Detailed Analysis of Proposals made by GST Council vide 45th GST Council Meeting

1.0 Background of 45th GST Council Meeting:

The GST Council inorder to reduce rates on certain products and provide some trade facilitation measures on account of 3rd wave of COVID – 19 which is expected to be outbreaking soon. The 45th GST Council meeting was highly requested from trade & industry to announce relief measures & reducing rates of certain products in view of COVID – 19 & Black Fungus.

The discussion of meetings has been highlighted in below paras.

2.0 Analysis of GST Council Meeting Highlights – Legal Updates & Rate Cut Proposals: –

2.1 TRADE FACILITATION MEASURES

[1] Reduction in frequency to file ITC 04

Requirement of filing FORM GST ITC-04 under rule 45 (3) of the CGST Rules has been relaxed as under:

Taxpayers whose annual aggregate turnover in preceding financial year is above Rs. 5 crores shall furnish ITC-04 once in six months;

a) Taxpayers whose annual aggregate turnover in preceding financial year is above Rs. 5 crores shall furnish ITC-04 semi-annually.

b) Taxpayers whose annual aggregate turnover in preceding financial year is upto Rs. 5 crores shall furnish ITC-04 annually

Analysis:

(i) GST ITC – 04: Job Worker: In view of trade facilitation, the said amendment has been carried out. This amendment relaxes compliance burden to a certain extent. The GST ITC 04 is to be furnished by registered person sending goods for job – working under cover of delivery challan.

(ii) Meaning of Aggregate Turnover: It shall be noted that, the annual aggregate turnover shall be taken of preceding financial year of PRINCIPAL. Following are the components to be added in aggregate turnover: –

| Provision | Aggregate Turnover means aggregate of: | Provision | Aggregate Turnover excludes |

| Section 2(6) of CGST Act | Value of all taxable supplies

(Excluding the value of inward supplies on which tax is payable by a person on reverse charge basis) |

Section 2(6) of CGST Act | Central tax, State tax, Union territory tax, integrated tax and cess

|

| Exempt Supplies (Non-GST, Nil Rated & Wholly exempted supplies) |

|||

| Exports of goods or services or both | |||

| Inter-State supplies of persons having the same Permanent Account Number. | |||

| To be computed on all India basis |

(iii) Here a person may argue in case of newly formed business that, in preceding F.Y., since the turnover was less than 5 crores (basically 0), thus, he has to file annually, instead of semi-annually. The drafting should have provided “financial year or preceding” instead of just preceding financial year, so that proper information can be received by department.

[2] Ineligible Credit “availed and utilised” – Interest to be charged @ 18%, w.r.e.f. 1st July, 2017

Press Release Extract: In the spirit of earlier council decision that interest is to be charged only in respect of net cash liability, Section 50 (3) of the CGST Act to be amended retrospectively, w.e.f. 01.07.2017, to provide that interest is to be paid by a taxpayer on “ineligible ITC availed and utilized” and not on “ineligible ITC availed”. It has also been decided that interest in such cases should be charged on ineligible ITC availed and utilized at 18% w.e.f. 01.07.2017.

Notes:

1. As per prevalent section 50(3) of CGST Act, “A taxable person who makes an undue or excess claim of input tax credit under subsection (10) of section 42 or undue or excess reduction in output tax liability under subsection (10) of section 43, shall pay interest on such undue or excess claim or on such undue or excess reduction, as the case may be, at such rate not exceeding twenty-four per cent., as may be notified by the Government on the recommendations of the Council.”

2. Government has amended section 50(1) to provide interest on net cash liability, on the similar lines, government has confirmed upcoming amendment in section 50(3). The interest would only be levied on such amount of input tax credit which is availed and utilised (not on just availment) @ 18% p.a.

3. In other words, if a taxpayer has wrongly availed ineligible ITC and has the balance in electronic credit ledger equivalent to such extent, it may be inferred that no interest would be charged on the same. The matter of concern arises whether, government would treat balance left in electronic credit ledger on FIFO basis of invoice date or whether it will allow non-levy of interest provided amount equivalent to ineligible ITC is lying in electronic credit ledger.

4. It can be further noted that, government seem to make the change retrospectively, giving a room to taxpayers who have paid interest already @ 24% on ITC claimed in excess. The refund shall be allowed to such tax payers so as to maintain parity between them.

5. It can be analysed from wordings that, if a taxpayer avails ineligible ITC, and reverses before utilisation, no interest would be levied.

[3] Unutilised Cash Balances of CGST & IGST – Transfer between distinct persons of different states:

Press Release Extract: Unutilized balance in CGST and IGST cash ledger may be allowed to be transferred between distinct persons (entities having same PAN but registered in different states), without going through the refund procedure, subject to certain safeguards.

Notes:

1. It is very important to note that government has only considered wordings in press release as “entities having same PAN but registered in different state”, however a person can be a distinct person if it has 2 different registrations in same state for 2 different place of businesses as per Rule 11 of CGST Rules.

2. This is a welcomed change, which will reduce the compliance of filing application for refund on tax payers.

[4] Circulars to be issued in respect of various matters:

Clarification on scope of “intermediary services

Government has just said that, it will issue a circular on intermediary scope. Let us analyse why such circular is needed: –

As per section 2(13) of IGST Act, “intermediary” means a broker, an agent or any other person, by whatever name called, who arranges or facilitates the supply of goods or services or both, or securities, between two or more persons, but does not include a person who supplies such goods or services or both or securities on his own account.

The intermediary was always a burning issue before department and tax payers, in respect of refund claims as one of the condition as mentioned in section 2(6) of IGST Act is not fulfilled i.e., Place of supply. As per section 13(8) of IGST Act, where supplier or recipient are located outside India, the place of supply in case of intermediary services shall be location of supplier of services (contradicting to destination principle).

The footprints of Intermediary can be traced back to 2012, wherein government has issued Education Guide on Taxation of Services, 2012 wherein it provides for who is an Intermediary & place of supply aspects. As per said guide following are key notes in resect of intermediary services: –

(a) Nature & Value: An intermediary cannot alter the nature or value of the service, the supply of which he facilitates on behalf of his principal, although the principal may authorize the intermediary to negotiate a different price

(b) Separation of Value: Separation of value: The value of an intermediary’s service is invariably identifiable from the main supply of service that he is arranging. It can be based on an agreed percentage of the sale or purchase price. Generally, the amount charged by an agent from his principal is referred to as “commission”

And such other parameters.

(ii) Clarification relating to interpretation of the term “merely establishment of distinct person” in condition (v) of the Section 2 (6) of the IGST Act 2017 for export of services.

Press Release Extract: A person incorporated in India under the Companies Act, 2013 and a person incorporated under the laws of any other country are to be treated as separate legal entities and would not be barred by the condition (v) of the sub-section (6) of the section 2 of the IGST Act 2017 for considering a supply of service as export of services

Notes:

1. There are in totality, the 5 conditions for an activity to regard it as export of services. One of the said 5 conditions is the parties should not be merely establishment of distinct persons.

2. As per Explanation 2 to section 8 of IGST Act, “A person carrying on a business through a branch or an agency or a representational office in any territory shall be treated as having an establishment in that territory.”.

3. It would be worth to note that, if an entity is located in 2 different countries and have been incorporated under two different laws, then such entities are not be treated as “mere establishment of distinct persons”. Further, holding companies and subsidiary companies are also not treated as distinct persons.

4. Further, it is pertinent to note that, if condition (v) is not fulfilled the said services would be exempt supplies in light of Notification 9/2017 – IT(R).

(iii) Clarification in respect of Debit Note – Delinking:

Press Release Extract: W.e.f. 01.01.2021, the date of issuance of debit note (and not the date of underlying invoice) shall determine the relevant financial year for the purpose of section 16(4) of CGST Act, 2017.

Analysis:

Government has already delinked ITC availment time-limit vide NN 92/2020 w.e.f. 1st January, 2021, however, concerns arose, that whether such delinking would be applicable on underlying invoice issued after 1.01.2021 or debit note issued after 1.01.2021, it is hereby recommended to consider “debit note date” as relevant date.

Delinking of Invoice date w.r.t. Debit note [Notification No. 92/2020, dt. 22-12-2020 w.e.f. 1st January, 2021]: Prior to 1st January, 2021; the ITC in respect of debit note was restricted upto the credit restriction date of tax invoice. However, w.e.f. 1st January, 2021; debit note has been given independent time limit for availment of input tax credit. Below example would make it clearer: –

| Scenario | Invoice Date | Debit Note Date | Due date to file 3B of September | Date of filing annual return | Upto when credit can be taken in respect of debit note |

| Prior to 1st January, 2021 | 1-8-2019 | 5-11-2020 | 20th October, 2020 (Linked to Invoice) |

25th November, 2020 | 20th October, 2020

(Thus, ITC of debit note cannot be taken) |

| After 1st January, 2021 | 1-8-2020 | 5-11-2021 | 20th October, 2022

(Linked to Debit note) |

25th November, 2022 | 20th October, 2022

(Thus, ITC of debit note can be taken) |

| (Note: There is no time limit to issue debit note) | |||||

Other procedural areas:

(a) There is no need to carry the physical copy of tax invoice in cases where invoice has been generated by the supplier in the manner prescribed under rule 48(4) of the CGST Rules, 2017;

(b) Only those goods which are actually subjected to export duty i.e., on which some export duty has to be paid at the time of export, will be covered under the restriction imposed under section 54(3) of CGST Act, 2017 from availment of refund of accumulated ITC.

(c) Provision to be incorporated in in CGST Rules, 2017 for removing ambiguity regarding procedure and time limit for filing refund of tax wrongfully paid as specified in section 77(1) of the CGST/SGST Act and section 19(1) of the IGST Act.

2.2 MEASURES STREAMLINING COMPLIANCES IN GST:

1. Aadhaar authentication of registration to be made mandatory for being eligible for filing refund claim and application for revocation of cancellation of registration.

2. Late fee for delayed filing of FORM GSTR-1 to be auto-populated and collected in next open return in FORM GSTR-3B.

3. Refund to be disbursed in the bank account, which is linked with same PAN on which registration has been obtained under GST.

4. Rule 59(6) of the CGST Rules to be amended with effect from 01.01.2022 to provide that a registered person shall not be allowed to furnish FORM GSTR-1, if he has not furnished the return in FORM GSTR-3B for the preceding month.

5. Rule 36(4) of CGST Rules, 2017 to be amended, once the proposed clause (aa) of section 16(2) of CGST Act, 2017 is notified, to restrict availment of ITC in respect of invoices/ debit notes, to the extent the details of such invoices/ debit notes are furnished by the supplier in FORM GSTR-1/ IFF and are communicated to the registered person in FORM GSTR-2B.

2.3 CHANGES IN RATE OF TAX AND SERVICE EXEMPTIONS (Only relevant are covered)

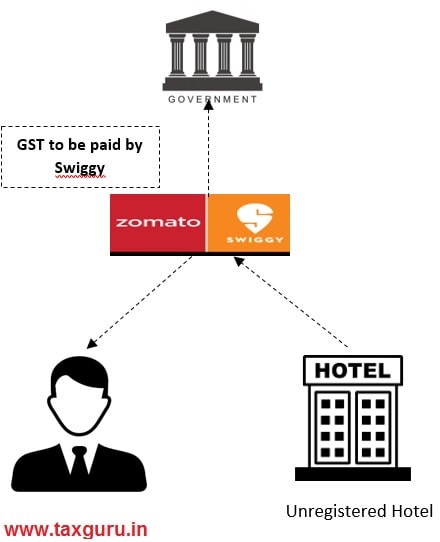

1. ECOMMERCE OPERATORS:

E Commerce Operators are being made liable to pay tax on following services provided through them

(i) transport of passengers, by any type of motor vehicles through it [w.e.f. 1st January, 2022]

(ii) restaurant services provided through it with some exceptions [w.e.f. 1st January, 2022]

Analysis:

(i) Passenger Transport services: Till now, the passenger transportation services through e – commerce operator vide Radio Taxi, “maxicab”, “motorcab” and “motor cycle” were covered, however, from now, Government is intending to cover transport of passengers by any type of motor vehicle.

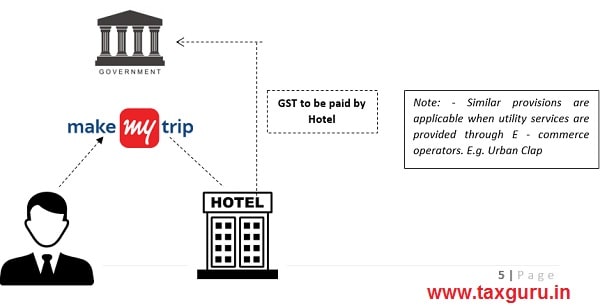

(ii) Restaurant services:

PRESENT SCENARIO:

CASE WHERE HOTEL BOOKED THROUGH MAKE MY TRIP IS REGISTERED UNDER GST

CASE WHERE HOTEL BOOKED THROUGH MAKE MY TRIP IS REGISTERED UNDER GST

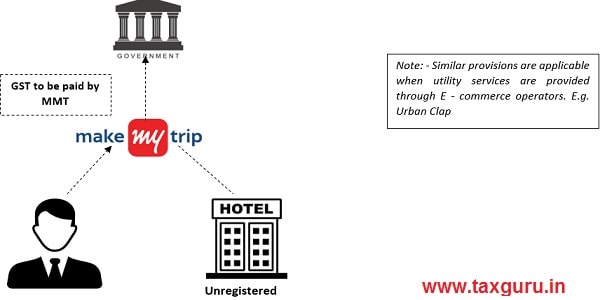

PROBABLE SCENARIO:

CASE WHERE HOTEL BOOKED THROUGH MAKE MY TRIP IS NOT REGISTERED UNDER GST

Admission to amusement parks having rides etc. attracts GST rate of 18%. The GST rate of 28% applies only to admission to such facilities that have casinos etc.

2.4 CHANGES IN RATE OF TAX OF GOODS AND EXEMPTIONS (Only relevant are covered)

(i) URP OF MENTHA OIL – RCM, EXPORTS ONLY UNDER LUT: Supply of Mentha oil from unregistered person has been brought under reverse charge u/s 9(4). Further, Council has also recommended that exports of Mentha oil should be allowed only against LUT and consequential refund of input tax credit.

(ii) BRICKS – COMPOSITION SCHEME W.E.F 1ST APRIL, 2022 [6% WITHOUT ITC, 12% WITH ITC]: Brick kilns would be brought under special composition scheme with threshold limit of Rs. 20 lakhs, with effect from 1.4.2022. Bricks would attract GST at the rate of 6% without ITC under the scheme. GST rate of 12% with ITC would otherwise apply to bricks.

(iii) PETROLEUM PRODUCTS WOULD BE OUT OF AMBIT AS OF NOW: In terms of the recent directions of the Hon’ble High Court of Kerala, the issue of whether specified petroleum products should be brought within the ambit of GST was placed for consideration before the Council. After due deliberation, the Council was of the view that it is not appropriate to do so at this stage.

(iv) COMPENSATION CESS COLLECTION EXHAUSTED TO REPAY BORROWINGS TO BRIDGE GAP OF 2020-21 & 2021-22: On the issue of compensation scenario, a presentation was made to the Council wherein it was brought out that the revenue collections from Compensation Cess in the period beyond June 2022 till April 2026 would be exhausted in repayment of borrowings and debt servicing made to bridge the gap in 2020-21 and 2021-22.

(v) REDUCTION & INCREASE IN RATE OF GST [PENS TO 18%(FROM 12%/18%), PHARMA PRODUCTS TO 12% (FROM 18%)]

GST Council has recommended reduction in rate of tax as well as increase in rate of tax of several products. In case of reduction of rate of tax, will give rise to accumulation of credit, however government has denied refund vide Circular 135/05/2020 – GST. The businesses need to visit section 14 of CGST Act, which covers scenarios in relation to change in rate of taxes.

(vi) EXTENSION OF REDUCTION RATE TO 31ST DECEMBER IN REGARDS TO COVID RELATED ITEMS: Extension of existing concessional GST rates (currently valid till 30th September, 2021) on following Covid-19 treatment drugs, up to 31st December, 2021, namely: –

(i) Amphotericin B -nil

(ii) Remdesivir – 5%

(iii) Tocilizumab -nil

(iv) Anti-coagulants like Heparin – 5%

(vii) NEW ITEMS ADDED IN REDUCED RATE – COVID:

Reduction of GST rate to 5% on more Covid-19 treatment drugs, up to 31st December, 2021,

(i) Itolizumab

(ii) Posaconazole

(iii) Infliximab

(iv) Favipiravir

(v) Casirivimab & Imdevimab

(vi) 2-Deoxy-D-Glucose

(vii) Bamlanivimab & Etesevimab

sir, Iron ore rate increased to 18% from 5% from which date it will be applicable

From which date RCM on purchase of Mentha oil from unregistered dealer will be applicable.

Very good explanation. Thank u sir.

Thank you for your comment sir.