CBEC PRESS RELEASE

GST on Telecom Services

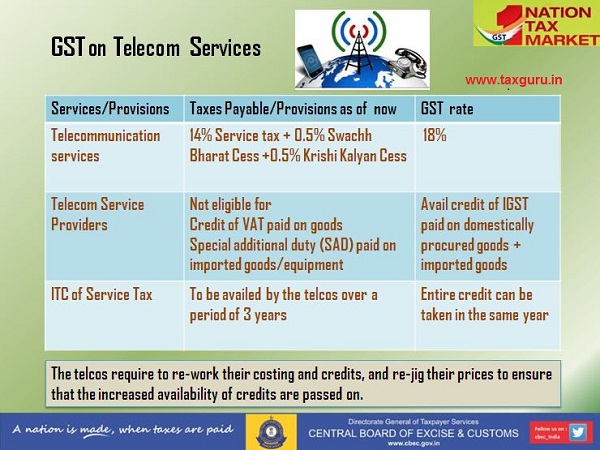

Telecommunication services presently attract service tax of 14% along with Swachh Bharat Cess (SBC) of 0.5% and Krishi Kalyan Cess (KKC) of 0.5%. While service tax is a pure value added tax, the above mentioned cesses are not. This is for the reason that while no ITC (input tax credit) of SBC is available, the ITC of KKC is allowed to be set off only against KKC. Therefore, both the cesses are turnover tax.

2. As against the above, the telecommunication services will attract GST of 18% in the GST regime, which is a pure value added tax because full ITC of inputs and input services used in the course or furtherance of business by the telecommunication service provider would be available.

3. Moreover, presently telecom service providers are neither eligible for credit of VAT paid on goods nor of special additional duty (SAD) paid on imported goods/ equipment. However, under GST, telecom service providers would avail credit of IGST paid on domestically procured goods as also imported goods. As per some estimates, this additional input tax credit would be as much as 2% of the turnover of the telecom industry. Further, ITC of service tax paid on assignment of spectrum by the Government in 2016 is presently allowed to be availed of by the telcos over a period of 3 years. In the GST regime, the entire credit can be taken in the same year. Resultantly, the balance two-thirds credit of the previous year would be admissible in the current financial year itself. All of these would reduce the telcos liability to pay GST through cash to about 87% of what they paid in the last fiscal.

4. Thus, the telcos are required to re-work their costing and credits availability and re-jig their prices and ensure that the increased availability of credits is passed on to the customers by lowering their costs.