The present article is an attempt to explain the concept of e-invoice, how it will operate. It is expected that the document will also be useful for the taxpayers, tax consultants and the software companies to adopt the designed standard.

Is e-invoicing a system wherein taxpayers need to generate the invoices centrally or will the invoice generated using the accounting software or PoS machines will now be E-Invoices.? Many questions persist in minds of readers.

To bring a clarity, readers may take a note that a myth is hovering in the air that invoice shall now be generated from the govt’s tax portal. However, e-invoice is not at all a mechanism of generation of invoices from a central portal of tax department, as such a mechanism will bring numerous restrictions to the way business is conducted. The direct creation or generation of e-invoice from GST portal or any other govt’s portal is not at all envisaged in the e-invoicing concept.

As a matter of fact, every taxpayer has it’s own requirements which cannot be met using a single software. Therefore, various accounting/billing software are being used to meet the invoicing requirements. However, they can’t be understood by another computer software system. Say an invoice generated in SAP cannot be read by a system using Tally. Hence a need was felt to standardize the format in which electronic data of an invoice will be shared with others to ensure interoperability of the data. This need led to the concept of what we today call as e-invoicing.

Without wasting much of the time in the history and geography of the concept, let us move to the steps to be undertaken in order to comply with this law:

Page Contents

Flow of the e-invoice generation, registration and receipt of confirmation

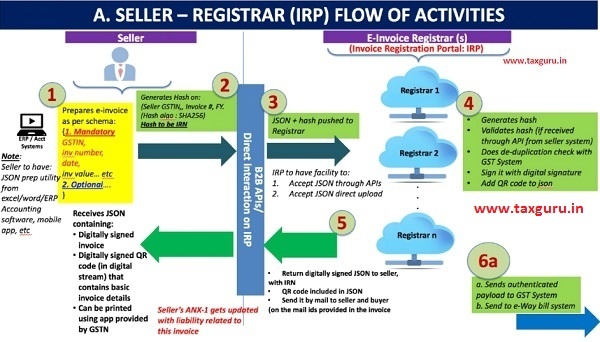

The flow of the e-invoice generation, registration and receipt of confirmation can be logically divided into two major parts.

1. The first part being the interaction between the business (supplier in case of invoice) and the Invoice Registration Portal (IRP).

2. The second part is the interaction between the IRP and the GST/E-Way Bill System.

Part A. Flow from Supplier (commonly known as seller) to IRP

Step 1: The seller shall generate the invoice in same manner as it was being done earlier. However, this time he needs to ensure that the invoice contains all the necessary parameters that have been published earlier under e-invoice schema [Readers may refer to https://www.gstn.org/e-invoice/ for detailed schema].

Step 2: The supplier needs to ensure that the billing software has been upgraded, such that it is capable to generate JSON of the invoice to upload it to the IRP. The IRP will only take JSON of the e-invoice.

Note: The small and medium size taxpayers (having annual turnover below Rs 1.5 Crores) can avail accounting and billing system being offered by GSTN free of cost.

Step 3: The seller shall upload the JSON on the IRP. The JSON may be uploaded directly on the IRP or through GSPs or through third party provided apps.

The same has been explained through the help of the attached diagram.

Part B. Flow from IRP to GSTN System and E-way Bill Portal

IRP will generate a hash based on seller’s GSTIN, document type, document no. and F.Y and verify the hash from the Central Registry of GST System to ensure that the same document (invoice etc.) from the same supplier pertaining to same year is not being uploaded again. On receipt of confirmation from Central Registry, IRP will add its signature on the invoice data and a QR code to the JSON. The QR code will contain GSTIN of seller and buyer, invoice number, invoice date, number of line items, HSN of major commodity contained in the invoice as per value, hash etc.

The hash computed by IRP will become the IRN (Invoice Reference Number) of the e-invoice. This shall be unique to each invoice for the entire financial year in the entire GST System for a taxpayer.

The digitally signed JSON with IRN will be transferred to the seller along with the QR code and the said details then will be automatically uploaded on the GSTN Portal and the E-Way Bill portal. The GST system will update the details in ANX-1 of the seller and ANX-2 of the buyer, which will in turn determine the tax liability and ITC.

The e-invoice schema includes parameters e.g. ‘Transporter Id’ and ‘Vehicle Number’ for creating and generating e-way bills. The seller shall only enter the transporter code and the vehicle number (if available with him) at the time of generation of e-invoice. In that case, the E-Way bill system will accordingly create e-way bill using this data.

Note: It is important to ensure that mandatory fields of the invoice are filled in before generating JSON. The e-invoice shall not be accepted in the GST System unless all the mandatory items are present

Small taxpayers can use one of the eight free accounting/billing software currently listed by GSTN. Also, the GSTN will provide offline tools wherein the invoice data will be manually entered, and the tool will generate the JSON. Also, the taxpayers can use third party accounting software for doing this.

Certain Features of E-invoicing under GST:

1. Format of IRN: IRN will be based on hash of GSTIN of generator of document (invoice or credit note or debit note), financial year, document type and document number.

2. Digital signature by IRP: The IRP after ensuring that the hash is unique to the invoice, will digitally sign it which will then make it a valid e-invoice for the seller and the buyer. The IRP will also push this signed e-invoice to the GST and the E-Way bill systems.

3. QR Code: The seller will be returned a signed JSON with all details including a QR code. The QR code will consist of the following e-invoice parameters: a) GSTIN of supplier; b) GSTIN of Recipient; c)Invoice number; d) Date of generation of invoice; e) Invoice value (taxable value and gross tax); f) Number of line items; g) HSN Code of main item (the line item having highest taxable value); h) Unique Invoice Reference Number (hash).

4. Multiple Registrar for IRN System: Multiple registrars (IRPs) will be put in place to ensure 24X7 operations without any break. To start with, NIC will be the first Registrar. GST System will also provide IRP services in due course of time.

5. Standardization of e-Invoice: The e-invoice schema and template as approved by the GST Council, are available at https://www.gstn.org/e-invoice/. The same has been notified by the Govt of India vide Notification No. 02/2020 dated 01st Jan 2020.

Modes of creating e-invoice under GST

Multiple modes will be made available so that taxpayer can use the best mode based on his/her need. The modes given below are envisaged at this stage under the proposed system for e-invoice, through the IRP (Invoice Registration Portal):

1. Web based,

2. API based,

3. Mobile app based,

4. offline tool based and

5. GSP based

Printing of Invoice under GST

The businesses will receive a signed JSON from the IRP. This payload can be received, converted to readable format and populated into a PDF file. The taxpayer can then print his paper invoice.

Cancellation of e-invoice under GST

The seller can upload the IRN of the e-invoice already reported, if that invoice has been cancelled by him/her. The cancellation of an invoice will be done by using the ‘Cancel IRN’ API (published on the e-invoice portal).

Amendment of e-invoice under GST

The amendment of e-invoice already uploaded on IRP will be done only on GST portal. Any amended e-invoice, if reported to IRP, will get rejected as its IRN (unique hash) will be already be existing in the IRP system. Hence amendment of invoices will not be possible through the IRP.

Disclaimer: The views, expressions, opinion is solely an interpretation of the author and does not assures of the correctness of interpretation. The author reserves the right not to be responsible for the topicality, correctness, completeness or quality of the information provided above in this article.

Author Bio