplies:

Exempt Supply :

As per Sec 2(47) of CGST Act: “exempt supply” means supply of any goods or services or both which attracts nil rate of tax or which may be wholly exempt from tax under section 11, or under section 6 of the Integrated Goods and Services Tax Act, and includes non-taxable supply;

There are three types of Exempted Supplies :

1. Nil Rate Supply : The Tariff Rate is Nil

2. Wholly Exempt from Tax – Through a Notification

3. Non- Taxable Supply – Not in GST like – Alcohol for human Consumption & Five Petroleum Products.

Difference between Exempted Supplies & Zero Rated Supplies

In case of exempted Supplies, since there is no tax charged on outward supply, the Input Tax Credit is not allowed. Whereas Zero-rated supply refers to items that are

taxable, but the rate of tax is nil on their supplies and

therefore, Input Tax Credit is allowed. However as per Sec 16. (2) of IGST Act, Input Tax Credit is allowed for Exempted items also when they are Exported.

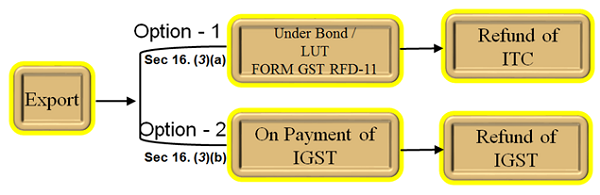

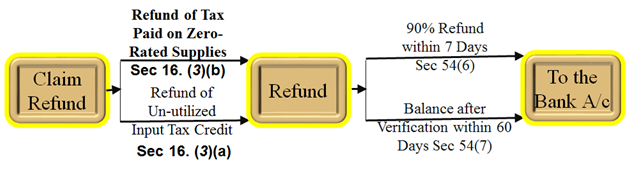

Zero Rated Supply – Refund of Un-utilized Input Tax Credit or Refund of IGST Paid on Such Exports

Exports can be made under Two Options

1. Option – 1 : Exports may be made under Bond or Letter of Undertaking without payment of integrated tax (IGST)

2. Option – 2 : Exports may also be done on payment of integrated tax

Refund of Credit

Sec 16. (3) of IGST Act : A registered person making zero rated supply shall be eligible to claim refund under either of the following options, namely:––

a) he may supply goods or services or both under bond or Letter of Undertaking, subject to such conditions, safeguards and procedure as may be prescribed, without payment of integrated tax and claim refund of unutilised input tax credit; or

b) he may supply goods or services or both, subject to such conditions, safeguards and procedure as may be prescribed, on payment of integrated tax and claim refund of such tax paid on goods or services or both supplied,

in accordance with the provisions of section 54 of the Central Goods and Services Tax Act or the rules made thereunder.

Accordingly, in case of Option -1 that is when exports are made without payment of tax under Bond or LUT the un-utilized credit can be claimed as refund. However when exports are made on payment of tax (IGST), the amount of IGST can be claimed as refund.

No Refund of Un-utilised Input Tax Credit in Certain Cases :

Sec 54(3) of CGST Act : Subject to the provisions of sub-section (10), a registered person may claim refund of any un-utilised input tax credit at the end of any tax period:

Provided that no refund of un-utilised input tax credit shall be allowed in cases other than–– zero rated supplies made without payment of tax;

Provided further that no refund of unutilised input tax credit shall be allowed in cases where the goods exported out of India are subjected to export duty:

Provided also that no refund of input tax credit shall be allowed, if the supplier of goods or services or both avails of drawback in respect of central tax or claims refund of the integrated tax paid on such supplies.

Means Refund of Un-utilized Credit is not allowed in the following cases :

1. When Export Supplies are subjected to export duty:

2. When Drawback is availed

3. When claims refund of the integrated tax paid on such supplies

Time Bound Refund

As per Sec 54(6) of CGST Act, Ninety per cent of the Total Amount so claimed shall be refunded on a Provisional basis.

Sec 54(7) of CGST Act : The proper officer shall issue the order under sub-section (5) within sixty days from the date of receipt of application complete in all respects.

Note : In case of refund not granted within 60 days from the date of making application & received acknowledgement for refund, interest is payable at the rate of 6% (Section 56 of CGST Act) – Notification No. 13/2017, 28th June, 2017

Please note that making of Refund Application is possible only after filling of Monthly Return GST – 3 or GST – 3B. Means until that time plus additional seven days the exporter should wait, and shouls carried with wrong notion of seven days from the exports.

Export Procedure

> The goods and services can be exported either on payment of IGST or under bond or Letter of Undertaking (LUT) without payment of IGST.

[Notification No. 16/2017-Central Tax, Circular Nos. 2/2/2017-GST and 4/4/2017-GST]

A) Export without payment of IGST & Refund Claim of Accumulated ITC

> As per Rule 96A of the Central Goods and Services Tax Rules, 2017 ( The CGST Rules), any registered person exporting goods or services without payment of integrated tax is required to furnish a bond or a Letter of Undertaking (LUT) in FORM GST RFD-11.

Furnishing of LUT & it’s Validity:

> Exporters who are eligible to export under LUT has been specified along with the conditions and safeguards in the Notification No. 16/2017-Central Tax dated 01-07-2017.

> The following registered person shall be eligible for submission of Letter of Undertaking in place of a bond:-

(a) a status holder as specified in paragraph 5 of the Foreign Trade Policy 2015-2020; or

(b) who has received the due foreign inward remittances amounting to a minimum of 10% of the export turnover, which should not be less than one crore rupees, in the preceding financial year,

and he has not been prosecuted for any offence under the Central Goods and Services Tax Act, 2017 (12 of 2017) or under any of the existing laws in case where the amount of tax evaded exceeds two hundred and fifty lakh rupees.

> The Letter of Undertaking shall be furnished in duplicate for a financial year in the annexure to FORM GST RFD – 11 referred to in sub-rule (1) of rule 96A of the Central Goods and Services Tax Rules, 2017 and it shall be executed by the working partner, the Managing Director or the Company Secretary or the proprietor or by a person duly authorised by such working partner or Board of Directors of such company or proprietor on the letter head of the registered person.

> Circular No. 26/2017- Customs dated 1st July, 2017 has clarified the procedure as prescribed under rule 96A. Format of LUT is prescribed in the Circular.

> Letter of Undertaking (LUT) shall be valid for 12 months

Furnishing of Bond:

> All exporters, not covered above under LUT would submit bond. The procedure for submission and acceptance of bond has been prescribed vide circular No. 2/2/2017-GSTdated 4 th July, 2017 & Circular No. 4/4/2017-GST, 7 th July, 2017.

> FORM RFD -11 under rule 96A of the CGST Rules requires furnishing a bank guarantee with bond. Field formations have requested for clarity on the amount of bank guarantee as a security for the bond.

> Running bond (separate bond for each consignment / export not required) will be required to cover amount of tax involved in export based on estimated tax liability as assessed by exporter.

> The bond shall be furnished on non-judicial stamp paper of the value as applicable in the State in which bond is being furnished.

> Jurisdictional Commissioner to decide amount of bank guarantee depending upon exporter’s track record

> No bank guarantee required if Commissioner is satisfied

> In any case the bank guarantee should normally not exceed 15% of the bond amount.

Bond / LUT to be submitted manually to jurisdictional Deputy/Assistant Commissioner, till module is available on portal

Exporter may furnish bond/LUT before Central Tax Authority or State Tax Authority till the administrative mechanism for assigning of tax payers to respective authority implemented

Exports may be allowed under existing LUTs/Bonds till 31st July 2017. Exporters shall submit the LUTs/bond in the revised format latest by 31st July, 2017.

Export Procedure for Refund Claim of Accumulated ITC

> In case of goods and services exported under bond or LUT, the exporter can claim refund of accumulated ITCon account of export – Rule 96 A: Refund of Input Tax Credit export of goods or services under bond or Letter of Undertaking.

> Any registered person availing the option to supply goods or services for export without payment of integrated tax shall furnish, prior to export, a bond or a Letter of Undertaking in FORM GST RFD-11 to the jurisdictional Commissioner, binding himself to pay the tax due along with the interest

> The exporter claiming refund of unutilized input tax credit will file an application electronically through the Common Portal, either directly or through a Facilitation Centre notified by the GST Commissioner. The application shall be accompanied by documents as prescribed in the said rules.

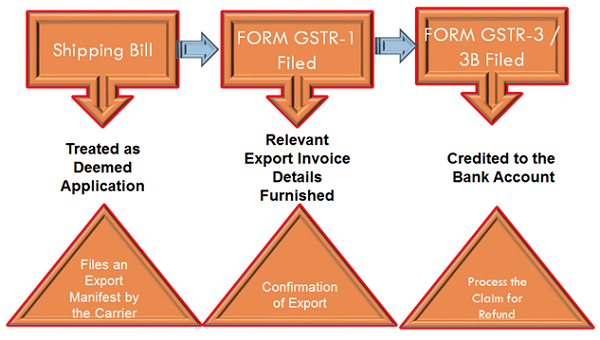

> Application for refund shall be filed only after the export manifest or an export report, as the case may be, is delivered under section 41 of the Customs Act, 1962 in respect of such goods.

> The details of the export invoices contained in FORM GSTR-1 furnished on the common portal shall be electronically transmitted to the system designated by Customs and a confirmation that the goods covered by the said invoices have been exported out of India shall be electronically transmitted to the common portal from the said system.

B) Export Procedure on Payment of IGST & Refund of IGST Paid

> In case of goods exported on payment of IGST, refund of IGST can be claimed after the goods have been exported –Rule 96 of CGST Rules : Refund of integrated tax paid on goods exported

> For Export of goods the shipping bill is the only document required to be filed with the Customs for making exports. Requirement of filing the ARE 1/ARE 2 has been done away with.

> The shipping bill filed by an exporter shall be deemed to be an application for refund of integrated tax paid on the goods exported out of India and such application shall be deemed to have been filed only after submission of export general manifest and furnishing of a valid return in Form GSTR-3 by the applicant.

> The details of the relevant export invoices contained in FORM GSTR-1 shall be transmitted electronically by the common portal to the system designated by the Customs and the said system shall electronically transmit to the common portal, a confirmation that the goods covered by the said invoices have been exported out of India.

> Upon the receipt of the information regarding the furnishing of a valid return in FORM GSTR-3 from the common portal, the system designated by the Customs shall process the claim for refund and an amount equal to the integrated tax paid in respect of each shipping bill or bill of export shall be electronically credited to the bank account of the applicantmentioned in his registration particulars and as intimated to the Customs authorities.

> Refund procedure shall as a consequence come into operation only when the registrants file the above mentioned returns.

Sealing of Export Containers:

> Circular No. 26/2017-Customs; Dt : 1st July, 2017

> For the sake of uniformity and ease of doing business, Board has decided to simplify the procedure relating to factory stuffing hitherto carried out under the supervision of the Central Excise officers. It is the endeavor of the Board to create a trust based environment where compliance in accordance with the extant laws is ensured by strengthening Risk Management System and Intelligence setup of the department. Accordingly, Board has decided to lay down a simplified procedure for stuffing and sealing of export goods in containers.

> It has been decided to do away with the sealing of containers with export goods by CBEC officials. Self-sealing procedure shall be followed The concept of merchant or manufacturer exporter would become irrelevant under the GST regime. The procedure in respect of the supplies made for export is same for both merchant exporter and a manufacturer exporter.

> Any exporter desirous of availing self-sealing procedure shall inform the jurisdictional Custom Officer of the rank of Superintendent or Appraiser of Customs, at least 15 days before the first planned movement of a consignment. This is a onetime exercise.

> Self-Sealing permission once given by a Principal Commissioner/Commissioner of Customs shall be valid for export at all the customs stations.

> The exporter shall seal the container with the tamper proof electronic-seal of standard specification. The electronic seal should have a unique number which should be declared in the Shipping Bill. Before sealing the container, the exporter shall feed the data such as name of the exporter, IEC code, GSTIN number, description of the goods, tax invoice number, name of the authorized signatory (for affixing the e-seal) and Shipping Bill number in the electronic seal.

> Thereafter, container shall be sealed with the same electronic seal before leaving the premises.

> The exporter intending to clear export goods on self-clearance (without employing a Customs Broker) shall file the Shipping Bill under digital signature.

> Board has decided that the above revised procedure regarding sealing of containers shall be effective from 01.09.2017.

> Therefore, as a measure of facilitation, the existing practice of sealing the container with a bottle seal under Central Excise supervision or otherwise would continue till 01st September, 2017.

Filling of Shipping Bill :

> Quoting GSTIN in Shipping bill is mandatory if the export product attracts GST for domestic clearance.

> Quoting PAN (Permanent Account Number), which is authorized as Import Export code by DGFT, would suffice if the exporter exclusively deals with products which are either wholly exempt from GST or out of GST regime.

> In case of exports by specialized agencies such as United Nations Organization or notified Multilateral Financial Institutions, Embassies and Consulates, the exporter can quote Unique Identity Number, instead of GSTIN, in the Shipping bill.

> Without GSTIN or PAN or UIN, the Shipping bill cannot be filed.

> The claim for refund of IGST paid or Input Tax Credit on inputs consumed in goods exported cannot be processed without GSTIN and GST Invoice details in Shipping Bill.

> Commercial Invoice information should be provided in the Shipping Bill. Wherever Commercial Invoice is different from Tax Invoice, details of both have to be provided in the Shipping Bill.

> Taxable value and Tax amount should be mentioned against each item in the Shipping bill for processing the refund amount. Multiple tax invoices issued by same GSTIN holder are allowed in one Shipping bill for the same consignee.

> State code is part of GSTIN numbering scheme. However, in the Shipping Bill for the field “State of origin” declare the State code from where export goods originated as it was being done before.

Export of Goods to Nepal and Bhutan Treated as Zero Rated and Qualify for all the Export Benefits

Export of goods to Nepal or Bhutan fulfills the condition of GST Law regarding taking goods out of India. Hence, export of goods to Nepal and Bhutan will be treated as zero orated and consequently will also qualify for all the benefits available to zero rated supplies under the GST regime irrespective of the fact that export realization is received in Indian Currency. However, the definition of ‘export of services’ in the GST Law requires that the payment for such services should have been received by the supplier of services in convertible foreign exchange.

(Author can be reached at snpanigrahi@rediffmail.com)

Author Bio

Factory stuffing container – physically container reached at our factory dated 20/04/2020 but can we prepared GST Tax invoice dated 19/04/2020 (with payment of IGST) for shipping bill preparation/filling. & E-seal report.

Sir, please clear me that what would be the State of Origin to put when an Exporter of Assam procure the export meterial from Gujrata ?

Dear sir, I have a doubt, can you please quote the section or notification where it is written that export to Nepal or Bhutan can be realized in Indian currency and further the section which says that for other countries realisation of export proceed is only in foreign exchange. For service it is in IGST Act itself I definition it is clearly mentioned that the proceeds must be in foreign exchange. I shall be grateful for your help in this regard.

Thanking you…Gokulesh

actually we had exports in august and september against LUT (without payment of tax).

Mistakenly, when we were entering data online on the portal, we also entered our export liability as IGST in table 3.1(b).

It also got settled through our ITC.

Now what should we do to get refunds ?

whether we shall file 6A with payment of tax ?

DEAR SIR,

EXPORT OF GOODS TO NEPAL TREATED AS ZERO RATED SHOULD WE HAVE TO CHARGE IGST TAX IF WE DONT OPT BOND OR LUT. PLEASE GIVE YOUR KIND ADVISE. THANKS IN ADVANCE.

I require Letter format for applying to Customs for getting permisison for factory container stuffing under self sealing under gst regime. Thanks and regards

Exhaustively covered. Thanks!

Hi..

We are exporting Rice from India to Saudi Arabia. There is No GST applicable on Rice.. However There is 18% GST on Packing material like Bags. Please advise if exporter need to pay 18% GST on Bags to manufacturer and same will be refund by GST department or any other procedure.

Sir,

It’s one of the best article about Export procedure under GST. I’m in confuse to submit bond for services too? because we were providing medical transcription services to USA Hospitals. Request you to clarify the same..

In case of export of services there will be no export manifest. So is the following clause applicable: “Application for refund shall be filed only after the export manifest or an export report, as the case may be, is delivered under section 41 of the Customs Act, 1962 in respect of such goods.”

sir

before GST regime we would to mention one consolidated commercial invoice in shipping bill for 6 excise tax invoices along with ARE -1 .

Since ARE -1 have been subsumed in GST tax invoice so where should we fill up the details of tax invoice in shipping bill as there is no prescribed column in shipping bill for the same .

Good Article

In case of export under LUT(RFD-11) Can we avail ITC refunds plus DBK(custom portion only) B

OR

DUTY DRAWBACK -A

Good Article.

In case of supply of goods under LUT (RFD-11) Can we avail

ITC Refund Plus Drawback (only custom portion)

or

Duty drawback benefit.

Hello Sir,

very Good Information,

Sir, If we export services with zero rated but we have not given LOU or Bond then we won’t get ITC and/or refund of ITC. Is that correct?

I am asking this for freelancers. All freelancers provide Software or outsourcing services but they won’t incurred much expenses to claim ITC so if they ready to loose ITC then they no need to provide LOU or Bond right? and they can provide zero rated only right?

Hi Panigrahi,

Thanks for the wonderful post. Could you please tell about the procedure for the export of services by payment of IGST without opting Bond/LUT.

The Article is very good and very much helpful. Thank you sir.

The article is very much helpful. Thanks a lot for nice presentation.