Articles related to How to claim Refund Amount of Excess balance available in Electronic Credit Ledger? (Under utilization of IGST, CGST, SGST)

We export of goods & services under bond/LUT without payment of IGST and total credit available for the purchase of goods & services are not fully utilized for payment of CGST, SGST, IGST henceforth whatever credit available in our electronic credit ledger account how to claim the refund on it are discussed here:

First, before filing of the refund claim manually let’s understand:

(1) What is RFD 01 A form?

(2) How to calculate Refund amount (Unutilized credit of IGST, CGST, SGST)?

– Meaning of Taxable Turnover of Zero-rated supply of goods or services.

– Meaning of Net Input Tax credit & Adjusted Total Turnover

(3) Which are the documents to be submitted at the time of manual submission refund claim?

(1) What is RFD 01 A Form

Ans: RFD 01 A form of Refund of Input Tax Credit on Export of Goods & Services without Payment of Integrated Tax (export under Bond/Letter of undertaking).

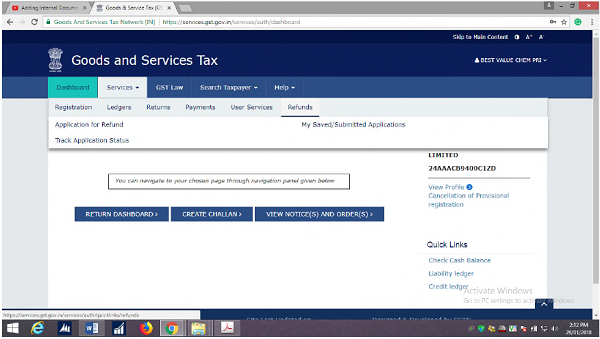

Online form available on gst.gov.in website.

Click on Services menu ——> Refunds ——> Application for Refund —–> Fill Up Refund of ITC on Export of Goods & Services without Payment of Integrated Tax

(2) How to calculate Refund amount (Unutilized credit of IGST, CGST, SGST)?

Ans: Refund of ITC on Export of Goods and Services without payment of Integrated Tax – Goods are sold under bond or letter of an undertaking as well as unutilization of IGST, CGST, SGST credit amount mention as under:

Step to be followed while calculating Refund Amount:

(1) Computation of Refund claimed as per statement 3A on which mention Turnover of zero-rated supply of goods and services

(2) Net Input Tax credit

(3) Adjusted Total Turnover

Computation of Refund claimed (Statement 3A)

Meaning of Taxable Turnover of Zero-rated supply of goods or services.

Turnover of zero-rated supply of goods means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or Letter of Undertaking.

At the time of calculating Turnover of zero-rated supply of goods – goods which were sold under rebate claim total turnover of that goods should be excluded because of goods which were export under rebate claim for that purpose separate procedure to be followed.

Turnover of zero-rated supply of services means a value of zero-rated supply of services made without payment of tax under bond or Letter of an undertaking.

Meaning of Net Input Tax credit & Adjusted Total Turnover.

Net Input Tax Credit: Input tax credit available during the month. (credit which was availed during the month are taken to be considered). Input Tax credit of IGST, CGST, SGST are availed during the month separately disclosed in the online form of RFD 01 at the time of Filing.

Adjusted total Turnover: Adjusted total turnover inclusive of Domestic Turnover + Zero rated supply (Export Turnover) – exempt supplies.

Turnover means the aggregate value of all taxable supplies (exclude inward supplies on which tax is payable by a person on reverse charge

Domestic Turnover: Turnover of all goods are sold in interstate and intrastate transaction.

Zero rate supply: Turnover of export goods under bond as well as a rebate.

AMOUNT ELIGIBLE FOR REFUND CLAIM:

The Lower amount of comparison of all 3 should be eligible for taking Refund Amount.

The Value which was derived as per statement of 3A is compared with Balance available in Electronic Credit Ledger and Tax credit availed during the period. Once comparison was complete than lowest refund amount would be eligible for Refund.

Value as per Statement 3A: calculation already made in above

Balance in Electronic Credit ledger: Balance which is available in electronic ledger credit account at the time of submission of form RFD 01A.

Tax Credit availed during the period: If we apply for refund claim file for the month of Sept 2017 than total credit availed during that month should be taken.

(3) Which are the documents to be submitted at the time of manual submission refund claim?

Ans: Following Documents to be attached at the time when manually submission for taking Refund Claim.

a. Copy of duly online filed GST RFD 01 A Form

b. Acknowledgement copy (ARN) for online submission of form RFD 01A

c. Electronic credit register showing Debit amount of refund claim

d. Annexures (As per Statement of 3 & 5 of RFD 01)

e. Copies of an issue of all Taxable invoices of export of services / Bank Realization certificate in case of export of service.

f. Copies of all Taxable invoices, Shipping Bill, Bill of Export, BRC and summary of invoices pertaining to zero-rated supplies (export of goods without payment of IGST & export of goods with payment of IGST).

g. Copies of invoices pertaining to inward supply (purchases) on which tax credit has been availed during the month along with a summary of invoices.

h. Invoices copy and summary statement for Domestic Sales.

i. Copy of duly filed GSTR – 3B for respective month

j. Copy of duly filed GSTR -1 for respective month

k. Declaration under the 2ndproviso to section 54(3) export of goods is not subject to export duty.

l. Declaration under the 3rd proviso to section 54(3) no drawback in respect of central tax has been claimed/shall be claimed or no refund of IGST paid on supplies has been claimed.

m. Declaration under section 54(3) declares ITC availed on the goods or services used for making “Nil” rated/ exempted supplies has not been included in the refund of ITC claim.

n. Declaration related to claimants have not contravened to Rule 91(1) and incidence of tax has not passed to any other person as per rule 89(2)(1).

o. Cancelled cheque of bank (Bank on which refund amount will be deposit)

RFD 01A online filed form along with all above mention documents submitted to the respective jurisdictional officer. Once all documents submitted successfully than the departmental officer issue provisional order of Refund claim as per Form RFD 04 and Payment Advice as per Form RFD 05.

RFD 04 provisional refund order issued by officer of central jurisdiction along with the signature, date & place. RFD 04 form details mention as under:

| Sr No | Description | Central Tax | State/UT Tax | Integrated Tax | Cess |

| i | Amount of Refund Claimed | ***** | ***** | ***** | ***** |

| I (a) | Corrected Amount of refund claimed | ***** | ***** | ***** | ***** |

| ii | 10% of the amount at i(a) claimed as refund (to be sanctioned later) | ***** | ***** | ***** | ***** |

| iii | Balance Amount (i(a)-ii) | ***** | ***** | ***** | ***** |

| iv | Amount of Refund sanctioned | ***** | ***** | ***** | ***** |

Total Amount of Refund claimed to disclose amount which was already mentioned in Acknowledgement copy of RFD 01.

90% of the Total Amount of Refund Claimed approved by the department and mention in a corrected amount of refund claimed.

10% of Total Amount of Refund claim release after completion of final sanction of refund order.

Bank Details also mention in Provisional Refund Order as per below format:

| v | Bank Account No. as per application | ********** |

| vi. | Name of the Bank | ********** |

| vii. | Address of the Bank/Branch | ********** |

| viii. | IFSC code no of Bank | ********** |

| ix. | MICR code | ********** |

RFD 05 Payment Advice issued by the department in that separately disclosed all details of (IGST/CGST/SGST) amount related to Refund (as per sanction order).

Provisional Refund Order (RFD 04) and Payment Advice (RFD 05) both are issued at the same time by the Officer of Central Jurisdiction.

All CGST, SGST, IGST Refund claim amount sanction by the Central Jurisdiction location where your premises fall but for taking refund claim of SGST amount provisional refund order copy submitted to the respective state jurisdiction & state officer will release SGST amount of refund claim while CGST, IGST refund claim release & receivable from central jurisdictional officer.

Disclaimer: The contents of this document are solely for informational purpose. It does not constitute professional advice. Neither the authors accept any liabilities for any loss or damage of any kind arising out of any information in this document nor for any actions taken in reliance thereon.

I want to know if we want to file refund 18-19 ,19-20,20-21 in inverted tax structure but in credit ledger balance is nill in 18-19 ,19-20,20-21, but in 21-22 balnce is available then can we file for refund

I want to know if we want to file refund 18-19 ,19-20,20-21 in inverted tax structure but in credit ledger balance is nill in 18-19 ,19-20,20-21, but in 21-22 balnce is available then can we file for refund

Dear Sir,

I wanted to know that Net ITC means ITC availed as per GSTR-3B i.e. inclusive of capital goods

sir,

we have excess balance in electronic credit ledger for 2017-18 financial year appx. more than 15 Lakhs including IGST CGST AND SGST, where as in our case input tax rate is 18% and output tax rate is 12%, there by out input tax gets accumulates, so please guide me how to apply for refund of excess credit in electronic credit ledger.

I am to surrender GST, has filed for Refund. All the amounts in the cash ledger IGST, CGST, SGST have been made to refund.

Now i have ITC pending in Electronic Credit Ledger of amount Rs. 644/-, how can i get this amount.

Dear Sir,

To get refund of ITC available in the electronic credit ledger in terms of IGST,CGST and SGST, Can we cear the goods by paying IGST and also CGST and SGST since the IGST available is not sufficient ?

Dear Sir,

We have IGST,CGST and SGST credits in the electronic cash ledgers.i want to know while exporting can I pay IGST and also CGST and sgst since the available credit of IGST is enough ?so that can i get refund of these amounts on completion of Export ?

sir kindly guide on following points

1) Net ITC means as per GSTR 3B (i.e. after ITC Reversed As per Rule 42 & 43 of CGST/SGST rules ) and

2) in Statement- 3 [rule 89(2)(b) and 89(2)(c)]

Refund Type:Export without payment of tax (accumulated ITC) there is no direct link available for Shipping for some Expenses like Professional fees, raw material / stores & spares used for mfg,others office exp. than how we claim refund in this statement.

Sir, My query is that if we purchased the goods in the month of Dec 2017 and Input was declared in GSTR3 but exported the same goods in the month of Jan 2018 under LUT(Zero Rated). and in the month of Jan 2018 there is no purchase and no input tax credit available,what amount of refund we will get for the goods exported in Jan 2018

All issue covered in one related to refund very nic